Forensic Accounting: Voided Invoice Analysis and Evidence

VerifiedAdded on 2023/01/11

|5

|586

|81

Report

AI Summary

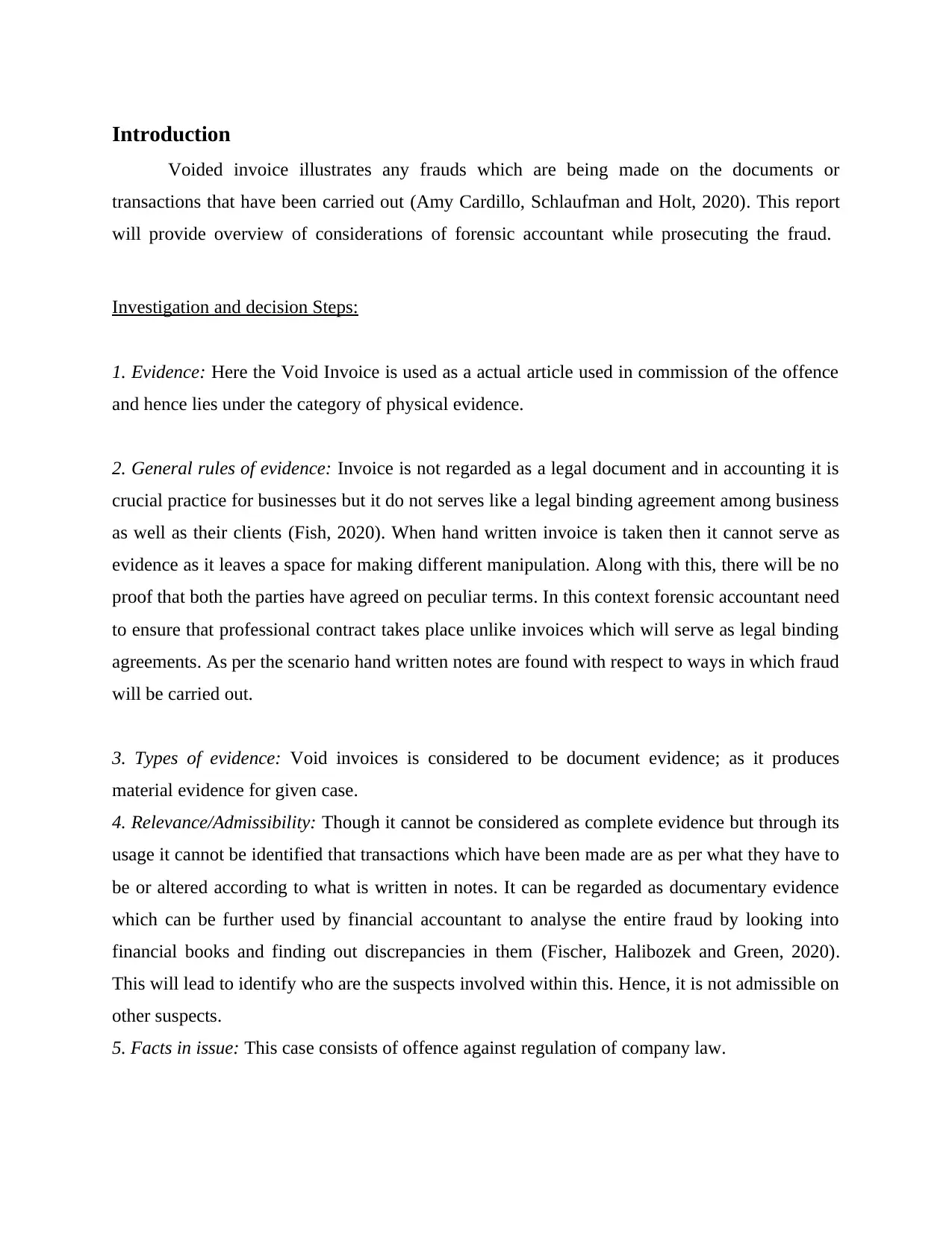

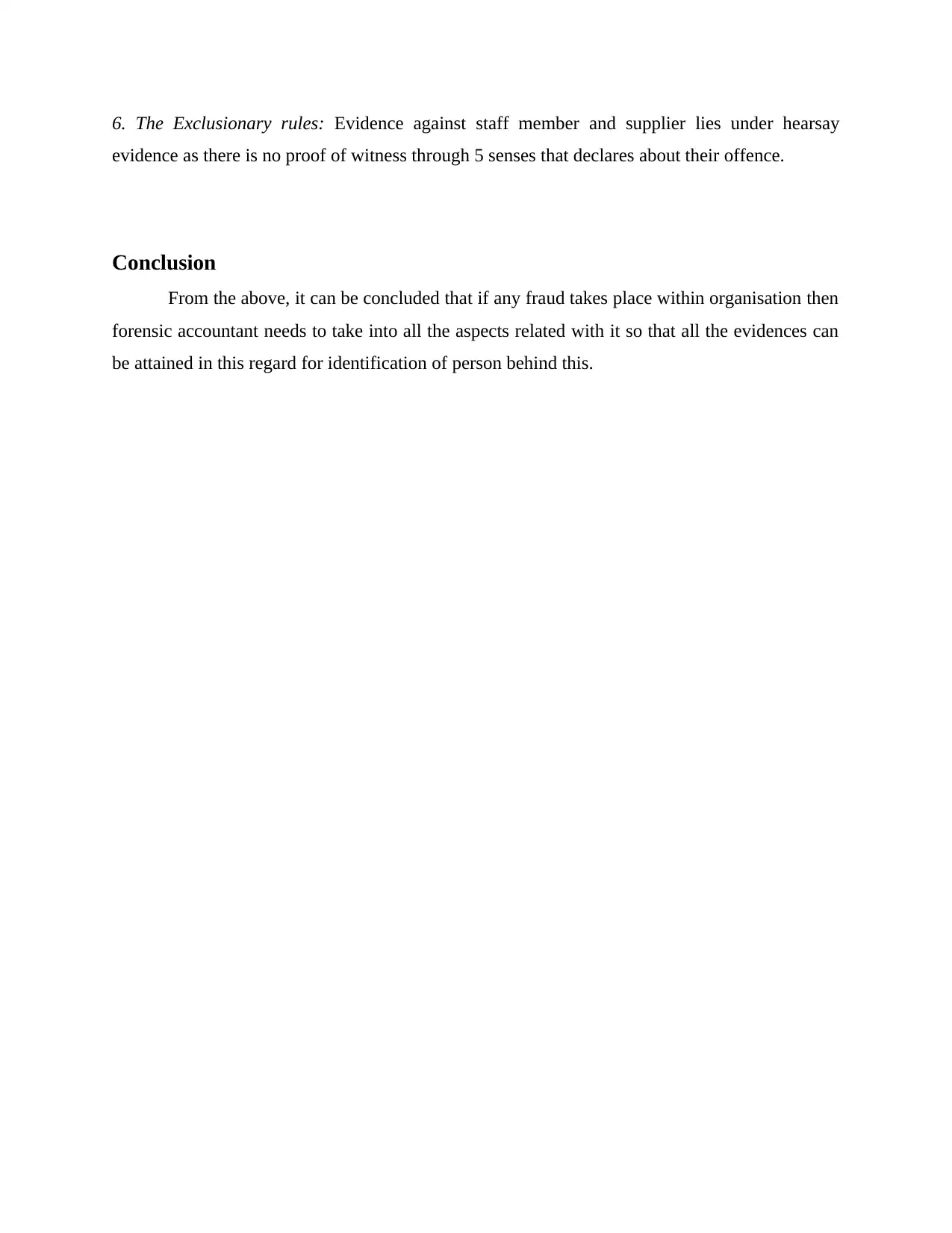

This report analyzes a voided invoice as a crucial piece of evidence in financial fraud investigations, focusing on the role of forensic accounting. The report begins by classifying the voided invoice as documentary evidence and explores its relevance, admissibility, and the legal considerations surrounding it. It examines how the invoice can be used to uncover fraudulent activities, referencing the importance of legal binding agreements and the limitations of handwritten invoices. The report further discusses the application of general rules of evidence, the types of evidence, and the exclusionary rules. The conclusion emphasizes the need for a comprehensive approach by forensic accountants to gather all related evidence for identifying those responsible for financial fraud. The report references several academic sources to support its analysis.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.