Impact of Forensic Accounting on Corporate Governance in Retail

VerifiedAdded on 2023/06/12

|22

|5642

|374

Report

AI Summary

This report provides a conceptual and theoretical analysis of forensic accounting within Australian retail corporations, focusing on its role in detecting and preventing fraudulent activities. The study examines the impact of forensic accounting on internal corporate governance, highlighting its importance in addressing issues like insolvency, data leakage, and intellectual property theft. It discusses the limitations of traditional auditing methods and emphasizes the need for professional skepticism in identifying financial discrepancies. The research aims to identify the types of fraudulent activities, assess the effectiveness of forensic accounting in fraud prevention, and investigate the challenges faced by firms due to financial misconduct. Ultimately, the report seeks to provide recommendations for improving forensic accounting practices and mitigating financial risks within retail corporations, using a mixed-methods approach for data collection and analysis.

Running head: FORENSIC ACCOUNTING

Impact of Forensic Accounting on Organisation

Name of the Student:

Name of the University:

Author Note:

Impact of Forensic Accounting on Organisation

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FORENSIC ACCOUNTING

Executive Summary

The study focuses on the conceptual and theoretical analysis of the forensic accounting in the

retail corporations in Australia. The retail sectors often experience a collapsing situation that

includes the date of insolvency, unauthorized leakage of commercially sensitive information, and

theft of intellectual properties. The research study intends to evaluate the extent to which the

forensic accounting helps in aiding the diverse fraudulent activities and influencing the internal

corporate governance process.

The audit profession indicates that the management ensures a chief accountability for

recognizing and preventing the fraudulent business concerns. The effective forensic accounting

procedures help in understanding the method of motivating the employees to maintain the high

level of integrity. Forensic accounting process ensures that the field of the corporate governance

takes the active participation in mitigating the emerging risks within the organisation.

The study discusses the appropriate design and data collection process for investigating the

major aspects of the research area. The use of the mixed method approach is suitable for this

study. Considering the techniques of primary and secondary data, the study will develop the

concerned ideas about the subject matter.

FORENSIC ACCOUNTING

Executive Summary

The study focuses on the conceptual and theoretical analysis of the forensic accounting in the

retail corporations in Australia. The retail sectors often experience a collapsing situation that

includes the date of insolvency, unauthorized leakage of commercially sensitive information, and

theft of intellectual properties. The research study intends to evaluate the extent to which the

forensic accounting helps in aiding the diverse fraudulent activities and influencing the internal

corporate governance process.

The audit profession indicates that the management ensures a chief accountability for

recognizing and preventing the fraudulent business concerns. The effective forensic accounting

procedures help in understanding the method of motivating the employees to maintain the high

level of integrity. Forensic accounting process ensures that the field of the corporate governance

takes the active participation in mitigating the emerging risks within the organisation.

The study discusses the appropriate design and data collection process for investigating the

major aspects of the research area. The use of the mixed method approach is suitable for this

study. Considering the techniques of primary and secondary data, the study will develop the

concerned ideas about the subject matter.

2

FORENSIC ACCOUNTING

Table of Contents

1.0 Introduction................................................................................................................................4

1.1 Background of the Research......................................................................................................4

1.2 Problem Statement.....................................................................................................................5

1.3 Research Aim.............................................................................................................................6

1.4 Research Objectives...................................................................................................................6

1.5 Research Questions....................................................................................................................7

2.0 Literature Review......................................................................................................................7

2.1 Concept of Forensic Accounting...............................................................................................8

2.2 Conceptual Analysis of ‘Fraud’...............................................................................................10

2.3 Corruption and Fraud in Australian Corporations...................................................................10

2.4 Impact of Forensic Accounting in Detecting the Frauds.........................................................12

2.5 Financial Accounting Benefits in providing the connected link.............................................13

2.6 Effectiveness of the Forensic Accounting on Improving Corporate Governance...................13

2.7 Article relevancy with the literature........................................................................................14

2.8 Gap in the literature.................................................................................................................15

3.0 Research Methodology............................................................................................................16

3.1 Research Type.........................................................................................................................16

3.2 Research Approach..................................................................................................................16

3.3 Data Collection Type...............................................................................................................17

3.4 Sampling..................................................................................................................................17

3.5 Data Analysis...........................................................................................................................18

3.6 Ethical Concerns......................................................................................................................18

FORENSIC ACCOUNTING

Table of Contents

1.0 Introduction................................................................................................................................4

1.1 Background of the Research......................................................................................................4

1.2 Problem Statement.....................................................................................................................5

1.3 Research Aim.............................................................................................................................6

1.4 Research Objectives...................................................................................................................6

1.5 Research Questions....................................................................................................................7

2.0 Literature Review......................................................................................................................7

2.1 Concept of Forensic Accounting...............................................................................................8

2.2 Conceptual Analysis of ‘Fraud’...............................................................................................10

2.3 Corruption and Fraud in Australian Corporations...................................................................10

2.4 Impact of Forensic Accounting in Detecting the Frauds.........................................................12

2.5 Financial Accounting Benefits in providing the connected link.............................................13

2.6 Effectiveness of the Forensic Accounting on Improving Corporate Governance...................13

2.7 Article relevancy with the literature........................................................................................14

2.8 Gap in the literature.................................................................................................................15

3.0 Research Methodology............................................................................................................16

3.1 Research Type.........................................................................................................................16

3.2 Research Approach..................................................................................................................16

3.3 Data Collection Type...............................................................................................................17

3.4 Sampling..................................................................................................................................17

3.5 Data Analysis...........................................................................................................................18

3.6 Ethical Concerns......................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FORENSIC ACCOUNTING

References......................................................................................................................................19

FORENSIC ACCOUNTING

References......................................................................................................................................19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FORENSIC ACCOUNTING

1.0 Introduction

The current business world has been facing the considerable challenges from the

fraudulent activities and numerous scandals in every industry. The forensic accounting is a

terminology that deals with the accounting, investigation, and auditing skills to examine the

financial statement of the company. With the help of a structured forensic accounting document,

a company can present the proof to the court if any fraudulent act is suspected. According to

Seda and Kramer (2015), it is important for each organisation to investigate the fraud and

corruption, which are the significant elements of the role of a forensic accountant. In addition to

this, forensic accounting even deals with several mismanagements occur within the organisation.

The study will thus focus on the conceptual and theoretical analysis of the forensic accounting in

the retail corporations in Australia. The identification of the research aim, objectives, and

research questions will be connected to the findings obtained from the literature. The use of the

appropriate methodologies will also be discussed in this study to gather the insightful knowledge

on this context.

1.1 Background of the Research

The current business scenario is widely surrounded by the extensive competition. Each of

the organisations strives to achieve excellence and strengthen the competitive position. Louwers

(2015) identified that this entire business arena has been experiencing the continuous frauds and

scandals regularly. Forensic accounting is a practice that audits the internal financial statements

of a firm to identify the loopholes and undertake the fruitful steps to mitigate the issues. Bhasin

(2017) even defined that forensic accounting generally uses the different accounting skills that

are effective enough to conduct an investigative act against the fraudulent activities underlying

FORENSIC ACCOUNTING

1.0 Introduction

The current business world has been facing the considerable challenges from the

fraudulent activities and numerous scandals in every industry. The forensic accounting is a

terminology that deals with the accounting, investigation, and auditing skills to examine the

financial statement of the company. With the help of a structured forensic accounting document,

a company can present the proof to the court if any fraudulent act is suspected. According to

Seda and Kramer (2015), it is important for each organisation to investigate the fraud and

corruption, which are the significant elements of the role of a forensic accountant. In addition to

this, forensic accounting even deals with several mismanagements occur within the organisation.

The study will thus focus on the conceptual and theoretical analysis of the forensic accounting in

the retail corporations in Australia. The identification of the research aim, objectives, and

research questions will be connected to the findings obtained from the literature. The use of the

appropriate methodologies will also be discussed in this study to gather the insightful knowledge

on this context.

1.1 Background of the Research

The current business scenario is widely surrounded by the extensive competition. Each of

the organisations strives to achieve excellence and strengthen the competitive position. Louwers

(2015) identified that this entire business arena has been experiencing the continuous frauds and

scandals regularly. Forensic accounting is a practice that audits the internal financial statements

of a firm to identify the loopholes and undertake the fruitful steps to mitigate the issues. Bhasin

(2017) even defined that forensic accounting generally uses the different accounting skills that

are effective enough to conduct an investigative act against the fraudulent activities underlying

5

FORENSIC ACCOUNTING

the organisational functions. The report acts as the proof for the fraudulent activities that can be

shown to the court or any legal proceeding. It has been observed that the retail corporations face

such discrepancy in their financial activities on a regular basis. Bhasin (2015) observed that the

retail sectors often experience a collapsing situation that includes the date of insolvency,

unauthorized leakage of commercially sensitive information, and theft of intellectual properties.

In fact, in some of the cases, it is also observed that the retail corporations fail to comply with the

regulatory governance, such as Competition and Consumer Act 2010 (Bologna and Shaw,

2013). The development of the forensic auditing process would be helpful in such case to

identify the discrepancy and take the action against it to mitigate the challenges quickly.

1.2 Problem Statement

The research study is entirely concentrating on exploring the conceptual and theoretical

underpinning related to the forensic accounting system. The research study is focusing on

critically examine the recognizable impacts of the forensic accounting process for addressing and

resolving the fraudulent activities within the retail firms. The observation of this examination

report would suggest the appropriate corporate governance process that can be undertaken to

mitigate the challenges in a significant manner. The research study intends to evaluate the extent

to which the forensic accounting helps in aiding the diverse fraudulent activities and influencing

the internal corporate governance process. Botes, and Saadeh (2016) implied that the external

auditing credibility generally depends on the techniques and procedures undertaken by different

countries. This analysis even involves with numerous criticisms directed by the external

activities. Such financial scams cause the lack of integrity among the public that leads towards

property losses, which is a greater concerns for the business.

FORENSIC ACCOUNTING

the organisational functions. The report acts as the proof for the fraudulent activities that can be

shown to the court or any legal proceeding. It has been observed that the retail corporations face

such discrepancy in their financial activities on a regular basis. Bhasin (2015) observed that the

retail sectors often experience a collapsing situation that includes the date of insolvency,

unauthorized leakage of commercially sensitive information, and theft of intellectual properties.

In fact, in some of the cases, it is also observed that the retail corporations fail to comply with the

regulatory governance, such as Competition and Consumer Act 2010 (Bologna and Shaw,

2013). The development of the forensic auditing process would be helpful in such case to

identify the discrepancy and take the action against it to mitigate the challenges quickly.

1.2 Problem Statement

The research study is entirely concentrating on exploring the conceptual and theoretical

underpinning related to the forensic accounting system. The research study is focusing on

critically examine the recognizable impacts of the forensic accounting process for addressing and

resolving the fraudulent activities within the retail firms. The observation of this examination

report would suggest the appropriate corporate governance process that can be undertaken to

mitigate the challenges in a significant manner. The research study intends to evaluate the extent

to which the forensic accounting helps in aiding the diverse fraudulent activities and influencing

the internal corporate governance process. Botes, and Saadeh (2016) implied that the external

auditing credibility generally depends on the techniques and procedures undertaken by different

countries. This analysis even involves with numerous criticisms directed by the external

activities. Such financial scams cause the lack of integrity among the public that leads towards

property losses, which is a greater concerns for the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FORENSIC ACCOUNTING

On the other hand, Crain et al. (2016) argued that the transaction volumes enlarge the

corporation size, which affects the external audit accountability. It is essential to present the

appropriate financial statement to create a fair view of the financial reporting. This practices

helps in detecting the probable frauds by drifting an external audit. The audit profession indicates

that the management ensures a chief accountability for recognizing and preventing the fraudulent

business concerns. It is important to develop the professional skepticism while identifying the

frauds thorough the internal audit process (DiGabriele and Huber, 2015). The prevalent frauds

may create the materially incorrect financial pronouncements. The accountant and legal

practitioners may receive the fruitful insights by reviewing the failures in the various statutory

and audit procedures that are generally used for detecting or preventing frauds. The study is thus

concentrating on analyzing the issues with the financial losses and increasing rate of the

fraudulent activities. The study even intends to identify the effectiveness of forensic accounting

process to mitigate the challenges due to such inappropriateness in the financial accounting

systems of the retail corporations.

1.3 Research Aim

The research study aims to identify the fruitfulness of the forensic accounting process to

detect the internal fraudulent financial concerns within the retail corporations. The study also

attempts to identify the challenges faced due to the financial frauds take place within the

organisations and effects of these challenges to maintain the appropriate corporate governance.

1.4 Research Objectives

To identify the types of fraudulent activities and discrepancies within the retail

corporations

FORENSIC ACCOUNTING

On the other hand, Crain et al. (2016) argued that the transaction volumes enlarge the

corporation size, which affects the external audit accountability. It is essential to present the

appropriate financial statement to create a fair view of the financial reporting. This practices

helps in detecting the probable frauds by drifting an external audit. The audit profession indicates

that the management ensures a chief accountability for recognizing and preventing the fraudulent

business concerns. It is important to develop the professional skepticism while identifying the

frauds thorough the internal audit process (DiGabriele and Huber, 2015). The prevalent frauds

may create the materially incorrect financial pronouncements. The accountant and legal

practitioners may receive the fruitful insights by reviewing the failures in the various statutory

and audit procedures that are generally used for detecting or preventing frauds. The study is thus

concentrating on analyzing the issues with the financial losses and increasing rate of the

fraudulent activities. The study even intends to identify the effectiveness of forensic accounting

process to mitigate the challenges due to such inappropriateness in the financial accounting

systems of the retail corporations.

1.3 Research Aim

The research study aims to identify the fruitfulness of the forensic accounting process to

detect the internal fraudulent financial concerns within the retail corporations. The study also

attempts to identify the challenges faced due to the financial frauds take place within the

organisations and effects of these challenges to maintain the appropriate corporate governance.

1.4 Research Objectives

To identify the types of fraudulent activities and discrepancies within the retail

corporations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FORENSIC ACCOUNTING

To critically examine the effectiveness of forensic accounting process to detect or

prevent the internal financial frauds

To investigate the challenges faced by the firms due to the external and internal

fraudulent financial concerns

To provide the preferable recommendations to mitigate the challenges with the Forensic

Accounting planning within the retail corporations

1.5 Research Questions

How the forensic accounting system helps in addressing and managing the financial

frauds in retail corporations?

To what extent the forensic accounting system becomes obligatory to undertake the audit

process for developing sound corporate governance?

What are the major challenges faced due to the emergence of the financial frauds within

the corporation?

How these challenges can be mitigated by using the appropriate forensic accounting

process?

2.0 Literature Review

The literature study explores the conceptual and theoretical analysis of the subject areas

and describes the associated elements to develop the complete understanding of the research

study. The research concentrates on the considerable challenges faced by the corporations due to

the emerging financial scams and internal fraudulent activities that cause greater financial loss

and reputational damage (Domino, Giordano and Webinger 2017). It can be stated that the

forensic accountants need to be much efficient in terms of developing the concerns regarding the

FORENSIC ACCOUNTING

To critically examine the effectiveness of forensic accounting process to detect or

prevent the internal financial frauds

To investigate the challenges faced by the firms due to the external and internal

fraudulent financial concerns

To provide the preferable recommendations to mitigate the challenges with the Forensic

Accounting planning within the retail corporations

1.5 Research Questions

How the forensic accounting system helps in addressing and managing the financial

frauds in retail corporations?

To what extent the forensic accounting system becomes obligatory to undertake the audit

process for developing sound corporate governance?

What are the major challenges faced due to the emergence of the financial frauds within

the corporation?

How these challenges can be mitigated by using the appropriate forensic accounting

process?

2.0 Literature Review

The literature study explores the conceptual and theoretical analysis of the subject areas

and describes the associated elements to develop the complete understanding of the research

study. The research concentrates on the considerable challenges faced by the corporations due to

the emerging financial scams and internal fraudulent activities that cause greater financial loss

and reputational damage (Domino, Giordano and Webinger 2017). It can be stated that the

forensic accountants need to be much efficient in terms of developing the concerns regarding the

8

FORENSIC ACCOUNTING

internal control system of the organisation. In addition to this, it is noticeable that this aspect

even involves the continuous monitoring if the institutional needs that are often affected by the

fraudulent acts. It is noticeable that the current business arena has been experiencing extreme

frauds in the financial calculations (Golden, Skalak and Clayton, 2011). The regular

improvements in the forensic accounting process can help in identifying the mistakes or the

fraudulent acts. Organisations require using the appropriate forensic audit report if there is the

failure observed in governance or internal control. The examination of the internal audit reports

sometimes unable to identify the loopholes due to which the corporations fail to achieve the

success in developing the appropriate corporate governance procedures (Matson, 2016).

Moreover, it affects the integrity level that leads to lack of faith and loss of customer base. The

forensic accounting is a procedure to examine such discrepancy and resolve the issues for the

organisational benefits. The literature study would provide the conceptual analysis of the key

factors associated with the forensic accounting process. This study will also help in identifying

the impacts of these elements on the corporate governance process within a firm. The obtained

ideas from the literature will be used for developing the clear understanding of the research study

in the further section.

2.1 Concept of Forensic Accounting

Forensic accounting is a terminology that defines the method of internal financial audit to

investigate the financial statement of a firm. According to Nelson, Brayman and Barry (2012),

the forensic accounting process helps in preparing the financial statements that can be presented

to any court or legal proceeding in order to address the identified issues with the fraudulent acts

within the firm. Nelson, Brayman and Barry (2012) also defined that forensic accounting is the

practice of internal and external financial audits that provides the clear explanations of the real

FORENSIC ACCOUNTING

internal control system of the organisation. In addition to this, it is noticeable that this aspect

even involves the continuous monitoring if the institutional needs that are often affected by the

fraudulent acts. It is noticeable that the current business arena has been experiencing extreme

frauds in the financial calculations (Golden, Skalak and Clayton, 2011). The regular

improvements in the forensic accounting process can help in identifying the mistakes or the

fraudulent acts. Organisations require using the appropriate forensic audit report if there is the

failure observed in governance or internal control. The examination of the internal audit reports

sometimes unable to identify the loopholes due to which the corporations fail to achieve the

success in developing the appropriate corporate governance procedures (Matson, 2016).

Moreover, it affects the integrity level that leads to lack of faith and loss of customer base. The

forensic accounting is a procedure to examine such discrepancy and resolve the issues for the

organisational benefits. The literature study would provide the conceptual analysis of the key

factors associated with the forensic accounting process. This study will also help in identifying

the impacts of these elements on the corporate governance process within a firm. The obtained

ideas from the literature will be used for developing the clear understanding of the research study

in the further section.

2.1 Concept of Forensic Accounting

Forensic accounting is a terminology that defines the method of internal financial audit to

investigate the financial statement of a firm. According to Nelson, Brayman and Barry (2012),

the forensic accounting process helps in preparing the financial statements that can be presented

to any court or legal proceeding in order to address the identified issues with the fraudulent acts

within the firm. Nelson, Brayman and Barry (2012) also defined that forensic accounting is the

practice of internal and external financial audits that provides the clear explanations of the real

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FORENSIC ACCOUNTING

and estimated disputes in the corporations. “Forensic” is the term, which is generally used in

legal proceeding or courts in time of presenting the evidence of financial disputes. The forensic

accountants are the external auditors who review the entire financial statement of the

corporations by developing the deeper understanding regarding the parameter. The forensic

accounting practice is adopted to identify the types of crimes and investigate the issues with the

“crimes against property”. Especially, the external auditors review the financial statements if the

internal auditor fails to identify the disputes. Rezaee, Larry Crumbley and Elmore (2004) also

identified that the forensic accountants are often considered as the fraud investigators or the

investigative accountants that belong to the external source of the firm.

The theoretical explanation of the forensic accounting determines that there are a set of

activities due to which these practices are undertaken by the external and the internal auditors.

Seda and Peterson Kramer (2015) stated that organisations require using the appropriate forensic

audit report if there is the failure observed in governance or internal control. Supporting such

statement, Singleton and Singleton (2010) analyzed that this process is most suitable in terms of

creating the report on ‘conflict of interest’. In terms of identifying the reasons for the collapsing

corporate scenario that often involves the date of insolvency. Taylor, Bogdan and DeVault

(2015) presented the idea of the theft of intellectual property require the development of the clear

audit report of the internal financial statement. The use of the forensic accounting practices is

quite necessary in such cases. Furthermore, this suitable practice helps in identifying the

challenges faced by the corporations due to the complex reconciliation unauthorized leakage of

the information, which is commercially sensitive. In some of the cases, as stated by Smith

(2015), the corporations fail to comply with some specifications associated with the regulatory

requirements, such as Competition and Consumer Act 2010. The forensic accounting process

FORENSIC ACCOUNTING

and estimated disputes in the corporations. “Forensic” is the term, which is generally used in

legal proceeding or courts in time of presenting the evidence of financial disputes. The forensic

accountants are the external auditors who review the entire financial statement of the

corporations by developing the deeper understanding regarding the parameter. The forensic

accounting practice is adopted to identify the types of crimes and investigate the issues with the

“crimes against property”. Especially, the external auditors review the financial statements if the

internal auditor fails to identify the disputes. Rezaee, Larry Crumbley and Elmore (2004) also

identified that the forensic accountants are often considered as the fraud investigators or the

investigative accountants that belong to the external source of the firm.

The theoretical explanation of the forensic accounting determines that there are a set of

activities due to which these practices are undertaken by the external and the internal auditors.

Seda and Peterson Kramer (2015) stated that organisations require using the appropriate forensic

audit report if there is the failure observed in governance or internal control. Supporting such

statement, Singleton and Singleton (2010) analyzed that this process is most suitable in terms of

creating the report on ‘conflict of interest’. In terms of identifying the reasons for the collapsing

corporate scenario that often involves the date of insolvency. Taylor, Bogdan and DeVault

(2015) presented the idea of the theft of intellectual property require the development of the clear

audit report of the internal financial statement. The use of the forensic accounting practices is

quite necessary in such cases. Furthermore, this suitable practice helps in identifying the

challenges faced by the corporations due to the complex reconciliation unauthorized leakage of

the information, which is commercially sensitive. In some of the cases, as stated by Smith

(2015), the corporations fail to comply with some specifications associated with the regulatory

requirements, such as Competition and Consumer Act 2010. The forensic accounting process

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FORENSIC ACCOUNTING

helps in identifying the gap more specifically to fulfill the requirements with proper efficiency.

In addition to this, the effective forensic accounting practices help in investigating the issues

occur due to the multiple payments of the invoices, overpayments of the fees, taxes, and other

charges.

2.2 Conceptual Analysis of ‘Fraud’

The detailed analysis regarding the role of forensic accountants determines the in-doeth

investigations surrounding the alleged frauds, illegal activities, and corruptions conducted by any

employee associated with the organisation. According to DiGabriele and Huber (2015), it often

involves the investigations of several external concerns related to corruption, frauds, and other

business crimes. The role of the forensic accountants depends on the term ‘fraud’ that identifies

the crime made by a lay person that is needed to be investigated. Durtschi and Rufus (2017)

defined that ‘fraud’ is conceptualized as the dishonest activity that causes the potential financial

loss to any entity or person and it even includes the theft of property or money. Fraudulent

activities even involve the deliberate concealment, falsification, and destruction of the

documents that are used for performing business functions (Henry and Ganiyu, 2018). This type

of theft of property is termed as ‘fraud’ within an entity. This terminology generally deals with

crime focused legislations and creates the significant damage to the corporation. The forensic

accountants need to perform their responsibility to deal with such mismanagement and

discrepancy to resolve the issues and protect the organisations from such practices.

2.3 Corruption and Fraud in Australian Corporations

There are numerous debates formulated over the concept of fraudulent acts within the

Australian corporations. At the end, it becomes the significant aspects for the industry within

FORENSIC ACCOUNTING

helps in identifying the gap more specifically to fulfill the requirements with proper efficiency.

In addition to this, the effective forensic accounting practices help in investigating the issues

occur due to the multiple payments of the invoices, overpayments of the fees, taxes, and other

charges.

2.2 Conceptual Analysis of ‘Fraud’

The detailed analysis regarding the role of forensic accountants determines the in-doeth

investigations surrounding the alleged frauds, illegal activities, and corruptions conducted by any

employee associated with the organisation. According to DiGabriele and Huber (2015), it often

involves the investigations of several external concerns related to corruption, frauds, and other

business crimes. The role of the forensic accountants depends on the term ‘fraud’ that identifies

the crime made by a lay person that is needed to be investigated. Durtschi and Rufus (2017)

defined that ‘fraud’ is conceptualized as the dishonest activity that causes the potential financial

loss to any entity or person and it even includes the theft of property or money. Fraudulent

activities even involve the deliberate concealment, falsification, and destruction of the

documents that are used for performing business functions (Henry and Ganiyu, 2018). This type

of theft of property is termed as ‘fraud’ within an entity. This terminology generally deals with

crime focused legislations and creates the significant damage to the corporation. The forensic

accountants need to perform their responsibility to deal with such mismanagement and

discrepancy to resolve the issues and protect the organisations from such practices.

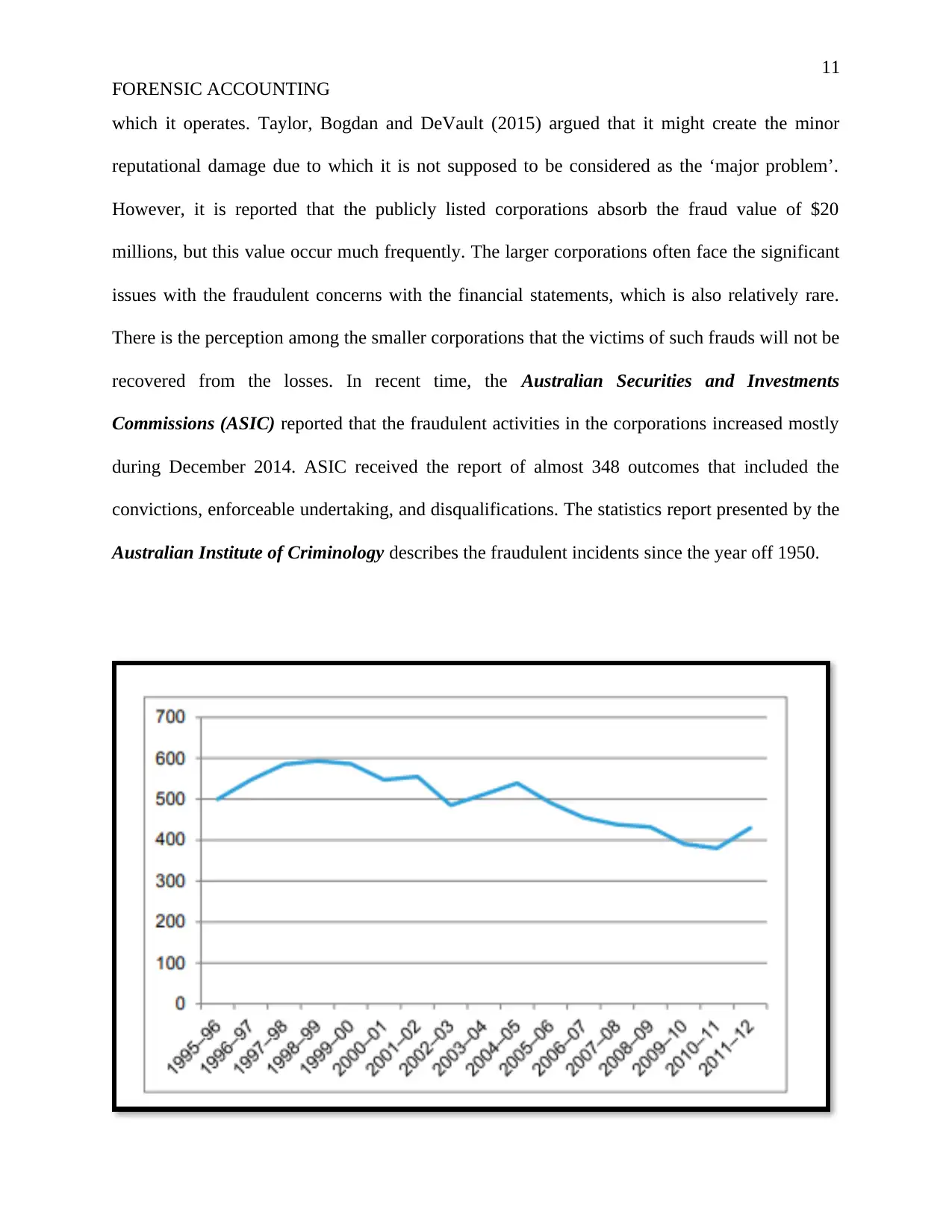

2.3 Corruption and Fraud in Australian Corporations

There are numerous debates formulated over the concept of fraudulent acts within the

Australian corporations. At the end, it becomes the significant aspects for the industry within

11

FORENSIC ACCOUNTING

which it operates. Taylor, Bogdan and DeVault (2015) argued that it might create the minor

reputational damage due to which it is not supposed to be considered as the ‘major problem’.

However, it is reported that the publicly listed corporations absorb the fraud value of $20

millions, but this value occur much frequently. The larger corporations often face the significant

issues with the fraudulent concerns with the financial statements, which is also relatively rare.

There is the perception among the smaller corporations that the victims of such frauds will not be

recovered from the losses. In recent time, the Australian Securities and Investments

Commissions (ASIC) reported that the fraudulent activities in the corporations increased mostly

during December 2014. ASIC received the report of almost 348 outcomes that included the

convictions, enforceable undertaking, and disqualifications. The statistics report presented by the

Australian Institute of Criminology describes the fraudulent incidents since the year off 1950.

FORENSIC ACCOUNTING

which it operates. Taylor, Bogdan and DeVault (2015) argued that it might create the minor

reputational damage due to which it is not supposed to be considered as the ‘major problem’.

However, it is reported that the publicly listed corporations absorb the fraud value of $20

millions, but this value occur much frequently. The larger corporations often face the significant

issues with the fraudulent concerns with the financial statements, which is also relatively rare.

There is the perception among the smaller corporations that the victims of such frauds will not be

recovered from the losses. In recent time, the Australian Securities and Investments

Commissions (ASIC) reported that the fraudulent activities in the corporations increased mostly

during December 2014. ASIC received the report of almost 348 outcomes that included the

convictions, enforceable undertaking, and disqualifications. The statistics report presented by the

Australian Institute of Criminology describes the fraudulent incidents since the year off 1950.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.