University Name, ACCT20071: IFRS and Intangible Asset Accounting

VerifiedAdded on 2023/06/09

|11

|2458

|91

Report

AI Summary

This research report examines the impact of International Financial Reporting Standards (IFRS) adoption on the accounting for intangible assets, focusing on the Australian context. The report begins with an introduction to the topic, followed by a discussion of the economic consequences of IFRS adoption and the accounting treatment of intangible assets as per IFRS. It then analyzes the specific impacts of IFRS adoption on intangible assets, including the challenges faced by companies in valuation and impairment testing, with Wesfarmers Limited as a case study. The report highlights the difficulties in recognizing and de-recognizing intangible assets, along with the implications for financial statements, such as changes in net assets and debt-to-equity ratios. The conclusion summarizes the key findings and emphasizes the challenges associated with IFRS adoption in the accounting of intangible assets.

Running head: FOUNDATIONS IN ACCOUNTING

Foundations in Accounting

Name of the Student

Name of the University

Author’s Note

Foundations in Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FOUNDATIONS IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Economic Consequences of IFRS Adoption...................................................................................2

Accounting for Intangible Assets as per IFRS................................................................................3

Impact of IFRS Adoption in Intangible Assets................................................................................4

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Table of Contents

Introduction......................................................................................................................................2

Economic Consequences of IFRS Adoption...................................................................................2

Accounting for Intangible Assets as per IFRS................................................................................3

Impact of IFRS Adoption in Intangible Assets................................................................................4

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

2FOUNDATIONS IN ACCOUNTING

Introduction

On 1 January 2005, all the Australian companies had to adopt the principles and

regulations of International Financial Reporting Standards (IFRS) at the time of the preparation

and presentation of the financial statements. From then, it has been challenging for the

companies in Australia in financial accounting due to the implementation of the principles of

IFRS. There have been major changes in the accounting standards and financial reporting of the

companies due to the adoption of IFRS. It was anticipated that there would be significant effects

of the adoption of IFRS on various financial aspects; and one of such aspects is Intangible Assets

(Bryce, Ali & Mather, 2015). After the adoption of the strategies of IFRS, there have been

foremost changes in the intangible assets accounting by the companies. The main aim of this

report is to evaluate different impacts of the adoption of IFRS on the intangible assets accounting

for the companies. For this purpose, Wesfarmers Limited is taken into consideration for this

report. Wesfarmers is one of the leading conglomerates in Australia. The company was

established in the year of 1914 and it is headquartered at Perth, Western Australia, Australia

(wesfarmers.com.au, 2018).

Economic Consequences of IFRS Adoption

The presence of certain objectives can be seen behind the introduction of the standards

and principles of IFRS for the companies all over the world; and there is not any exception of

this fact in case of the Australian companies. It can be observed that there are two major reasons

behind the introduction of the standards and principles of IFRS (Daske et al., 2013). The first

reason can be considered the belief that the adoption of IFRS would bring superior quality in the

accounting works and they are more comprehensive while comparing with the national or

Introduction

On 1 January 2005, all the Australian companies had to adopt the principles and

regulations of International Financial Reporting Standards (IFRS) at the time of the preparation

and presentation of the financial statements. From then, it has been challenging for the

companies in Australia in financial accounting due to the implementation of the principles of

IFRS. There have been major changes in the accounting standards and financial reporting of the

companies due to the adoption of IFRS. It was anticipated that there would be significant effects

of the adoption of IFRS on various financial aspects; and one of such aspects is Intangible Assets

(Bryce, Ali & Mather, 2015). After the adoption of the strategies of IFRS, there have been

foremost changes in the intangible assets accounting by the companies. The main aim of this

report is to evaluate different impacts of the adoption of IFRS on the intangible assets accounting

for the companies. For this purpose, Wesfarmers Limited is taken into consideration for this

report. Wesfarmers is one of the leading conglomerates in Australia. The company was

established in the year of 1914 and it is headquartered at Perth, Western Australia, Australia

(wesfarmers.com.au, 2018).

Economic Consequences of IFRS Adoption

The presence of certain objectives can be seen behind the introduction of the standards

and principles of IFRS for the companies all over the world; and there is not any exception of

this fact in case of the Australian companies. It can be observed that there are two major reasons

behind the introduction of the standards and principles of IFRS (Daske et al., 2013). The first

reason can be considered the belief that the adoption of IFRS would bring superior quality in the

accounting works and they are more comprehensive while comparing with the national or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FOUNDATIONS IN ACCOUNTING

domestic standards. It needs to be mentioned that high quality of financial reporting and effective

financial disclosure has association with the value of the companies along with the market

liquidity. In the presence of this fact, the introduction of IFRS should lead to the increased

market liquidity along with the cost of capital reduction (Brüggemann, Hitz & Sellhorn, 2013).

The second major objective behind the introduction of the standards of IFRS is to bring

comparability in the financial statements so that it becomes less costly for the investors to

compare the financial information of the companies across the countries. This aspect will lead to

the cross-border investments and the incorporation of the capital market all over the world. It can

be seen from the above discussion that the main aim of the introduction of IFRS standards was to

improve the quality as well as accuracy of financial reporting across the countries (Horton,

Serafeim & Serafeim, 2013).

Accounting for Intangible Assets as per IFRS

As per the earlier discussion, the Australian companies adopted the principles of IFRS on

January 1, 2005. In the present situation, Australian Accounting Standard Board (AASB) has

provided the companies with the required standards and regulations for the accounting treatment

of intangible assets as per the standards of IFRS. For this reason, the Australian companies are

required to comply with the standards and regulations of AASB 138 Intangible Assets at the time

of the accounting treatments of intangible assets of their businesses (aasb.gov.au, 2018). This

regulation is also applicable for Wesfarmers. According to AASB 138, the obligation on the

companies for the recognition of intangible assets is when it is probable that there will be a flow

of expected economic profit from the asset to the business organization and it is possible for the

companies to measure the cost of the intangible assets on reliable basis. In this process, the

business organizations have the author to make valid assumptions for gaining the future benefits

domestic standards. It needs to be mentioned that high quality of financial reporting and effective

financial disclosure has association with the value of the companies along with the market

liquidity. In the presence of this fact, the introduction of IFRS should lead to the increased

market liquidity along with the cost of capital reduction (Brüggemann, Hitz & Sellhorn, 2013).

The second major objective behind the introduction of the standards of IFRS is to bring

comparability in the financial statements so that it becomes less costly for the investors to

compare the financial information of the companies across the countries. This aspect will lead to

the cross-border investments and the incorporation of the capital market all over the world. It can

be seen from the above discussion that the main aim of the introduction of IFRS standards was to

improve the quality as well as accuracy of financial reporting across the countries (Horton,

Serafeim & Serafeim, 2013).

Accounting for Intangible Assets as per IFRS

As per the earlier discussion, the Australian companies adopted the principles of IFRS on

January 1, 2005. In the present situation, Australian Accounting Standard Board (AASB) has

provided the companies with the required standards and regulations for the accounting treatment

of intangible assets as per the standards of IFRS. For this reason, the Australian companies are

required to comply with the standards and regulations of AASB 138 Intangible Assets at the time

of the accounting treatments of intangible assets of their businesses (aasb.gov.au, 2018). This

regulation is also applicable for Wesfarmers. According to AASB 138, the obligation on the

companies for the recognition of intangible assets is when it is probable that there will be a flow

of expected economic profit from the asset to the business organization and it is possible for the

companies to measure the cost of the intangible assets on reliable basis. In this process, the

business organizations have the author to make valid assumptions for gaining the future benefits

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FOUNDATIONS IN ACCOUNTING

from those assets. AASB 138 also states that the business organizations have the obligation for

the measurement of the intangible assets at cost process (aasb.gov.au, 2018). In case a business

organization does the acquisition of an intangible asset at no cost, the company is required to

consider the present fair value of those asses as the cost price. Apart from these major

regulations, the companies are needed to comply with different standards for the accounting of

intangible assets (aasb.gov.au, 2018).

Impact of IFRS Adoption in Intangible Assets

After the adoption of the standards of IFRS, it was the most difficult task for the

accounting regulators to regulate the accounting procedures for intangible assets. This is

considered as the major issue due to the major growth in international mergers and acquisitions

along with the rapid growth in the international financial market. In Australia, before the

inception of IFRS, the presence of some accounting standards can be seen for the accounting of

intangible assets; such as AASB 1011 Accounting for Research and Development Costs and

AASB 1013 Accounting for Goodwill. The requirement for the companies was to capitalize and

amortize the purchase of goodwill through earnings via straight-line method over a period of five

to twenty years. The procedures for the accounting of intangible assets was much simpler that the

post period of IFRS introduction (Ahmed, Chalmers & Khlif, 2013).

However, the adoption of the standards of IFRS has forced the accounting standard

setters to adopt a more conservative approach for the intangible asset valuation. As per the

current requirement in AASB 138 as per IFRS, only the externally purchased goodwill and other

intangible assets like patents, licenses and others can be capitalized and subject to the

from those assets. AASB 138 also states that the business organizations have the obligation for

the measurement of the intangible assets at cost process (aasb.gov.au, 2018). In case a business

organization does the acquisition of an intangible asset at no cost, the company is required to

consider the present fair value of those asses as the cost price. Apart from these major

regulations, the companies are needed to comply with different standards for the accounting of

intangible assets (aasb.gov.au, 2018).

Impact of IFRS Adoption in Intangible Assets

After the adoption of the standards of IFRS, it was the most difficult task for the

accounting regulators to regulate the accounting procedures for intangible assets. This is

considered as the major issue due to the major growth in international mergers and acquisitions

along with the rapid growth in the international financial market. In Australia, before the

inception of IFRS, the presence of some accounting standards can be seen for the accounting of

intangible assets; such as AASB 1011 Accounting for Research and Development Costs and

AASB 1013 Accounting for Goodwill. The requirement for the companies was to capitalize and

amortize the purchase of goodwill through earnings via straight-line method over a period of five

to twenty years. The procedures for the accounting of intangible assets was much simpler that the

post period of IFRS introduction (Ahmed, Chalmers & Khlif, 2013).

However, the adoption of the standards of IFRS has forced the accounting standard

setters to adopt a more conservative approach for the intangible asset valuation. As per the

current requirement in AASB 138 as per IFRS, only the externally purchased goodwill and other

intangible assets like patents, licenses and others can be capitalized and subject to the

5FOUNDATIONS IN ACCOUNTING

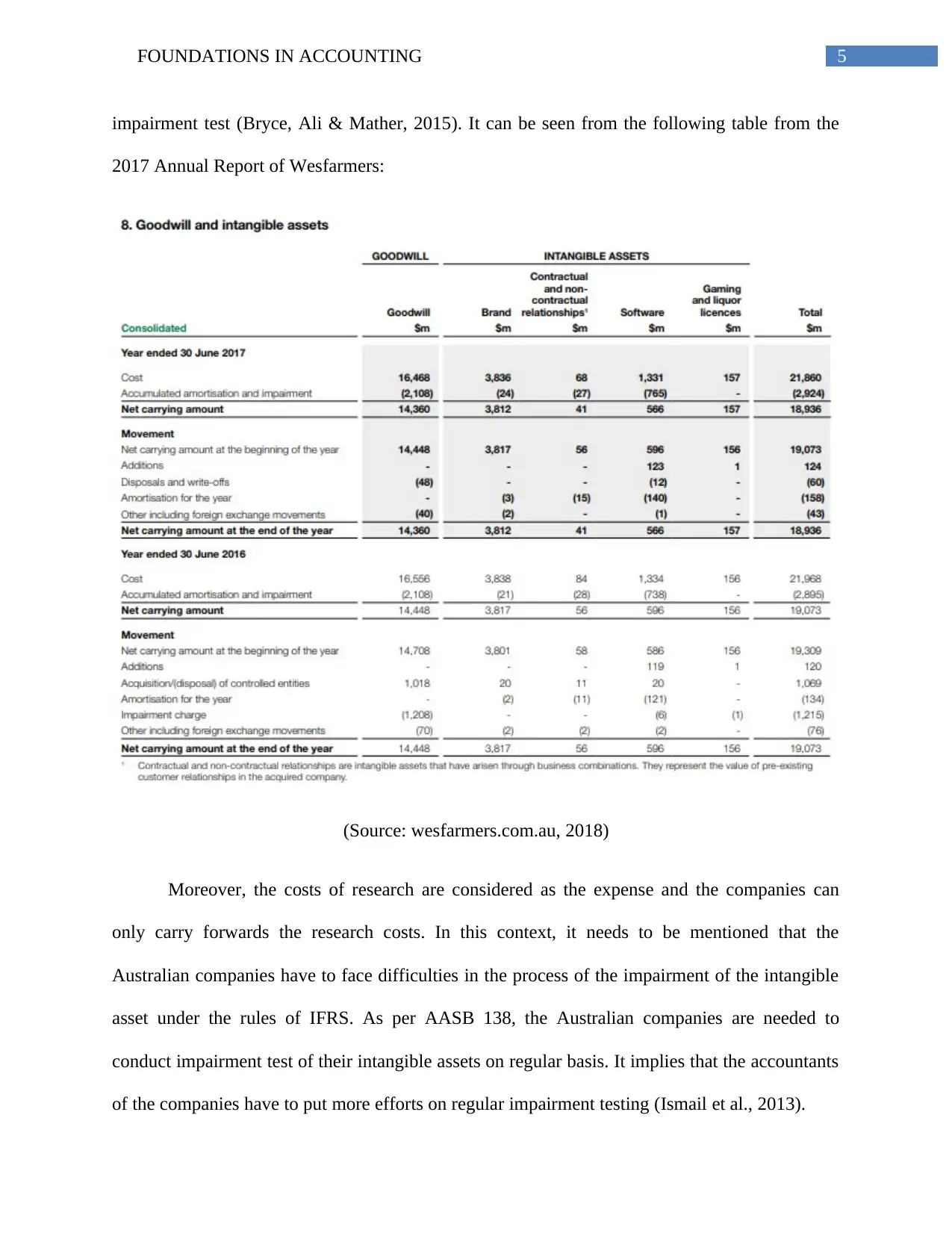

impairment test (Bryce, Ali & Mather, 2015). It can be seen from the following table from the

2017 Annual Report of Wesfarmers:

(Source: wesfarmers.com.au, 2018)

Moreover, the costs of research are considered as the expense and the companies can

only carry forwards the research costs. In this context, it needs to be mentioned that the

Australian companies have to face difficulties in the process of the impairment of the intangible

asset under the rules of IFRS. As per AASB 138, the Australian companies are needed to

conduct impairment test of their intangible assets on regular basis. It implies that the accountants

of the companies have to put more efforts on regular impairment testing (Ismail et al., 2013).

impairment test (Bryce, Ali & Mather, 2015). It can be seen from the following table from the

2017 Annual Report of Wesfarmers:

(Source: wesfarmers.com.au, 2018)

Moreover, the costs of research are considered as the expense and the companies can

only carry forwards the research costs. In this context, it needs to be mentioned that the

Australian companies have to face difficulties in the process of the impairment of the intangible

asset under the rules of IFRS. As per AASB 138, the Australian companies are needed to

conduct impairment test of their intangible assets on regular basis. It implies that the accountants

of the companies have to put more efforts on regular impairment testing (Ismail et al., 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FOUNDATIONS IN ACCOUNTING

The major requirement under the standards of IFRS for the companies is that they are

needed to recognize and record more intangible assets in their financial statements. One major

reason why regulating intangible assets is a controversial as well as difficult job because the

standard setters as well as companies have to face two major dilemmas at the time of considering

the economic consequences of the decisions related to intangible asset valuation (Cascino &

Gassen, 2015). The tradeoff between the possibilities of manipulation vs. the possibilities to

signal at the time of the selection of accounting treatments for intangible assets. Two theories can

be mentioned at this point; they are opportunistic theory and efficient contracting theory. As per

the opportunistic theory, the managers select the accounting policies for the maximization of

their own interests instead of providing valuable information to the investors and the financial

statements users. Thus, under IFRS, the managers of the companies get the chance to do

manipulation with the financial information as they are given discretionary power. As per,

efficient contracting theory, the mangers have the option to provide more true financial position

of the companies with the help of discretionary power (Su & Wells, 2015).

Another major area of impact on the adoption of IFRS standards can be seen in the form

of the de-recognition of the intangible assets of the businesses. Under the standard of AASB 138,

the companies are needed to recognize the intangible assets that have been purchased at cost

value. Thus, the companies are needed to de-recognize the internally generated assets of their

business. This aspect has created difficulties for the accountants of the companies as they have to

go through complex accounting procedures for the recognition as well as de-recognition of the

intangible assets (Christensen & Nikolaev, 2013).

The major requirement under the standards of IFRS for the companies is that they are

needed to recognize and record more intangible assets in their financial statements. One major

reason why regulating intangible assets is a controversial as well as difficult job because the

standard setters as well as companies have to face two major dilemmas at the time of considering

the economic consequences of the decisions related to intangible asset valuation (Cascino &

Gassen, 2015). The tradeoff between the possibilities of manipulation vs. the possibilities to

signal at the time of the selection of accounting treatments for intangible assets. Two theories can

be mentioned at this point; they are opportunistic theory and efficient contracting theory. As per

the opportunistic theory, the managers select the accounting policies for the maximization of

their own interests instead of providing valuable information to the investors and the financial

statements users. Thus, under IFRS, the managers of the companies get the chance to do

manipulation with the financial information as they are given discretionary power. As per,

efficient contracting theory, the mangers have the option to provide more true financial position

of the companies with the help of discretionary power (Su & Wells, 2015).

Another major area of impact on the adoption of IFRS standards can be seen in the form

of the de-recognition of the intangible assets of the businesses. Under the standard of AASB 138,

the companies are needed to recognize the intangible assets that have been purchased at cost

value. Thus, the companies are needed to de-recognize the internally generated assets of their

business. This aspect has created difficulties for the accountants of the companies as they have to

go through complex accounting procedures for the recognition as well as de-recognition of the

intangible assets (Christensen & Nikolaev, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FOUNDATIONS IN ACCOUNTING

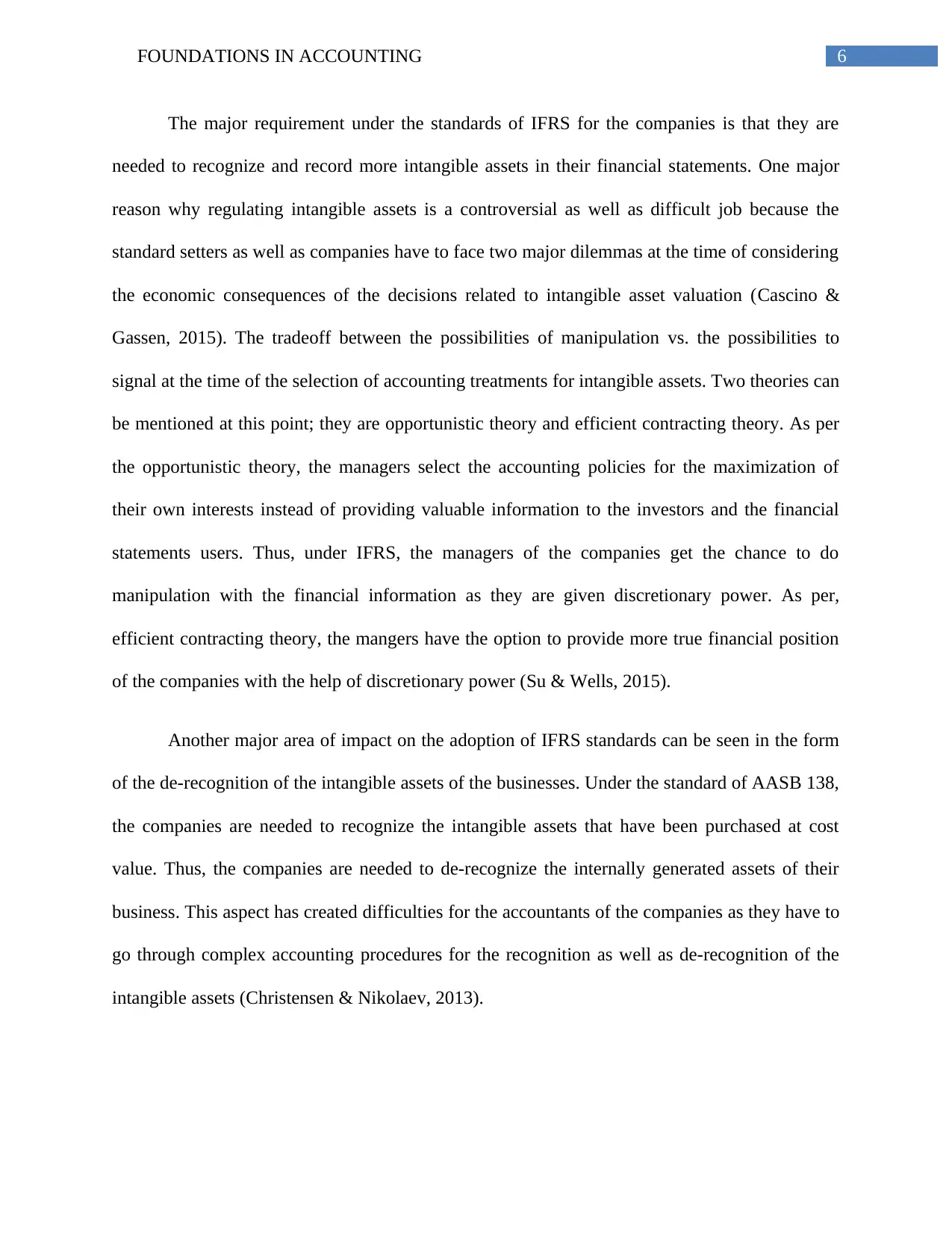

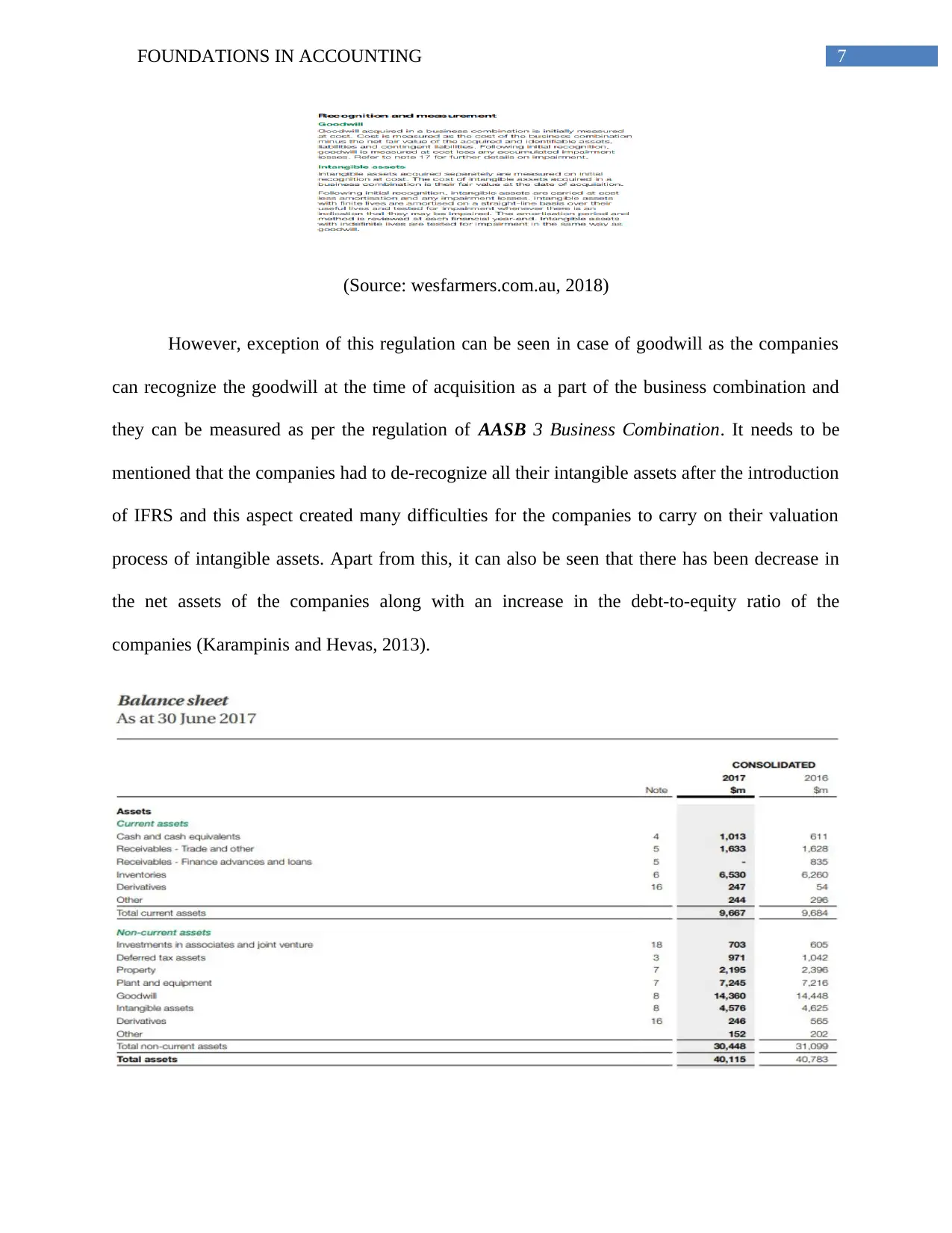

(Source: wesfarmers.com.au, 2018)

However, exception of this regulation can be seen in case of goodwill as the companies

can recognize the goodwill at the time of acquisition as a part of the business combination and

they can be measured as per the regulation of AASB 3 Business Combination. It needs to be

mentioned that the companies had to de-recognize all their intangible assets after the introduction

of IFRS and this aspect created many difficulties for the companies to carry on their valuation

process of intangible assets. Apart from this, it can also be seen that there has been decrease in

the net assets of the companies along with an increase in the debt-to-equity ratio of the

companies (Karampinis and Hevas, 2013).

(Source: wesfarmers.com.au, 2018)

However, exception of this regulation can be seen in case of goodwill as the companies

can recognize the goodwill at the time of acquisition as a part of the business combination and

they can be measured as per the regulation of AASB 3 Business Combination. It needs to be

mentioned that the companies had to de-recognize all their intangible assets after the introduction

of IFRS and this aspect created many difficulties for the companies to carry on their valuation

process of intangible assets. Apart from this, it can also be seen that there has been decrease in

the net assets of the companies along with an increase in the debt-to-equity ratio of the

companies (Karampinis and Hevas, 2013).

8FOUNDATIONS IN ACCOUNTING

(Source: wesfarmers.com.au, 2018)

Along with the above, there are many instances where the companies have to face

immense difficulties in meeting their excising debt agreements in the presence of the ne IFRS

standards. It needs to be mentioned that in the year 2004, large number of firms were not

fundamentally prepared to adopt the IFRS principles and this aspect create difficulties for them

(Christensen & Nikolaev, 2013).

It can be observed that many Australian companies requested AASB for exempt

themselves from compiling with the regulations of IFRS related to the intangible asset valuation.

In this context, the aim of IFRS needs to be mentioned that is to implement a uniform accounting

system for the countries all over the world. For this reason, the International Accounting

Standard Board (IASB) overrode the demand of these companies (Ahmed, Chalmers & Khlif,

2013).

Conclusion

From the above discussion, it can be seen that the main aim of the introduction of new

standards of IFRS was the establishment of a uniform accounting standards and the accounting

for intangible assets was one of them. The above discussion shows the fact that the Australian

companies have to face some major difficulties from the adoption of the standards of IFRS

related to intangible assets. Most of the companies had to de-recognize their intangible assets as

they are needed to consider the cost value of the intangible assets. It can also be observed that the

IASB has not materialized the request of the Australian companies to exempt them from the

IFRS regulations of the intangible assets.

(Source: wesfarmers.com.au, 2018)

Along with the above, there are many instances where the companies have to face

immense difficulties in meeting their excising debt agreements in the presence of the ne IFRS

standards. It needs to be mentioned that in the year 2004, large number of firms were not

fundamentally prepared to adopt the IFRS principles and this aspect create difficulties for them

(Christensen & Nikolaev, 2013).

It can be observed that many Australian companies requested AASB for exempt

themselves from compiling with the regulations of IFRS related to the intangible asset valuation.

In this context, the aim of IFRS needs to be mentioned that is to implement a uniform accounting

system for the countries all over the world. For this reason, the International Accounting

Standard Board (IASB) overrode the demand of these companies (Ahmed, Chalmers & Khlif,

2013).

Conclusion

From the above discussion, it can be seen that the main aim of the introduction of new

standards of IFRS was the establishment of a uniform accounting standards and the accounting

for intangible assets was one of them. The above discussion shows the fact that the Australian

companies have to face some major difficulties from the adoption of the standards of IFRS

related to intangible assets. Most of the companies had to de-recognize their intangible assets as

they are needed to consider the cost value of the intangible assets. It can also be observed that the

IASB has not materialized the request of the Australian companies to exempt them from the

IFRS regulations of the intangible assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FOUNDATIONS IN ACCOUNTING

References

2017 Annual Report. (2018). Retrieved from http://www.wesfarmers.com.au/docs/default-

source/reports/j000901-ar17_interactive_final.pdf?sfvrsn=4

Adibah Wan Ismail, W., Anuar Kamarudin, K., van Zijl, T., & Dunstan, K. (2013). Earnings

quality and the adoption of IFRS-based accounting standards: Evidence from an

emerging market. Asian Review of Accounting, 21(1), 53-73.

Ahmed, K., Chalmers, K., & Khlif, H. (2013). A meta-analysis of IFRS adoption effects. The

International Journal of Accounting, 48(2), 173-217.

Brüggemann, U., Hitz, J. M., & Sellhorn, T. (2013). Intended and unintended consequences of

mandatory IFRS adoption: A review of extant evidence and suggestions for future

research. European Accounting Review, 22(1), 1-37.

Bryce, M., Ali, M. J., & Mather, P. R. (2015). Accounting quality in the pre-/post-IFRS adoption

periods and the impact on audit committee effectiveness—Evidence from

Australia. Pacific-Basin Finance Journal, 35, 163-181.

Cascino, S., & Gassen, J. (2015). What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies, 20(1), 242-282.

Christensen, H. B., & Nikolaev, V. V. (2013). Does fair value accounting for non-financial assets

pass the market test?. Review of Accounting Studies, 18(3), 734-775.

References

2017 Annual Report. (2018). Retrieved from http://www.wesfarmers.com.au/docs/default-

source/reports/j000901-ar17_interactive_final.pdf?sfvrsn=4

Adibah Wan Ismail, W., Anuar Kamarudin, K., van Zijl, T., & Dunstan, K. (2013). Earnings

quality and the adoption of IFRS-based accounting standards: Evidence from an

emerging market. Asian Review of Accounting, 21(1), 53-73.

Ahmed, K., Chalmers, K., & Khlif, H. (2013). A meta-analysis of IFRS adoption effects. The

International Journal of Accounting, 48(2), 173-217.

Brüggemann, U., Hitz, J. M., & Sellhorn, T. (2013). Intended and unintended consequences of

mandatory IFRS adoption: A review of extant evidence and suggestions for future

research. European Accounting Review, 22(1), 1-37.

Bryce, M., Ali, M. J., & Mather, P. R. (2015). Accounting quality in the pre-/post-IFRS adoption

periods and the impact on audit committee effectiveness—Evidence from

Australia. Pacific-Basin Finance Journal, 35, 163-181.

Cascino, S., & Gassen, J. (2015). What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies, 20(1), 242-282.

Christensen, H. B., & Nikolaev, V. V. (2013). Does fair value accounting for non-financial assets

pass the market test?. Review of Accounting Studies, 18(3), 734-775.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FOUNDATIONS IN ACCOUNTING

Daske, H., Hail, L., Leuz, C., & Verdi, R. (2013). Adopting a label: Heterogeneity in the

economic consequences around IAS/IFRS adoptions. Journal of Accounting

Research, 51(3), 495-547.

Group, D. (2018). Who we are . Wesfarmers.com.au. Retrieved 7 August 2018, from

http://www.wesfarmers.com.au/who-we-are/who-we-are

Horton, J., Serafeim, G., & Serafeim, I. (2013). Does mandatory IFRS adoption improve the

information environment?. Contemporary accounting research, 30(1), 388-423.

Impairment of Assets. (2018). Retrieved from

http://www.aasb.gov.au/admin/file/content102/c3/AASB136_07-04_ERDRjun10_07-

09.pdf

Intangible Assets. (2018). Retrieved from

http://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-

18.pdf

Karampinis, N.I. and Hevas, D.L., 2013. Effects of IFRS adoption on tax-induced incentives for

financial earnings management: evidence from Greece. The International Journal of

Accounting, 48(2), pp.218-247.

Su, W. H., & Wells, P. (2015). The association of identifiable intangible assets acquired and

recognised in business acquisitions with postacquisition firm performance. Accounting &

Finance, 55(4), 1171-1199.

Daske, H., Hail, L., Leuz, C., & Verdi, R. (2013). Adopting a label: Heterogeneity in the

economic consequences around IAS/IFRS adoptions. Journal of Accounting

Research, 51(3), 495-547.

Group, D. (2018). Who we are . Wesfarmers.com.au. Retrieved 7 August 2018, from

http://www.wesfarmers.com.au/who-we-are/who-we-are

Horton, J., Serafeim, G., & Serafeim, I. (2013). Does mandatory IFRS adoption improve the

information environment?. Contemporary accounting research, 30(1), 388-423.

Impairment of Assets. (2018). Retrieved from

http://www.aasb.gov.au/admin/file/content102/c3/AASB136_07-04_ERDRjun10_07-

09.pdf

Intangible Assets. (2018). Retrieved from

http://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-

18.pdf

Karampinis, N.I. and Hevas, D.L., 2013. Effects of IFRS adoption on tax-induced incentives for

financial earnings management: evidence from Greece. The International Journal of

Accounting, 48(2), pp.218-247.

Su, W. H., & Wells, P. (2015). The association of identifiable intangible assets acquired and

recognised in business acquisitions with postacquisition firm performance. Accounting &

Finance, 55(4), 1171-1199.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.