Capital Budgeting: FP17 Project Financial Analysis and Evaluation

VerifiedAdded on 2020/03/16

|15

|2114

|168

Report

AI Summary

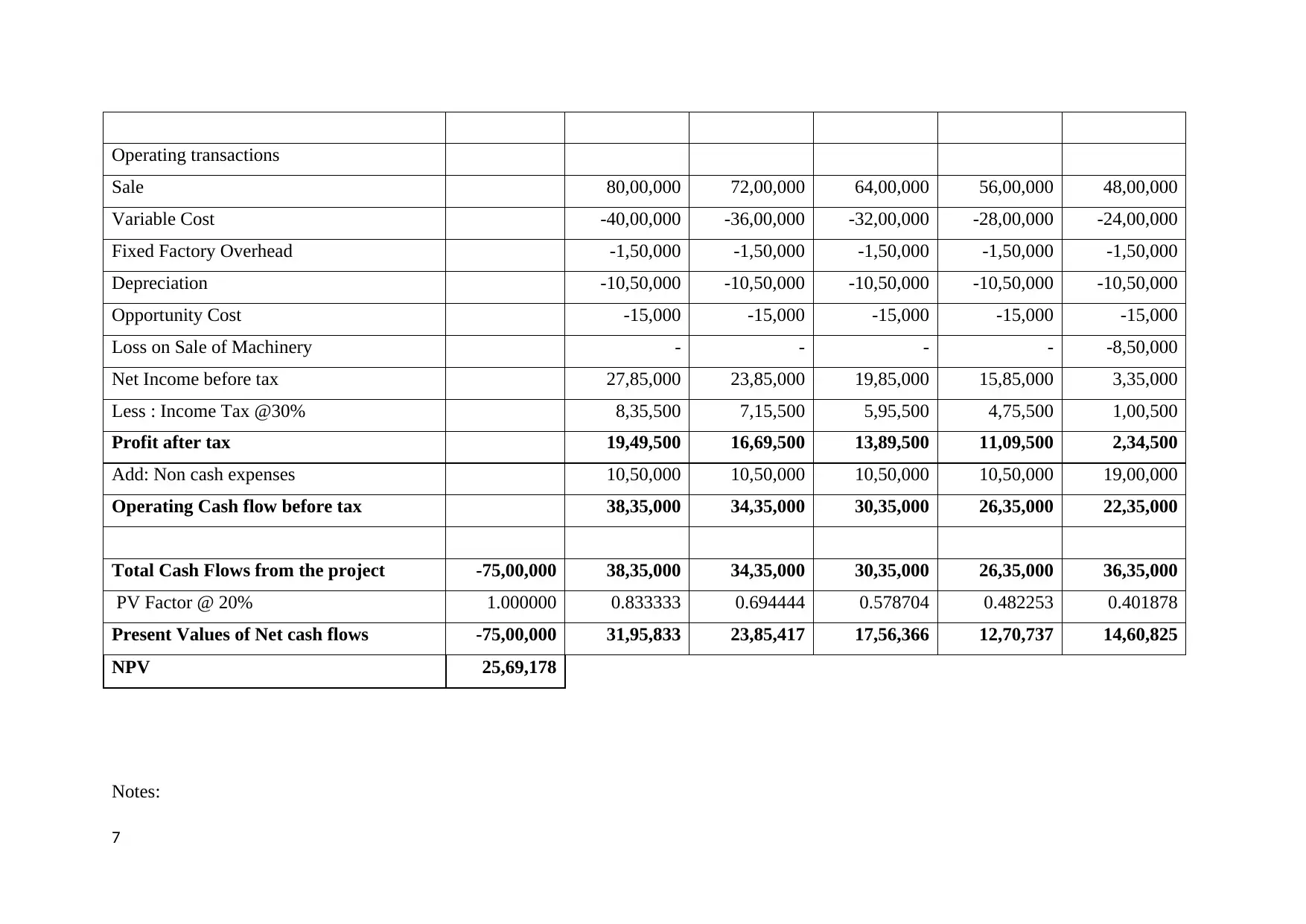

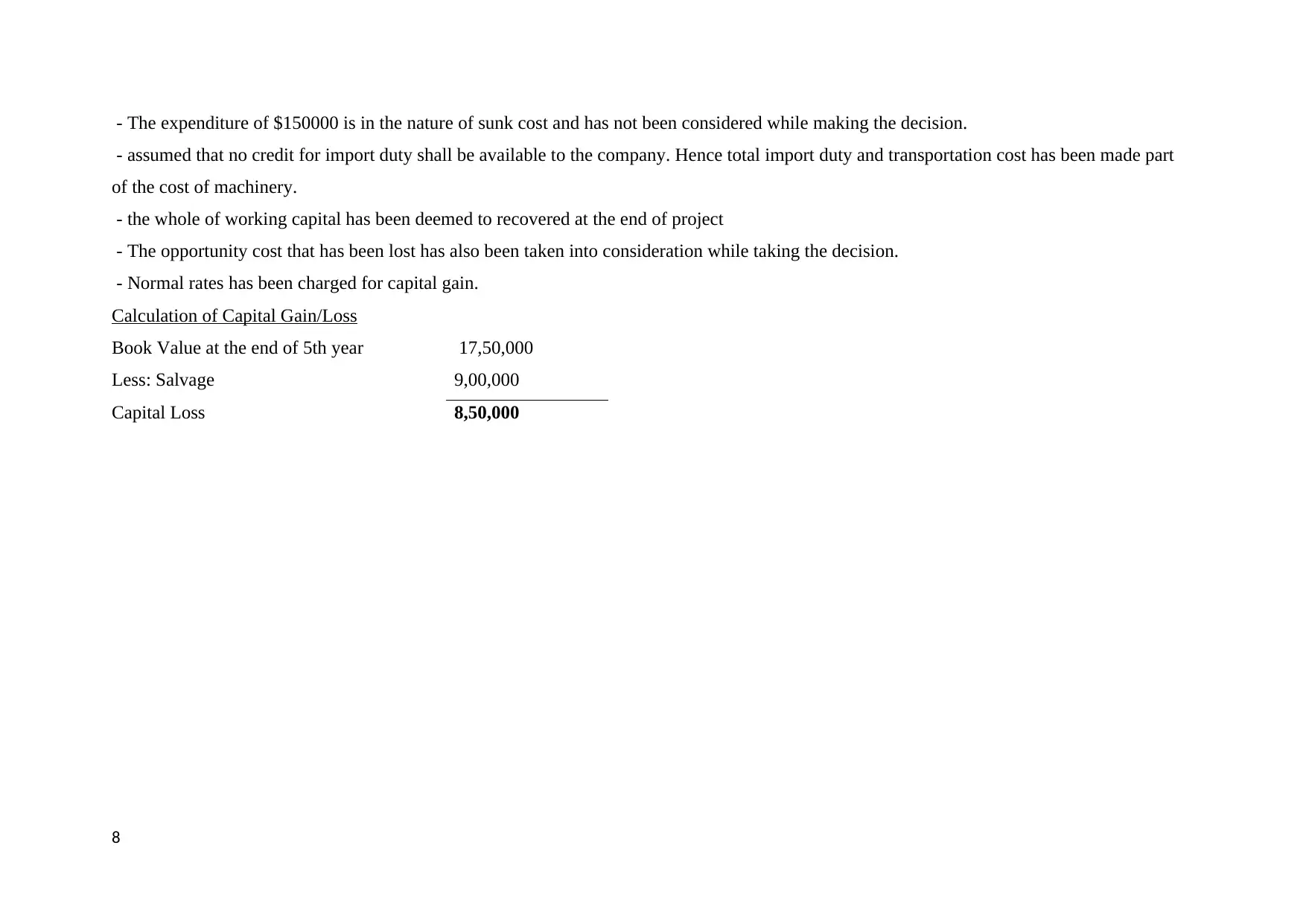

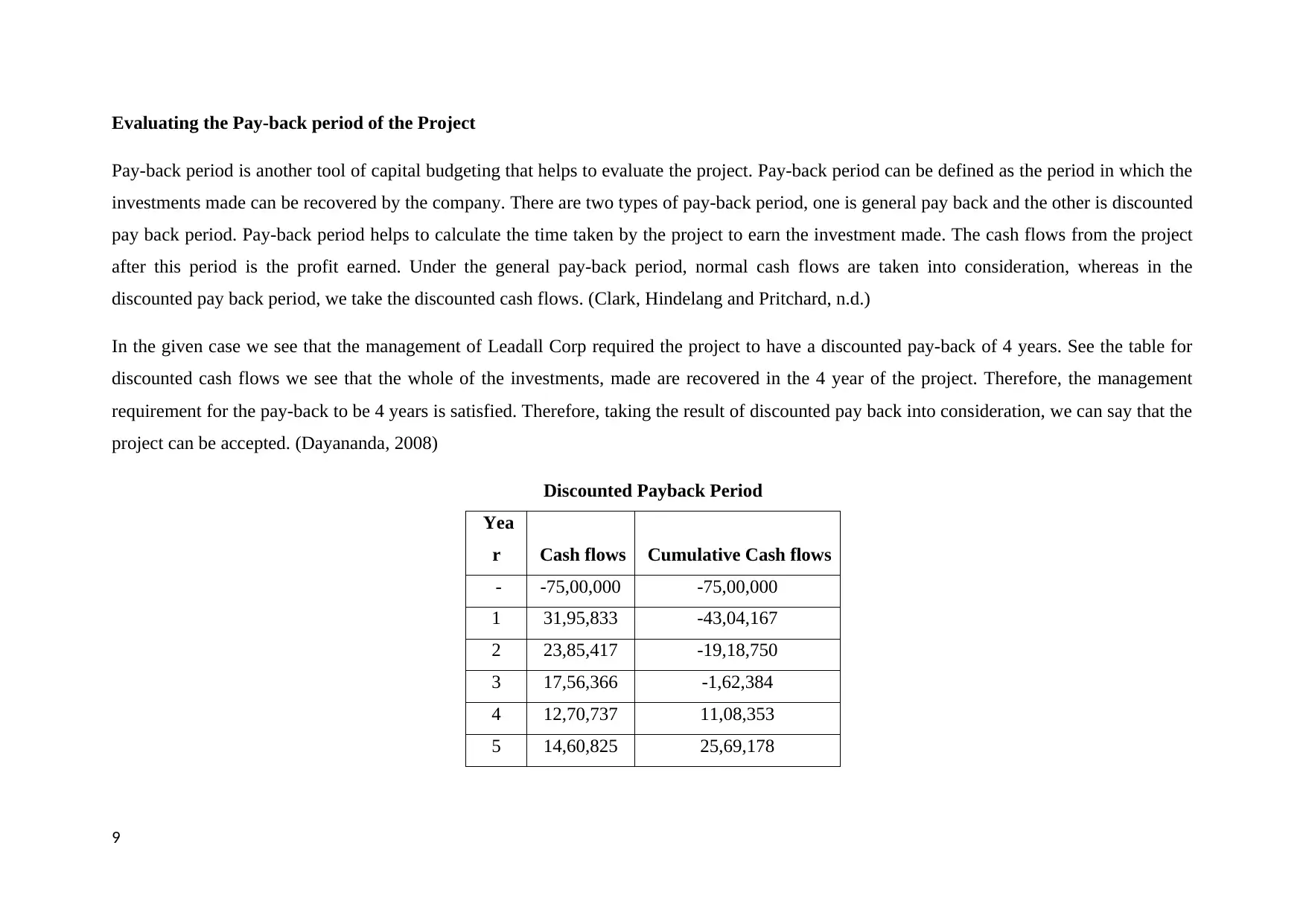

This report provides a comprehensive analysis of the FP17 project for Leadall Corp, focusing on capital budgeting techniques. It begins with an executive summary and introduction to capital budgeting, emphasizing its role in organizational decision-making. The findings section presents both quantitative and qualitative analyses. The quantitative analysis includes detailed calculations of the project's Net Present Value (NPV) and discounted payback period, demonstrating the financial viability of the project. The qualitative analysis considers factors such as fund availability, working capital requirements, economic volatility, government policies, and the importance of accurate assumptions in capital budgeting. The recommendation section concludes that the project should be accepted based on the positive NPV and the satisfaction of the management's payback period requirement. The report also assesses the impact of allocating a portion of sales revenue to Research & Development, showing that the project remains viable. The report concludes by summarizing the key findings and reinforcing the utility of capital budgeting for sound financial decision-making. The report includes calculations and references to support its findings.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.