Applied Financial Planning (FPC002): Client Services & Obligations

VerifiedAdded on 2023/06/03

|44

|18268

|379

Report

AI Summary

This assignment focuses on outlining the initial and ongoing financial planning services provided to clients, specifically Simon and Nadia Johnson. It details the role of a financial advisor, including the services offered and the remuneration structure, ensuring FOFA compliance. The assignment explains the financial planning process, emphasizing the steps taken to provide the best advice and meet financial planning obligations. It also covers potential problems arising from non-compliance and the recourse available to clients in case of disputes. The assignment provides a verbal response to the clients, addressing their concerns and explaining the services in a clear and understandable manner.

Applied Financial Planning

(FPC002)

Assignment

Total marks: 100

Personal ID: 1046

I have read the Assignment Guide in the ‘General assessment information’ and have applied the

word count principles to my work.

My word count for this assignment is: [Enter your word count] words

Your assignment should be loaded into KapLearn by 11.30 pm on the due date.

All times are based on AEDT/AEST time zones.

Refer to ‘Time remaining’ on the ‘Assignment’ page in KapLearn to ensure you submit

your assignment by the specified due date and time.

Checklist

I have completed my assignment using Word and Excel.

I have completed my assignment using Calibri, Arial, Times New Roman or Verdana fonts.

I have added my Personal ID on this page.

I have added my word count on this page.

I have added my Personal ID in front of the filename in the footer on the second page.

I have saved the file to be uploaded as PersonalID_FPC002_AS_v6

Each question of my assignment is within the word limit guidelines for that question as per the

‘General assessment information’ (Assessment Assignment General assessment information).

My assignment file size is no larger than 2 MB.

If tables were required, they are visible as text, not as links or images.

I have not removed the marking grid from the footer.

I have submitted my assignment as per the instructions in KapLearn.

(FPC002)

Assignment

Total marks: 100

Personal ID: 1046

I have read the Assignment Guide in the ‘General assessment information’ and have applied the

word count principles to my work.

My word count for this assignment is: [Enter your word count] words

Your assignment should be loaded into KapLearn by 11.30 pm on the due date.

All times are based on AEDT/AEST time zones.

Refer to ‘Time remaining’ on the ‘Assignment’ page in KapLearn to ensure you submit

your assignment by the specified due date and time.

Checklist

I have completed my assignment using Word and Excel.

I have completed my assignment using Calibri, Arial, Times New Roman or Verdana fonts.

I have added my Personal ID on this page.

I have added my word count on this page.

I have added my Personal ID in front of the filename in the footer on the second page.

I have saved the file to be uploaded as PersonalID_FPC002_AS_v6

Each question of my assignment is within the word limit guidelines for that question as per the

‘General assessment information’ (Assessment Assignment General assessment information).

My assignment file size is no larger than 2 MB.

If tables were required, they are visible as text, not as links or images.

I have not removed the marking grid from the footer.

I have submitted my assignment as per the instructions in KapLearn.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marker feedback

Comment on overall performance:

For marker use only.

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 2 © Kaplan Higher Education

Comment on overall performance:

For marker use only.

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 2 © Kaplan Higher Education

Instructions to students

• This assignment covers all topics and accounts for 50% of your final grade.

• There is one (1) case study in this assignment:

– Section A contains two (2) questions worth a total of 35 marks

– Section B contains three (3) questions worth a total of 65 marks.

You should answer all questions.

• The overall word limit for the assignment is 5,250 words. Marks will only be awarded for answers up

to the word limit (plus 10%) for each question. Any material written after this will not be counted

towards your mark for that question. Headings, quotes and references within the body of the answer

are included in the word count. Numerical tables, calculations, and reference lists are not included.

For more information on word counts and their rationale, go to Assessment Assignment

General assessment information.

• Refer to the Criteria-based Marking Guide for guidelines on what is expected for each question.

• The ‘General assessment information’ section in KapLearn contains information about format and

presentation, word limits, citations and referencing, collusion, plagiarism and other policies,

useful resources, submitting your assignment and accessing your results.

• Full workings must be shown for all calculations. Show all calculations in the text of your assignment and

NOT attached as an appendix, unless specifically stated in the question.

• Answers are to be in your own words. Reference and cite all your sources (within the text of your

answer) when quoting or using material from external sources. Include a reference list at the end of

your assignment. Refer to the ‘Referencing and Citations Guide’ available from the ‘Library Learning

Hub’ in KapLearn for further information on referencing.

• Indicative weightings are noted beside each question. Use these weightings to assist you with your

allocation of time and resources. The weightings indicate the relative importance of each question.

• State all assumptions used in providing your answer.

• Requests for special consideration or information pertaining to special consideration written in the body

of the assignment will not be considered by the marker. Refer to the ‘special consideration’ section of

the Assessment Policy on Kaplan’s website for more information.

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 3 © Kaplan Higher Education

• This assignment covers all topics and accounts for 50% of your final grade.

• There is one (1) case study in this assignment:

– Section A contains two (2) questions worth a total of 35 marks

– Section B contains three (3) questions worth a total of 65 marks.

You should answer all questions.

• The overall word limit for the assignment is 5,250 words. Marks will only be awarded for answers up

to the word limit (plus 10%) for each question. Any material written after this will not be counted

towards your mark for that question. Headings, quotes and references within the body of the answer

are included in the word count. Numerical tables, calculations, and reference lists are not included.

For more information on word counts and their rationale, go to Assessment Assignment

General assessment information.

• Refer to the Criteria-based Marking Guide for guidelines on what is expected for each question.

• The ‘General assessment information’ section in KapLearn contains information about format and

presentation, word limits, citations and referencing, collusion, plagiarism and other policies,

useful resources, submitting your assignment and accessing your results.

• Full workings must be shown for all calculations. Show all calculations in the text of your assignment and

NOT attached as an appendix, unless specifically stated in the question.

• Answers are to be in your own words. Reference and cite all your sources (within the text of your

answer) when quoting or using material from external sources. Include a reference list at the end of

your assignment. Refer to the ‘Referencing and Citations Guide’ available from the ‘Library Learning

Hub’ in KapLearn for further information on referencing.

• Indicative weightings are noted beside each question. Use these weightings to assist you with your

allocation of time and resources. The weightings indicate the relative importance of each question.

• State all assumptions used in providing your answer.

• Requests for special consideration or information pertaining to special consideration written in the body

of the assignment will not be considered by the marker. Refer to the ‘special consideration’ section of

the Assessment Policy on Kaplan’s website for more information.

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 3 © Kaplan Higher Education

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Learning outcomes (LO) mapping Marks

1. Apply techniques to establish and develop client relationships. 10

4. Conduct appropriate quantitative and qualitative research as part of the financial planning

process.

20

5. Assess clients’ goals and financial position to form the basis of advice. 30

6. Design a suitable asset allocation and investment strategy for a client. 10

7. Present recommendations of suitable products and strategies that you have developed. 20

8. Apply the financial planning process to ensure clients’ objectives and needs are met. 10

Total marks 100

Criteria-based Marking Guide

The Criteria-based Marking Guide provided at the end of each question is designed to assist students to

understand what is expected of them in each question and to let them know how their performance will be

judged. It provides advice about the criteria used in the marking of the question and what discriminates

between an excellent, satisfactory and unsatisfactory answer.

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 4 © Kaplan Higher Education

1. Apply techniques to establish and develop client relationships. 10

4. Conduct appropriate quantitative and qualitative research as part of the financial planning

process.

20

5. Assess clients’ goals and financial position to form the basis of advice. 30

6. Design a suitable asset allocation and investment strategy for a client. 10

7. Present recommendations of suitable products and strategies that you have developed. 20

8. Apply the financial planning process to ensure clients’ objectives and needs are met. 10

Total marks 100

Criteria-based Marking Guide

The Criteria-based Marking Guide provided at the end of each question is designed to assist students to

understand what is expected of them in each question and to let them know how their performance will be

judged. It provides advice about the criteria used in the marking of the question and what discriminates

between an excellent, satisfactory and unsatisfactory answer.

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 4 © Kaplan Higher Education

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Background

You are a financial adviser employed with MoneySmart Financial Services. You are licensed to advise in all

types of securities, managed investments, superannuation and insurance. You have formal referral

arrangements with other advisers for estate planning and mortgage/debt advice, therefore you do not

need to cover these areas in any detail in your answers.

Assume you have provided your clients with a financial services guide. Your licensee’s approved product list

is at Appendix A.

Case study: Simon and Nadia Johnson

Simon and Nadia Johnson have been referred to you by their accountant for investment advice.

Nadia received an inheritance of $600,000 from her father’s estate two years ago. Shortly after,

their accountant established a discretionary trust for these inherited funds named the

Johnson Family Trust. The trustee is a company, Johnson Pty Ltd, of which Simon and Nadia are directors.

The beneficiaries of the trust are Simon, Nadia and their two children. Wills and enduring powers of

attorney have also been established. The family trust can take most forms of investment and registered

securities; however, no investment strategy has been established. The inheritance was originally placed in

a one-month Bank of Melbourne term deposit, which has been rolling over monthly since then and is

currently paying 1.0% p.a. interest. The trust costs them $2,000 p.a. to run.

Nadia has had little experience with investing but would like to increase her knowledge. Simon is more

confident about his knowledge of financial matters but like Nadia is time-poor. He understands the need for

diversification and the benefits of long-term growth assets. They have a long-term investment outlook of

10 years and are interested in both managed investments and maybe direct Australian shares.

Simon and Nadia’s completed fact find and risk profiling questionnaires are at Appendix B.

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 5 © Kaplan Higher Education

You are a financial adviser employed with MoneySmart Financial Services. You are licensed to advise in all

types of securities, managed investments, superannuation and insurance. You have formal referral

arrangements with other advisers for estate planning and mortgage/debt advice, therefore you do not

need to cover these areas in any detail in your answers.

Assume you have provided your clients with a financial services guide. Your licensee’s approved product list

is at Appendix A.

Case study: Simon and Nadia Johnson

Simon and Nadia Johnson have been referred to you by their accountant for investment advice.

Nadia received an inheritance of $600,000 from her father’s estate two years ago. Shortly after,

their accountant established a discretionary trust for these inherited funds named the

Johnson Family Trust. The trustee is a company, Johnson Pty Ltd, of which Simon and Nadia are directors.

The beneficiaries of the trust are Simon, Nadia and their two children. Wills and enduring powers of

attorney have also been established. The family trust can take most forms of investment and registered

securities; however, no investment strategy has been established. The inheritance was originally placed in

a one-month Bank of Melbourne term deposit, which has been rolling over monthly since then and is

currently paying 1.0% p.a. interest. The trust costs them $2,000 p.a. to run.

Nadia has had little experience with investing but would like to increase her knowledge. Simon is more

confident about his knowledge of financial matters but like Nadia is time-poor. He understands the need for

diversification and the benefits of long-term growth assets. They have a long-term investment outlook of

10 years and are interested in both managed investments and maybe direct Australian shares.

Simon and Nadia’s completed fact find and risk profiling questionnaires are at Appendix B.

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 5 © Kaplan Higher Education

Section A (35 marks)

Instructions to students

There are two (2) questions in this section. Answer all questions.

Question 1 (10 marks | Word limit: 700 words)

LO8: Apply the financial planning process to ensure clients’ objectives and needs are met.

Outline the details of the initial and ongoing services you will provide to Simon and Nadia. Your answer must

be written as a direct verbal response to the clients and should include the following (answer each section

separately):

(a) Explain what a financial adviser’s role is, and what services you can provide to your clients. (2 marks)

(b) How will you be remunerated and by whom. (Ensure your answer is FOFA compliant.) (1 mark)

(c) Explain the process and/or steps you will apply and the reasons why, in order to provide the best

advice for them and to satisfy your financial planning obligations. (4 marks)

(d) Describe the problems that could arise for both you and your clients if you do not fulfil your

obligations. (2 marks)

(e) Explain the recourse available to your clients if there is a dispute about the advice you provide to

them. (1 mark)

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 6 © Kaplan Higher Education

Instructions to students

There are two (2) questions in this section. Answer all questions.

Question 1 (10 marks | Word limit: 700 words)

LO8: Apply the financial planning process to ensure clients’ objectives and needs are met.

Outline the details of the initial and ongoing services you will provide to Simon and Nadia. Your answer must

be written as a direct verbal response to the clients and should include the following (answer each section

separately):

(a) Explain what a financial adviser’s role is, and what services you can provide to your clients. (2 marks)

(b) How will you be remunerated and by whom. (Ensure your answer is FOFA compliant.) (1 mark)

(c) Explain the process and/or steps you will apply and the reasons why, in order to provide the best

advice for them and to satisfy your financial planning obligations. (4 marks)

(d) Describe the problems that could arise for both you and your clients if you do not fulfil your

obligations. (2 marks)

(e) Explain the recourse available to your clients if there is a dispute about the advice you provide to

them. (1 mark)

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 6 © Kaplan Higher Education

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

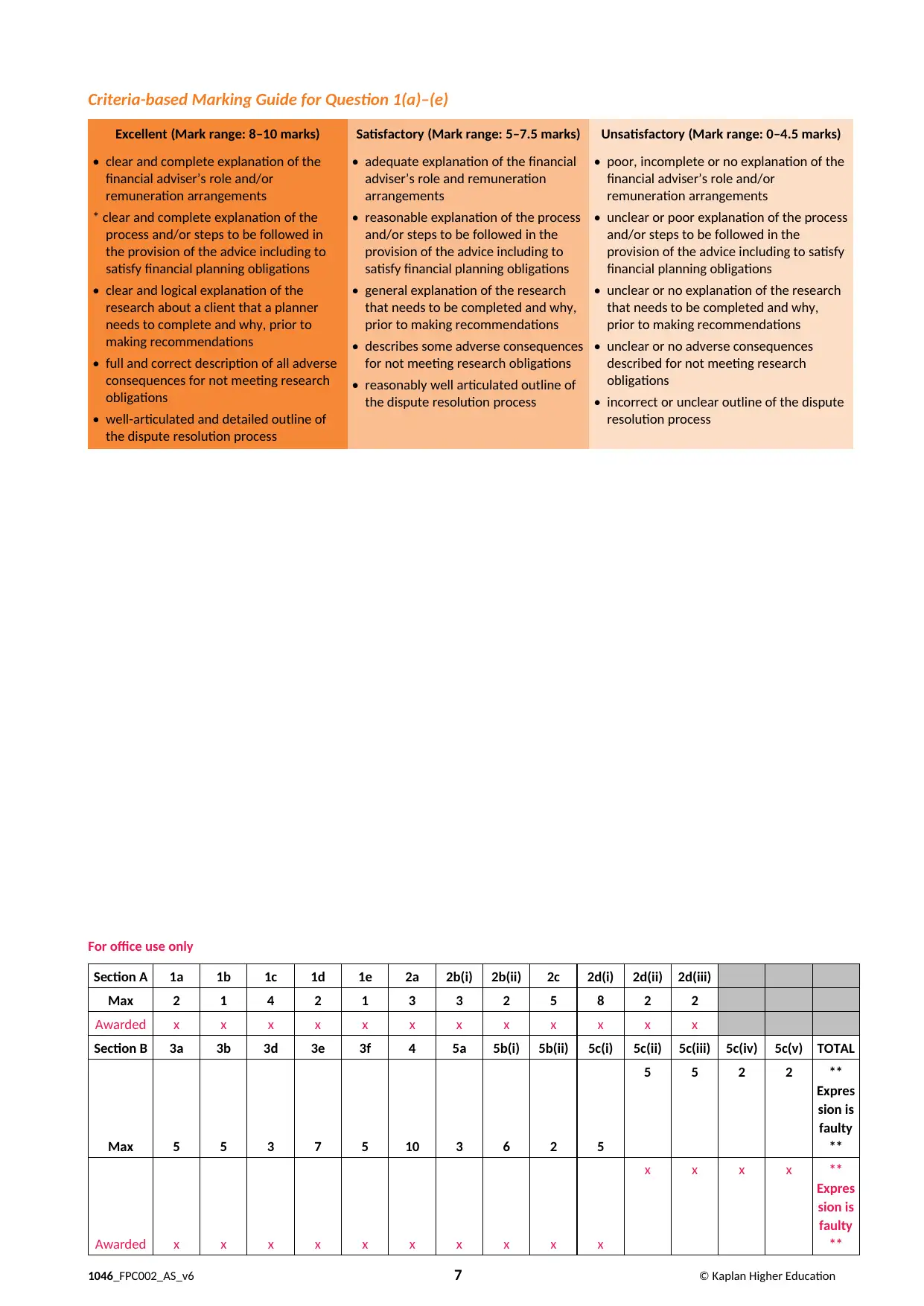

Criteria-based Marking Guide for Question 1(a)–(e)

Excellent (Mark range: 8–10 marks) Satisfactory (Mark range: 5–7.5 marks) Unsatisfactory (Mark range: 0–4.5 marks)

• clear and complete explanation of the

financial adviser’s role and/or

remuneration arrangements

* clear and complete explanation of the

process and/or steps to be followed in

the provision of the advice including to

satisfy financial planning obligations

• clear and logical explanation of the

research about a client that a planner

needs to complete and why, prior to

making recommendations

• full and correct description of all adverse

consequences for not meeting research

obligations

• well-articulated and detailed outline of

the dispute resolution process

• adequate explanation of the financial

adviser’s role and remuneration

arrangements

• reasonable explanation of the process

and/or steps to be followed in the

provision of the advice including to

satisfy financial planning obligations

• general explanation of the research

that needs to be completed and why,

prior to making recommendations

• describes some adverse consequences

for not meeting research obligations

• reasonably well articulated outline of

the dispute resolution process

• poor, incomplete or no explanation of the

financial adviser’s role and/or

remuneration arrangements

• unclear or poor explanation of the process

and/or steps to be followed in the

provision of the advice including to satisfy

financial planning obligations

• unclear or no explanation of the research

that needs to be completed and why,

prior to making recommendations

• unclear or no adverse consequences

described for not meeting research

obligations

• incorrect or unclear outline of the dispute

resolution process

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 7 © Kaplan Higher Education

Excellent (Mark range: 8–10 marks) Satisfactory (Mark range: 5–7.5 marks) Unsatisfactory (Mark range: 0–4.5 marks)

• clear and complete explanation of the

financial adviser’s role and/or

remuneration arrangements

* clear and complete explanation of the

process and/or steps to be followed in

the provision of the advice including to

satisfy financial planning obligations

• clear and logical explanation of the

research about a client that a planner

needs to complete and why, prior to

making recommendations

• full and correct description of all adverse

consequences for not meeting research

obligations

• well-articulated and detailed outline of

the dispute resolution process

• adequate explanation of the financial

adviser’s role and remuneration

arrangements

• reasonable explanation of the process

and/or steps to be followed in the

provision of the advice including to

satisfy financial planning obligations

• general explanation of the research

that needs to be completed and why,

prior to making recommendations

• describes some adverse consequences

for not meeting research obligations

• reasonably well articulated outline of

the dispute resolution process

• poor, incomplete or no explanation of the

financial adviser’s role and/or

remuneration arrangements

• unclear or poor explanation of the process

and/or steps to be followed in the

provision of the advice including to satisfy

financial planning obligations

• unclear or no explanation of the research

that needs to be completed and why,

prior to making recommendations

• unclear or no adverse consequences

described for not meeting research

obligations

• incorrect or unclear outline of the dispute

resolution process

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 7 © Kaplan Higher Education

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Insert your answers to Question 1(a)–(e) below this line

a) A financial advisors’ role is to develop investment strategies which will include both strategic and

product solutions to help clients meet their financial goals and objectives. An advisor must follow best

interest duty to ensure that the clients are placed in the better financial position. Examples of services

are as follow:

Better manage income and expenditure to meet future developments

Minimise debt

Provide protection against loss or damage through using insurance

Minimise tax within the permissible legal framework

Invest a windfall such as inheritance

b) Remuneration for Financial advisers are as follow:

Trailing commission as a result of FOFA reforms:

o Trailing commissions can no longer be paid on new investment products but

existing arrangements as at 1 July 2013 were unaffected. Trailing commissions

need to be disclosed to existing clients annually through an FDS

o Insurance products were originally excluded but will now be included as a result of

the life insurance reform regime. From 1 January 2018, initial commissions will be

capped at 60% and ongoing commissions at 20%. This will be phased in over a

three-year period. In addition, there will be a two-year upfront commission

‘clawback’ with 100% clawback in year one and 60% clawback if a policy lapses in

year two.

Fee-for-advice/service: As a result of FOFA, the method for charging new clients is a fee-for-

advice/service arrangement. Financial advisers can charge:

o For work undertaken according to a cost schedule (e.g. prepare a written SOA for

$1,500)

o For work on an hourly rate

o A rate based on total assets under advice, usually as a percentage of the assets,

providing an agreed level of service.

c) The steps areas follow:

Collect and assess client’s financial data & other relevant info

This is to better understand the clients’ current financial situation by using a data-gathering

tool, known as the fact find or the needs analysis questionnaires which represents of all

relevant questions and issues which need to be discussed with the client.

Determine the client’s objectives & goals

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 8 © Kaplan Higher Education

a) A financial advisors’ role is to develop investment strategies which will include both strategic and

product solutions to help clients meet their financial goals and objectives. An advisor must follow best

interest duty to ensure that the clients are placed in the better financial position. Examples of services

are as follow:

Better manage income and expenditure to meet future developments

Minimise debt

Provide protection against loss or damage through using insurance

Minimise tax within the permissible legal framework

Invest a windfall such as inheritance

b) Remuneration for Financial advisers are as follow:

Trailing commission as a result of FOFA reforms:

o Trailing commissions can no longer be paid on new investment products but

existing arrangements as at 1 July 2013 were unaffected. Trailing commissions

need to be disclosed to existing clients annually through an FDS

o Insurance products were originally excluded but will now be included as a result of

the life insurance reform regime. From 1 January 2018, initial commissions will be

capped at 60% and ongoing commissions at 20%. This will be phased in over a

three-year period. In addition, there will be a two-year upfront commission

‘clawback’ with 100% clawback in year one and 60% clawback if a policy lapses in

year two.

Fee-for-advice/service: As a result of FOFA, the method for charging new clients is a fee-for-

advice/service arrangement. Financial advisers can charge:

o For work undertaken according to a cost schedule (e.g. prepare a written SOA for

$1,500)

o For work on an hourly rate

o A rate based on total assets under advice, usually as a percentage of the assets,

providing an agreed level of service.

c) The steps areas follow:

Collect and assess client’s financial data & other relevant info

This is to better understand the clients’ current financial situation by using a data-gathering

tool, known as the fact find or the needs analysis questionnaires which represents of all

relevant questions and issues which need to be discussed with the client.

Determine the client’s objectives & goals

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 8 © Kaplan Higher Education

This provides crucial information as to the reason why the clients seek advice and their

financial aspirations. Failing to determine goals and objectives may lead to the adviser

making recommendations that do not align with the clients’ expectations.

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 9 © Kaplan Higher Education

financial aspirations. Failing to determine goals and objectives may lead to the adviser

making recommendations that do not align with the clients’ expectations.

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 9 © Kaplan Higher Education

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Identify any financial problems that may exist

This is about analysing all information collected and then conducting a gap analysis

between where the client is, what they want to achieve and what they will realistically be

able to achieve. An important element of this step is ensuring that the client understands

all associated risks of making changes to their financial activities.

Prepare a written plan that contains alternatives and recommendations

Preparation of SOA which outlines the advice to the client as well as any other information

the client needs in order to make informed decisions about the. SOA must be a clear and

succinct document which complies with all compulsory elements pertaining to the advice,

including scope of advice, current position, goals and objectives, issues identified,

disclosures and recommended trade-offs, strategies and solutions; and it must meet all

best interests duty obligations. It should outline the risks and benefits of the advice, the

advantages and disadvantages of the advice and alternative strategies that have been

considered and rejected in favour of the advice provided.

Present recommendations and implement plan

An SOA is presented to the client at a meeting where the adviser explains the reasoning

behind their recommendations and what the expected outcomes will be if the advice is

implemented. It is the adviser’s responsibility to ensure that the client understands both

the pros and cons of their recommendations, and to obtain agreement to proceed with

implementation of the plan by having the client sign an authority to proceed, noting any

changes or variations to the SOA that the client may request (e.g. requesting a lower life

insurance amount).

Review plan

Client needs and circumstances are not static and will inevitably change over time. Periodic

reviews of a financial plan, once it has been implemented, ensure that the plan is adapted

or modified if required in response to changing needs and circumstances.

d) Clients may be placed in a difficult financial situation, and if ASIC finds an adviser is guilty of

misconduct they can be banned from providing financial advice, either for a period of time or for

life depending on the seriousness of the actions.

e) Clients should try to talk it over with the adviser, if that does not work, clients can make a

complaint via adviser’s internal dispute resolution system (this can be found within FSG). They must

provide a response to clients within 45 days. Should the clients still unhappy with the response,

they can contact the external dispute resolution (The business must tell you which scheme it

belongs to).

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 10 © Kaplan Higher Education

This is about analysing all information collected and then conducting a gap analysis

between where the client is, what they want to achieve and what they will realistically be

able to achieve. An important element of this step is ensuring that the client understands

all associated risks of making changes to their financial activities.

Prepare a written plan that contains alternatives and recommendations

Preparation of SOA which outlines the advice to the client as well as any other information

the client needs in order to make informed decisions about the. SOA must be a clear and

succinct document which complies with all compulsory elements pertaining to the advice,

including scope of advice, current position, goals and objectives, issues identified,

disclosures and recommended trade-offs, strategies and solutions; and it must meet all

best interests duty obligations. It should outline the risks and benefits of the advice, the

advantages and disadvantages of the advice and alternative strategies that have been

considered and rejected in favour of the advice provided.

Present recommendations and implement plan

An SOA is presented to the client at a meeting where the adviser explains the reasoning

behind their recommendations and what the expected outcomes will be if the advice is

implemented. It is the adviser’s responsibility to ensure that the client understands both

the pros and cons of their recommendations, and to obtain agreement to proceed with

implementation of the plan by having the client sign an authority to proceed, noting any

changes or variations to the SOA that the client may request (e.g. requesting a lower life

insurance amount).

Review plan

Client needs and circumstances are not static and will inevitably change over time. Periodic

reviews of a financial plan, once it has been implemented, ensure that the plan is adapted

or modified if required in response to changing needs and circumstances.

d) Clients may be placed in a difficult financial situation, and if ASIC finds an adviser is guilty of

misconduct they can be banned from providing financial advice, either for a period of time or for

life depending on the seriousness of the actions.

e) Clients should try to talk it over with the adviser, if that does not work, clients can make a

complaint via adviser’s internal dispute resolution system (this can be found within FSG). They must

provide a response to clients within 45 days. Should the clients still unhappy with the response,

they can contact the external dispute resolution (The business must tell you which scheme it

belongs to).

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 10 © Kaplan Higher Education

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Words: 810

End of answers to Question 1(a)–(e)

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 11 © Kaplan Higher Education

End of answers to Question 1(a)–(e)

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 11 © Kaplan Higher Education

Question 2 (25 marks | Word limit: 1,200 words)

LO1: Apply techniques to establish and develop client relationships.

LO4: Conduct appropriate quantitative and qualitative research as part of the financial planning process.

LO5: Assess clients’ goals and financial position to form the basis of advice.

Refer to Appendix B to answer the following questions. It provides a snapshot of the data that you have

collected at your first meeting with Simon and Nadia and contains necessary information about their

circumstances.

Note: You will need to determine Simon and Nadia’s individual risk profiles, based on their responses to the

risk profile questions and resulting scores to answer questions 2(b) and (c) below.

(a) Briefly describe both positive and negative criticisms regarding the qualitative and quantitative data

collected. (3 marks)

(b) You begin to conduct some risk profiling within the client needs analysis. Simon immediately

becomes defensive, saying to you: ‘I’ve undertaken my own risk profiling before coming in to see

you, and I’m comfortable and satisfied that I’m a high growth investor — weren’t you listening?’

As their adviser, what would you say in response to his comments? Your answer must be written as a

direct verbal response to Simon, and must:

(i) include demonstrations/examples of active listening and ‘non-verbal’ skills you would employ

while listening to and then responding to him (3 marks)

(ii) include open and closed questions in your response. (2 marks)

(c) What concerns would you raise with Nadia regarding her risk profile? Base your explanation on her

objectives, current asset class allocation and information in the case study, including her stated

investor risk type, and the investor risk type you think she is. (5 marks)

(d) (i) Create detailed net worth and cash flow statements for Simon and Nadia. (Refer Topic 9

activity.) Note: You do not need to create separate statements for the Johnson Family Trust.

(8 marks)

(ii) Calculate the following financial ratios for Simon and Nadia:

• net worth ratio (total net worth/total assets)

• liquidity ratio (liquid assets/current debts)

• savings (savings/net income)

• monthly debt service (monthly debt commitments/monthly net income).

Note: Show all workings. (2 marks)

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 12 © Kaplan Higher Education

LO1: Apply techniques to establish and develop client relationships.

LO4: Conduct appropriate quantitative and qualitative research as part of the financial planning process.

LO5: Assess clients’ goals and financial position to form the basis of advice.

Refer to Appendix B to answer the following questions. It provides a snapshot of the data that you have

collected at your first meeting with Simon and Nadia and contains necessary information about their

circumstances.

Note: You will need to determine Simon and Nadia’s individual risk profiles, based on their responses to the

risk profile questions and resulting scores to answer questions 2(b) and (c) below.

(a) Briefly describe both positive and negative criticisms regarding the qualitative and quantitative data

collected. (3 marks)

(b) You begin to conduct some risk profiling within the client needs analysis. Simon immediately

becomes defensive, saying to you: ‘I’ve undertaken my own risk profiling before coming in to see

you, and I’m comfortable and satisfied that I’m a high growth investor — weren’t you listening?’

As their adviser, what would you say in response to his comments? Your answer must be written as a

direct verbal response to Simon, and must:

(i) include demonstrations/examples of active listening and ‘non-verbal’ skills you would employ

while listening to and then responding to him (3 marks)

(ii) include open and closed questions in your response. (2 marks)

(c) What concerns would you raise with Nadia regarding her risk profile? Base your explanation on her

objectives, current asset class allocation and information in the case study, including her stated

investor risk type, and the investor risk type you think she is. (5 marks)

(d) (i) Create detailed net worth and cash flow statements for Simon and Nadia. (Refer Topic 9

activity.) Note: You do not need to create separate statements for the Johnson Family Trust.

(8 marks)

(ii) Calculate the following financial ratios for Simon and Nadia:

• net worth ratio (total net worth/total assets)

• liquidity ratio (liquid assets/current debts)

• savings (savings/net income)

• monthly debt service (monthly debt commitments/monthly net income).

Note: Show all workings. (2 marks)

For office use only

Section A 1a 1b 1c 1d 1e 2a 2b(i) 2b(ii) 2c 2d(i) 2d(ii) 2d(iii)

Max 2 1 4 2 1 3 3 2 5 8 2 2

Awarded x x x x x x x x x x x x

Section B 3a 3b 3d 3e 3f 4 5a 5b(i) 5b(ii) 5c(i) 5c(ii) 5c(iii) 5c(iv) 5c(v) TOTAL

Max 5 5 3 7 5 10 3 6 2 5

5 5 2 2 **

Expres

sion is

faulty

**

Awarded x x x x x x x x x x

x x x x **

Expres

sion is

faulty

**

1046_FPC002_AS_v6 12 © Kaplan Higher Education

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 44

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.