Financial Performance Analysis: Fortescue Metals Group Limited Report

VerifiedAdded on 2021/06/15

|16

|1088

|99

Report

AI Summary

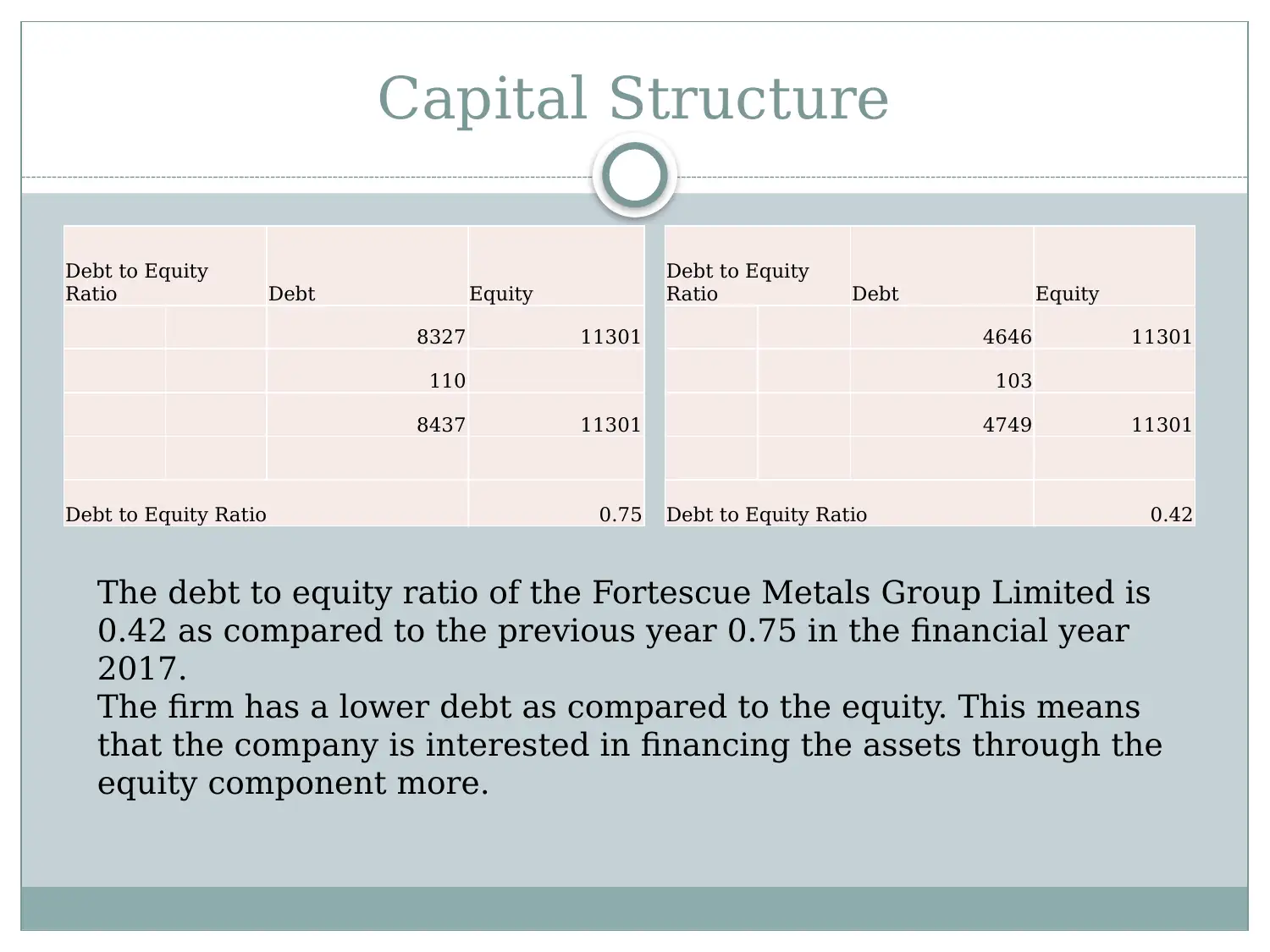

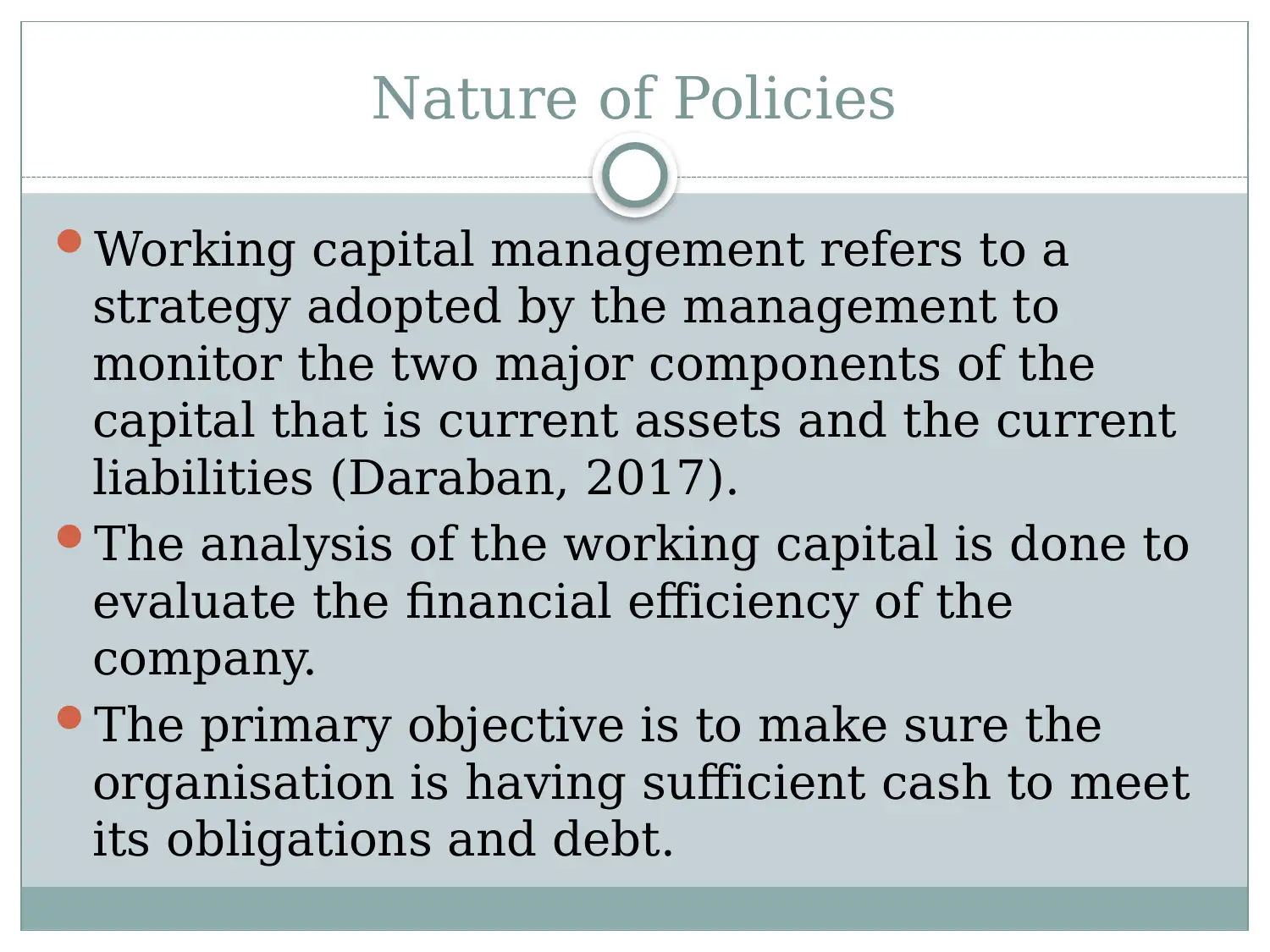

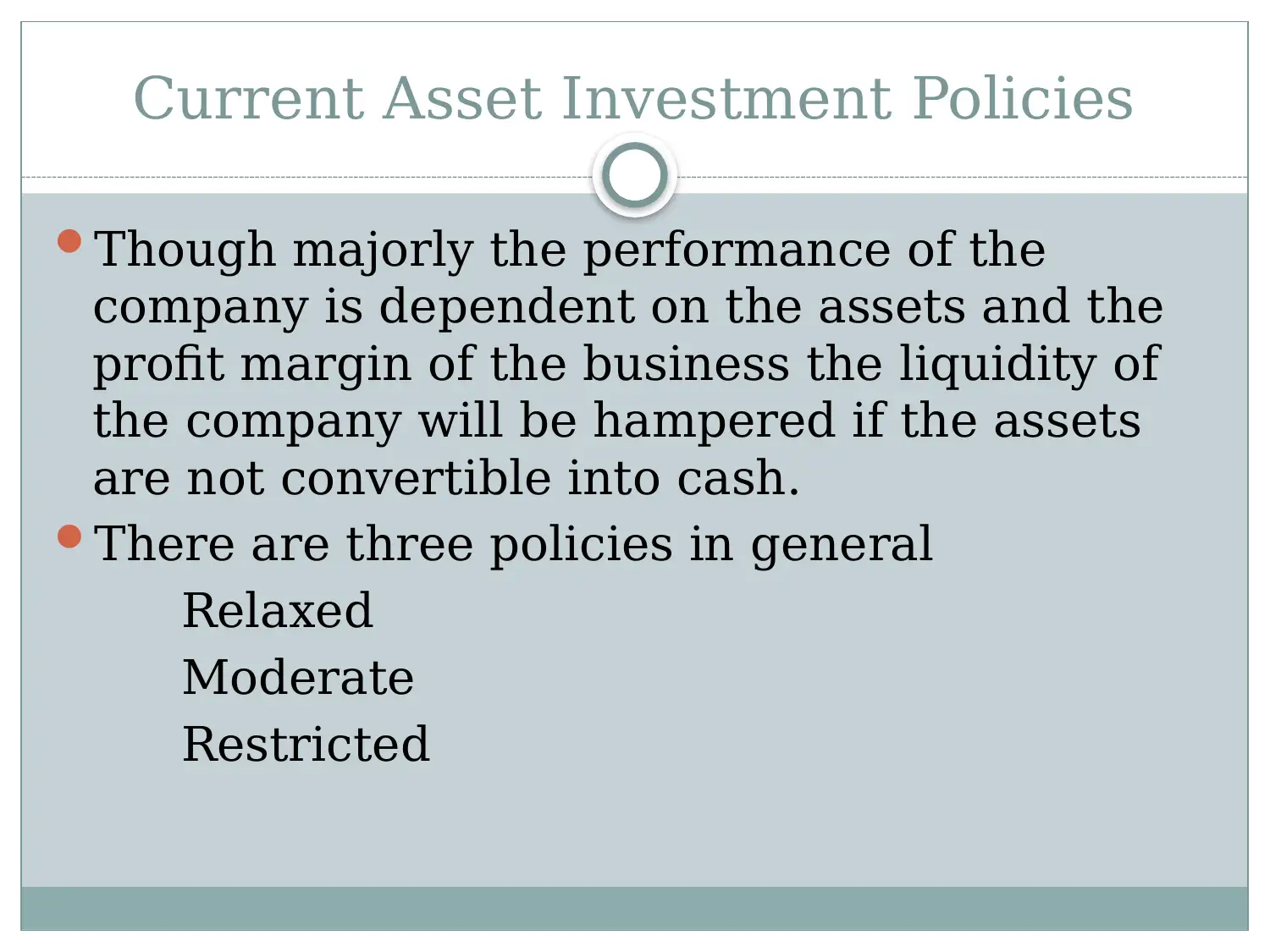

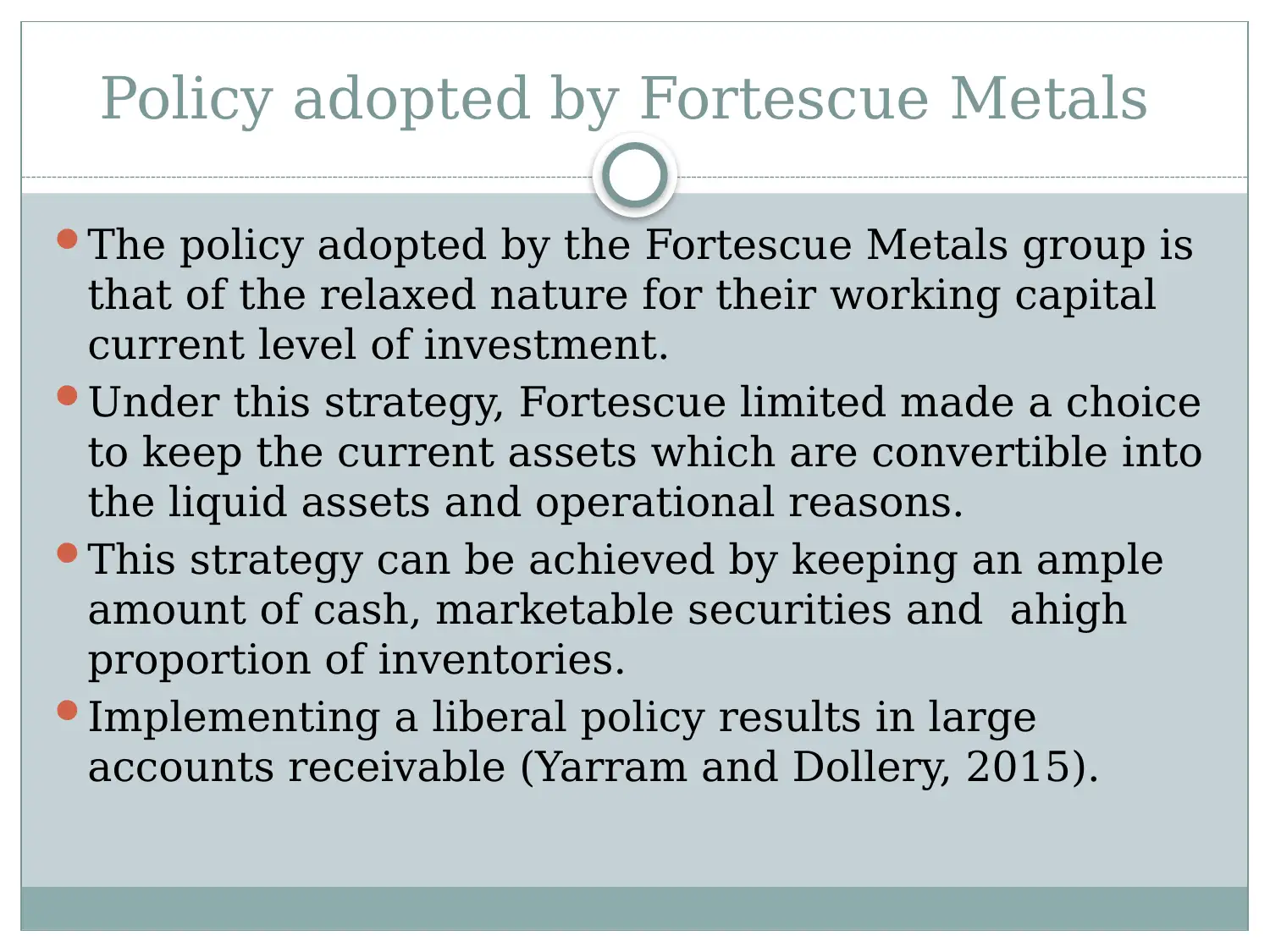

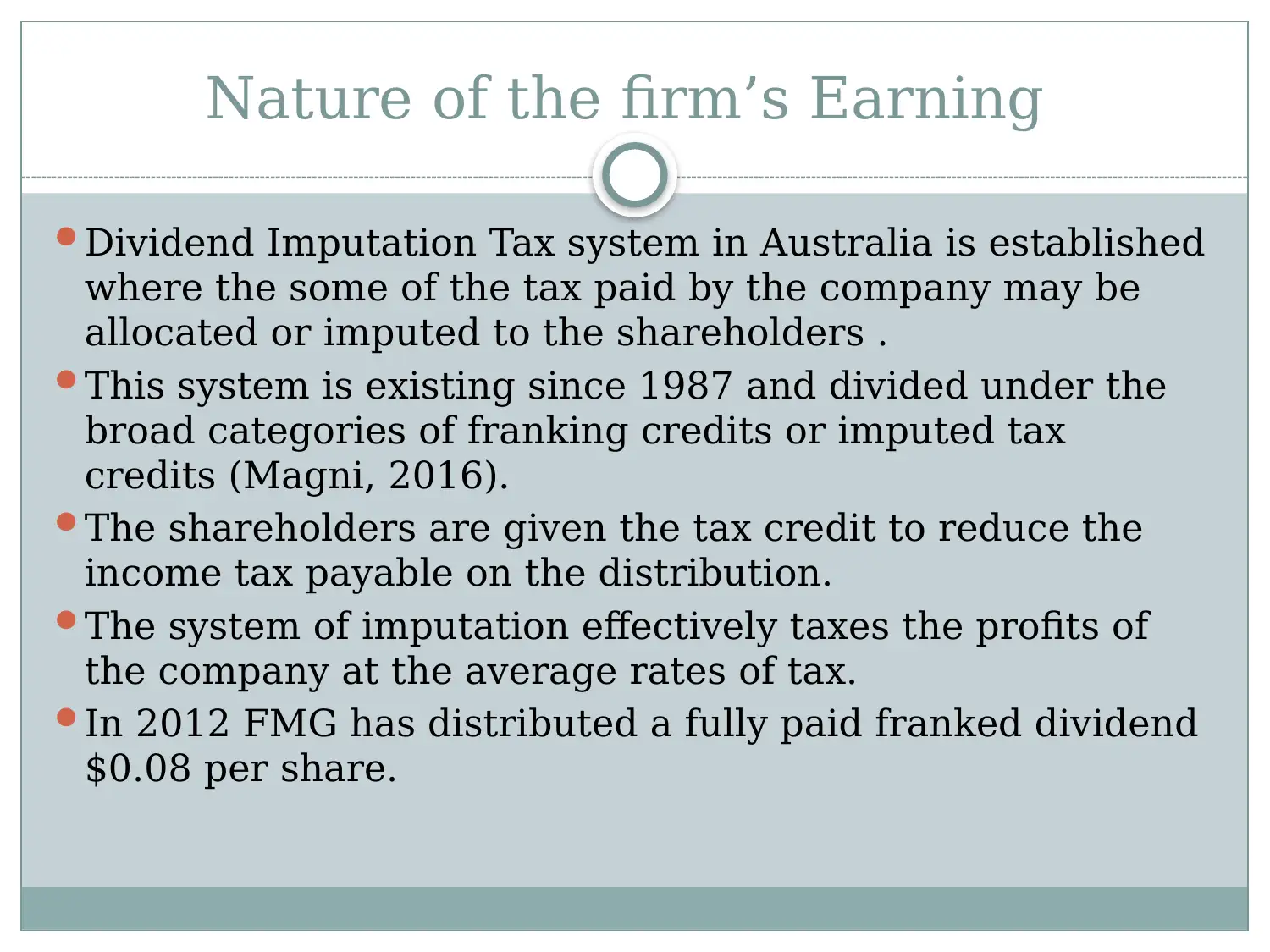

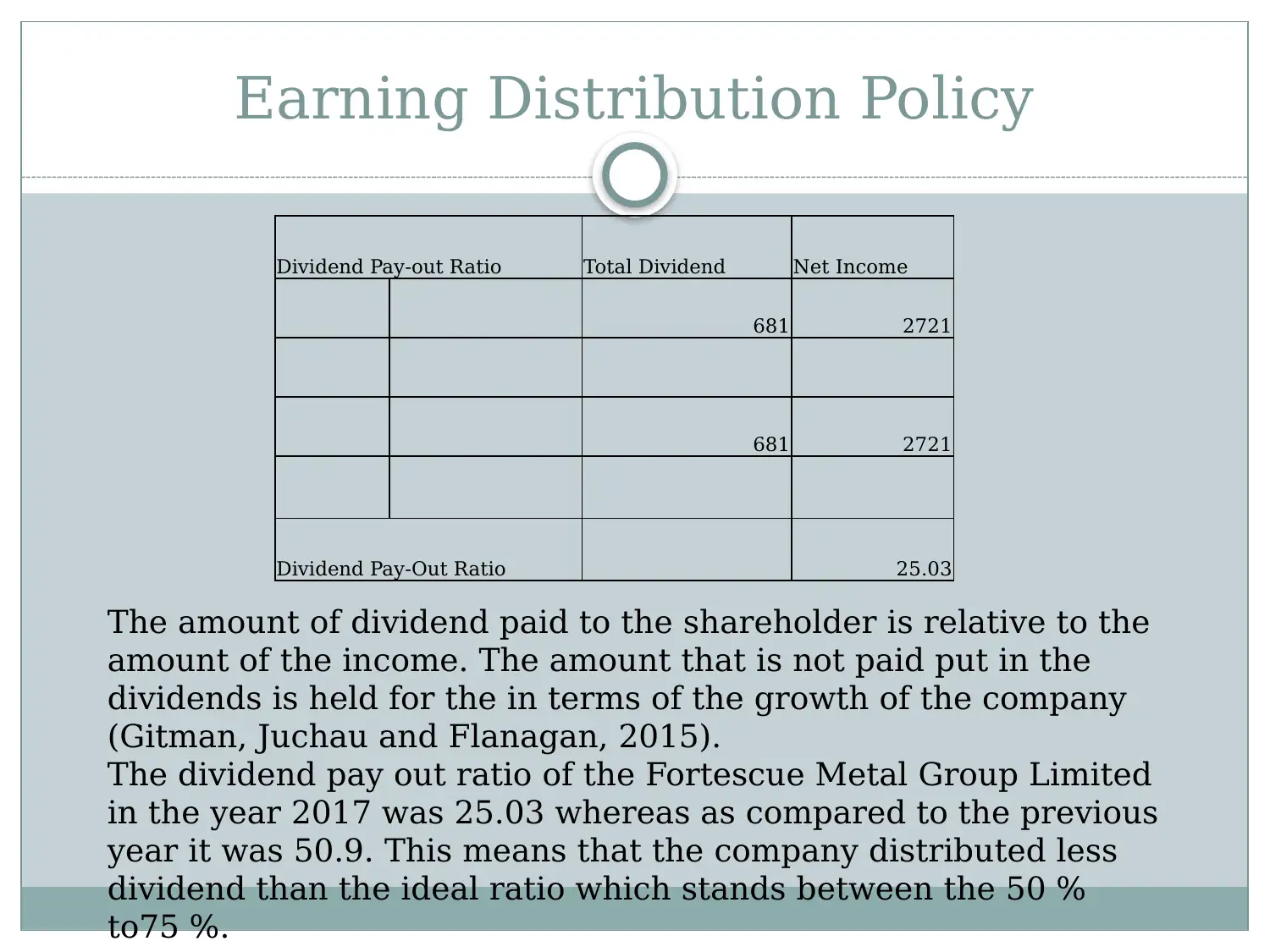

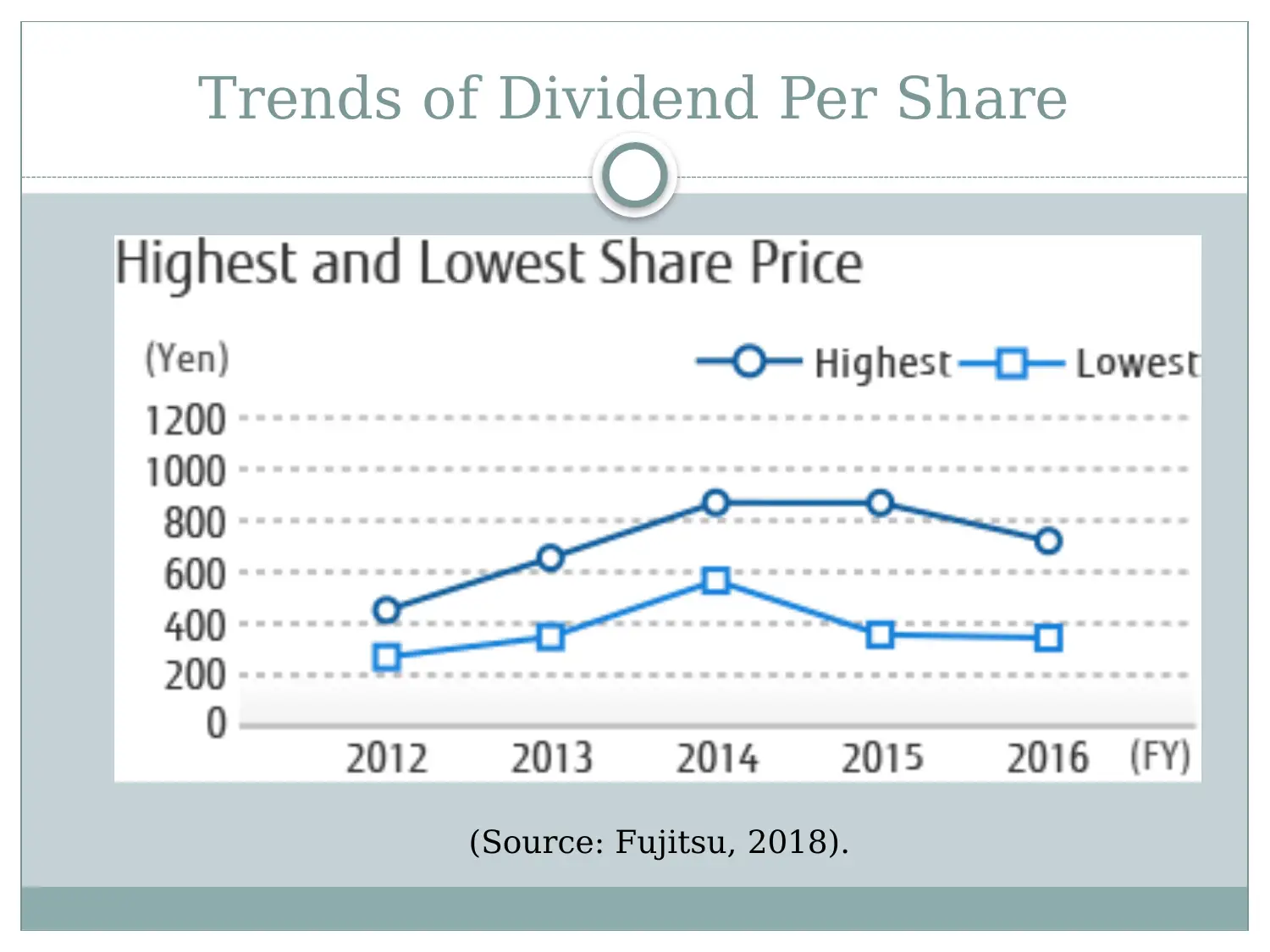

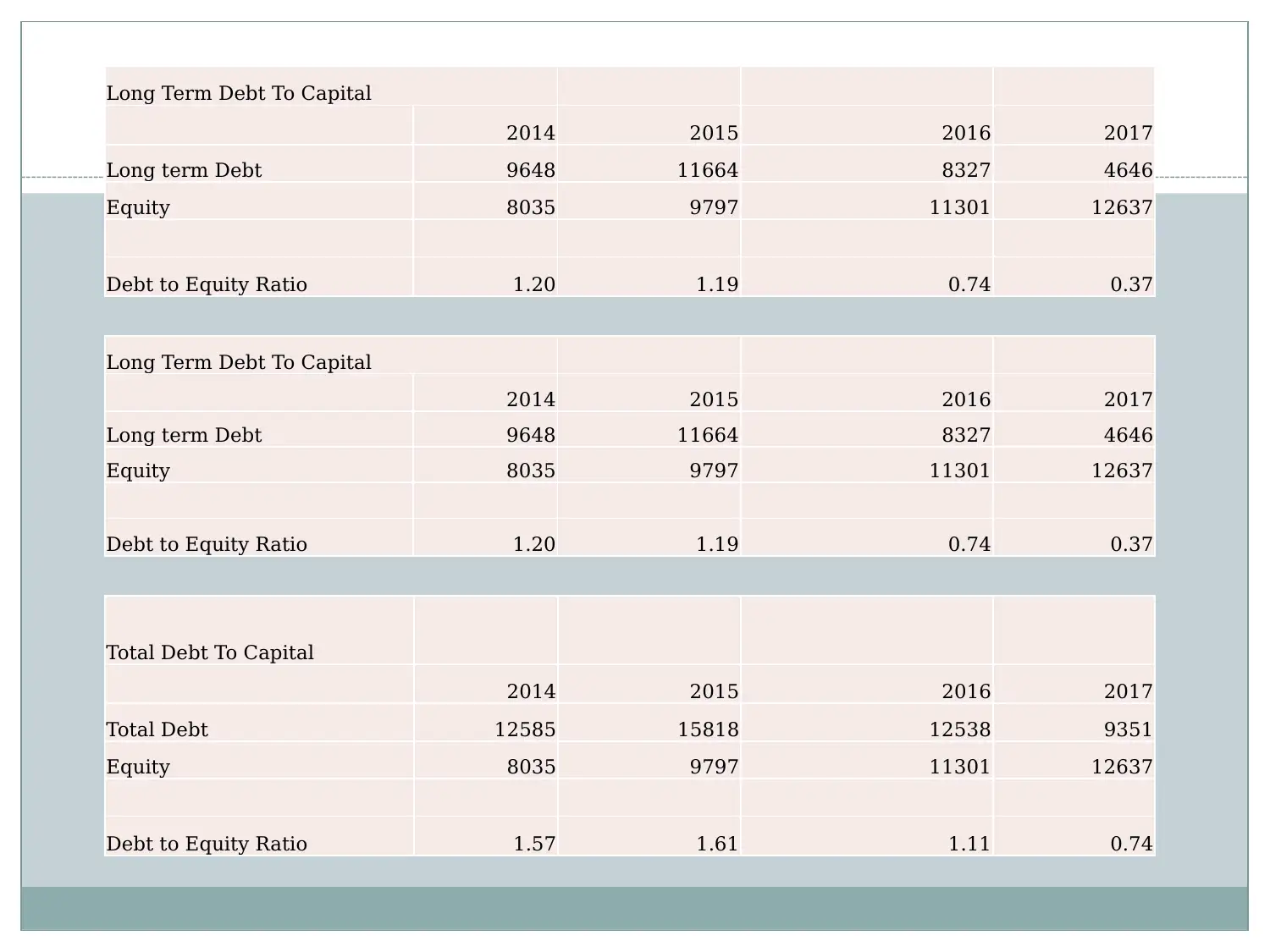

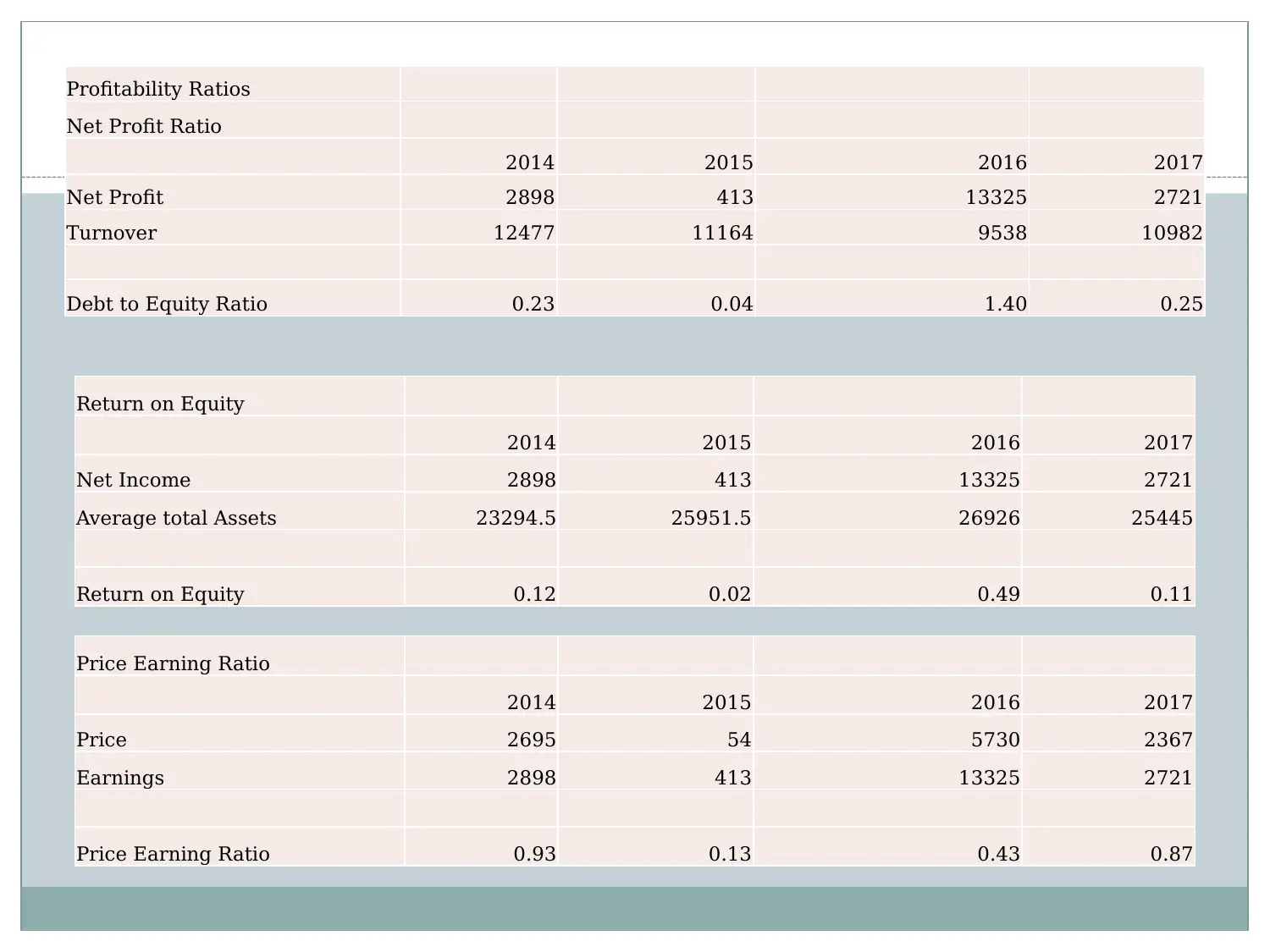

This report provides a financial analysis of Fortescue Metals Group Limited, examining its capital structure, working capital management, and dividend policies. The report details the company's debt-to-equity ratio, highlighting its preference for financing through equity. It discusses the company's relaxed approach to working capital management, emphasizing the importance of maintaining sufficient liquid assets. Furthermore, the report analyzes the company's dividend imputation tax system and its dividend payout ratio, noting trends in dividend per share and the implementation of a dividend reinvestment plan. The analysis also touches upon the impact of financial policies on market share and share price, providing an overview of the company's financial strategy and its implications.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.