Accounting in Context: Forensic Accounting in Retail Sector UK

VerifiedAdded on 2021/04/21

|17

|6777

|363

Report

AI Summary

This report investigates the influence of forensic accounting on addressing deceptive and fraudulent activities, aiming to ensure robust corporate governance in UK retail firms. It highlights forensic accounting as a crucial tool for combating financial crimes and ensuring corporate governance. The study examines a retail corporation's structure and organizational hierarchy, focusing on how forensic accounting can aid in detecting and preventing fraud, as requested by the Financial Director. The report analyzes key issues, synthesizes arguments from academic articles, and presents recommendations to enhance fraud detection efforts and strengthen corporate governance in the retail sector. It emphasizes the importance of forensic accounting services in fraud prevention and the need for increased public awareness and demand for these services.

Running head: ACCOUNTING IN CONTEXT

Accounting in Context

University Name

Student Name

Authors’ Note

Accounting in Context

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

ACCOUNTING IN CONTEXT

Executive Summary

The current study essentially ascertains the overall influence of particularly forensic

accounting in addressing deceptive and fraudulent deeds in a bid to make certain

good corporate codes in diverse selected corporation of UK. Forensic accounting

can be indicated as an effectual tool for addressing financial crimes in business

concerns. In addition to this, forensic audit helps in making certain corporate

governance in particular business concerns. Founded on this, the study suggested

that firms need to implement forensic accounting in order to add to the efforts of

decreasing fraudulent actions for making certain good corporate governance code in

retail business concerns.

ACCOUNTING IN CONTEXT

Executive Summary

The current study essentially ascertains the overall influence of particularly forensic

accounting in addressing deceptive and fraudulent deeds in a bid to make certain

good corporate codes in diverse selected corporation of UK. Forensic accounting

can be indicated as an effectual tool for addressing financial crimes in business

concerns. In addition to this, forensic audit helps in making certain corporate

governance in particular business concerns. Founded on this, the study suggested

that firms need to implement forensic accounting in order to add to the efforts of

decreasing fraudulent actions for making certain good corporate governance code in

retail business concerns.

3

ACCOUNTING IN CONTEXT

Table of Contents

Context..........................................................................................................................3

Decision that the Financial Director has asked for.......................................................5

Key Issues....................................................................................................................5

Synthesis of the arguments from the articles...............................................................7

Suggestions................................................................................................................13

References.................................................................................................................14

ACCOUNTING IN CONTEXT

Table of Contents

Context..........................................................................................................................3

Decision that the Financial Director has asked for.......................................................5

Key Issues....................................................................................................................5

Synthesis of the arguments from the articles...............................................................7

Suggestions................................................................................................................13

References.................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

ACCOUNTING IN CONTEXT

Effect of forensic accounting as an important tool for prevention of fraud in

selected firm of UK

Context

Background of the Study

The business world has continued to experience several scandals regularly that

again have led to loss of asset as well as money for company’s shareholders.

Forensic accounting indicates towards the use of diverse accounting skills that can

be used to examine fraud or embezzlement and assess particular financial

information for use in different legal proceedings. The current study takes into

consideration the operations of the retail corporation, a British supermarket giant.

The serious fraud office essentially has launched specific investigations undertaken

by the watchdogs and this can exceed examination by the Financial Conduct

Authority (Mehta and Bhavani 2017). Essentially, retail corporations have been co-

effective fully and can continue to do undertake investigations. The scandal of retail

corporations essentially initiated SFO to undertake criminal examination into

practices of accounting at particularly Tesco Plc. The present study analyses primary

context of the study that explains the structure of the corporation that is taken into

account for the current study. Moving further, the current study explains key issues

that illustrate all the research questions, synthesis of specific arguments from the

selected articles and presents then recommendations.

Organization Structure of the firm

Retail corporations (for example, Tesco plc) are British transnational groceries that

markets general products. The company follows a specific hierarchical structure of

organization. Particularly, in this specific structure, both positions along with

obligations are necessarily divided into different parts to make certain that work will

be undertaken efficiently as well as smoothly. Essentially, the ones operating at the

top echelon of the business pyramid have the optimum accountabilities as well as

authorities. In this retail firm operating in UK, the Board of Directors consists of

minimum 10 members and considerable alterations can happen on the board

particularly during a particular period of time. The company has an appointed CEO

(chief executive officer), CFO (Chief Financial Officer) and specific numbers of Non-

Executive Directors along with Non-Executive Officer. The organization structure of

the retail firm operating in UK (for say, Tesco plc) necessarily contains different

committees that report to the board of the company. Again the members of the

executive committee are primarily led by the chief of the group. The organizational

framework of the retail firm can be considered to be highly hierarchical reflecting the

wide scope of the business (Nigrini 2016). There are four different layers of

administration within a specific store that can generate annoying bureaucracy with a

bad influence on the entire process of coordination as well as collaboration among

managers of the corporation. Therefore, it is recommended that reduction of the

layers of management of the firm can be done for creating higher flexibility along with

faster information flow.

ACCOUNTING IN CONTEXT

Effect of forensic accounting as an important tool for prevention of fraud in

selected firm of UK

Context

Background of the Study

The business world has continued to experience several scandals regularly that

again have led to loss of asset as well as money for company’s shareholders.

Forensic accounting indicates towards the use of diverse accounting skills that can

be used to examine fraud or embezzlement and assess particular financial

information for use in different legal proceedings. The current study takes into

consideration the operations of the retail corporation, a British supermarket giant.

The serious fraud office essentially has launched specific investigations undertaken

by the watchdogs and this can exceed examination by the Financial Conduct

Authority (Mehta and Bhavani 2017). Essentially, retail corporations have been co-

effective fully and can continue to do undertake investigations. The scandal of retail

corporations essentially initiated SFO to undertake criminal examination into

practices of accounting at particularly Tesco Plc. The present study analyses primary

context of the study that explains the structure of the corporation that is taken into

account for the current study. Moving further, the current study explains key issues

that illustrate all the research questions, synthesis of specific arguments from the

selected articles and presents then recommendations.

Organization Structure of the firm

Retail corporations (for example, Tesco plc) are British transnational groceries that

markets general products. The company follows a specific hierarchical structure of

organization. Particularly, in this specific structure, both positions along with

obligations are necessarily divided into different parts to make certain that work will

be undertaken efficiently as well as smoothly. Essentially, the ones operating at the

top echelon of the business pyramid have the optimum accountabilities as well as

authorities. In this retail firm operating in UK, the Board of Directors consists of

minimum 10 members and considerable alterations can happen on the board

particularly during a particular period of time. The company has an appointed CEO

(chief executive officer), CFO (Chief Financial Officer) and specific numbers of Non-

Executive Directors along with Non-Executive Officer. The organization structure of

the retail firm operating in UK (for say, Tesco plc) necessarily contains different

committees that report to the board of the company. Again the members of the

executive committee are primarily led by the chief of the group. The organizational

framework of the retail firm can be considered to be highly hierarchical reflecting the

wide scope of the business (Nigrini 2016). There are four different layers of

administration within a specific store that can generate annoying bureaucracy with a

bad influence on the entire process of coordination as well as collaboration among

managers of the corporation. Therefore, it is recommended that reduction of the

layers of management of the firm can be done for creating higher flexibility along with

faster information flow.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

ACCOUNTING IN CONTEXT

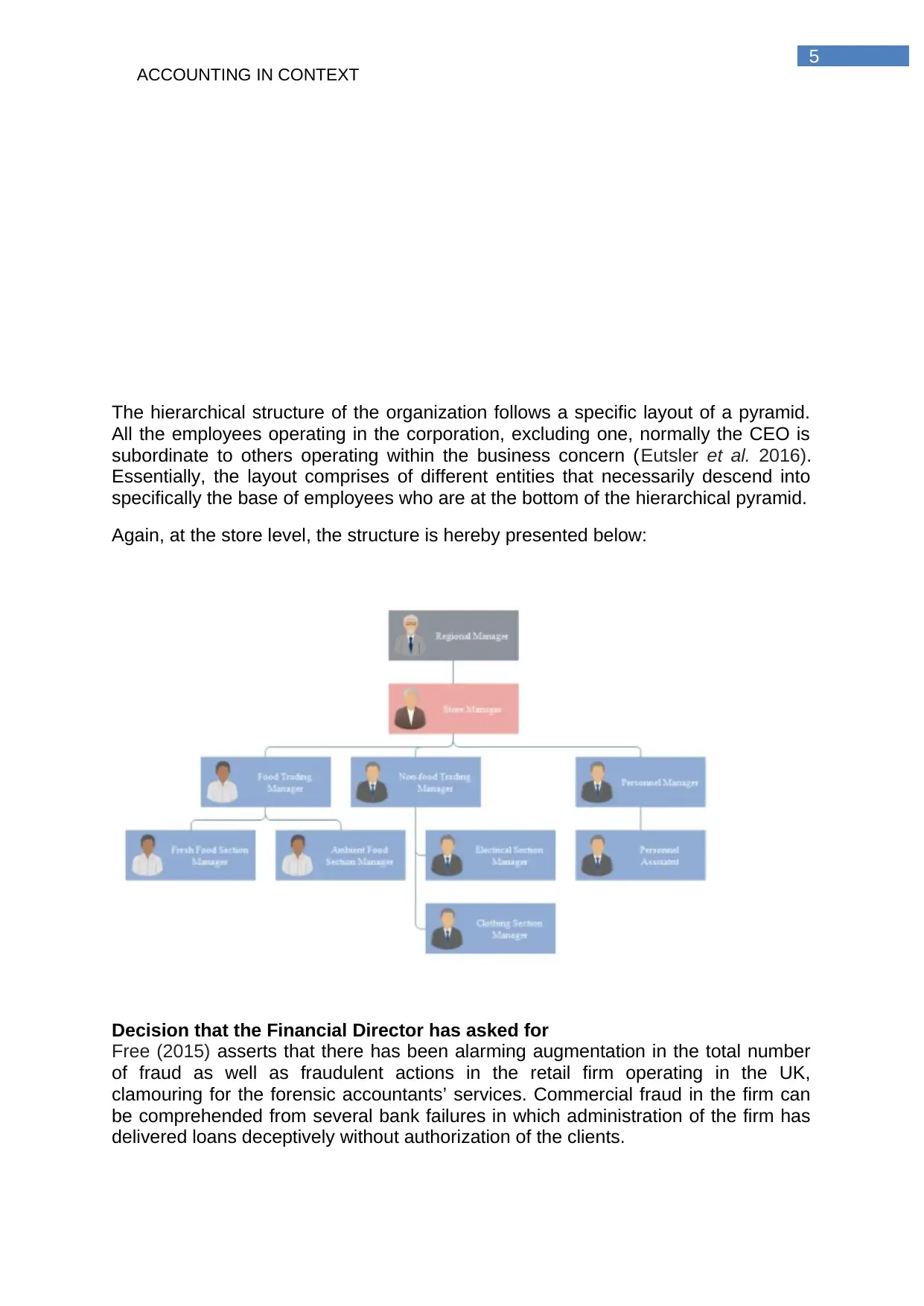

The hierarchical structure of the organization follows a specific layout of a pyramid.

All the employees operating in the corporation, excluding one, normally the CEO is

subordinate to others operating within the business concern (Eutsler et al. 2016).

Essentially, the layout comprises of different entities that necessarily descend into

specifically the base of employees who are at the bottom of the hierarchical pyramid.

Again, at the store level, the structure is hereby presented below:

Decision that the Financial Director has asked for

Free (2015) asserts that there has been alarming augmentation in the total number

of fraud as well as fraudulent actions in the retail firm operating in the UK,

clamouring for the forensic accountants’ services. Commercial fraud in the firm can

be comprehended from several bank failures in which administration of the firm has

delivered loans deceptively without authorization of the clients.

ACCOUNTING IN CONTEXT

The hierarchical structure of the organization follows a specific layout of a pyramid.

All the employees operating in the corporation, excluding one, normally the CEO is

subordinate to others operating within the business concern (Eutsler et al. 2016).

Essentially, the layout comprises of different entities that necessarily descend into

specifically the base of employees who are at the bottom of the hierarchical pyramid.

Again, at the store level, the structure is hereby presented below:

Decision that the Financial Director has asked for

Free (2015) asserts that there has been alarming augmentation in the total number

of fraud as well as fraudulent actions in the retail firm operating in the UK,

clamouring for the forensic accountants’ services. Commercial fraud in the firm can

be comprehended from several bank failures in which administration of the firm has

delivered loans deceptively without authorization of the clients.

6

ACCOUNTING IN CONTEXT

The financial director of the company (in this case a retail firm) essentially intends to

study the way forensic and investigative accounting can help in detecting accounting

fraud and addressing the issue. The director of the firm intends to comprehend the

way forensic accounting can augment financial skills along with investigative

mentality that in turn can assist in various legal aspects and a specialised accounting

field (Seda and Kramer 2015). Additionally, the financial director is also keen to

investigate the engagements that stem from litigation and the way forensic

accounting can be observed as a specific feature of accounting that can fittingly

analyse legal matters and can offer higher assurance level. As per previous reports,

it can be hereby said that system of forensic accounting can be utilized to overturn

all the seepages that lead to collapse of business concerns. Fundamentally, forensic

accounting exercises try to find out errors, participate in various operational vagaries

along with unexpected transactions before they develop into fraud.

Key Issues

The key issues are to analytically examine overall impact of forensic accounting in

addressing fraudulent actions in a bid to make certain good corporate governance

exercises. In addition to this, the study also intends to examine the overall extent to

which forensic accounting can help in combating diverse fraudulent actions and

analyse the way the same can influence the governance of different business

concerns. In addition to this, credibility of processes of external audit has been

questioned in diverse nations (Herbert et al. 2017). Essentially, this can be

evidenced by wide spread criticism directed to different external assessors. The

causes for criticism are mainly loss of faith by primarily public to external audit owing

to different financial scandals along with mega frauds that has directed the way

towards big corporations leading to investment along with property loss.

Again, with enhancement in the volume of business transactions and augmentation

in the size of business concerns, the accountability of external audit has transformed

from ascertaining the true as well as correctness of financial assertion to true and fair

reporting. Essentially, this drifting of accountability has made process of detection

and deterrent of fraud less viable. Essentially the profession of audit mentions that

management has primary accountability of detection as well as fraud prevention in

the corporation. Even though engagement of audit might be planned with

professional scepticism identifying that fraud might be prevalent and this might

possibly make financial assertions materially incorrect. Again, this does not assure

detection of fraud. Essentially, failure of statutory audits for the purpose of detection,

prevention and exposal of frauds can make accountant as well as legal practitioners

to discover better ways to avert fraud from occurring and exposing them when they

happen (Asare et al. 2015). Intrinsically, this has directed the way towards increase

of forensic accounting as a profession. Forensic accounting engage the entire

procedure of undertaking forensic assessment, counting preparation of specialist

report and witness statement and potentially acting as a specialist witness in legal

happenings. Various researches undertaken on the subject of forensic accounting

essentially comprise of the rationale of utilizing forensic accounting on decrease of

gap of audit expectation. Lee et al. (2015) stated that introduction of particularly

forensic audit was an important mechanism in lessening audit expectation gap. ()

suggests that the influence of the forensic accounting services on fraud detection as

well as deterrence. Application of foreign accounting services directed to the

increase of fraud deterrence. Ezejiofor et al. (2016) examined that studies instituted

ACCOUNTING IN CONTEXT

The financial director of the company (in this case a retail firm) essentially intends to

study the way forensic and investigative accounting can help in detecting accounting

fraud and addressing the issue. The director of the firm intends to comprehend the

way forensic accounting can augment financial skills along with investigative

mentality that in turn can assist in various legal aspects and a specialised accounting

field (Seda and Kramer 2015). Additionally, the financial director is also keen to

investigate the engagements that stem from litigation and the way forensic

accounting can be observed as a specific feature of accounting that can fittingly

analyse legal matters and can offer higher assurance level. As per previous reports,

it can be hereby said that system of forensic accounting can be utilized to overturn

all the seepages that lead to collapse of business concerns. Fundamentally, forensic

accounting exercises try to find out errors, participate in various operational vagaries

along with unexpected transactions before they develop into fraud.

Key Issues

The key issues are to analytically examine overall impact of forensic accounting in

addressing fraudulent actions in a bid to make certain good corporate governance

exercises. In addition to this, the study also intends to examine the overall extent to

which forensic accounting can help in combating diverse fraudulent actions and

analyse the way the same can influence the governance of different business

concerns. In addition to this, credibility of processes of external audit has been

questioned in diverse nations (Herbert et al. 2017). Essentially, this can be

evidenced by wide spread criticism directed to different external assessors. The

causes for criticism are mainly loss of faith by primarily public to external audit owing

to different financial scandals along with mega frauds that has directed the way

towards big corporations leading to investment along with property loss.

Again, with enhancement in the volume of business transactions and augmentation

in the size of business concerns, the accountability of external audit has transformed

from ascertaining the true as well as correctness of financial assertion to true and fair

reporting. Essentially, this drifting of accountability has made process of detection

and deterrent of fraud less viable. Essentially the profession of audit mentions that

management has primary accountability of detection as well as fraud prevention in

the corporation. Even though engagement of audit might be planned with

professional scepticism identifying that fraud might be prevalent and this might

possibly make financial assertions materially incorrect. Again, this does not assure

detection of fraud. Essentially, failure of statutory audits for the purpose of detection,

prevention and exposal of frauds can make accountant as well as legal practitioners

to discover better ways to avert fraud from occurring and exposing them when they

happen (Asare et al. 2015). Intrinsically, this has directed the way towards increase

of forensic accounting as a profession. Forensic accounting engage the entire

procedure of undertaking forensic assessment, counting preparation of specialist

report and witness statement and potentially acting as a specialist witness in legal

happenings. Various researches undertaken on the subject of forensic accounting

essentially comprise of the rationale of utilizing forensic accounting on decrease of

gap of audit expectation. Lee et al. (2015) stated that introduction of particularly

forensic audit was an important mechanism in lessening audit expectation gap. ()

suggests that the influence of the forensic accounting services on fraud detection as

well as deterrence. Application of foreign accounting services directed to the

increase of fraud deterrence. Ezejiofor et al. (2016) examined that studies instituted

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

ACCOUNTING IN CONTEXT

that preventive, training, identification, prosecution and investigation stratagem are

utilized in handling fraud nuisance.

Fleming et al. (2016) asserted that there are several researches who have asserted

about the influence of forensic accounting service in the process of fraud prevention

both globally as well as regionally. However, with augmentation in frauds and

ensuing losses, the study intends to institute the significance of forensic accounting

services in detecting and overcoming fraud in the particular sector. Again, at the time

when public can be made aware of the entire theme, then in that case they can

actually demand for the service that they invest in. Therefore, it is from this identified

gap in research that the study intends to seek solution to the question whether

forensic accounting services can prove to be effective in fraud prevention in specific

fields of business.

Objective of the research

The objective of the current research is as stated below:

- To institute the way and the extent to which forensic accounting can exert

impact on the process of fraud prevention in retail firm operating in UK

Research Questions

The research questions formulated for the current study are as presented below:

- Can the system of forensic accounting be considered to be an effectual tool

for dealing with the issues of pecuniary offences in business concerns?

- Is it essential to carry out forensic audit for the purpose of ensuring good

corporate governance code in corporations?

Synthesis of the arguments from the articles

Numerous academic scholars have come across the expression “Forensic

Accounting”. McMahon et al. (2016) considered the term forensic accounting as a

painstaking exercise of gathering data and analysing diverse sections of provision of

support for the purpose of litigation, consultation and examination of fraud. As

rihghtly indicated by Popoola et al. (2016), forensic investigation can help in the

process of ascertainment as well as institution of various facts that can support legal

matters. Using forensic accounting is about detection and investigation of a crime in

a bid to divulge all the attending characteristics and identification of offenders.

Therefore, as per the views of Popoola et al. (2016), system of forensic accounting

can be regarded as the process of inferring, summing up and reflecting intricate

pecuniary subjects appropriately, precisely as well as factually particularly in the

court of law as a specialist. In this connection it can be said that accounting and

particularly forensic accounting is adequately thorough and inclusive that in turn can

help in individual professional judgement as regards different financial items in the

books of accounts of firms and inventories. This in turn helps in presentation of

higher quality that can remain sustainable in different adversarial lawful proceedings

or else administrative evaluation.

As per the International Journal of Academic Research in Management and

Business by McMahon et al. (2016), forensic accountants possess skills as well as

training to understand the apparent numbers and go beyond the apparent numbers

ACCOUNTING IN CONTEXT

that preventive, training, identification, prosecution and investigation stratagem are

utilized in handling fraud nuisance.

Fleming et al. (2016) asserted that there are several researches who have asserted

about the influence of forensic accounting service in the process of fraud prevention

both globally as well as regionally. However, with augmentation in frauds and

ensuing losses, the study intends to institute the significance of forensic accounting

services in detecting and overcoming fraud in the particular sector. Again, at the time

when public can be made aware of the entire theme, then in that case they can

actually demand for the service that they invest in. Therefore, it is from this identified

gap in research that the study intends to seek solution to the question whether

forensic accounting services can prove to be effective in fraud prevention in specific

fields of business.

Objective of the research

The objective of the current research is as stated below:

- To institute the way and the extent to which forensic accounting can exert

impact on the process of fraud prevention in retail firm operating in UK

Research Questions

The research questions formulated for the current study are as presented below:

- Can the system of forensic accounting be considered to be an effectual tool

for dealing with the issues of pecuniary offences in business concerns?

- Is it essential to carry out forensic audit for the purpose of ensuring good

corporate governance code in corporations?

Synthesis of the arguments from the articles

Numerous academic scholars have come across the expression “Forensic

Accounting”. McMahon et al. (2016) considered the term forensic accounting as a

painstaking exercise of gathering data and analysing diverse sections of provision of

support for the purpose of litigation, consultation and examination of fraud. As

rihghtly indicated by Popoola et al. (2016), forensic investigation can help in the

process of ascertainment as well as institution of various facts that can support legal

matters. Using forensic accounting is about detection and investigation of a crime in

a bid to divulge all the attending characteristics and identification of offenders.

Therefore, as per the views of Popoola et al. (2016), system of forensic accounting

can be regarded as the process of inferring, summing up and reflecting intricate

pecuniary subjects appropriately, precisely as well as factually particularly in the

court of law as a specialist. In this connection it can be said that accounting and

particularly forensic accounting is adequately thorough and inclusive that in turn can

help in individual professional judgement as regards different financial items in the

books of accounts of firms and inventories. This in turn helps in presentation of

higher quality that can remain sustainable in different adversarial lawful proceedings

or else administrative evaluation.

As per the International Journal of Academic Research in Management and

Business by McMahon et al. (2016), forensic accountants possess skills as well as

training to understand the apparent numbers and go beyond the apparent numbers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

ACCOUNTING IN CONTEXT

to manage different business actualities of various circumstances. Analytical

evaluation, analysis, summarization along with arrangement of intricate pecuniary

business associated issues is prominent characteristics of the occupation. Thus,

services of forensic accounting utilize the skills and competence of practitioners in

the areas of financial accounting, auditing, and management of tax as well as other

skills.

Forensic Assessor and forensic accounting

As rightly put forward by Huang et al. (2017), forensic auditors are essentially the

experts in the field of financial matters who are appropriately trained in the process

of detection, investigation as well as deterrence of fraud along with white collar

offence that need to be put forward for legal proceedings to the court or public

debate. Therefore, auditors in forensic area are necessarily specialists in various

monetary aspects who are well skilled in the areas of detection, investigation and

deterrence of fraud along with white collar crimes. On the other hand, as per AICPA,

services of forensic accounting normally involve implementation of particular skills in

audit, various quantitative mechanisms, business, particular areas of law, advanced

information as well as computer expertises in handling new technologies,

investigative and skills of research to pull together evaluate and analyse evidential

matter that in the field of forensic examination is termed as evidence. Forensic

auditor possesses skills and proficiency and can be said to undertake examination

on financial matter that might be utilized in court of law. As suggested by Bhasin

(2016), it is accountability of administration to place particular system in position by

which internal fraud can be minimised otherwise entirely wiped out from the system.

Essentially, an appropriate system of internal control can play a veritable role in

detection of the fraud, waste as well as abuse that take place within the corporation

and might engage different employees, contract members of staff else wise vendors.

Instances of internal fraud include falsification of figures, lifting of stores, store lifting

and many others.

Financial Fraud

According to Bolt-Lee and Kern (2015), financial scam can be considered as an

offence regarding deception for acquiring money otherwise different products

unlawfully. Again, fraud can be identified as the criminal activity carried out against

property, including unlawful translation of property belonging to others. Fraud is also

said to include cronyism, political donation, bribes, setting artificial process of pricing

along with frauds of different kinds. EFCC Act intends to capture a wide variety of

different economic as well as financial crimes observed both within as well as

outside business concerns. In essence, Dilla and Raschke (2015) defines fraudulent

actions as illegal acts that can violate different subsisting legislation and can include

any kind of frauds starting from trafficking, bribery and looting, money laundering,

use of narcotics and any kind of corrupt unprofessional conducts counting currency,

piracy, theft of firm’s intellectual property, dumping of different harmful and toxic

waste or prohibited goods and many others. Dilla and Raschke (2015) are of the

opinion that financial fraud in business concerns can differ widely in features and

mechanisms of operation. In itself, fraud can also be categorised into two different

manners that includes feature of fraudsters and mechanisms implemented in

undertaking the fraudulent action. Based on the nature as well as characteristics of

the offenders, fraud can also be categorised into three different groups, such as

ACCOUNTING IN CONTEXT

to manage different business actualities of various circumstances. Analytical

evaluation, analysis, summarization along with arrangement of intricate pecuniary

business associated issues is prominent characteristics of the occupation. Thus,

services of forensic accounting utilize the skills and competence of practitioners in

the areas of financial accounting, auditing, and management of tax as well as other

skills.

Forensic Assessor and forensic accounting

As rightly put forward by Huang et al. (2017), forensic auditors are essentially the

experts in the field of financial matters who are appropriately trained in the process

of detection, investigation as well as deterrence of fraud along with white collar

offence that need to be put forward for legal proceedings to the court or public

debate. Therefore, auditors in forensic area are necessarily specialists in various

monetary aspects who are well skilled in the areas of detection, investigation and

deterrence of fraud along with white collar crimes. On the other hand, as per AICPA,

services of forensic accounting normally involve implementation of particular skills in

audit, various quantitative mechanisms, business, particular areas of law, advanced

information as well as computer expertises in handling new technologies,

investigative and skills of research to pull together evaluate and analyse evidential

matter that in the field of forensic examination is termed as evidence. Forensic

auditor possesses skills and proficiency and can be said to undertake examination

on financial matter that might be utilized in court of law. As suggested by Bhasin

(2016), it is accountability of administration to place particular system in position by

which internal fraud can be minimised otherwise entirely wiped out from the system.

Essentially, an appropriate system of internal control can play a veritable role in

detection of the fraud, waste as well as abuse that take place within the corporation

and might engage different employees, contract members of staff else wise vendors.

Instances of internal fraud include falsification of figures, lifting of stores, store lifting

and many others.

Financial Fraud

According to Bolt-Lee and Kern (2015), financial scam can be considered as an

offence regarding deception for acquiring money otherwise different products

unlawfully. Again, fraud can be identified as the criminal activity carried out against

property, including unlawful translation of property belonging to others. Fraud is also

said to include cronyism, political donation, bribes, setting artificial process of pricing

along with frauds of different kinds. EFCC Act intends to capture a wide variety of

different economic as well as financial crimes observed both within as well as

outside business concerns. In essence, Dilla and Raschke (2015) defines fraudulent

actions as illegal acts that can violate different subsisting legislation and can include

any kind of frauds starting from trafficking, bribery and looting, money laundering,

use of narcotics and any kind of corrupt unprofessional conducts counting currency,

piracy, theft of firm’s intellectual property, dumping of different harmful and toxic

waste or prohibited goods and many others. Dilla and Raschke (2015) are of the

opinion that financial fraud in business concerns can differ widely in features and

mechanisms of operation. In itself, fraud can also be categorised into two different

manners that includes feature of fraudsters and mechanisms implemented in

undertaking the fraudulent action. Based on the nature as well as characteristics of

the offenders, fraud can also be categorised into three different groups, such as

9

ACCOUNTING IN CONTEXT

internal fraud, external fraud and mixed fraud. Steventon et al. (2017) suggests that

internal fraud refers to the ones committed by different employees including directors

of business concerns, whilst external fraud refers to the ones committed by

individuals who are not associated to the business concern. Again, missed fraud

indicates towards outsiders who collide with the members of the staff as well as

directors of the corporation.

Forensic Accounting and Instances of financial fraud

As rightly indicated by Chan et al. (2015), forensic accountants can be indicated as

experienced assessors, accountants as well as investigators of legal and pecuniary

documents that are necessarily hired for probing into probable fears of various

fraudulent actions within a corporation. Otherwise they are necessarily hired by a

firm to avert fraudulent actions to take place. Mansor (2015) carried out a

presentation on the condition of operations of certain banks and delivered sordid

particular of banks. According to reports, five different banks were declared to be

solvent with the disclosure that they had mostly corroded funds of the shareholders

and violated particular ratios in banking. As per the report presented by the Centre of

Forensic Studies, the rising need for forensic along with investigative accounting in

the segment of banking stems from the nature of modern day banking that includes

huge volume of intricate data, that in turn makes it difficult to supervise these

transaction by implementing manual processes of audit. According to Bhasin (2015),

this consequently turns the control utility of process of auditing very ineffective.

Impact of forensic auditing on corporate governance codes of firms

As correctly indicated by Van Akkeren and Buckby (2017), statutory audit can be

considered as an audit that is obligatory by law as to put credence to firm’s

pecuniary assertions and make certain that adequate and appropriate pecuniary

declarations have been prepared as required by statutes and regulations.

Essentially, external assessor by law has the need to be appointed by firm’s

shareholders. In most of the cases the management of business concerns can

appoint external auditor on the behalf of shareholders for the purpose of assessment

of books of accounts. In this regard, it can be hereby said that the appointment mode

of different external assessor has negatively affected performance of external

assessors in undertaking the corporate governance functionalities effectually thereby

making financiers to lose confidence in yearly reports presented by firms.

Fundamentally, external auditors are also delivered guidance that has the capability

to enhance quality of audit in detecting different material misstatements in financial

reports. This can in it itself help in the process of detection of fraudulent actions or

else error. In addition to this, this comprises of suggestions that an evaluator might

respond to a detected risk of different material misstatement as well as errors

stemming from fraudulent actions. Adebisi and Gbegi (2015) asserts that failure of

the structure of the corporate communication has made financial community

comprehend that there is a huge requirement for specialised professionals that can

help in the process of identifying, divulging as well as preventing various

weaknesses in three distinct areas namely, poor state of corporate governance, poor

internal control, deceitful financial statement. Nonetheless, these stated

accountabilities have not been properly accepted by assessors, therefore, leading to

corporate fraud and corporate failures together with poor corporate governance. In a

bid to make certain appropriate accountability and avert fraud by the administration,

ACCOUNTING IN CONTEXT

internal fraud, external fraud and mixed fraud. Steventon et al. (2017) suggests that

internal fraud refers to the ones committed by different employees including directors

of business concerns, whilst external fraud refers to the ones committed by

individuals who are not associated to the business concern. Again, missed fraud

indicates towards outsiders who collide with the members of the staff as well as

directors of the corporation.

Forensic Accounting and Instances of financial fraud

As rightly indicated by Chan et al. (2015), forensic accountants can be indicated as

experienced assessors, accountants as well as investigators of legal and pecuniary

documents that are necessarily hired for probing into probable fears of various

fraudulent actions within a corporation. Otherwise they are necessarily hired by a

firm to avert fraudulent actions to take place. Mansor (2015) carried out a

presentation on the condition of operations of certain banks and delivered sordid

particular of banks. According to reports, five different banks were declared to be

solvent with the disclosure that they had mostly corroded funds of the shareholders

and violated particular ratios in banking. As per the report presented by the Centre of

Forensic Studies, the rising need for forensic along with investigative accounting in

the segment of banking stems from the nature of modern day banking that includes

huge volume of intricate data, that in turn makes it difficult to supervise these

transaction by implementing manual processes of audit. According to Bhasin (2015),

this consequently turns the control utility of process of auditing very ineffective.

Impact of forensic auditing on corporate governance codes of firms

As correctly indicated by Van Akkeren and Buckby (2017), statutory audit can be

considered as an audit that is obligatory by law as to put credence to firm’s

pecuniary assertions and make certain that adequate and appropriate pecuniary

declarations have been prepared as required by statutes and regulations.

Essentially, external assessor by law has the need to be appointed by firm’s

shareholders. In most of the cases the management of business concerns can

appoint external auditor on the behalf of shareholders for the purpose of assessment

of books of accounts. In this regard, it can be hereby said that the appointment mode

of different external assessor has negatively affected performance of external

assessors in undertaking the corporate governance functionalities effectually thereby

making financiers to lose confidence in yearly reports presented by firms.

Fundamentally, external auditors are also delivered guidance that has the capability

to enhance quality of audit in detecting different material misstatements in financial

reports. This can in it itself help in the process of detection of fraudulent actions or

else error. In addition to this, this comprises of suggestions that an evaluator might

respond to a detected risk of different material misstatement as well as errors

stemming from fraudulent actions. Adebisi and Gbegi (2015) asserts that failure of

the structure of the corporate communication has made financial community

comprehend that there is a huge requirement for specialised professionals that can

help in the process of identifying, divulging as well as preventing various

weaknesses in three distinct areas namely, poor state of corporate governance, poor

internal control, deceitful financial statement. Nonetheless, these stated

accountabilities have not been properly accepted by assessors, therefore, leading to

corporate fraud and corporate failures together with poor corporate governance. In a

bid to make certain appropriate accountability and avert fraud by the administration,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

ACCOUNTING IN CONTEXT

the forensic assessors help the management by delivering software packages that

can help management to detect and avert fraud. The executive directors of the firm

are aware of the fact that forensic assessors might be invited to identify and prevent

different fraud. They can also make certain that their business concerns have a

proper system of internal control, checks as well as balances that are transparent, in

that way positively exerting influence on the corporate governance.

Prior notions

Services of forensic accounting can be considered to be immensely important when

legal aspects of a business are involved. As forensic accounting mainly refers to the

usage of specific skills of professional accounting in areas concerning potential or

else actual civil litigation, therefore, the forensic accountant can be involved by

adjuster or else a lawyer for the purpose of auditing books of accounts (Henry and

Ganiyu 2017).

Numerous academic scholars have postulated several theories in their articles that

can help in understanding different fraudulent actions in a specific business

arrangement. Review of prior literature can help in the process of guiding the study

and therefore help in understanding the underlying issues and the ways of relating

the same (Bhasin 2016). There needs to be a mechanism to shield corporations from

fraudulent actions such as incorporating the actions of forensic accounting in the

control environment. Thus, this study also takes into account the utilization of

services of forensic accounting as a way of decreasing frauds in firms particularly in

retail firms operating in the UK.

The themes of White Collar Crime Theory, Fraud scale notions; Hollinger Clark

Notion as well as Cressy Fraud Triangle Theory can help in exploring all the causes

of the financial frauds as the foundation to prevention of various occurrences.

White Collar Crime Theory

As correctly mentioned by Gbegi and Adebisi (2014), white collar crime theory is

credited with formulation and design of white collar crime theory. Essentially, the

theory also argues that particularly crime is not a preserve of different poor

individuals as earlier researchers suggested. In addition to this, Gbegi and Adebisi

(2014) stated that the poverty was hardly ever to the white collar crimes and

therefore is not the prime driver of crime. Again, the theory also attempts to

assimilate the crime of white collar class belonging to the upper class with various

economic as well as business activities. Essentially, the status of different

professionals with a specific community generates an atmosphere of admiration and

threats. There are different members of the community who admire professionals but

are also fearful of tribulation in case if they provoke those individuals. Admiration

along with fear of qualified professionals also leads to less harsher punishment for

criminals belong to white collar class. In essence, the present theory suggests that

the traditional system of criminal justice delivers less harsh punishment to criminals

of the white collar class. As per this notion, crime is usually inculcated from diverse

cross interaction with individuals already participating in various fraudulent actions.

Othman et al. (2015) observed that criminal behaviour can be learned in relation to

the ones who can define this kind of behaviour constructively and with remoteness to

the ones who perceive this kind of behaviour to be unfavourable. As rightly indicated

by Seda and Kramer (2015), the theory is primarily founded on the supposition that a

ACCOUNTING IN CONTEXT

the forensic assessors help the management by delivering software packages that

can help management to detect and avert fraud. The executive directors of the firm

are aware of the fact that forensic assessors might be invited to identify and prevent

different fraud. They can also make certain that their business concerns have a

proper system of internal control, checks as well as balances that are transparent, in

that way positively exerting influence on the corporate governance.

Prior notions

Services of forensic accounting can be considered to be immensely important when

legal aspects of a business are involved. As forensic accounting mainly refers to the

usage of specific skills of professional accounting in areas concerning potential or

else actual civil litigation, therefore, the forensic accountant can be involved by

adjuster or else a lawyer for the purpose of auditing books of accounts (Henry and

Ganiyu 2017).

Numerous academic scholars have postulated several theories in their articles that

can help in understanding different fraudulent actions in a specific business

arrangement. Review of prior literature can help in the process of guiding the study

and therefore help in understanding the underlying issues and the ways of relating

the same (Bhasin 2016). There needs to be a mechanism to shield corporations from

fraudulent actions such as incorporating the actions of forensic accounting in the

control environment. Thus, this study also takes into account the utilization of

services of forensic accounting as a way of decreasing frauds in firms particularly in

retail firms operating in the UK.

The themes of White Collar Crime Theory, Fraud scale notions; Hollinger Clark

Notion as well as Cressy Fraud Triangle Theory can help in exploring all the causes

of the financial frauds as the foundation to prevention of various occurrences.

White Collar Crime Theory

As correctly mentioned by Gbegi and Adebisi (2014), white collar crime theory is

credited with formulation and design of white collar crime theory. Essentially, the

theory also argues that particularly crime is not a preserve of different poor

individuals as earlier researchers suggested. In addition to this, Gbegi and Adebisi

(2014) stated that the poverty was hardly ever to the white collar crimes and

therefore is not the prime driver of crime. Again, the theory also attempts to

assimilate the crime of white collar class belonging to the upper class with various

economic as well as business activities. Essentially, the status of different

professionals with a specific community generates an atmosphere of admiration and

threats. There are different members of the community who admire professionals but

are also fearful of tribulation in case if they provoke those individuals. Admiration

along with fear of qualified professionals also leads to less harsher punishment for

criminals belong to white collar class. In essence, the present theory suggests that

the traditional system of criminal justice delivers less harsh punishment to criminals

of the white collar class. As per this notion, crime is usually inculcated from diverse

cross interaction with individuals already participating in various fraudulent actions.

Othman et al. (2015) observed that criminal behaviour can be learned in relation to

the ones who can define this kind of behaviour constructively and with remoteness to

the ones who perceive this kind of behaviour to be unfavourable. As rightly indicated

by Seda and Kramer (2015), the theory is primarily founded on the supposition that a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

ACCOUNTING IN CONTEXT

individual belonging to the white collar class is likely to receive lenient sentence from

respective court of law in comparison to the street criminals.

Fraud Triangle Theory

As rightly indicated by Rezaee and Wang (2017), the theory evaluates personal

features of a fraudsters in association to fraud that is committed in the corporation.

Rezaee et al. (2016) hypothesised particularly three different criteria for mainly

criminal breaches of trust. Essentially, these comprised of non-sharable pecuniary

issues, knowledge of functioning of a particular enterprise and opportunity to breach

trust. This theory that was developed was referred to as the fraud triangle. The

notion comprises of components that are perceived stress, presence of an

opportunity and consequent rationale of the fraudulent action. Essentially, perceived

pressure from different non sharable pecuniary requirement generates a motive for

diverse fraud. Individuals might be encountering financial else wise other problems,

for example, huge medical bills, victim of drug abuse, alcohol. The individual might

perhaps be leading a very luxurious life that is not necessarily sustainable with their

earnings. Again, sheer greed can also be an important factor and motivator behind

fraud. Rezaee and Wang (2017) are of the view that opportunities are primarily

created by weak system of internal control, bad management oversight and by

means of exploitation of one’s position, power and authority. According to this notion,

chances to commit fraud might happen in case of there is failure on the part of the

management to implement adequate processes for detection of fraudulent actions.

As per the fraud triangle, chance can be considered as the only controllable factor by

a specific business concern and the threat of probable detection can be regarded as

an important facet of detection in the process of prevention of fraud. Again,

rationalization can be regarded as a vital component in majority of cases of fraud.

Fundamentally, the Fraud Triangle theory presents an effective conceptual model

that has widely served as a help to assessors of fraud in comprehending various

antecedents of fraud. Thorough research in this area of fraud revealed the fact that

there existed specific conditions and circumstances of fraud triangle within various

corporations where frauds have been carried out. Assessors of fraud have

necessarily utilised the fraud triangle as a certain standard mechanism since the

period of 1950s to comprehend motivations of fraudsters.

Agency theory

Agency theory can be considered as one of the most important theoretical structure

that can guide the present study. This notion is extensively implemented in the

literature of accounting to illustrate as well as predict the process of appointment

along with external auditors’ and consultants’ performance. Agathee and Ramen

(2017) argues that this concept also delivers an effective theoretical structure for

studying functions of internal assessment. The concept of this theory also aids to

elucidate and forecast the overall subsistence of internal audit together with the roles

and accountabilities that are assigned to various internal assessors by the business

concerns and that agency theory forecasts the way the function of internal

assessment can get affected by the change in the organization. According to Bhasin

(2015), agency theory illustrates business concerns as necessary framework to

maintain agreements, and ways to exercise requisite controls that can minimize

diverse opportunistic behaviour of different agents. In a bid to go with the interests of

ACCOUNTING IN CONTEXT

individual belonging to the white collar class is likely to receive lenient sentence from

respective court of law in comparison to the street criminals.

Fraud Triangle Theory

As rightly indicated by Rezaee and Wang (2017), the theory evaluates personal

features of a fraudsters in association to fraud that is committed in the corporation.

Rezaee et al. (2016) hypothesised particularly three different criteria for mainly

criminal breaches of trust. Essentially, these comprised of non-sharable pecuniary

issues, knowledge of functioning of a particular enterprise and opportunity to breach

trust. This theory that was developed was referred to as the fraud triangle. The

notion comprises of components that are perceived stress, presence of an

opportunity and consequent rationale of the fraudulent action. Essentially, perceived

pressure from different non sharable pecuniary requirement generates a motive for

diverse fraud. Individuals might be encountering financial else wise other problems,

for example, huge medical bills, victim of drug abuse, alcohol. The individual might

perhaps be leading a very luxurious life that is not necessarily sustainable with their

earnings. Again, sheer greed can also be an important factor and motivator behind

fraud. Rezaee and Wang (2017) are of the view that opportunities are primarily

created by weak system of internal control, bad management oversight and by

means of exploitation of one’s position, power and authority. According to this notion,

chances to commit fraud might happen in case of there is failure on the part of the

management to implement adequate processes for detection of fraudulent actions.

As per the fraud triangle, chance can be considered as the only controllable factor by

a specific business concern and the threat of probable detection can be regarded as

an important facet of detection in the process of prevention of fraud. Again,

rationalization can be regarded as a vital component in majority of cases of fraud.

Fundamentally, the Fraud Triangle theory presents an effective conceptual model

that has widely served as a help to assessors of fraud in comprehending various

antecedents of fraud. Thorough research in this area of fraud revealed the fact that

there existed specific conditions and circumstances of fraud triangle within various

corporations where frauds have been carried out. Assessors of fraud have

necessarily utilised the fraud triangle as a certain standard mechanism since the

period of 1950s to comprehend motivations of fraudsters.

Agency theory

Agency theory can be considered as one of the most important theoretical structure

that can guide the present study. This notion is extensively implemented in the

literature of accounting to illustrate as well as predict the process of appointment

along with external auditors’ and consultants’ performance. Agathee and Ramen

(2017) argues that this concept also delivers an effective theoretical structure for

studying functions of internal assessment. The concept of this theory also aids to

elucidate and forecast the overall subsistence of internal audit together with the roles

and accountabilities that are assigned to various internal assessors by the business

concerns and that agency theory forecasts the way the function of internal

assessment can get affected by the change in the organization. According to Bhasin

(2015), agency theory illustrates business concerns as necessary framework to

maintain agreements, and ways to exercise requisite controls that can minimize

diverse opportunistic behaviour of different agents. In a bid to go with the interests of

12

ACCOUNTING IN CONTEXT

the agents as well as principles, an inclusive agreement is basically written for the

purpose of addressing the agents’ as well as principles’ interests.

ACCOUNTING IN CONTEXT

the agents as well as principles, an inclusive agreement is basically written for the

purpose of addressing the agents’ as well as principles’ interests.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.