FIN203 Corporate Finance: Fortescue Metals Group Analysis Report

VerifiedAdded on 2023/06/07

|12

|2376

|58

Report

AI Summary

This report analyzes the financial performance of Fortescue Metals Group, an Australian iron ore company. It examines the company's opportunities and threats, focusing on its cash conversion cycle, capital structure, and equity financing strategies. The assignment includes calculations and analysis of key financial metrics, such as the cash conversion cycle and the valuation of bonds and stocks using the dividend growth model. Furthermore, it explores capital budgeting techniques, including net present value, internal rate of return, and discounted payback period to evaluate potential investment projects. The report also delves into market capitalization and its determinants, providing a holistic overview of Fortescue Metals Group's financial health and investment prospects.

RUNNING HEAD: FINANCE

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance 2

Contents

Part 2...........................................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3...............................................................................................................................................4

Question 4...............................................................................................................................................6

Question 5...............................................................................................................................................7

Question 6...............................................................................................................................................7

Part 3...........................................................................................................................................................8

Part A......................................................................................................................................................8

Part B.......................................................................................................................................................8

Question 1-3........................................................................................................................................8

Question 4...........................................................................................................................................9

Question 5.........................................................................................................................................10

References.................................................................................................................................................11

Contents

Part 2...........................................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3...............................................................................................................................................4

Question 4...............................................................................................................................................6

Question 5...............................................................................................................................................7

Question 6...............................................................................................................................................7

Part 3...........................................................................................................................................................8

Part A......................................................................................................................................................8

Part B.......................................................................................................................................................8

Question 1-3........................................................................................................................................8

Question 4...........................................................................................................................................9

Question 5.........................................................................................................................................10

References.................................................................................................................................................11

Finance 3

Part 2

Question 1

Fortescue Metals Group is an Australian Iron Ore Company indulged in the business of

developing, exploring, producing and selling iron ore. A coordinated store network has been

possessed by the organization through which it directs its activities. The organization owns three

mining site in Pilbara, Herb Elliott Port in Port Hedland and the quickest haul railroad in the

world. Its main activities include the extraction and distribution of iron mineral and supply the

same through a wide production network (Reuters. 2018).

Opportunity

One of the key open doors accessible with the organization is to build its ability to 155mpta so as

to enhance its market share and improve its imports. Extending the same will result in overall

growth and development of the company. Likewise, it can target new markets on the worldwide

level, once the exports have been enhanced and expanded (Fortescue Metals. 2017).

Threats

• Changing condition of the surroundings in which the company operates is major

threat to it. The business practices of Fortescue influenced the environment and make

the ecologically sensitive.

• Existing rivals in the market make the opposition extreme. Organizations like BHP

Billiton and Rio Tinto are now beating the industry. This is also one of the

significant dangers to the firm (Fortescue Metals. 2017).

Part 2

Question 1

Fortescue Metals Group is an Australian Iron Ore Company indulged in the business of

developing, exploring, producing and selling iron ore. A coordinated store network has been

possessed by the organization through which it directs its activities. The organization owns three

mining site in Pilbara, Herb Elliott Port in Port Hedland and the quickest haul railroad in the

world. Its main activities include the extraction and distribution of iron mineral and supply the

same through a wide production network (Reuters. 2018).

Opportunity

One of the key open doors accessible with the organization is to build its ability to 155mpta so as

to enhance its market share and improve its imports. Extending the same will result in overall

growth and development of the company. Likewise, it can target new markets on the worldwide

level, once the exports have been enhanced and expanded (Fortescue Metals. 2017).

Threats

• Changing condition of the surroundings in which the company operates is major

threat to it. The business practices of Fortescue influenced the environment and make

the ecologically sensitive.

• Existing rivals in the market make the opposition extreme. Organizations like BHP

Billiton and Rio Tinto are now beating the industry. This is also one of the

significant dangers to the firm (Fortescue Metals. 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance 4

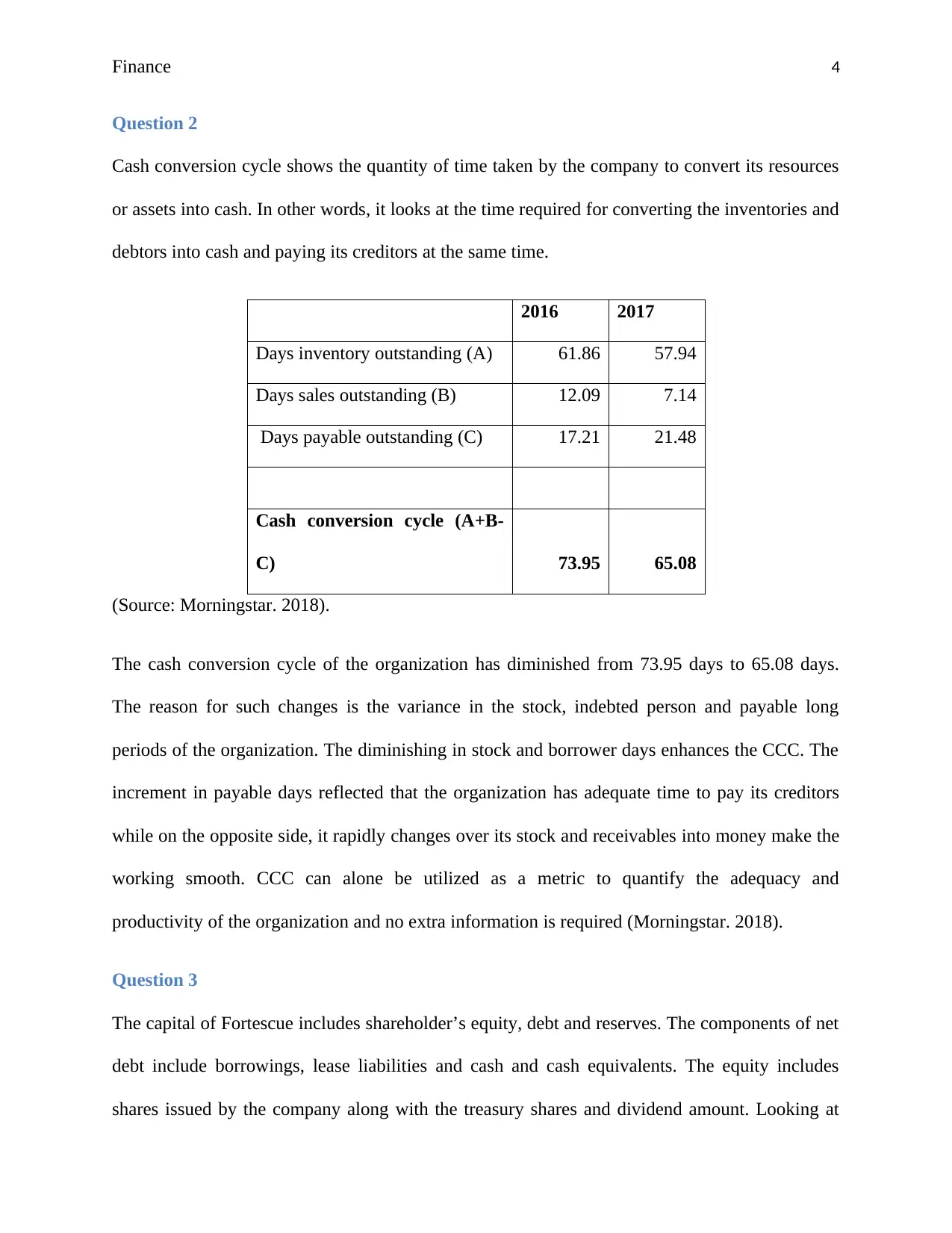

Question 2

Cash conversion cycle shows the quantity of time taken by the company to convert its resources

or assets into cash. In other words, it looks at the time required for converting the inventories and

debtors into cash and paying its creditors at the same time.

2016 2017

Days inventory outstanding (A) 61.86 57.94

Days sales outstanding (B) 12.09 7.14

Days payable outstanding (C) 17.21 21.48

Cash conversion cycle (A+B-

C) 73.95 65.08

(Source: Morningstar. 2018).

The cash conversion cycle of the organization has diminished from 73.95 days to 65.08 days.

The reason for such changes is the variance in the stock, indebted person and payable long

periods of the organization. The diminishing in stock and borrower days enhances the CCC. The

increment in payable days reflected that the organization has adequate time to pay its creditors

while on the opposite side, it rapidly changes over its stock and receivables into money make the

working smooth. CCC can alone be utilized as a metric to quantify the adequacy and

productivity of the organization and no extra information is required (Morningstar. 2018).

Question 3

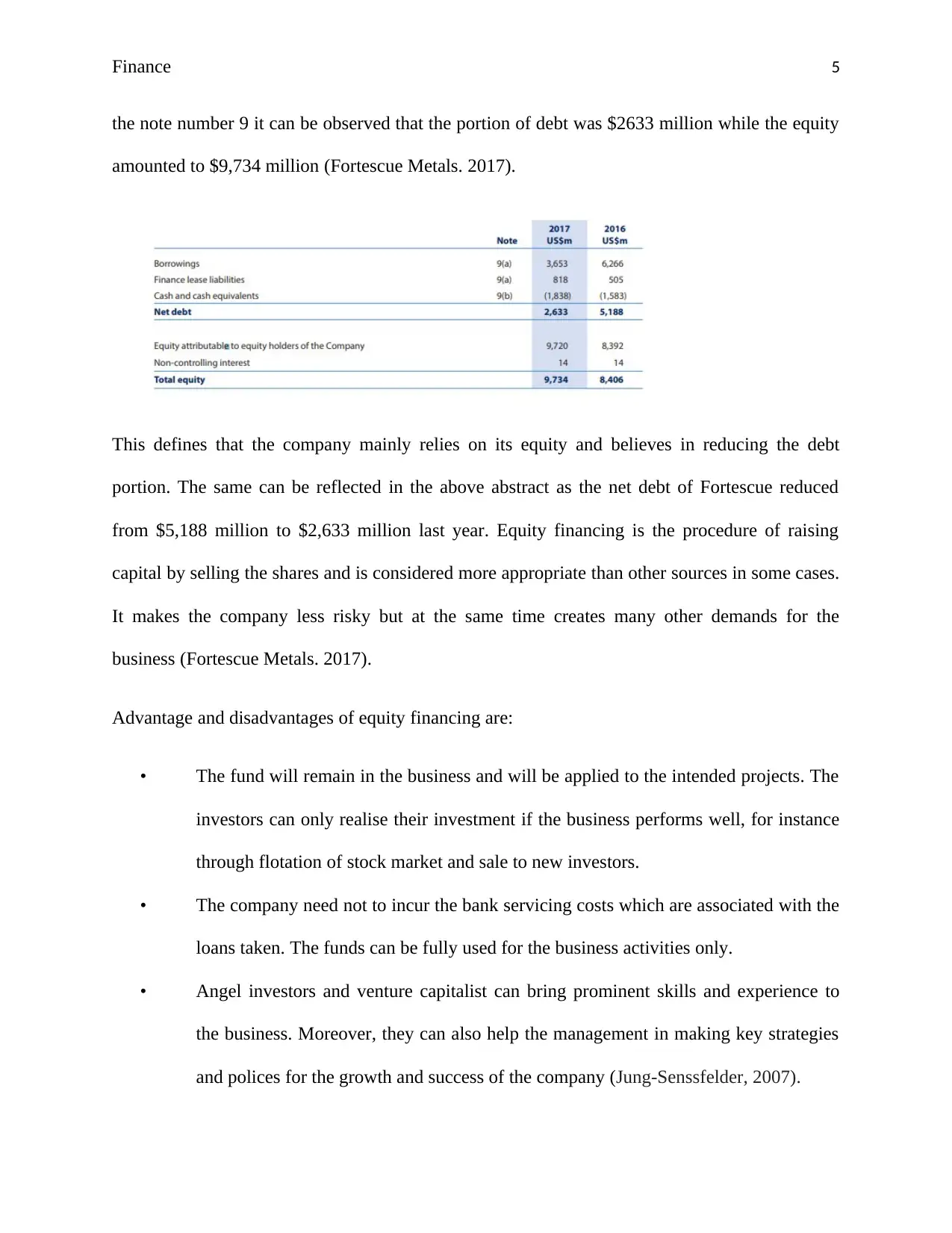

The capital of Fortescue includes shareholder’s equity, debt and reserves. The components of net

debt include borrowings, lease liabilities and cash and cash equivalents. The equity includes

shares issued by the company along with the treasury shares and dividend amount. Looking at

Question 2

Cash conversion cycle shows the quantity of time taken by the company to convert its resources

or assets into cash. In other words, it looks at the time required for converting the inventories and

debtors into cash and paying its creditors at the same time.

2016 2017

Days inventory outstanding (A) 61.86 57.94

Days sales outstanding (B) 12.09 7.14

Days payable outstanding (C) 17.21 21.48

Cash conversion cycle (A+B-

C) 73.95 65.08

(Source: Morningstar. 2018).

The cash conversion cycle of the organization has diminished from 73.95 days to 65.08 days.

The reason for such changes is the variance in the stock, indebted person and payable long

periods of the organization. The diminishing in stock and borrower days enhances the CCC. The

increment in payable days reflected that the organization has adequate time to pay its creditors

while on the opposite side, it rapidly changes over its stock and receivables into money make the

working smooth. CCC can alone be utilized as a metric to quantify the adequacy and

productivity of the organization and no extra information is required (Morningstar. 2018).

Question 3

The capital of Fortescue includes shareholder’s equity, debt and reserves. The components of net

debt include borrowings, lease liabilities and cash and cash equivalents. The equity includes

shares issued by the company along with the treasury shares and dividend amount. Looking at

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance 5

the note number 9 it can be observed that the portion of debt was $2633 million while the equity

amounted to $9,734 million (Fortescue Metals. 2017).

This defines that the company mainly relies on its equity and believes in reducing the debt

portion. The same can be reflected in the above abstract as the net debt of Fortescue reduced

from $5,188 million to $2,633 million last year. Equity financing is the procedure of raising

capital by selling the shares and is considered more appropriate than other sources in some cases.

It makes the company less risky but at the same time creates many other demands for the

business (Fortescue Metals. 2017).

Advantage and disadvantages of equity financing are:

• The fund will remain in the business and will be applied to the intended projects. The

investors can only realise their investment if the business performs well, for instance

through flotation of stock market and sale to new investors.

• The company need not to incur the bank servicing costs which are associated with the

loans taken. The funds can be fully used for the business activities only.

• Angel investors and venture capitalist can bring prominent skills and experience to

the business. Moreover, they can also help the management in making key strategies

and polices for the growth and success of the company (Jung-Senssfelder, 2007).

the note number 9 it can be observed that the portion of debt was $2633 million while the equity

amounted to $9,734 million (Fortescue Metals. 2017).

This defines that the company mainly relies on its equity and believes in reducing the debt

portion. The same can be reflected in the above abstract as the net debt of Fortescue reduced

from $5,188 million to $2,633 million last year. Equity financing is the procedure of raising

capital by selling the shares and is considered more appropriate than other sources in some cases.

It makes the company less risky but at the same time creates many other demands for the

business (Fortescue Metals. 2017).

Advantage and disadvantages of equity financing are:

• The fund will remain in the business and will be applied to the intended projects. The

investors can only realise their investment if the business performs well, for instance

through flotation of stock market and sale to new investors.

• The company need not to incur the bank servicing costs which are associated with the

loans taken. The funds can be fully used for the business activities only.

• Angel investors and venture capitalist can bring prominent skills and experience to

the business. Moreover, they can also help the management in making key strategies

and polices for the growth and success of the company (Jung-Senssfelder, 2007).

Finance 6

• It ultimately helps in maximizing the shareholder value and lead to innovative growth

ideas for the business.

Disadvantages

• Raising funds from equity financing may prove to be costly, time consuming and

demanding from the company as it takes management to shift their focus from core

activities to shareholders.

• It gives some power and authority to the investors for taking management decisions

for the company.

• Managers have to invest their time in providing regular and reliable information to

the potential investors.

• Adoption of equity financing also involves some sort of regulatory and legal issues to

which the compliance is very much necessary for the company (Coyle, 2002).

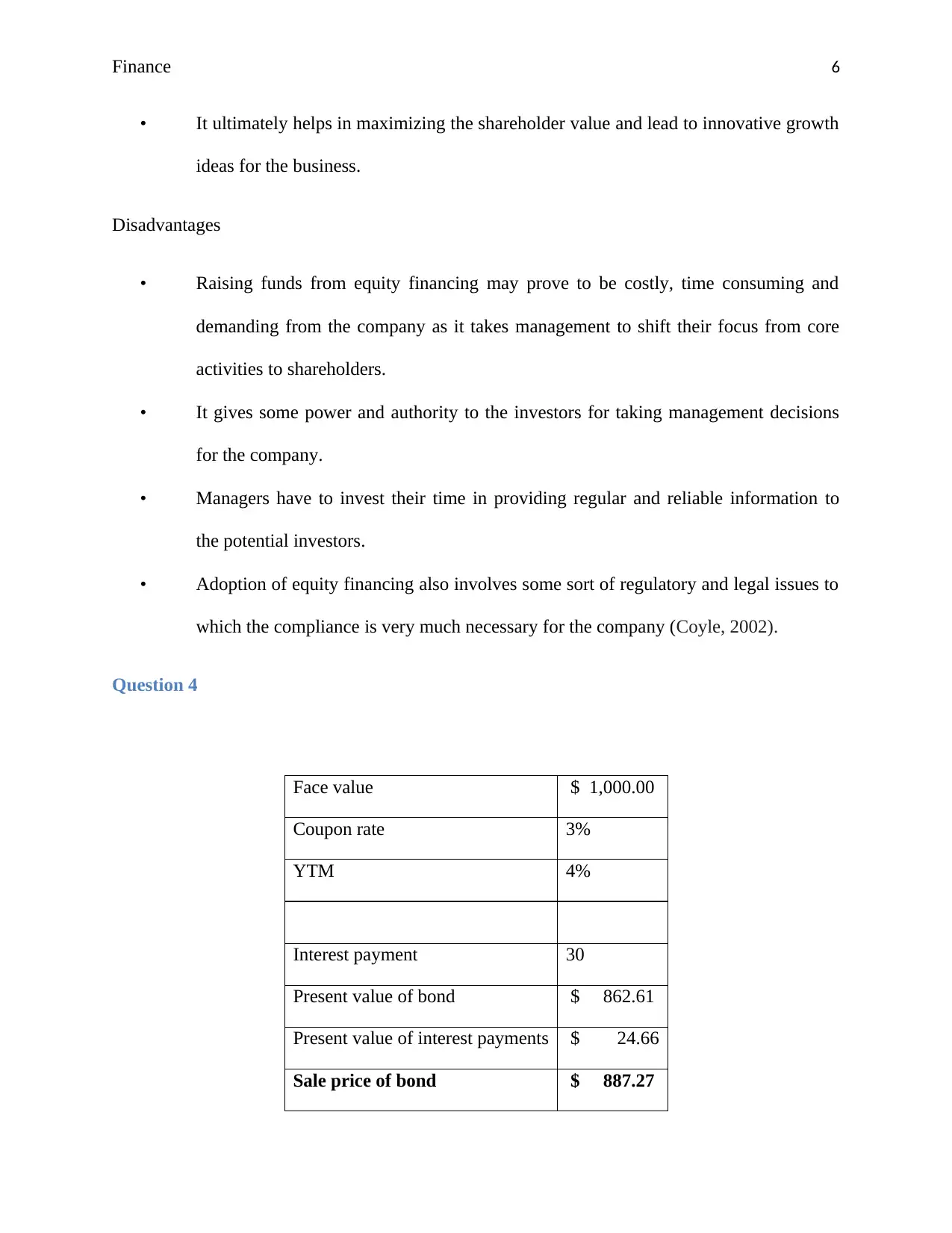

Question 4

Face value $ 1,000.00

Coupon rate 3%

YTM 4%

Interest payment 30

Present value of bond $ 862.61

Present value of interest payments $ 24.66

Sale price of bond $ 887.27

• It ultimately helps in maximizing the shareholder value and lead to innovative growth

ideas for the business.

Disadvantages

• Raising funds from equity financing may prove to be costly, time consuming and

demanding from the company as it takes management to shift their focus from core

activities to shareholders.

• It gives some power and authority to the investors for taking management decisions

for the company.

• Managers have to invest their time in providing regular and reliable information to

the potential investors.

• Adoption of equity financing also involves some sort of regulatory and legal issues to

which the compliance is very much necessary for the company (Coyle, 2002).

Question 4

Face value $ 1,000.00

Coupon rate 3%

YTM 4%

Interest payment 30

Present value of bond $ 862.61

Present value of interest payments $ 24.66

Sale price of bond $ 887.27

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance 7

Question 5

Credit ratings indicate the probability of repayment of debt in full. Generally, investors look at

them to check that whether the bond will be fully repaid or not on the scale of high and low

probability. There are several rating agencies which gives rating to the bonds such as Standard &

Poor's (S&P), Moody's and Fitch IBCA. The ratings given by S&P are like AAA, BBB, BB,

CCC and others. BBB indicates lowest investment grade rating, though satisfactory but requires

monitoring. BB shows speculative bonds of low grade (Kisgen, 2006). The ratings usually affect

the cost o f borrowing means the interest rate which has to be paid by the issuer. If the credit

rating is lowered, for instance from BBB to BB then it will impact the bond price and bring a

decline in the same. The reason for such change is investors prefer to sell the bonds when credit

rating is reducing and purchase the same when they are improving.

The downgrade in the bond of Fortescue gives an indication to the investors that they should sell

the bond as the rating has been lowered. No, in this case they are not attractive assets for the

investors from the perspective of buying as their rating have been reduced and according to the

analyst they should be sold out (Langohr and Langohr, 2010).

Question 6

The value of stock calculated as per dividend growth model is $1.80. The current share price of

Fortescue Metals is $3.95 (Yahoo Finance. 2018). As per the calculation, the price of Fortescue

will fall in future so it will be recommended to purchase the same later on. Recently, it is traded

at $3.95 and in future it will fall to $1.80 so the wise decision will be to purchase later on.

Generally, investors seek the opportunities where the share price fall and so that they can

Question 5

Credit ratings indicate the probability of repayment of debt in full. Generally, investors look at

them to check that whether the bond will be fully repaid or not on the scale of high and low

probability. There are several rating agencies which gives rating to the bonds such as Standard &

Poor's (S&P), Moody's and Fitch IBCA. The ratings given by S&P are like AAA, BBB, BB,

CCC and others. BBB indicates lowest investment grade rating, though satisfactory but requires

monitoring. BB shows speculative bonds of low grade (Kisgen, 2006). The ratings usually affect

the cost o f borrowing means the interest rate which has to be paid by the issuer. If the credit

rating is lowered, for instance from BBB to BB then it will impact the bond price and bring a

decline in the same. The reason for such change is investors prefer to sell the bonds when credit

rating is reducing and purchase the same when they are improving.

The downgrade in the bond of Fortescue gives an indication to the investors that they should sell

the bond as the rating has been lowered. No, in this case they are not attractive assets for the

investors from the perspective of buying as their rating have been reduced and according to the

analyst they should be sold out (Langohr and Langohr, 2010).

Question 6

The value of stock calculated as per dividend growth model is $1.80. The current share price of

Fortescue Metals is $3.95 (Yahoo Finance. 2018). As per the calculation, the price of Fortescue

will fall in future so it will be recommended to purchase the same later on. Recently, it is traded

at $3.95 and in future it will fall to $1.80 so the wise decision will be to purchase later on.

Generally, investors seek the opportunities where the share price fall and so that they can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance 8

purchase them at that price and sell the same when price rises in order to book high profits.

Dividend growth rate model gives the future value of stock and indicates that whether the stock

will fall or rise in coming years. Therefore, according to the calculations, the investors should not

purchase the shares today and wait for it to decline in future (Corelli, 2017).

Part 3

Part A

The current market capitalization of the company is $12.295 billion (Yahoo Finance. 2018).

Market cap determines the value of the company at which it is traded in the market. It is

generally calculated by multiplying the number of shares by the current market price of the

share. In other words, it reflects the size of the entity and the market share covered by it. In 2017,

it was $11.85 billion. Generally significant changes in the value of shares outstanding and market

price of the stock can impact the market cap to a great extent. The market cap of Fortescue has

increased in 2018 as a result of rise in the number of shares. Though the share price slightly

reduced but increase in number of shares has bring the overall impact on the current market cap

of the company. The company has paid dividends and after that its stock price reduced as the

number of shares increased. This impacted the market cap and boosted up in the current year

(Abdolmohammadi, 2005).

Part B

Question 1-3

Refer excel.

purchase them at that price and sell the same when price rises in order to book high profits.

Dividend growth rate model gives the future value of stock and indicates that whether the stock

will fall or rise in coming years. Therefore, according to the calculations, the investors should not

purchase the shares today and wait for it to decline in future (Corelli, 2017).

Part 3

Part A

The current market capitalization of the company is $12.295 billion (Yahoo Finance. 2018).

Market cap determines the value of the company at which it is traded in the market. It is

generally calculated by multiplying the number of shares by the current market price of the

share. In other words, it reflects the size of the entity and the market share covered by it. In 2017,

it was $11.85 billion. Generally significant changes in the value of shares outstanding and market

price of the stock can impact the market cap to a great extent. The market cap of Fortescue has

increased in 2018 as a result of rise in the number of shares. Though the share price slightly

reduced but increase in number of shares has bring the overall impact on the current market cap

of the company. The company has paid dividends and after that its stock price reduced as the

number of shares increased. This impacted the market cap and boosted up in the current year

(Abdolmohammadi, 2005).

Part B

Question 1-3

Refer excel.

Finance 9

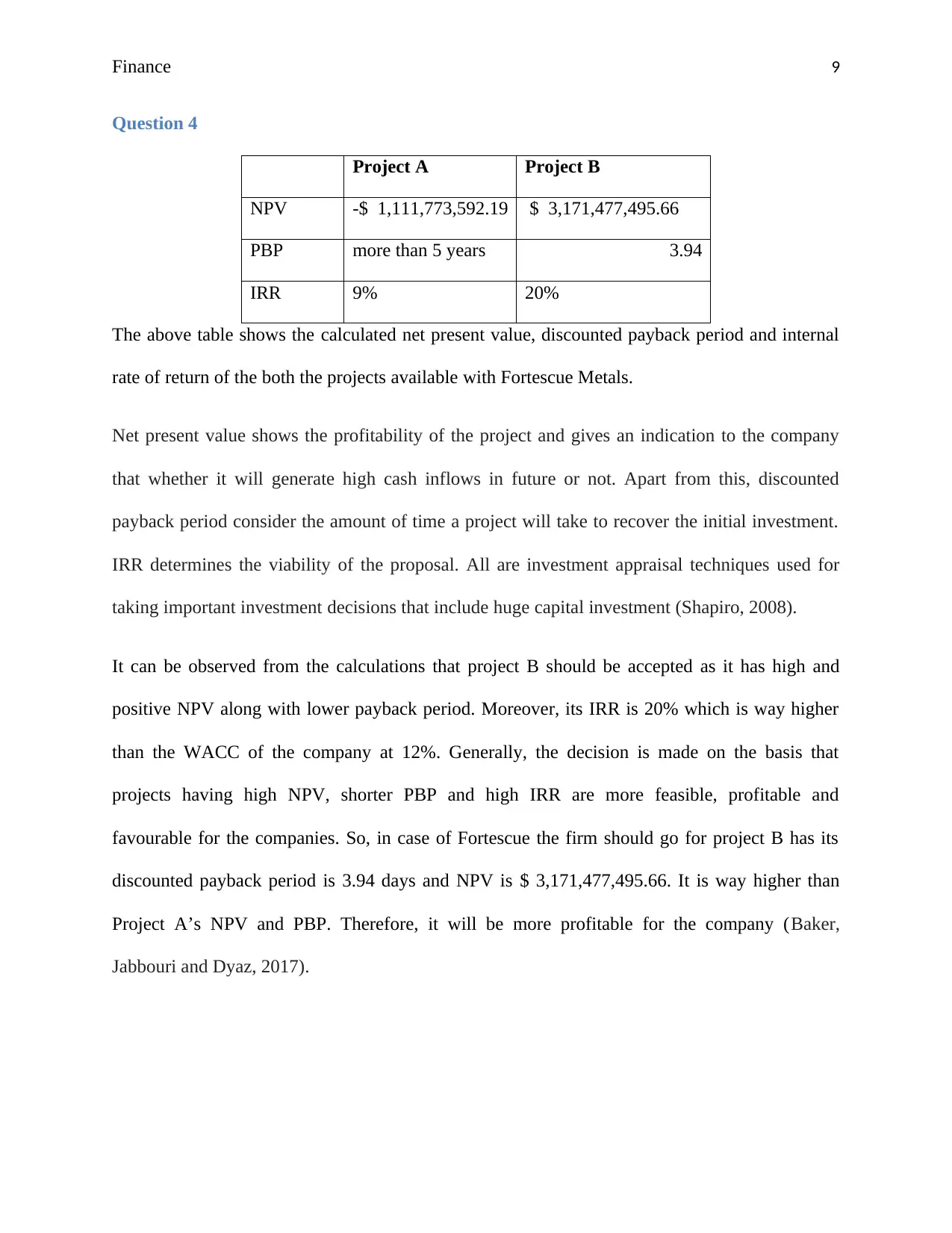

Question 4

Project A Project B

NPV -$ 1,111,773,592.19 $ 3,171,477,495.66

PBP more than 5 years 3.94

IRR 9% 20%

The above table shows the calculated net present value, discounted payback period and internal

rate of return of the both the projects available with Fortescue Metals.

Net present value shows the profitability of the project and gives an indication to the company

that whether it will generate high cash inflows in future or not. Apart from this, discounted

payback period consider the amount of time a project will take to recover the initial investment.

IRR determines the viability of the proposal. All are investment appraisal techniques used for

taking important investment decisions that include huge capital investment (Shapiro, 2008).

It can be observed from the calculations that project B should be accepted as it has high and

positive NPV along with lower payback period. Moreover, its IRR is 20% which is way higher

than the WACC of the company at 12%. Generally, the decision is made on the basis that

projects having high NPV, shorter PBP and high IRR are more feasible, profitable and

favourable for the companies. So, in case of Fortescue the firm should go for project B has its

discounted payback period is 3.94 days and NPV is $ 3,171,477,495.66. It is way higher than

Project A’s NPV and PBP. Therefore, it will be more profitable for the company (Baker,

Jabbouri and Dyaz, 2017).

Question 4

Project A Project B

NPV -$ 1,111,773,592.19 $ 3,171,477,495.66

PBP more than 5 years 3.94

IRR 9% 20%

The above table shows the calculated net present value, discounted payback period and internal

rate of return of the both the projects available with Fortescue Metals.

Net present value shows the profitability of the project and gives an indication to the company

that whether it will generate high cash inflows in future or not. Apart from this, discounted

payback period consider the amount of time a project will take to recover the initial investment.

IRR determines the viability of the proposal. All are investment appraisal techniques used for

taking important investment decisions that include huge capital investment (Shapiro, 2008).

It can be observed from the calculations that project B should be accepted as it has high and

positive NPV along with lower payback period. Moreover, its IRR is 20% which is way higher

than the WACC of the company at 12%. Generally, the decision is made on the basis that

projects having high NPV, shorter PBP and high IRR are more feasible, profitable and

favourable for the companies. So, in case of Fortescue the firm should go for project B has its

discounted payback period is 3.94 days and NPV is $ 3,171,477,495.66. It is way higher than

Project A’s NPV and PBP. Therefore, it will be more profitable for the company (Baker,

Jabbouri and Dyaz, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance 10

Question 5

No, the decision would not change as even after project A sold all of the assets worth $100

million because it’s NPV do increase but still remain negative. So, in this case also project B

should be accepted as it is more profitable comparatively. Though the sale of assets brings cash

into the business worth $100 million but it has to note that the project is still not capable enough

to cover the initial outlay which makes its NPV negative. So overall, it is interpreted that project

B should be accepted (BiermanJr and Smidt, 2014).

Question 5

No, the decision would not change as even after project A sold all of the assets worth $100

million because it’s NPV do increase but still remain negative. So, in this case also project B

should be accepted as it is more profitable comparatively. Though the sale of assets brings cash

into the business worth $100 million but it has to note that the project is still not capable enough

to cover the initial outlay which makes its NPV negative. So overall, it is interpreted that project

B should be accepted (BiermanJr and Smidt, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance 11

References

Abdolmohammadi, M.J. (2005). Intellectual capital disclosure and market capitalization. Journal

of intellectual capital, 6(3), pp.397-416.

Baker, H.K., Jabbouri, I. and Dyaz, C. (2017). Corporate finance practices in

Morocco. Managerial Finance, 43(8), 865-880.

BiermanJr, H. and Smidt, S. (2014). Advanced capital budgeting: Refinements in the economic

analysis of investment projects. Oxon: Routledge.

Corelli, A. (2017). Inside company valuation. Switzerland: Springer International Publishing.

Coyle, B. (2002). Equity Finance: Debt Equity Markets. UK: Global Professional Publishi.

Fortescue Metals (2017). Annual Report. [Online]. Available at:

https://www.fmgl.com.au/docs/default-source/default-document-library/fy2017-

annualreport.pdf?sfvrsn=1f931875_2 [Accessed 22 September 2018].

Jung-Senssfelder, K. (2007). Equity financing and covenants in venture capital: An augmented

contracting approach to optimal german contract design (Vol. 58). Inida: Springer Science &

Business Media.

Kisgen, D.J. (2006). Credit ratings and capital structure. The Journal of Finance, 61(3), pp.1035-

1072.

Langohr, H. and Langohr, P. (2010). The rating agencies and their credit ratings: what they are,

how they work, and why they are relevant (Vol. 510). England: John Wiley & Sons.

References

Abdolmohammadi, M.J. (2005). Intellectual capital disclosure and market capitalization. Journal

of intellectual capital, 6(3), pp.397-416.

Baker, H.K., Jabbouri, I. and Dyaz, C. (2017). Corporate finance practices in

Morocco. Managerial Finance, 43(8), 865-880.

BiermanJr, H. and Smidt, S. (2014). Advanced capital budgeting: Refinements in the economic

analysis of investment projects. Oxon: Routledge.

Corelli, A. (2017). Inside company valuation. Switzerland: Springer International Publishing.

Coyle, B. (2002). Equity Finance: Debt Equity Markets. UK: Global Professional Publishi.

Fortescue Metals (2017). Annual Report. [Online]. Available at:

https://www.fmgl.com.au/docs/default-source/default-document-library/fy2017-

annualreport.pdf?sfvrsn=1f931875_2 [Accessed 22 September 2018].

Jung-Senssfelder, K. (2007). Equity financing and covenants in venture capital: An augmented

contracting approach to optimal german contract design (Vol. 58). Inida: Springer Science &

Business Media.

Kisgen, D.J. (2006). Credit ratings and capital structure. The Journal of Finance, 61(3), pp.1035-

1072.

Langohr, H. and Langohr, P. (2010). The rating agencies and their credit ratings: what they are,

how they work, and why they are relevant (Vol. 510). England: John Wiley & Sons.

Finance 12

Morningstar (2018). Fortescue Metals Group Ltd. [Online]. Available at:

https://financials.morningstar.com/ratios/r.html?t=0P00006WI4&culture=en&platform=sal

[Accessed 22 September 2018].

Reuters (2018). Fortescue Metals Group Ltd (FMG.AX). [Online]. Available at:

https://www.reuters.com/finance/stocks/company-profile/FMG.AX [Accessed 22 September

2018].

Shapiro, A. C. (2008). Capital budgeting and investment analysis. India: Pearson Education.

Yahoo Finance (2018). Fortescue Metals Group Limited (FMG.AX). [Online]. Available at:

https://au.finance.yahoo.com/quote/FMG.AX/ [Accessed 22 September 2018].

Morningstar (2018). Fortescue Metals Group Ltd. [Online]. Available at:

https://financials.morningstar.com/ratios/r.html?t=0P00006WI4&culture=en&platform=sal

[Accessed 22 September 2018].

Reuters (2018). Fortescue Metals Group Ltd (FMG.AX). [Online]. Available at:

https://www.reuters.com/finance/stocks/company-profile/FMG.AX [Accessed 22 September

2018].

Shapiro, A. C. (2008). Capital budgeting and investment analysis. India: Pearson Education.

Yahoo Finance (2018). Fortescue Metals Group Limited (FMG.AX). [Online]. Available at:

https://au.finance.yahoo.com/quote/FMG.AX/ [Accessed 22 September 2018].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.