DFP8v3 Advanced Financial Planning: Building Forster's Wealth Strategy

VerifiedAdded on 2023/04/22

|68

|20631

|447

Case Study

AI Summary

This assignment presents a comprehensive financial planning case study centered around David and Alyssa Forster, a couple seeking advice on building a long-term wealth strategy, particularly in light of Alyssa's recent redundancy and an inheritance. The case details their personal information, assets (including personally held investments, superannuation, shares in a private company, inheritance, and redundancy payment), liabilities, and financial goals. The assignment requires the development of a Statement of Advice (SOA) including cash flow tables and projections, and answering specific questions related to financial planning strategies, investment recommendations, risk management, and estate planning considerations tailored to the Forsters' unique circumstances. The ultimate goal is to provide the Forsters with a robust financial plan that addresses their wealth creation, retirement, and estate planning needs while providing them with peace of mind.

Assignment

Advanced Financial Planning (DFP8_AS_v3)

Student identification(student to complete)

Please complete the fields shaded grey.

Student number

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Result summary(assessor to complete)

First submission Resubmission (if required)

Part 3 Demonstrated Demonstrated

Part 4 Demonstrated Demonstrated

Feedback (assessor to complete)

[insert assessor feedback]

Advanced Financial Planning (DFP8_AS_v3)

Student identification(student to complete)

Please complete the fields shaded grey.

Student number

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Result summary(assessor to complete)

First submission Resubmission (if required)

Part 3 Demonstrated Demonstrated

Part 4 Demonstrated Demonstrated

Feedback (assessor to complete)

[insert assessor feedback]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Before you begin

Read everything in this document before you start your assignment forAdvanced Financial Planning

(DFP8v3).

About this document

This document includes the following four (4)parts:

• Part 1: Instructions for completing and submitting this assignment and statement of competency

• Part 2: The case study

• Part 3: The SOA:

– Statement of advice (SOA) template

– SOA Appendix 1: Cash flow tables (financial position before and after implementation of strategy)

– SOA Appendix 2: Projections and assumptions

• Part 4: Assignment questions (Parts A–G).

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the assignment within your enrolment period. Your study plan is in the KapLearnAdvanced Financial

Planning (DFP8v3) subject room.

Page 2 of 68

Read everything in this document before you start your assignment forAdvanced Financial Planning

(DFP8v3).

About this document

This document includes the following four (4)parts:

• Part 1: Instructions for completing and submitting this assignment and statement of competency

• Part 2: The case study

• Part 3: The SOA:

– Statement of advice (SOA) template

– SOA Appendix 1: Cash flow tables (financial position before and after implementation of strategy)

– SOA Appendix 2: Projections and assumptions

• Part 4: Assignment questions (Parts A–G).

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the assignment within your enrolment period. Your study plan is in the KapLearnAdvanced Financial

Planning (DFP8v3) subject room.

Page 2 of 68

Part 1: Instructions for completing and submitting this

assignment

Completing the assignment

The assignment

For this assignment you are required to complete the following tasks:

In your assessment workbook:

• Review Part 1: Review the key advice in which you are required to be proficient to complete this

assignment.

Part 2: Case study.

• Complete Part 3 (the SOA template), using the data in the case study

– complete SOA Appendix 1 cash flow tables

– complete SOA Appendix 2 projections and assumptions.

• Complete Part 4 (assignment questions) Parts A, B, C, D, E, F and G.

Most of the information and resources to help you answer the questions in this assignment can be found in

your topic notes. Some data will have to be sourcedexternally.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

You will be required to source additional information from other organisations in the financial services

industry to find the appropriate product/s to meet your client/s requirements, and perhaps to calculate

your advicefees.

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber

(e.g. 12345678_DFP8v3_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Page 3 of 68

assignment

Completing the assignment

The assignment

For this assignment you are required to complete the following tasks:

In your assessment workbook:

• Review Part 1: Review the key advice in which you are required to be proficient to complete this

assignment.

Part 2: Case study.

• Complete Part 3 (the SOA template), using the data in the case study

– complete SOA Appendix 1 cash flow tables

– complete SOA Appendix 2 projections and assumptions.

• Complete Part 4 (assignment questions) Parts A, B, C, D, E, F and G.

Most of the information and resources to help you answer the questions in this assignment can be found in

your topic notes. Some data will have to be sourcedexternally.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

You will be required to source additional information from other organisations in the financial services

industry to find the appropriate product/s to meet your client/s requirements, and perhaps to calculate

your advicefees.

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber

(e.g. 12345678_DFP8v3_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Page 3 of 68

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Submitting the assignment

You must submit your completed assignment in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete assignments will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make

any further changes to it.

You can submit your assignment earlier than the deadline if you are confident you have completed all parts

and have prepared a quality submission.

The assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be give an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Advanced Financial Planning (DFP8v3)

subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all the questions in

your assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore, you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed assignment.

How your assignment is graded

Assignment tasks are used to determine your competence in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either ‘competent’ or ‘not yet competent’.

Your assessor will follow the following process when marking your assignment:

• Assess your responses to each question, and its sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, as a whole, your responses to the questions have demonstrated overall competence.

Page 4 of 68

You must submit your completed assignment in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete assignments will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make

any further changes to it.

You can submit your assignment earlier than the deadline if you are confident you have completed all parts

and have prepared a quality submission.

The assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be give an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Advanced Financial Planning (DFP8v3)

subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all the questions in

your assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore, you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed assignment.

How your assignment is graded

Assignment tasks are used to determine your competence in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either ‘competent’ or ‘not yet competent’.

Your assessor will follow the following process when marking your assignment:

• Assess your responses to each question, and its sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, as a whole, your responses to the questions have demonstrated overall competence.

Page 4 of 68

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You need only amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission.

Your assessor will be in a better position to gauge the quality and nature of your changes. Ensure you leave

your first assessor’s comments in your assignment, so your second assessor can see the instructions that

were originally provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This assignment (in conjunction with the SOA presentation) is your opportunity to demonstrate your

competency inthese units:

FNSFPL508 Conduct complex financial planning research

FNSFPL602 Determine client requirements and expectations for clients with complex needs

FNSFPL603 Provide comprehensive monitoring and ongoing service

FNSFPL604 Develop complex and innovative financial planning strategies

FNSFPL605 Present and negotiate complex and innovative financial plans

FNSFPL606 Implement complex and innovative financial plans

FNSCUS505 Determine client requirements and expectations

FNSIAD501 Provide appropriate services, advice and products to clients

We are here to help

If you have any questions about this assignment you can post your query in the ‘Ask your Tutor’ forum in

your subject room. You can expect an answer from one of our technical advisers or student support

staffwithin 24 hours of your posting.

Statement of competency(student to complete)

All students completing this assignment are required to be proficient in the following advice areas:

• tax and estate planning

• superannuation

• insurance and risk protection

• financial planning

• securities.

Page 5 of 68

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You need only amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission.

Your assessor will be in a better position to gauge the quality and nature of your changes. Ensure you leave

your first assessor’s comments in your assignment, so your second assessor can see the instructions that

were originally provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This assignment (in conjunction with the SOA presentation) is your opportunity to demonstrate your

competency inthese units:

FNSFPL508 Conduct complex financial planning research

FNSFPL602 Determine client requirements and expectations for clients with complex needs

FNSFPL603 Provide comprehensive monitoring and ongoing service

FNSFPL604 Develop complex and innovative financial planning strategies

FNSFPL605 Present and negotiate complex and innovative financial plans

FNSFPL606 Implement complex and innovative financial plans

FNSCUS505 Determine client requirements and expectations

FNSIAD501 Provide appropriate services, advice and products to clients

We are here to help

If you have any questions about this assignment you can post your query in the ‘Ask your Tutor’ forum in

your subject room. You can expect an answer from one of our technical advisers or student support

staffwithin 24 hours of your posting.

Statement of competency(student to complete)

All students completing this assignment are required to be proficient in the following advice areas:

• tax and estate planning

• superannuation

• insurance and risk protection

• financial planning

• securities.

Page 5 of 68

Part 2: The casestudy

Background

You work for KeyPlan Pty Ltd, a financial planning company which is an Australian Financial Services Licence

holder and a registered life insurance broker.

Your company has planners who can provide advice in:

• superannuation

• investments and savings plans (including margin lending, securities, derivatives and

managed investments)

• constructing an investment portfolio

• strategic financial planning and asset allocation

• debentures

• retirement planning

• budget and cash flow planning

• debt management

• social security and other government benefits

• salary packaging

• insurance (i.e. life, disability, income protection and trauma)

• deposit and payment products

• estate planning.

Your advice is limited to the areas in which you have completed appropriate accreditation.

KeyPlan does not:

• help to establishself-managed superannuation funds

• provide real estate evaluations and advice

• prepare income tax returns

• undertakesuperannuation fund accounting

• administer superannuation funds

• prepare legal documents such as wills or trusts.

You can assume that you are registered with the Tax Practitioners Board (TPB) as a tax (financial) adviser.

You have organised a meeting with new clients, David and AlyssaForster, who are seeking advice about

their financial situation. Alyssa has just been made redundant from her current employer. This, together

with an inheritance Alyssa is about to receive, has made them concentrate their efforts to build an effective

long-term wealth strategy for their retirement.

David and Alyssawish to become more active investors, but admit they are busy and would rather enjoy

family time than manage investments when they are not working. They are looking for an effective wealth

creation strategy and an estate plan and want peace of mind knowing that their finances are structured to

meet their and the family’s needs.

The following pages detail the information you have obtained from them at your initial meeting.

Page 6 of 68

Background

You work for KeyPlan Pty Ltd, a financial planning company which is an Australian Financial Services Licence

holder and a registered life insurance broker.

Your company has planners who can provide advice in:

• superannuation

• investments and savings plans (including margin lending, securities, derivatives and

managed investments)

• constructing an investment portfolio

• strategic financial planning and asset allocation

• debentures

• retirement planning

• budget and cash flow planning

• debt management

• social security and other government benefits

• salary packaging

• insurance (i.e. life, disability, income protection and trauma)

• deposit and payment products

• estate planning.

Your advice is limited to the areas in which you have completed appropriate accreditation.

KeyPlan does not:

• help to establishself-managed superannuation funds

• provide real estate evaluations and advice

• prepare income tax returns

• undertakesuperannuation fund accounting

• administer superannuation funds

• prepare legal documents such as wills or trusts.

You can assume that you are registered with the Tax Practitioners Board (TPB) as a tax (financial) adviser.

You have organised a meeting with new clients, David and AlyssaForster, who are seeking advice about

their financial situation. Alyssa has just been made redundant from her current employer. This, together

with an inheritance Alyssa is about to receive, has made them concentrate their efforts to build an effective

long-term wealth strategy for their retirement.

David and Alyssawish to become more active investors, but admit they are busy and would rather enjoy

family time than manage investments when they are not working. They are looking for an effective wealth

creation strategy and an estate plan and want peace of mind knowing that their finances are structured to

meet their and the family’s needs.

The following pages detail the information you have obtained from them at your initial meeting.

Page 6 of 68

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

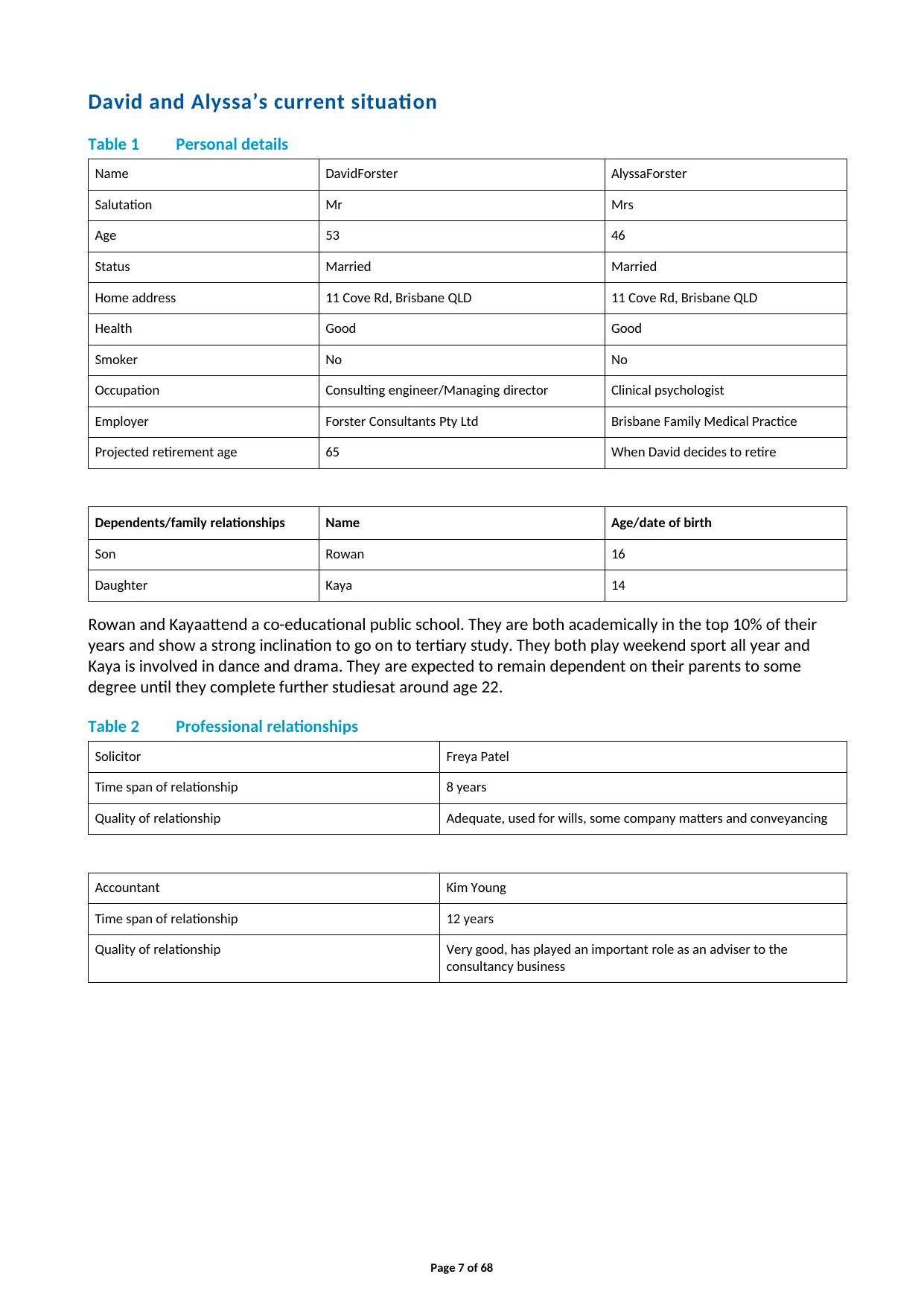

David and Alyssa’s current situation

Table 1 Personal details

Name DavidForster AlyssaForster

Salutation Mr Mrs

Age 53 46

Status Married Married

Home address 11 Cove Rd, Brisbane QLD 11 Cove Rd, Brisbane QLD

Health Good Good

Smoker No No

Occupation Consulting engineer/Managing director Clinical psychologist

Employer Forster Consultants Pty Ltd Brisbane Family Medical Practice

Projected retirement age 65 When David decides to retire

Dependents/family relationships Name Age/date of birth

Son Rowan 16

Daughter Kaya 14

Rowan and Kayaattend a co-educational public school. They are both academically in the top 10% of their

years and show a strong inclination to go on to tertiary study. They both play weekend sport all year and

Kaya is involved in dance and drama. They are expected to remain dependent on their parents to some

degree until they complete further studiesat around age 22.

Table 2 Professional relationships

Solicitor Freya Patel

Time span of relationship 8 years

Quality of relationship Adequate, used for wills, some company matters and conveyancing

Accountant Kim Young

Time span of relationship 12 years

Quality of relationship Very good, has played an important role as an adviser to the

consultancy business

Page 7 of 68

Table 1 Personal details

Name DavidForster AlyssaForster

Salutation Mr Mrs

Age 53 46

Status Married Married

Home address 11 Cove Rd, Brisbane QLD 11 Cove Rd, Brisbane QLD

Health Good Good

Smoker No No

Occupation Consulting engineer/Managing director Clinical psychologist

Employer Forster Consultants Pty Ltd Brisbane Family Medical Practice

Projected retirement age 65 When David decides to retire

Dependents/family relationships Name Age/date of birth

Son Rowan 16

Daughter Kaya 14

Rowan and Kayaattend a co-educational public school. They are both academically in the top 10% of their

years and show a strong inclination to go on to tertiary study. They both play weekend sport all year and

Kaya is involved in dance and drama. They are expected to remain dependent on their parents to some

degree until they complete further studiesat around age 22.

Table 2 Professional relationships

Solicitor Freya Patel

Time span of relationship 8 years

Quality of relationship Adequate, used for wills, some company matters and conveyancing

Accountant Kim Young

Time span of relationship 12 years

Quality of relationship Very good, has played an important role as an adviser to the

consultancy business

Page 7 of 68

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

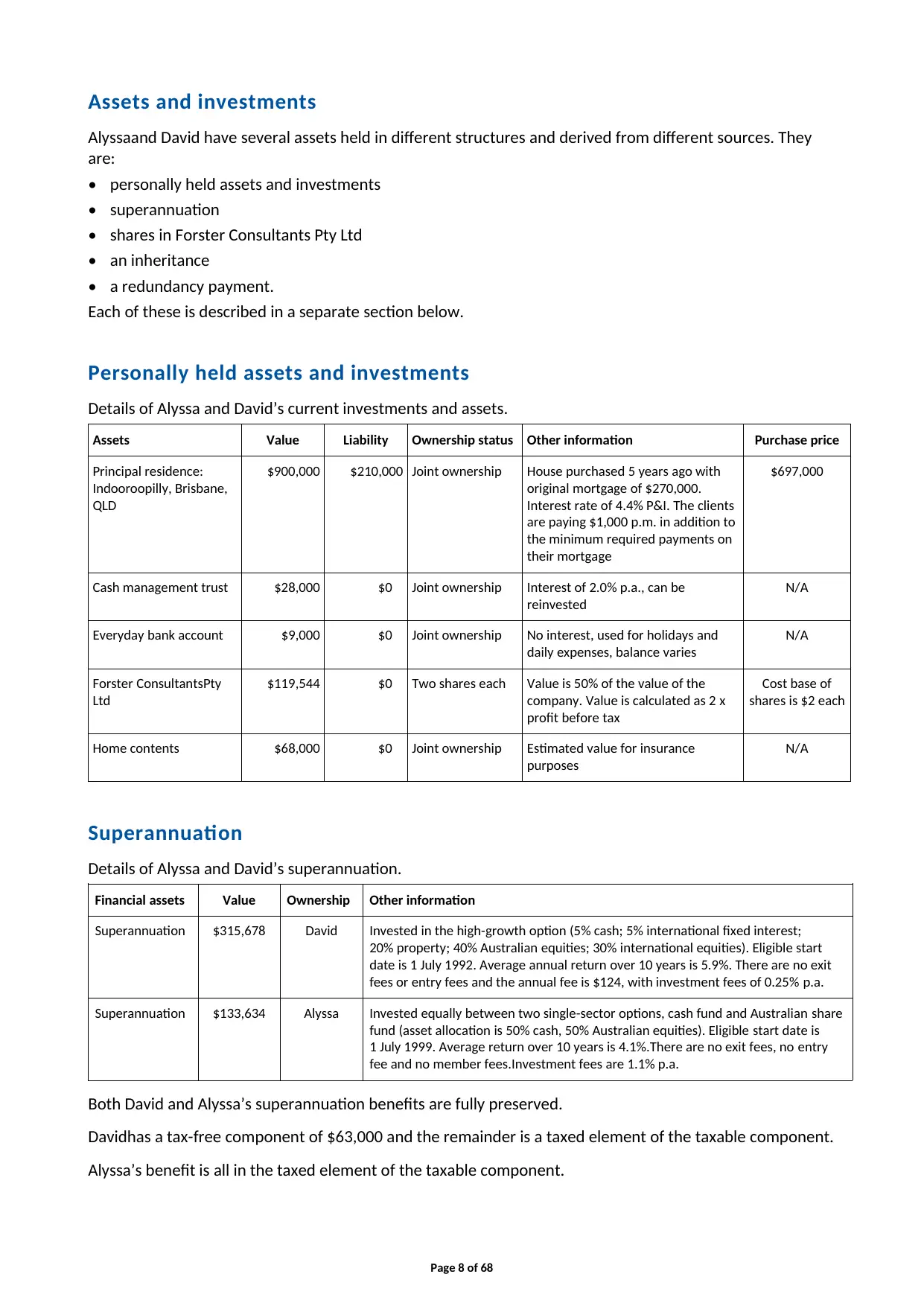

Assets and investments

Alyssaand David have several assets held in different structures and derived from different sources. They

are:

• personally held assets and investments

• superannuation

• shares in Forster Consultants Pty Ltd

• an inheritance

• a redundancy payment.

Each of these is described in a separate section below.

Personally held assets and investments

Details of Alyssa and David’s current investments and assets.

Assets Value Liability Ownership status Other information Purchase price

Principal residence:

Indooroopilly, Brisbane,

QLD

$900,000 $210,000 Joint ownership House purchased 5 years ago with

original mortgage of $270,000.

Interest rate of 4.4% P&I. The clients

are paying $1,000 p.m. in addition to

the minimum required payments on

their mortgage

$697,000

Cash management trust $28,000 $0 Joint ownership Interest of 2.0% p.a., can be

reinvested

N/A

Everyday bank account $9,000 $0 Joint ownership No interest, used for holidays and

daily expenses, balance varies

N/A

Forster ConsultantsPty

Ltd

$119,544 $0 Two shares each Value is 50% of the value of the

company. Value is calculated as 2 x

profit before tax

Cost base of

shares is $2 each

Home contents $68,000 $0 Joint ownership Estimated value for insurance

purposes

N/A

Superannuation

Details of Alyssa and David’s superannuation.

Financial assets Value Ownership Other information

Superannuation $315,678 David Invested in the high-growth option (5% cash; 5% international fixed interest;

20% property; 40% Australian equities; 30% international equities). Eligible start

date is 1 July 1992. Average annual return over 10 years is 5.9%. There are no exit

fees or entry fees and the annual fee is $124, with investment fees of 0.25% p.a.

Superannuation $133,634 Alyssa Invested equally between two single-sector options, cash fund and Australian share

fund (asset allocation is 50% cash, 50% Australian equities). Eligible start date is

1 July 1999. Average return over 10 years is 4.1%.There are no exit fees, no entry

fee and no member fees.Investment fees are 1.1% p.a.

Both David and Alyssa’s superannuation benefits are fully preserved.

Davidhas a tax-free component of $63,000 and the remainder is a taxed element of the taxable component.

Alyssa’s benefit is all in the taxed element of the taxable component.

Page 8 of 68

Alyssaand David have several assets held in different structures and derived from different sources. They

are:

• personally held assets and investments

• superannuation

• shares in Forster Consultants Pty Ltd

• an inheritance

• a redundancy payment.

Each of these is described in a separate section below.

Personally held assets and investments

Details of Alyssa and David’s current investments and assets.

Assets Value Liability Ownership status Other information Purchase price

Principal residence:

Indooroopilly, Brisbane,

QLD

$900,000 $210,000 Joint ownership House purchased 5 years ago with

original mortgage of $270,000.

Interest rate of 4.4% P&I. The clients

are paying $1,000 p.m. in addition to

the minimum required payments on

their mortgage

$697,000

Cash management trust $28,000 $0 Joint ownership Interest of 2.0% p.a., can be

reinvested

N/A

Everyday bank account $9,000 $0 Joint ownership No interest, used for holidays and

daily expenses, balance varies

N/A

Forster ConsultantsPty

Ltd

$119,544 $0 Two shares each Value is 50% of the value of the

company. Value is calculated as 2 x

profit before tax

Cost base of

shares is $2 each

Home contents $68,000 $0 Joint ownership Estimated value for insurance

purposes

N/A

Superannuation

Details of Alyssa and David’s superannuation.

Financial assets Value Ownership Other information

Superannuation $315,678 David Invested in the high-growth option (5% cash; 5% international fixed interest;

20% property; 40% Australian equities; 30% international equities). Eligible start

date is 1 July 1992. Average annual return over 10 years is 5.9%. There are no exit

fees or entry fees and the annual fee is $124, with investment fees of 0.25% p.a.

Superannuation $133,634 Alyssa Invested equally between two single-sector options, cash fund and Australian share

fund (asset allocation is 50% cash, 50% Australian equities). Eligible start date is

1 July 1999. Average return over 10 years is 4.1%.There are no exit fees, no entry

fee and no member fees.Investment fees are 1.1% p.a.

Both David and Alyssa’s superannuation benefits are fully preserved.

Davidhas a tax-free component of $63,000 and the remainder is a taxed element of the taxable component.

Alyssa’s benefit is all in the taxed element of the taxable component.

Page 8 of 68

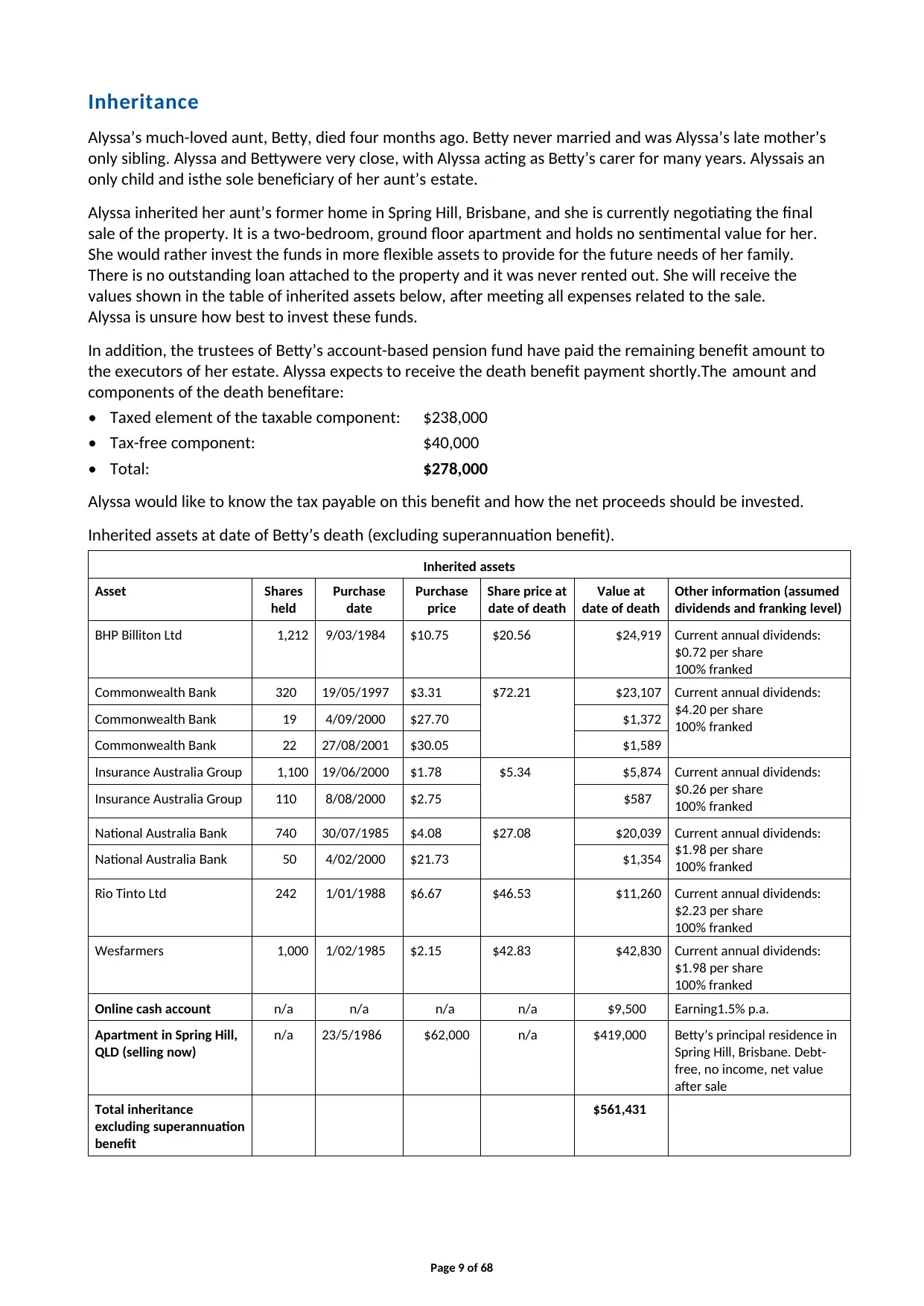

Inheritance

Alyssa’s much-loved aunt, Betty, died four months ago. Betty never married and was Alyssa’s late mother’s

only sibling. Alyssa and Bettywere very close, with Alyssa acting as Betty’s carer for many years. Alyssais an

only child and isthe sole beneficiary of her aunt’s estate.

Alyssa inherited her aunt’s former home in Spring Hill, Brisbane, and she is currently negotiating the final

sale of the property. It is a two-bedroom, ground floor apartment and holds no sentimental value for her.

She would rather invest the funds in more flexible assets to provide for the future needs of her family.

There is no outstanding loan attached to the property and it was never rented out. She will receive the

values shown in the table of inherited assets below, after meeting all expenses related to the sale.

Alyssa is unsure how best to invest these funds.

In addition, the trustees of Betty’s account-based pension fund have paid the remaining benefit amount to

the executors of her estate. Alyssa expects to receive the death benefit payment shortly.The amount and

components of the death benefitare:

• Taxed element of the taxable component: $238,000

• Tax-free component: $40,000

• Total: $278,000

Alyssa would like to know the tax payable on this benefit and how the net proceeds should be invested.

Inherited assets at date of Betty’s death (excluding superannuation benefit).

Inherited assets

Asset Shares

held

Purchase

date

Purchase

price

Share price at

date of death

Value at

date of death

Other information (assumed

dividends and franking level)

BHP Billiton Ltd 1,212 9/03/1984 $10.75 $20.56 $24,919 Current annual dividends:

$0.72 per share

100% franked

Commonwealth Bank 320 19/05/1997 $3.31 $72.21 $23,107 Current annual dividends:

$4.20 per share

100% franked

Commonwealth Bank 19 4/09/2000 $27.70 $1,372

Commonwealth Bank 22 27/08/2001 $30.05 $1,589

Insurance Australia Group 1,100 19/06/2000 $1.78 $5.34 $5,874 Current annual dividends:

$0.26 per share

100% franked

Insurance Australia Group 110 8/08/2000 $2.75 $587

National Australia Bank 740 30/07/1985 $4.08 $27.08 $20,039 Current annual dividends:

$1.98 per share

100% franked

National Australia Bank 50 4/02/2000 $21.73 $1,354

Rio Tinto Ltd 242 1/01/1988 $6.67 $46.53 $11,260 Current annual dividends:

$2.23 per share

100% franked

Wesfarmers 1,000 1/02/1985 $2.15 $42.83 $42,830 Current annual dividends:

$1.98 per share

100% franked

Online cash account n/a n/a n/a n/a $9,500 Earning1.5% p.a.

Apartment in Spring Hill,

QLD (selling now)

n/a 23/5/1986 $62,000 n/a $419,000 Betty’s principal residence in

Spring Hill, Brisbane. Debt-

free, no income, net value

after sale

Total inheritance

excluding superannuation

benefit

$561,431

Page 9 of 68

Alyssa’s much-loved aunt, Betty, died four months ago. Betty never married and was Alyssa’s late mother’s

only sibling. Alyssa and Bettywere very close, with Alyssa acting as Betty’s carer for many years. Alyssais an

only child and isthe sole beneficiary of her aunt’s estate.

Alyssa inherited her aunt’s former home in Spring Hill, Brisbane, and she is currently negotiating the final

sale of the property. It is a two-bedroom, ground floor apartment and holds no sentimental value for her.

She would rather invest the funds in more flexible assets to provide for the future needs of her family.

There is no outstanding loan attached to the property and it was never rented out. She will receive the

values shown in the table of inherited assets below, after meeting all expenses related to the sale.

Alyssa is unsure how best to invest these funds.

In addition, the trustees of Betty’s account-based pension fund have paid the remaining benefit amount to

the executors of her estate. Alyssa expects to receive the death benefit payment shortly.The amount and

components of the death benefitare:

• Taxed element of the taxable component: $238,000

• Tax-free component: $40,000

• Total: $278,000

Alyssa would like to know the tax payable on this benefit and how the net proceeds should be invested.

Inherited assets at date of Betty’s death (excluding superannuation benefit).

Inherited assets

Asset Shares

held

Purchase

date

Purchase

price

Share price at

date of death

Value at

date of death

Other information (assumed

dividends and franking level)

BHP Billiton Ltd 1,212 9/03/1984 $10.75 $20.56 $24,919 Current annual dividends:

$0.72 per share

100% franked

Commonwealth Bank 320 19/05/1997 $3.31 $72.21 $23,107 Current annual dividends:

$4.20 per share

100% franked

Commonwealth Bank 19 4/09/2000 $27.70 $1,372

Commonwealth Bank 22 27/08/2001 $30.05 $1,589

Insurance Australia Group 1,100 19/06/2000 $1.78 $5.34 $5,874 Current annual dividends:

$0.26 per share

100% franked

Insurance Australia Group 110 8/08/2000 $2.75 $587

National Australia Bank 740 30/07/1985 $4.08 $27.08 $20,039 Current annual dividends:

$1.98 per share

100% franked

National Australia Bank 50 4/02/2000 $21.73 $1,354

Rio Tinto Ltd 242 1/01/1988 $6.67 $46.53 $11,260 Current annual dividends:

$2.23 per share

100% franked

Wesfarmers 1,000 1/02/1985 $2.15 $42.83 $42,830 Current annual dividends:

$1.98 per share

100% franked

Online cash account n/a n/a n/a n/a $9,500 Earning1.5% p.a.

Apartment in Spring Hill,

QLD (selling now)

n/a 23/5/1986 $62,000 n/a $419,000 Betty’s principal residence in

Spring Hill, Brisbane. Debt-

free, no income, net value

after sale

Total inheritance

excluding superannuation

benefit

$561,431

Page 9 of 68

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

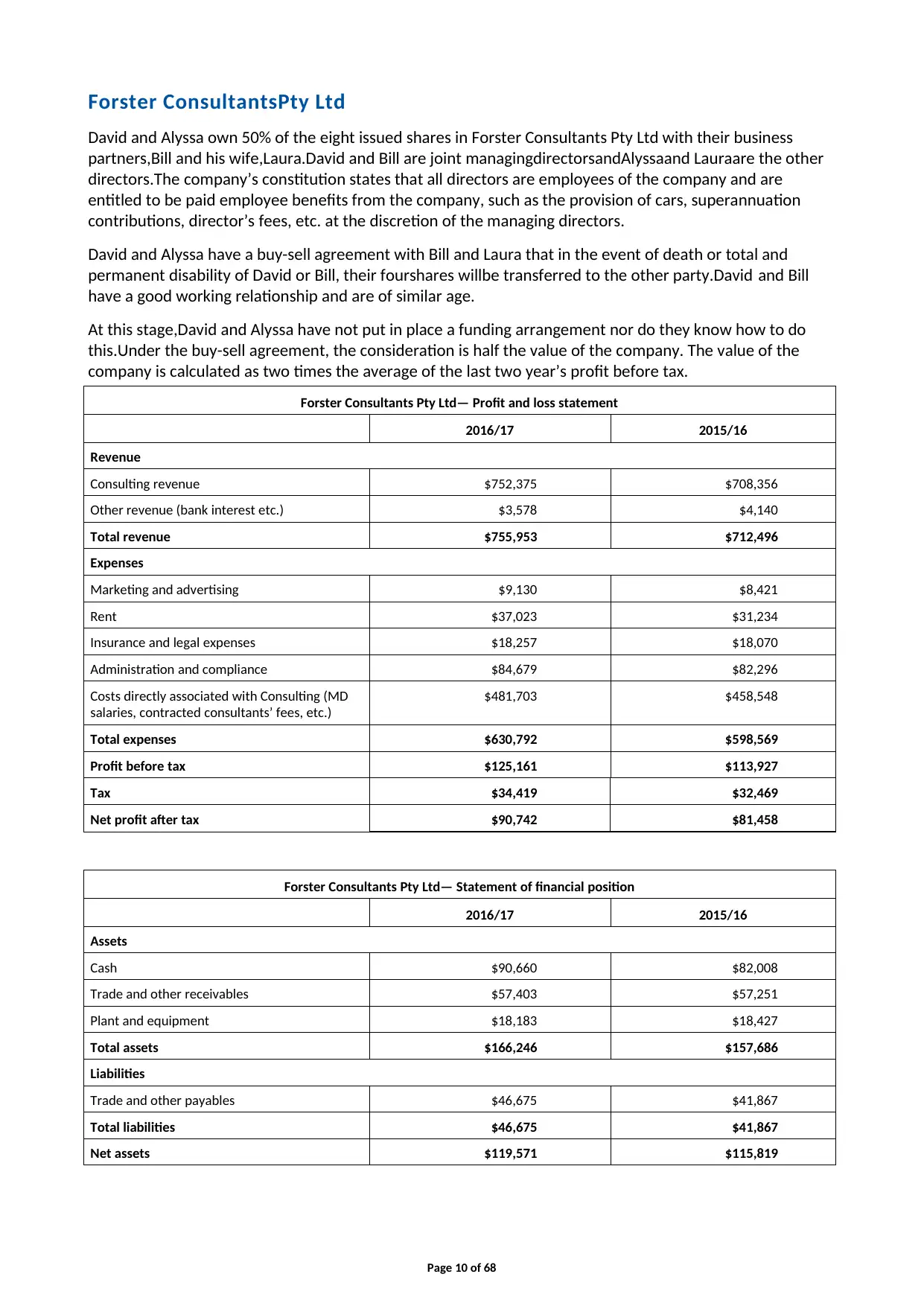

Forster ConsultantsPty Ltd

David and Alyssa own 50% of the eight issued shares in Forster Consultants Pty Ltd with their business

partners,Bill and his wife,Laura.David and Bill are joint managingdirectorsandAlyssaand Lauraare the other

directors.The company’s constitution states that all directors are employees of the company and are

entitled to be paid employee benefits from the company, such as the provision of cars, superannuation

contributions, director’s fees, etc. at the discretion of the managing directors.

David and Alyssa have a buy-sell agreement with Bill and Laura that in the event of death or total and

permanent disability of David or Bill, their fourshares willbe transferred to the other party.David and Bill

have a good working relationship and are of similar age.

At this stage,David and Alyssa have not put in place a funding arrangement nor do they know how to do

this.Under the buy-sell agreement, the consideration is half the value of the company. The value of the

company is calculated as two times the average of the last two year’s profit before tax.

Forster Consultants Pty Ltd— Profit and loss statement

2016/17 2015/16

Revenue

Consulting revenue $752,375 $708,356

Other revenue (bank interest etc.) $3,578 $4,140

Total revenue $755,953 $712,496

Expenses

Marketing and advertising $9,130 $8,421

Rent $37,023 $31,234

Insurance and legal expenses $18,257 $18,070

Administration and compliance $84,679 $82,296

Costs directly associated with Consulting (MD

salaries, contracted consultants’ fees, etc.)

$481,703 $458,548

Total expenses $630,792 $598,569

Profit before tax $125,161 $113,927

Tax $34,419 $32,469

Net profit after tax $90,742 $81,458

Forster Consultants Pty Ltd— Statement of financial position

2016/17 2015/16

Assets

Cash $90,660 $82,008

Trade and other receivables $57,403 $57,251

Plant and equipment $18,183 $18,427

Total assets $166,246 $157,686

Liabilities

Trade and other payables $46,675 $41,867

Total liabilities $46,675 $41,867

Net assets $119,571 $115,819

Page 10 of 68

David and Alyssa own 50% of the eight issued shares in Forster Consultants Pty Ltd with their business

partners,Bill and his wife,Laura.David and Bill are joint managingdirectorsandAlyssaand Lauraare the other

directors.The company’s constitution states that all directors are employees of the company and are

entitled to be paid employee benefits from the company, such as the provision of cars, superannuation

contributions, director’s fees, etc. at the discretion of the managing directors.

David and Alyssa have a buy-sell agreement with Bill and Laura that in the event of death or total and

permanent disability of David or Bill, their fourshares willbe transferred to the other party.David and Bill

have a good working relationship and are of similar age.

At this stage,David and Alyssa have not put in place a funding arrangement nor do they know how to do

this.Under the buy-sell agreement, the consideration is half the value of the company. The value of the

company is calculated as two times the average of the last two year’s profit before tax.

Forster Consultants Pty Ltd— Profit and loss statement

2016/17 2015/16

Revenue

Consulting revenue $752,375 $708,356

Other revenue (bank interest etc.) $3,578 $4,140

Total revenue $755,953 $712,496

Expenses

Marketing and advertising $9,130 $8,421

Rent $37,023 $31,234

Insurance and legal expenses $18,257 $18,070

Administration and compliance $84,679 $82,296

Costs directly associated with Consulting (MD

salaries, contracted consultants’ fees, etc.)

$481,703 $458,548

Total expenses $630,792 $598,569

Profit before tax $125,161 $113,927

Tax $34,419 $32,469

Net profit after tax $90,742 $81,458

Forster Consultants Pty Ltd— Statement of financial position

2016/17 2015/16

Assets

Cash $90,660 $82,008

Trade and other receivables $57,403 $57,251

Plant and equipment $18,183 $18,427

Total assets $166,246 $157,686

Liabilities

Trade and other payables $46,675 $41,867

Total liabilities $46,675 $41,867

Net assets $119,571 $115,819

Page 10 of 68

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

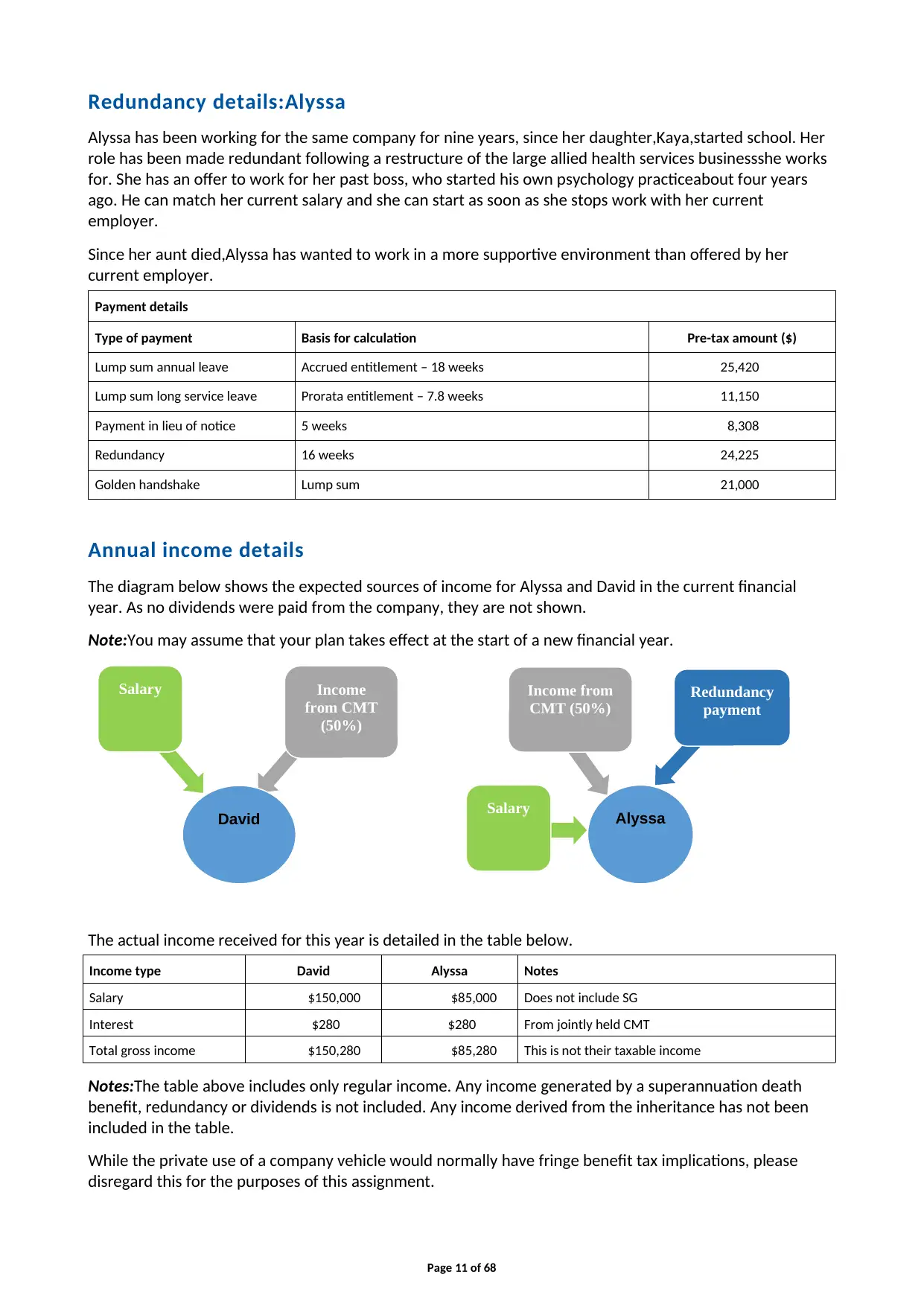

Redundancy details:Alyssa

Alyssa has been working for the same company for nine years, since her daughter,Kaya,started school. Her

role has been made redundant following a restructure of the large allied health services businessshe works

for. She has an offer to work for her past boss, who started his own psychology practiceabout four years

ago. He can match her current salary and she can start as soon as she stops work with her current

employer.

Since her aunt died,Alyssa has wanted to work in a more supportive environment than offered by her

current employer.

Payment details

Type of payment Basis for calculation Pre-tax amount ($)

Lump sum annual leave Accrued entitlement – 18 weeks 25,420

Lump sum long service leave Prorata entitlement – 7.8 weeks 11,150

Payment in lieu of notice 5 weeks 8,308

Redundancy 16 weeks 24,225

Golden handshake Lump sum 21,000

Annual income details

The diagram below shows the expected sources of income for Alyssa and David in the current financial

year. As no dividends were paid from the company, they are not shown.

Note:You may assume that your plan takes effect at the start of a new financial year.

The actual income received for this year is detailed in the table below.

Income type David Alyssa Notes

Salary $150,000 $85,000 Does not include SG

Interest $280 $280 From jointly held CMT

Total gross income $150,280 $85,280 This is not their taxable income

Notes:The table above includes only regular income. Any income generated by a superannuation death

benefit, redundancy or dividends is not included. Any income derived from the inheritance has not been

included in the table.

While the private use of a company vehicle would normally have fringe benefit tax implications, please

disregard this for the purposes of this assignment.

Page 11 of 68

Salary Income

from CMT

(50%)

Redundancy

payment

David Alyssa

Salary

Income from

CMT (50%)

Alyssa has been working for the same company for nine years, since her daughter,Kaya,started school. Her

role has been made redundant following a restructure of the large allied health services businessshe works

for. She has an offer to work for her past boss, who started his own psychology practiceabout four years

ago. He can match her current salary and she can start as soon as she stops work with her current

employer.

Since her aunt died,Alyssa has wanted to work in a more supportive environment than offered by her

current employer.

Payment details

Type of payment Basis for calculation Pre-tax amount ($)

Lump sum annual leave Accrued entitlement – 18 weeks 25,420

Lump sum long service leave Prorata entitlement – 7.8 weeks 11,150

Payment in lieu of notice 5 weeks 8,308

Redundancy 16 weeks 24,225

Golden handshake Lump sum 21,000

Annual income details

The diagram below shows the expected sources of income for Alyssa and David in the current financial

year. As no dividends were paid from the company, they are not shown.

Note:You may assume that your plan takes effect at the start of a new financial year.

The actual income received for this year is detailed in the table below.

Income type David Alyssa Notes

Salary $150,000 $85,000 Does not include SG

Interest $280 $280 From jointly held CMT

Total gross income $150,280 $85,280 This is not their taxable income

Notes:The table above includes only regular income. Any income generated by a superannuation death

benefit, redundancy or dividends is not included. Any income derived from the inheritance has not been

included in the table.

While the private use of a company vehicle would normally have fringe benefit tax implications, please

disregard this for the purposes of this assignment.

Page 11 of 68

Salary Income

from CMT

(50%)

Redundancy

payment

David Alyssa

Salary

Income from

CMT (50%)

Annual expenditure

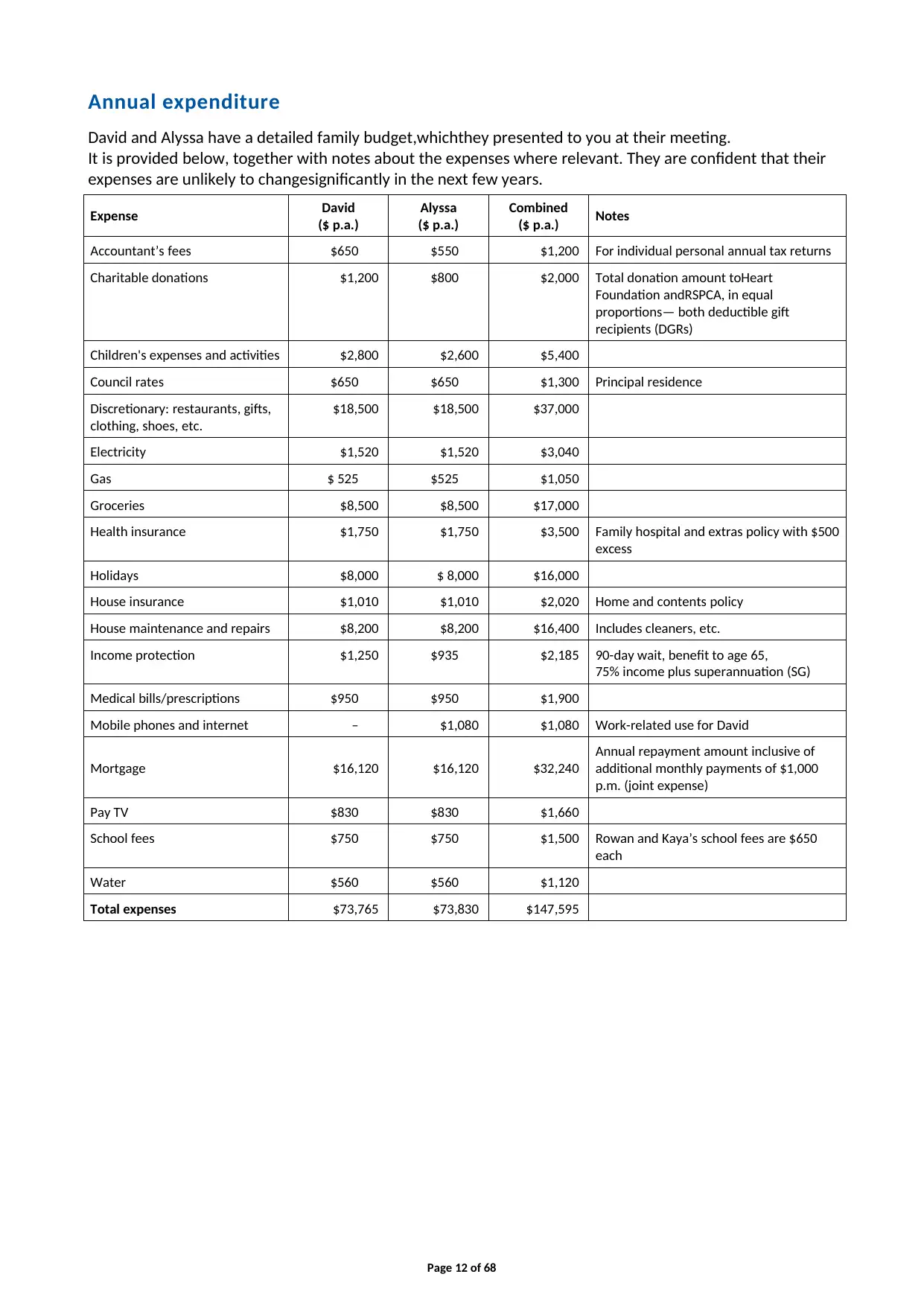

David and Alyssa have a detailed family budget,whichthey presented to you at their meeting.

It is provided below, together with notes about the expenses where relevant. They are confident that their

expenses are unlikely to changesignificantly in the next few years.

Expense David

($ p.a.)

Alyssa

($ p.a.)

Combined

($ p.a.) Notes

Accountant’s fees $650 $550 $1,200 For individual personal annual tax returns

Charitable donations $1,200 $800 $2,000 Total donation amount toHeart

Foundation andRSPCA, in equal

proportions— both deductible gift

recipients (DGRs)

Children's expenses and activities $2,800 $2,600 $5,400

Council rates $650 $650 $1,300 Principal residence

Discretionary: restaurants, gifts,

clothing, shoes, etc.

$18,500 $18,500 $37,000

Electricity $1,520 $1,520 $3,040

Gas $ 525 $525 $1,050

Groceries $8,500 $8,500 $17,000

Health insurance $1,750 $1,750 $3,500 Family hospital and extras policy with $500

excess

Holidays $8,000 $ 8,000 $16,000

House insurance $1,010 $1,010 $2,020 Home and contents policy

House maintenance and repairs $8,200 $8,200 $16,400 Includes cleaners, etc.

Income protection $1,250 $935 $2,185 90-day wait, benefit to age 65,

75% income plus superannuation (SG)

Medical bills/prescriptions $950 $950 $1,900

Mobile phones and internet – $1,080 $1,080 Work-related use for David

Mortgage $16,120 $16,120 $32,240

Annual repayment amount inclusive of

additional monthly payments of $1,000

p.m. (joint expense)

Pay TV $830 $830 $1,660

School fees $750 $750 $1,500 Rowan and Kaya’s school fees are $650

each

Water $560 $560 $1,120

Total expenses $73,765 $73,830 $147,595

Page 12 of 68

David and Alyssa have a detailed family budget,whichthey presented to you at their meeting.

It is provided below, together with notes about the expenses where relevant. They are confident that their

expenses are unlikely to changesignificantly in the next few years.

Expense David

($ p.a.)

Alyssa

($ p.a.)

Combined

($ p.a.) Notes

Accountant’s fees $650 $550 $1,200 For individual personal annual tax returns

Charitable donations $1,200 $800 $2,000 Total donation amount toHeart

Foundation andRSPCA, in equal

proportions— both deductible gift

recipients (DGRs)

Children's expenses and activities $2,800 $2,600 $5,400

Council rates $650 $650 $1,300 Principal residence

Discretionary: restaurants, gifts,

clothing, shoes, etc.

$18,500 $18,500 $37,000

Electricity $1,520 $1,520 $3,040

Gas $ 525 $525 $1,050

Groceries $8,500 $8,500 $17,000

Health insurance $1,750 $1,750 $3,500 Family hospital and extras policy with $500

excess

Holidays $8,000 $ 8,000 $16,000

House insurance $1,010 $1,010 $2,020 Home and contents policy

House maintenance and repairs $8,200 $8,200 $16,400 Includes cleaners, etc.

Income protection $1,250 $935 $2,185 90-day wait, benefit to age 65,

75% income plus superannuation (SG)

Medical bills/prescriptions $950 $950 $1,900

Mobile phones and internet – $1,080 $1,080 Work-related use for David

Mortgage $16,120 $16,120 $32,240

Annual repayment amount inclusive of

additional monthly payments of $1,000

p.m. (joint expense)

Pay TV $830 $830 $1,660

School fees $750 $750 $1,500 Rowan and Kaya’s school fees are $650

each

Water $560 $560 $1,120

Total expenses $73,765 $73,830 $147,595

Page 12 of 68

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 68

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.