Analysis of Laurie Manufacturing's Management Accounting Report

VerifiedAdded on 2022/11/09

|12

|973

|131

Report

AI Summary

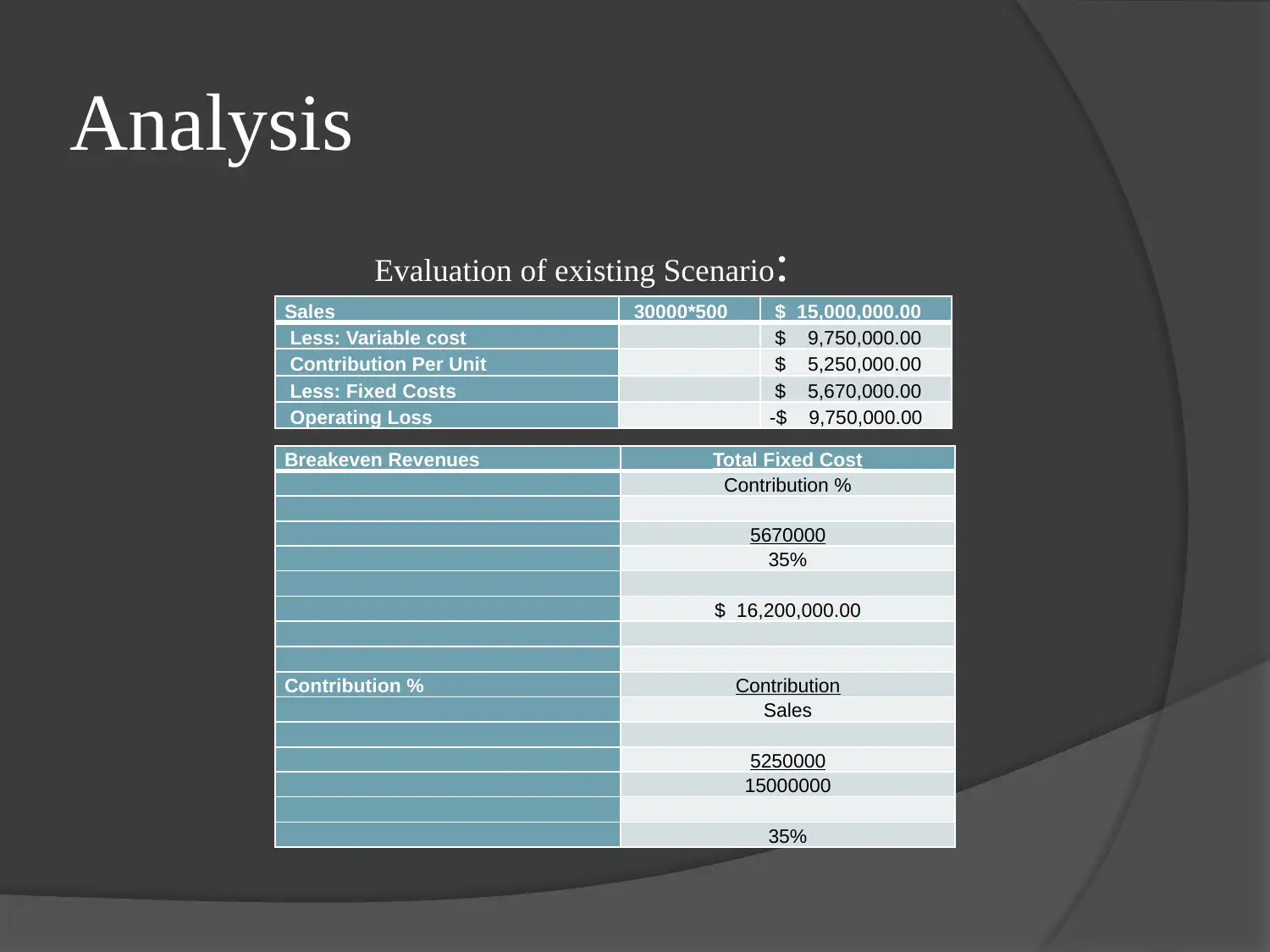

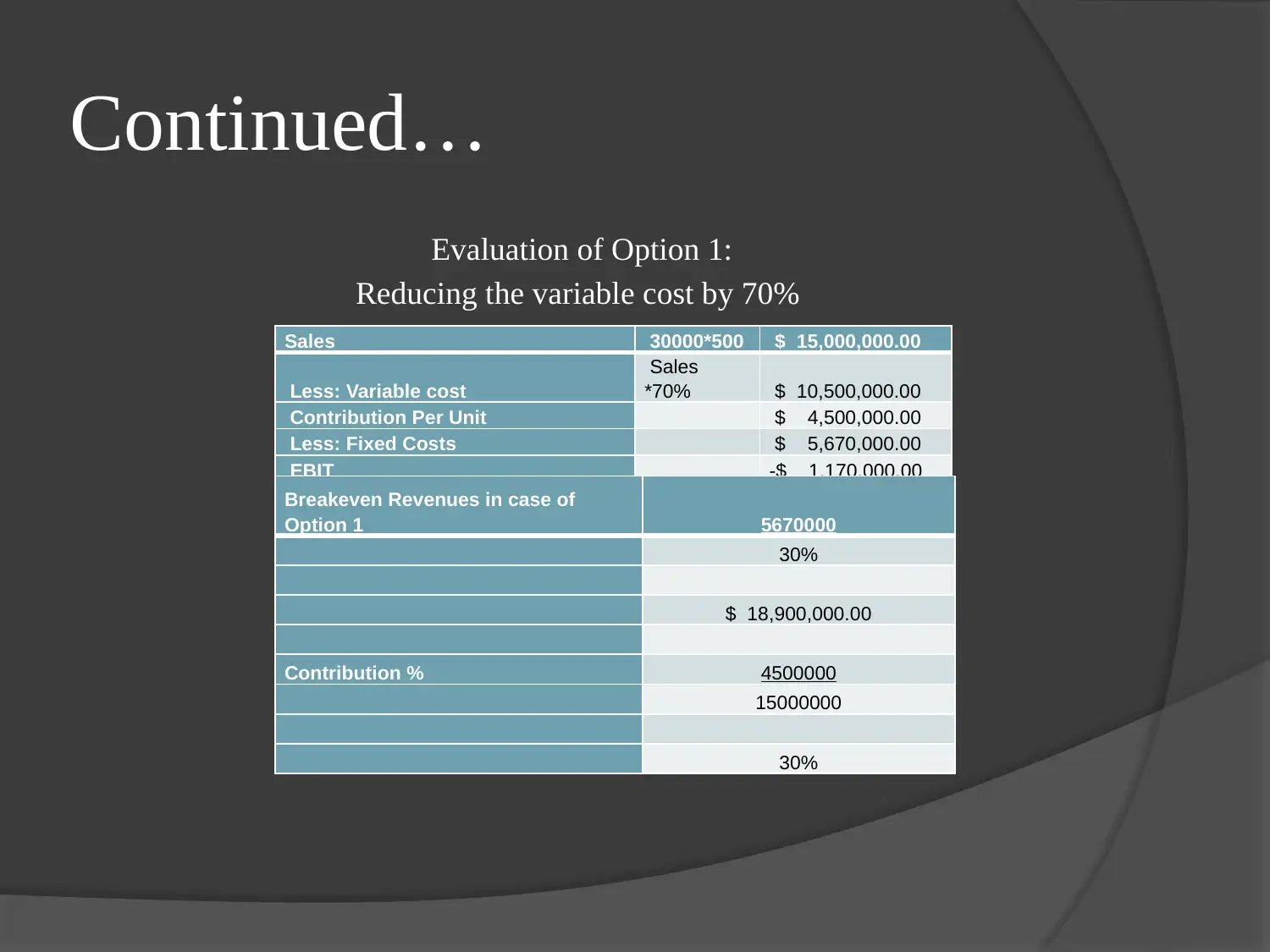

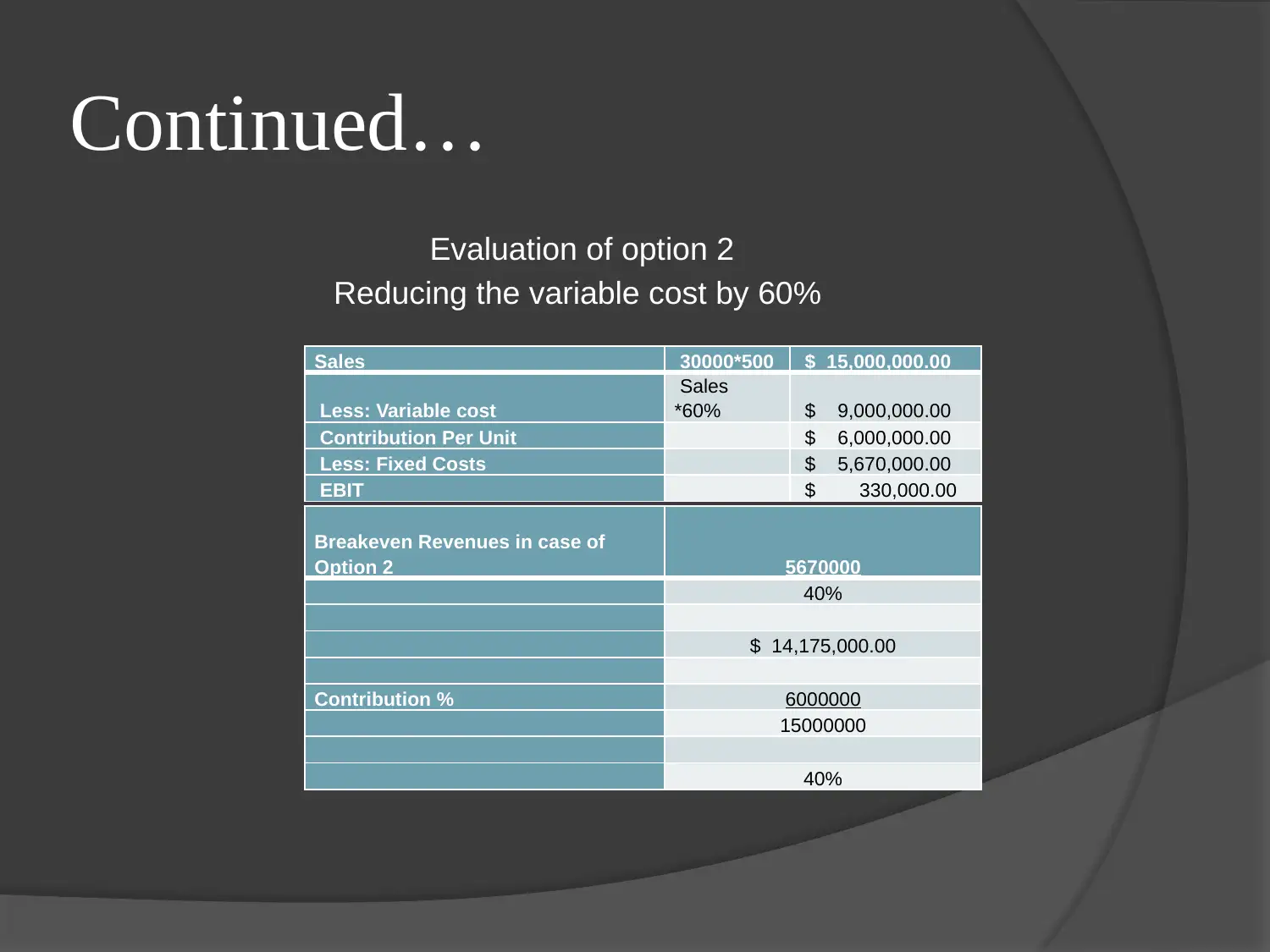

This report analyzes the management accounting case of Laurie Manufacturing Pty Ltd., a company manufacturing grass collection attachments. The analysis focuses on the company's operational profitability in 2018, revealing operational losses. Two options for improvement are evaluated: reducing variable costs and reducing waste disposal costs. The report examines the impact of each option on profitability, break-even points, and ethical considerations, highlighting the potential environmental repercussions of cost-cutting measures. The findings indicate that while reducing waste disposal costs improves profitability, it raises ethical concerns. The report provides limitations of each scenario and suggests action items for increasing sales or reducing costs responsibly. The report also critiques the management accountant's decision, emphasizing the importance of ethical considerations and the inclusion of environmental costs in decision-making to avoid incorrect estimations and potential long-term financial and non-monetary implications. The report follows APA referencing style.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.