Literature Review: Forensic Accounting, Frauds and Limitations

VerifiedAdded on 2023/06/07

|7

|2074

|388

Literature Review

AI Summary

This literature review provides an overview of forensic accounting, its definitions, and activities, highlighting its increasing importance in the global commercial framework. It examines the role of forensic accountants in analyzing financial records, detecting fraudulent activities, and assisting companies in legal proceedings. The review discusses the 'Fraud Triangle,' emphasizing how forensic accounting helps identify and prevent opportunities for fraud. Furthermore, it explores the significance of forensic accounting in financial fraud investigations, legal enforcements, and crucial financial activities. The review also acknowledges the limitations of forensic accounting, such as confidentiality concerns, negative publicity, and costs. Despite these limitations, the review concludes that forensic accounting is vital for ensuring profitability, competitiveness, and long-term sustainability in businesses worldwide.

Running head: LITRATURE REVIEW: FORENSIC ACCOUNTING

Literature Review: Forensic Accounting

Name of the Student

Name of the University

Author Note

Literature Review: Forensic Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1LITERATURE REVIEW: FORENSIC ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Forensic Accounting: Meaning and Definitions........................................................................2

Activities of Forensic Accountants............................................................................................2

Why Forensic Accounting is required in companies.................................................................3

Significance of Forensic Accounting.........................................................................................4

Limitations and Problems in Financial Accounting...................................................................4

Conclusion..................................................................................................................................5

References..................................................................................................................................6

Table of Contents

Introduction................................................................................................................................2

Forensic Accounting: Meaning and Definitions........................................................................2

Activities of Forensic Accountants............................................................................................2

Why Forensic Accounting is required in companies.................................................................3

Significance of Forensic Accounting.........................................................................................4

Limitations and Problems in Financial Accounting...................................................................4

Conclusion..................................................................................................................................5

References..................................................................................................................................6

2LITERATURE REVIEW: FORENSIC ACCOUNTING

Introduction

Accounting, as a separate discipline, has emerged as one of the significant

components in the global commercial framework, over the decades. With the international

business scenario becoming more integrated, inclusive and dynamics in the contemporary

period, considerably owing to phenomena like that of Globalisation, commercial

liberalisations, technological innovations and others, the importance of proper accounting

methods and tools are felt significantly in the operational framework of any kind of business

across the globe. This is because much of a company’s efficiency, cost-effectiveness,

profitability and sustainability depends on the presence of suitable and efficient accounting

methods.

However, in the recent period, with the increase in the commercial activities across

the globe and with the increasing technological developments and implementations (like that

of usage of internet), the financial security of the businesses has been becoming one of the

primary issues of concern. With time, the number of accounting scandals, frauds and unfair

activities can also be seen to be increasing in these scenarios. This is turn, has led to the

evolution of forensic accounting and the increased implementation of the same in the

business activities.

Keeping this into consideration, the following section of the report consists of an

extensive review of the existing literary and scholarly work in the domain of evolution,

importance, implication and limitations of forensic accounting, especially emphasizing on the

commercial domain of Australia.

Forensic Accounting: Meaning and Definitions

There exist various perceptions and definitons of the notion of “Forensic Accounting”

as a separate and independent genre in the accouning framework in general international

scenrio. In this context, Pedneault, et al. (2012), describes forensic accounting as an

amalgamation of accounting frameworks and principles, especially in the corporate scenario

with that of the techniliques and activities related to investigation and detection og any kind

of fraudulent or suspicious activities especially in the domians of finanical statements,

records and other financial activities of the companeis, in the contemproary global

commercial scenario. The assertions of the authors, can be seen to be augmented by the

argument put forward by Bhasin (2015), according to whom, the genre of forensic accounting

provides an analysis of accounting which is suitable to the court and which, in case of

contingencies, can help in forming the basis for debates, discussions and resolution of

disputes regarding the financial aspects of the different companies in the contemporary global

scenario.

Thus, from the assertions of the different literary works it is evident that the genre of

forensic accounting holds immense relevance in the financial activities and also in the overall

operational framework of the businesses, especially in the contemporary period of creation of

a global market for businesses, with increasing activities and dynamics in both the demand

side as well as supply side.

Activities of Forensic Accountants

In their elaborate literary work, regarding the development of the genre of forensic

accounting and the increasing implementation of the practices in this domain, increasingly, in

the contemporary business frameworks, Özkul and Pamukçu (2012), highlight the different

activities which are priamrily performed by the forensic accountants, especially in the domain

Introduction

Accounting, as a separate discipline, has emerged as one of the significant

components in the global commercial framework, over the decades. With the international

business scenario becoming more integrated, inclusive and dynamics in the contemporary

period, considerably owing to phenomena like that of Globalisation, commercial

liberalisations, technological innovations and others, the importance of proper accounting

methods and tools are felt significantly in the operational framework of any kind of business

across the globe. This is because much of a company’s efficiency, cost-effectiveness,

profitability and sustainability depends on the presence of suitable and efficient accounting

methods.

However, in the recent period, with the increase in the commercial activities across

the globe and with the increasing technological developments and implementations (like that

of usage of internet), the financial security of the businesses has been becoming one of the

primary issues of concern. With time, the number of accounting scandals, frauds and unfair

activities can also be seen to be increasing in these scenarios. This is turn, has led to the

evolution of forensic accounting and the increased implementation of the same in the

business activities.

Keeping this into consideration, the following section of the report consists of an

extensive review of the existing literary and scholarly work in the domain of evolution,

importance, implication and limitations of forensic accounting, especially emphasizing on the

commercial domain of Australia.

Forensic Accounting: Meaning and Definitions

There exist various perceptions and definitons of the notion of “Forensic Accounting”

as a separate and independent genre in the accouning framework in general international

scenrio. In this context, Pedneault, et al. (2012), describes forensic accounting as an

amalgamation of accounting frameworks and principles, especially in the corporate scenario

with that of the techniliques and activities related to investigation and detection og any kind

of fraudulent or suspicious activities especially in the domians of finanical statements,

records and other financial activities of the companeis, in the contemproary global

commercial scenario. The assertions of the authors, can be seen to be augmented by the

argument put forward by Bhasin (2015), according to whom, the genre of forensic accounting

provides an analysis of accounting which is suitable to the court and which, in case of

contingencies, can help in forming the basis for debates, discussions and resolution of

disputes regarding the financial aspects of the different companies in the contemporary global

scenario.

Thus, from the assertions of the different literary works it is evident that the genre of

forensic accounting holds immense relevance in the financial activities and also in the overall

operational framework of the businesses, especially in the contemporary period of creation of

a global market for businesses, with increasing activities and dynamics in both the demand

side as well as supply side.

Activities of Forensic Accountants

In their elaborate literary work, regarding the development of the genre of forensic

accounting and the increasing implementation of the practices in this domain, increasingly, in

the contemporary business frameworks, Özkul and Pamukçu (2012), highlight the different

activities which are priamrily performed by the forensic accountants, especially in the domain

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3LITERATURE REVIEW: FORENSIC ACCOUNTING

of corporate activities. As per the assertions of the authors, the primary roles played by the

forensic accountants, in the corporate scenario are as follows:

Analysis of various financial activities and records as well as statements of the

different companies and investigation of the financial evidences of the companies, so

as to examine the presence of any kind of fraudulent or unfair activities in this domain

Development of various computerised tools and applications for the purpose of easier

and more comprehensive as well as efficient ways of analysing the financial

evidences and also for more effective presentation of the financial evidences and any

kind of discrepancies (if any) present in the same (Bhasin, 2015)

Communication of the findings of their analysis to the relevant authorities, in the

forms of exhibits, proper documentations and reports and also organization and

collection of the relevant financial documents to empirically and statistically support

their assertions

Helping the companies their work for, in different legal proceedings in different

circumstances, which include testifying in the courts as expert witnesses on behalf of

their organizations and also preparing aids and evidences to support the companies’

case in the trial proceedings when contingency situations arise (Pedneault. et al.,

2012)

Why Forensic Accounting is required in companies

As highlighted by Miller and Power (2013), with the development of the corporate

frameowrk across the globe and with the increasing dynamics and activities as well as

complexities in the operational framework of the businesses, in the contemporary period, the

instances of fraudulent or unethical activities as well as suspicious transactions can be seen to

be increasing in the business organizations, which have been the primary reasons behing most

of the major finanical scams and scandals in the global as well as Australian corporate

scandals (like the recent banking scandals), in the contemporary period.

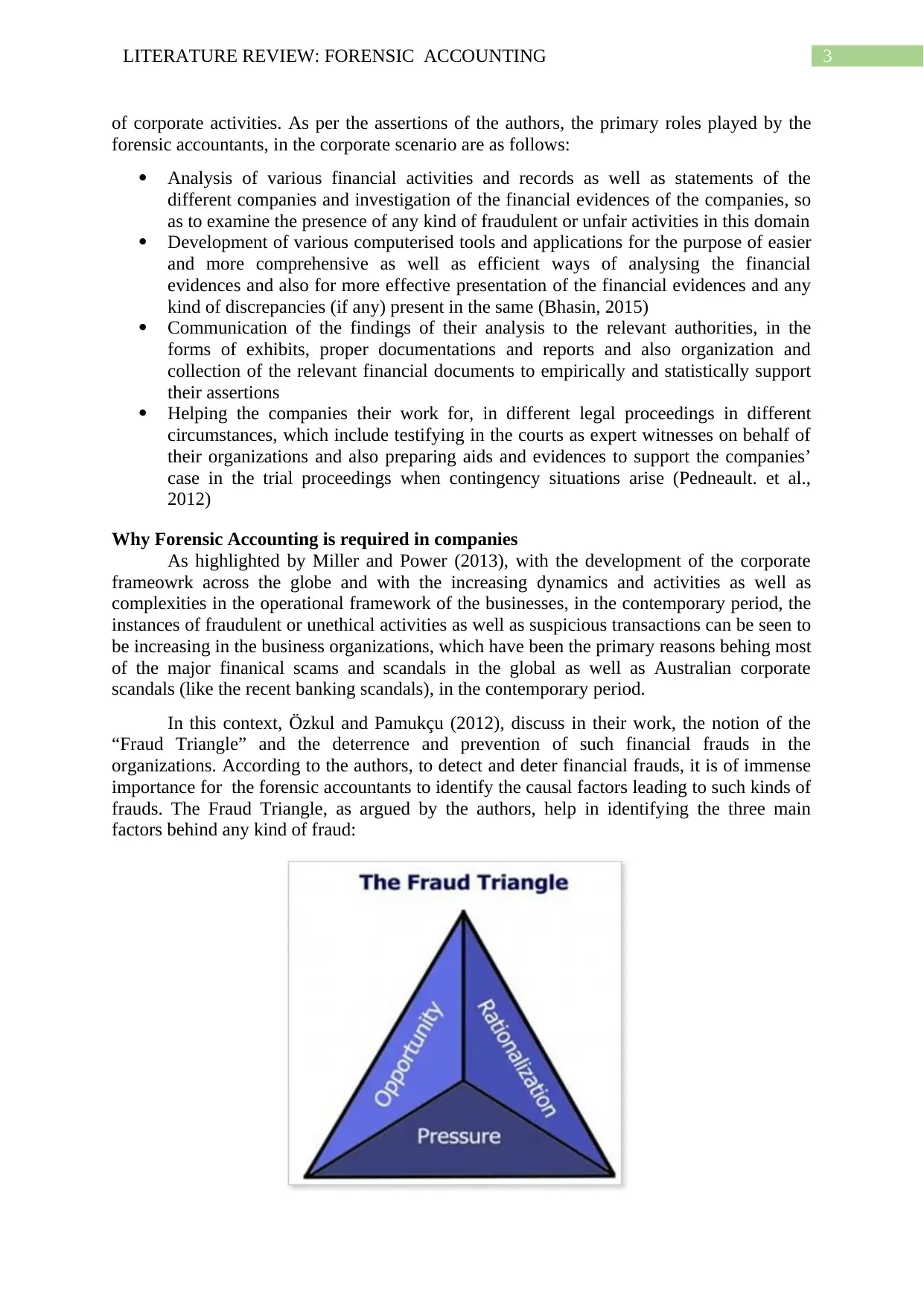

In this context, Özkul and Pamukçu (2012), discuss in their work, the notion of the

“Fraud Triangle” and the deterrence and prevention of such financial frauds in the

organizations. According to the authors, to detect and deter financial frauds, it is of immense

importance for the forensic accountants to identify the causal factors leading to such kinds of

frauds. The Fraud Triangle, as argued by the authors, help in identifying the three main

factors behind any kind of fraud:

of corporate activities. As per the assertions of the authors, the primary roles played by the

forensic accountants, in the corporate scenario are as follows:

Analysis of various financial activities and records as well as statements of the

different companies and investigation of the financial evidences of the companies, so

as to examine the presence of any kind of fraudulent or unfair activities in this domain

Development of various computerised tools and applications for the purpose of easier

and more comprehensive as well as efficient ways of analysing the financial

evidences and also for more effective presentation of the financial evidences and any

kind of discrepancies (if any) present in the same (Bhasin, 2015)

Communication of the findings of their analysis to the relevant authorities, in the

forms of exhibits, proper documentations and reports and also organization and

collection of the relevant financial documents to empirically and statistically support

their assertions

Helping the companies their work for, in different legal proceedings in different

circumstances, which include testifying in the courts as expert witnesses on behalf of

their organizations and also preparing aids and evidences to support the companies’

case in the trial proceedings when contingency situations arise (Pedneault. et al.,

2012)

Why Forensic Accounting is required in companies

As highlighted by Miller and Power (2013), with the development of the corporate

frameowrk across the globe and with the increasing dynamics and activities as well as

complexities in the operational framework of the businesses, in the contemporary period, the

instances of fraudulent or unethical activities as well as suspicious transactions can be seen to

be increasing in the business organizations, which have been the primary reasons behing most

of the major finanical scams and scandals in the global as well as Australian corporate

scandals (like the recent banking scandals), in the contemporary period.

In this context, Özkul and Pamukçu (2012), discuss in their work, the notion of the

“Fraud Triangle” and the deterrence and prevention of such financial frauds in the

organizations. According to the authors, to detect and deter financial frauds, it is of immense

importance for the forensic accountants to identify the causal factors leading to such kinds of

frauds. The Fraud Triangle, as argued by the authors, help in identifying the three main

factors behind any kind of fraud:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4LITERATURE REVIEW: FORENSIC ACCOUNTING

Figure 1: The Fraud Triangle

(Source: Algaonline.org, 2018)

The main factors of the Fraud Triangle can also be seen to be elaborated by Miller and

Power (2013), to be as follows:

Pressure- This shows the motive or need behind committing any kind of fraud

Rationalization- This indicates towards the mindset and thought processes of the person

committing the frauds, which justify their actions from their perspectives and from them

Opportunity- This refers to the situations or the circumstances which enables the concerned

people to commit the frauds

According to Özkul and Pamukçu (2012), the aspects and activities of forensic

accounting, mainly helps in identifying and preventing the third factor of the fraud triangle,

that is, the forensic accounting actitivies primarily try to identify the opporunities which

enable fraudulent activities in an organization and try to diminish or eradicate the same.

However, their assertions are also seen to be countered by Bhasin (2015), according to

whom, the forensic accounting activities not only detect the opportunities but also analyse the

presence or occurrence of any kind of fraudulent activities in the business organizations.

Significance of Forensic Accounting

With the number and magnitudes of corporated scandals and fraudulent activities in

the contemporary global commerical organizations, the significance of forensic accounting

practices in the operational frameworks of the business organizations can also be seen to be

increasing considerably. In this context, the primary importance of the roles played by the

forensic accounting and forensic accountants can be seen to be highlighted by Özkul and

Pamukçu (2012), to be as follows:

Financial Fraud Investigations- The primary crucial role played by the forensic accountants

in the business organizations, as highlighted by the authors, is that of investigation of the

various financial fraudulent activities by the different stakeholders of the companies,

including that of the employees, clients, other related companeis, etc., which in turn helps the

companies to stay efficient in their operations and contribute positively in their profitability

and competitiveness.

Legal Enforcements- Another importance of forensic accounting practices, can be seen to be

put forward by Bhasin (2015), as that of the facilitation of the enforcements of the different

regulatory policies and requirements by the government of the concerned countries, which in

turn help the governments of the countries to reduce the possibilities of corporate scandals,

thereby increasing not only the welfare of the individual companies and their stakeholders,

but also the overall welfare of the society.

Financial Activities- As asserted by Özkul and Pamukçu (2012), the forensic accountants

working for different companies, not only help in detection, prevention and reduction of

different types of frauds but also help in different crucial financial activities of the

companeis, like that of fixation of prices, manipulations of the stock market dynamics and

presentation of proper and authentic financial reports which in turn help the companeis to

take efficient and far-sighted financial as well as other production and operational decisions.

Figure 1: The Fraud Triangle

(Source: Algaonline.org, 2018)

The main factors of the Fraud Triangle can also be seen to be elaborated by Miller and

Power (2013), to be as follows:

Pressure- This shows the motive or need behind committing any kind of fraud

Rationalization- This indicates towards the mindset and thought processes of the person

committing the frauds, which justify their actions from their perspectives and from them

Opportunity- This refers to the situations or the circumstances which enables the concerned

people to commit the frauds

According to Özkul and Pamukçu (2012), the aspects and activities of forensic

accounting, mainly helps in identifying and preventing the third factor of the fraud triangle,

that is, the forensic accounting actitivies primarily try to identify the opporunities which

enable fraudulent activities in an organization and try to diminish or eradicate the same.

However, their assertions are also seen to be countered by Bhasin (2015), according to

whom, the forensic accounting activities not only detect the opportunities but also analyse the

presence or occurrence of any kind of fraudulent activities in the business organizations.

Significance of Forensic Accounting

With the number and magnitudes of corporated scandals and fraudulent activities in

the contemporary global commerical organizations, the significance of forensic accounting

practices in the operational frameworks of the business organizations can also be seen to be

increasing considerably. In this context, the primary importance of the roles played by the

forensic accounting and forensic accountants can be seen to be highlighted by Özkul and

Pamukçu (2012), to be as follows:

Financial Fraud Investigations- The primary crucial role played by the forensic accountants

in the business organizations, as highlighted by the authors, is that of investigation of the

various financial fraudulent activities by the different stakeholders of the companies,

including that of the employees, clients, other related companeis, etc., which in turn helps the

companies to stay efficient in their operations and contribute positively in their profitability

and competitiveness.

Legal Enforcements- Another importance of forensic accounting practices, can be seen to be

put forward by Bhasin (2015), as that of the facilitation of the enforcements of the different

regulatory policies and requirements by the government of the concerned countries, which in

turn help the governments of the countries to reduce the possibilities of corporate scandals,

thereby increasing not only the welfare of the individual companies and their stakeholders,

but also the overall welfare of the society.

Financial Activities- As asserted by Özkul and Pamukçu (2012), the forensic accountants

working for different companies, not only help in detection, prevention and reduction of

different types of frauds but also help in different crucial financial activities of the

companeis, like that of fixation of prices, manipulations of the stock market dynamics and

presentation of proper and authentic financial reports which in turn help the companeis to

take efficient and far-sighted financial as well as other production and operational decisions.

5LITERATURE REVIEW: FORENSIC ACCOUNTING

Limitations and Problems in Financial Accounting

Pedneault, et al. (2012) in their work, along with identifications of the benefits and

significances of forensic accounting in the contemporary global commerical scenario, also

highlight the major limitations of such practices to be as follows:

Confidentiality Concern- As per the arguments of the authors, as in general, external forensic

accountants scrutinise the financial records of different companies, the same in turn leads to

leakage and compromise of the confidential financial aspects of the concerned companies. In

spite of the presence of strict ethical norms in this regard, disclosure of financial aspects of

the companies frequently take place, thereby compromising the financial security of the

same.

Negative Publicity- The detection of frauds and ordeals like that of court trials also lead to

immesne negative publicity of the companies, which in turn hampers their reputation,

sustainability and profitability.

Costs- Bhasin (2015), also points out that forensic accounting is a highly expensive activity

involving costly and high-end softwares, expensive experts and the costs increase manifold in

cases of trials in the courts.

Conclusion

From the above discussion and review of the existing literary works, it is evident that

in spite of the presence of several limtations and bottlenecks, forensic accounting, has over

the years, gained immense importance and popularity in the global commercial framework

and the same plays several crucial roles in ensuring profitability, prospects, competitiveness

and long-term sustainability of the businesses across the globe.

Limitations and Problems in Financial Accounting

Pedneault, et al. (2012) in their work, along with identifications of the benefits and

significances of forensic accounting in the contemporary global commerical scenario, also

highlight the major limitations of such practices to be as follows:

Confidentiality Concern- As per the arguments of the authors, as in general, external forensic

accountants scrutinise the financial records of different companies, the same in turn leads to

leakage and compromise of the confidential financial aspects of the concerned companies. In

spite of the presence of strict ethical norms in this regard, disclosure of financial aspects of

the companies frequently take place, thereby compromising the financial security of the

same.

Negative Publicity- The detection of frauds and ordeals like that of court trials also lead to

immesne negative publicity of the companies, which in turn hampers their reputation,

sustainability and profitability.

Costs- Bhasin (2015), also points out that forensic accounting is a highly expensive activity

involving costly and high-end softwares, expensive experts and the costs increase manifold in

cases of trials in the courts.

Conclusion

From the above discussion and review of the existing literary works, it is evident that

in spite of the presence of several limtations and bottlenecks, forensic accounting, has over

the years, gained immense importance and popularity in the global commercial framework

and the same plays several crucial roles in ensuring profitability, prospects, competitiveness

and long-term sustainability of the businesses across the globe.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6LITERATURE REVIEW: FORENSIC ACCOUNTING

References

Algaonline.org, 2018. Association Of Local Government Auditors, KY - The Fraud Triangle.

[online] Algaonline.org. Available at: <https://algaonline.org/index.aspx?NID=417>

[Accessed 31 August 2018].

Bhasin, M.L., 2015. Contribution of Forensic Accounting to Corporate Governance: An

Exploratory Study of an Asian Country.

Miller, P. and Power, M., 2013. Accounting, organizing, and economizing: Connecting

accounting research and organization theory. The Academy of Management Annals, 7(1),

pp.557-605.

Özkul, F.U. and Pamukçu, A., 2012. Fraud detection and forensic accounting. In Emerging

fraud (pp. 19-41). Springer, Berlin, Heidelberg.

Pedneault, S., Silverstone, H., Rudewicz, F. and Sheetz, M., 2012. Forensic accounting and

fraud investigation for non-experts. John Wiley & Sons.

References

Algaonline.org, 2018. Association Of Local Government Auditors, KY - The Fraud Triangle.

[online] Algaonline.org. Available at: <https://algaonline.org/index.aspx?NID=417>

[Accessed 31 August 2018].

Bhasin, M.L., 2015. Contribution of Forensic Accounting to Corporate Governance: An

Exploratory Study of an Asian Country.

Miller, P. and Power, M., 2013. Accounting, organizing, and economizing: Connecting

accounting research and organization theory. The Academy of Management Annals, 7(1),

pp.557-605.

Özkul, F.U. and Pamukçu, A., 2012. Fraud detection and forensic accounting. In Emerging

fraud (pp. 19-41). Springer, Berlin, Heidelberg.

Pedneault, S., Silverstone, H., Rudewicz, F. and Sheetz, M., 2012. Forensic accounting and

fraud investigation for non-experts. John Wiley & Sons.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.