Comprehensive Analysis of the French Taxation System: A Report

VerifiedAdded on 2021/11/13

|11

|2142

|65

Report

AI Summary

This report provides a comprehensive overview of the French taxation system, focusing on income tax for individuals, unincorporated businesses, gift tax, and estate tax. It details income tax rates, the impact of residency, and the tax liability of employees earning a specific gross salary. The report explores gift tax exemptions, estate tax implications, and the filing procedures for families. It also covers deductions, employer tax withholding, FICA, VAT, and the criteria for filing tax returns. The analysis includes a calculation of income tax liability for an employee earning €60,000 annually, illustrating the application of tax rates across different income brackets. The report concludes by emphasizing the importance of residential status in determining tax obligations, differentiating between French residents and non-residents regarding worldwide income taxation.

Running head: TAXATION

Taxation

Name of the Student:

Name of the University:

Authors Note:

Taxation

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION

Contents

Introduction:....................................................................................................................................2

Income taxes for individuals in France:...........................................................................................2

Income tax liability of unincorporated business in the country:......................................................4

Gift tax and who pays gift tax:........................................................................................................4

Liability to pay gift tax in the country:............................................................................................4

Estate tax:.........................................................................................................................................4

Families file together or taxpayer taxed separately:........................................................................5

Dependants for computation of tax:................................................................................................5

Individuals and deductions:.............................................................................................................5

Are taxes withheld by employers?...................................................................................................5

FICA:...............................................................................................................................................5

Does everyone have to file tax returns in the country?...................................................................5

VAT or sales tax:.............................................................................................................................6

Tax liability:.....................................................................................................................................6

Summary:.........................................................................................................................................9

References:....................................................................................................................................10

TAXATION

Contents

Introduction:....................................................................................................................................2

Income taxes for individuals in France:...........................................................................................2

Income tax liability of unincorporated business in the country:......................................................4

Gift tax and who pays gift tax:........................................................................................................4

Liability to pay gift tax in the country:............................................................................................4

Estate tax:.........................................................................................................................................4

Families file together or taxpayer taxed separately:........................................................................5

Dependants for computation of tax:................................................................................................5

Individuals and deductions:.............................................................................................................5

Are taxes withheld by employers?...................................................................................................5

FICA:...............................................................................................................................................5

Does everyone have to file tax returns in the country?...................................................................5

VAT or sales tax:.............................................................................................................................6

Tax liability:.....................................................................................................................................6

Summary:.........................................................................................................................................9

References:....................................................................................................................................10

2

TAXATION

Introduction:

For Government of any country income tax is one of the primary sources to generate

revenue required for expenditures necessary to provide different services to general public of the

country including development of infrastructure and economic progress of poor and social

backward people in the country. It is important to have necessary information about income tax

structure of a country before accepting an employment or any other opportunity to settle in the

country. In this document a detailed discussion shall be made about the income tax structure in

France assuming that an individual has got an offer of employment from the country.

Income taxes for individuals in France:

The parliament determines taxation in France in the Annual budget. Thus, the parliamentarians

have the responsibility in each year to pass appropriate taxation rules to govern the provisions

related to taxation ion the country (Hoynes, Miller and Simon, 2015).

The liability to pay taxes in France is dependent on the residential status of an individual. A

resident of France is liable to pay tax on all of his income including the income earned in outside

the country. Thus, a French is liable for his worldwide income in France and required to file

French tax return (Piketty, 2015).

The personal taxes in the country can be primarily categorized into three categories, these are;

income tax in the country also known as French income tax, social security contributions, and

tax on goods and services in the country. A person who has come to the country for the purpose

of employment and is in receive of salary in the country will be liable to pay tax on such salary

income even if the person is not a French resident for income tax purpose (Blanchet, Fournier

TAXATION

Introduction:

For Government of any country income tax is one of the primary sources to generate

revenue required for expenditures necessary to provide different services to general public of the

country including development of infrastructure and economic progress of poor and social

backward people in the country. It is important to have necessary information about income tax

structure of a country before accepting an employment or any other opportunity to settle in the

country. In this document a detailed discussion shall be made about the income tax structure in

France assuming that an individual has got an offer of employment from the country.

Income taxes for individuals in France:

The parliament determines taxation in France in the Annual budget. Thus, the parliamentarians

have the responsibility in each year to pass appropriate taxation rules to govern the provisions

related to taxation ion the country (Hoynes, Miller and Simon, 2015).

The liability to pay taxes in France is dependent on the residential status of an individual. A

resident of France is liable to pay tax on all of his income including the income earned in outside

the country. Thus, a French is liable for his worldwide income in France and required to file

French tax return (Piketty, 2015).

The personal taxes in the country can be primarily categorized into three categories, these are;

income tax in the country also known as French income tax, social security contributions, and

tax on goods and services in the country. A person who has come to the country for the purpose

of employment and is in receive of salary in the country will be liable to pay tax on such salary

income even if the person is not a French resident for income tax purpose (Blanchet, Fournier

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION

and Piketty, 2017). As per the Parliament budget the following persons are liable to pay taxes in

the country;

I. A person who has his or her main place of residence in the country.

II. A person who has stayed in the country for 183 days or more in a calendar year.

III. The main occupation of the person is in the country.

IV. A person’s most substantial assets are in the country.

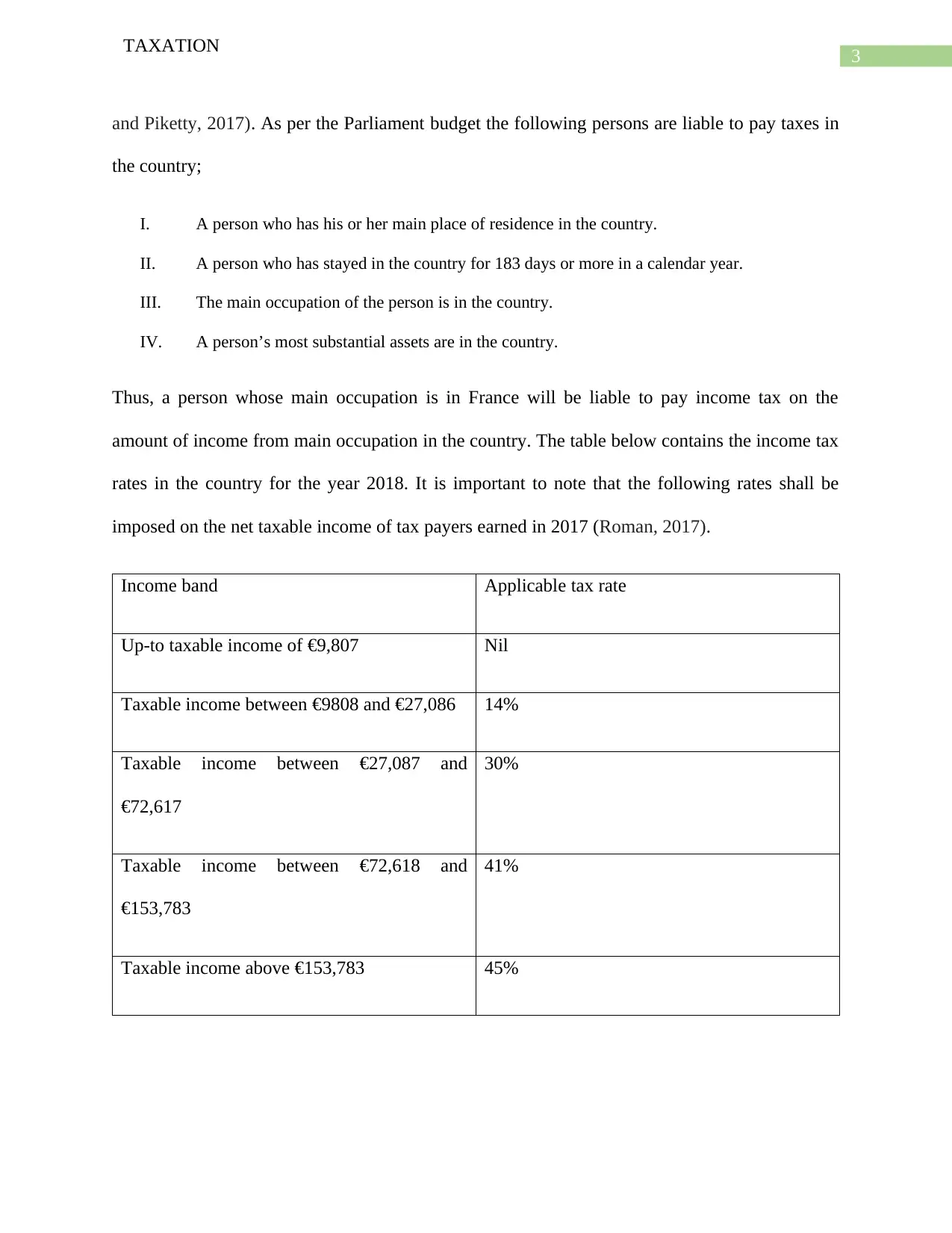

Thus, a person whose main occupation is in France will be liable to pay income tax on the

amount of income from main occupation in the country. The table below contains the income tax

rates in the country for the year 2018. It is important to note that the following rates shall be

imposed on the net taxable income of tax payers earned in 2017 (Roman, 2017).

Income band Applicable tax rate

Up-to taxable income of €9,807 Nil

Taxable income between €9808 and €27,086 14%

Taxable income between €27,087 and

€72,617

30%

Taxable income between €72,618 and

€153,783

41%

Taxable income above €153,783 45%

TAXATION

and Piketty, 2017). As per the Parliament budget the following persons are liable to pay taxes in

the country;

I. A person who has his or her main place of residence in the country.

II. A person who has stayed in the country for 183 days or more in a calendar year.

III. The main occupation of the person is in the country.

IV. A person’s most substantial assets are in the country.

Thus, a person whose main occupation is in France will be liable to pay income tax on the

amount of income from main occupation in the country. The table below contains the income tax

rates in the country for the year 2018. It is important to note that the following rates shall be

imposed on the net taxable income of tax payers earned in 2017 (Roman, 2017).

Income band Applicable tax rate

Up-to taxable income of €9,807 Nil

Taxable income between €9808 and €27,086 14%

Taxable income between €27,087 and

€72,617

30%

Taxable income between €72,618 and

€153,783

41%

Taxable income above €153,783 45%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION

Income tax liability of unincorporated business in the country:

There are mainly three types of business structures in the country. It is not essential to establish a

company to start and operate business in the country. The sole proprietor is liable to pay tax on

the amount of profit earned from business if the profit from such business along with other

taxable income of the sole proprietor is above the statutory limit of exempt income, i.e. €9,807.

Thus, earnings from sole proprietorship business is taxed before it flows through to the

individual (Evers, Miller and Spengel, 2015).

Gift tax and who pays gift tax:

Gifts are taxed in the country with certain exemptions up-to specified amounts to spouse,

children and grandchildren. Thus except in the cases where the gifts are made to spouse, child

and grandchild up to statutory limits all other gifts in the country are taxed. For Spouse an

amount of €76,000 in every ten years can be gifted without any tax on such gift. The statutory

limits reduce for child to €76,000 and to grandchild to €30,000 in every ten years (Markle,

2016).

Liability to pay gift tax in the country:

The liability to pay gift tax is dependent on the tax residential status of the donor and the donee

along with the gift’s location and nature of the gift. In case the donor is a tax resident of France

then the liability of gifts tax is on the shoulder of the donor. In case the donor is non-resident

then the liability arise to done provided the done has been a tax resident in the country for a

minimum of 6 years out of last 10 years (Lefebvre et. al. 2015).

Estate tax:

Yes, estates are taxed in the country. Known as inheritance tax a 40% tax is imposed on estates.

TAXATION

Income tax liability of unincorporated business in the country:

There are mainly three types of business structures in the country. It is not essential to establish a

company to start and operate business in the country. The sole proprietor is liable to pay tax on

the amount of profit earned from business if the profit from such business along with other

taxable income of the sole proprietor is above the statutory limit of exempt income, i.e. €9,807.

Thus, earnings from sole proprietorship business is taxed before it flows through to the

individual (Evers, Miller and Spengel, 2015).

Gift tax and who pays gift tax:

Gifts are taxed in the country with certain exemptions up-to specified amounts to spouse,

children and grandchildren. Thus except in the cases where the gifts are made to spouse, child

and grandchild up to statutory limits all other gifts in the country are taxed. For Spouse an

amount of €76,000 in every ten years can be gifted without any tax on such gift. The statutory

limits reduce for child to €76,000 and to grandchild to €30,000 in every ten years (Markle,

2016).

Liability to pay gift tax in the country:

The liability to pay gift tax is dependent on the tax residential status of the donor and the donee

along with the gift’s location and nature of the gift. In case the donor is a tax resident of France

then the liability of gifts tax is on the shoulder of the donor. In case the donor is non-resident

then the liability arise to done provided the done has been a tax resident in the country for a

minimum of 6 years out of last 10 years (Lefebvre et. al. 2015).

Estate tax:

Yes, estates are taxed in the country. Known as inheritance tax a 40% tax is imposed on estates.

5

TAXATION

Families file together or taxpayer taxed separately:

The income tax provisions in the country allows families to file income tax return together. Thus,

family members can jointly file income tax return in France.

Dependants for computation of tax:

Dependents are considered while computing income taxes of individuals in the country as the

allowances and deductions are available for the number of dependants.

Individuals and deductions:

Different types of deductions are allowed to individuals including house allowances, medical

allowances, education allowance and other such allowances to compute income tax liabilities of

an individual. (Benzarti and Carloni, 2017).

Are taxes withheld by employers?

Employers are liable to withheld tax on the gross amount of salary payable to the employees.

The employers must deduct such tax and deposit such taxes to the credit of the Government

(Benzarti and Carloni, 2016).

FICA:

Investors ain France are liable to pay FICA thus, yes investors are under obligation to pay

income FICA tax in the country.

Does everyone have to file tax returns in the country?

No, not everyone is required to file income tax returns in the country. Only the individuals who

have income liable to be taxed in the country is liable to file income tax return in the country.

Taxes on worldwide income or not:

TAXATION

Families file together or taxpayer taxed separately:

The income tax provisions in the country allows families to file income tax return together. Thus,

family members can jointly file income tax return in France.

Dependants for computation of tax:

Dependents are considered while computing income taxes of individuals in the country as the

allowances and deductions are available for the number of dependants.

Individuals and deductions:

Different types of deductions are allowed to individuals including house allowances, medical

allowances, education allowance and other such allowances to compute income tax liabilities of

an individual. (Benzarti and Carloni, 2017).

Are taxes withheld by employers?

Employers are liable to withheld tax on the gross amount of salary payable to the employees.

The employers must deduct such tax and deposit such taxes to the credit of the Government

(Benzarti and Carloni, 2016).

FICA:

Investors ain France are liable to pay FICA thus, yes investors are under obligation to pay

income FICA tax in the country.

Does everyone have to file tax returns in the country?

No, not everyone is required to file income tax returns in the country. Only the individuals who

have income liable to be taxed in the country is liable to file income tax return in the country.

Taxes on worldwide income or not:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION

Taxes on world-wide income French residents are subjected to income tax in the country

whereas non-resident individuals are only subjected to the income accruing in the country.

VAT or sales tax:

VAT is applicable in France and the eligible persons are liable to pay VAT at the rate of 20%.

The statutory exemption limit for VAT is €175.01.

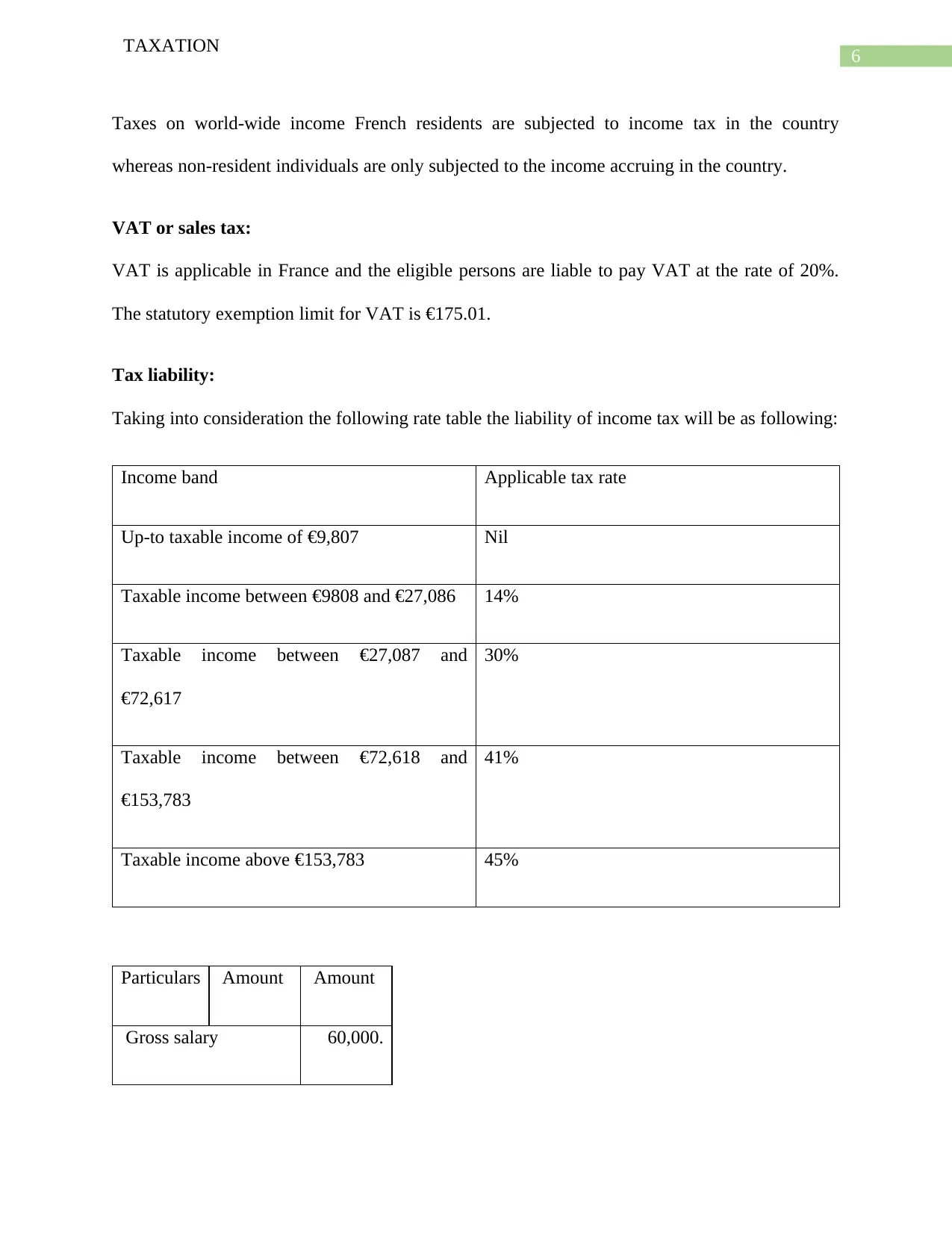

Tax liability:

Taking into consideration the following rate table the liability of income tax will be as following:

Income band Applicable tax rate

Up-to taxable income of €9,807 Nil

Taxable income between €9808 and €27,086 14%

Taxable income between €27,087 and

€72,617

30%

Taxable income between €72,618 and

€153,783

41%

Taxable income above €153,783 45%

Particulars Amount Amount

Gross salary 60,000.

TAXATION

Taxes on world-wide income French residents are subjected to income tax in the country

whereas non-resident individuals are only subjected to the income accruing in the country.

VAT or sales tax:

VAT is applicable in France and the eligible persons are liable to pay VAT at the rate of 20%.

The statutory exemption limit for VAT is €175.01.

Tax liability:

Taking into consideration the following rate table the liability of income tax will be as following:

Income band Applicable tax rate

Up-to taxable income of €9,807 Nil

Taxable income between €9808 and €27,086 14%

Taxable income between €27,087 and

€72,617

30%

Taxable income between €72,618 and

€153,783

41%

Taxable income above €153,783 45%

Particulars Amount Amount

Gross salary 60,000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION

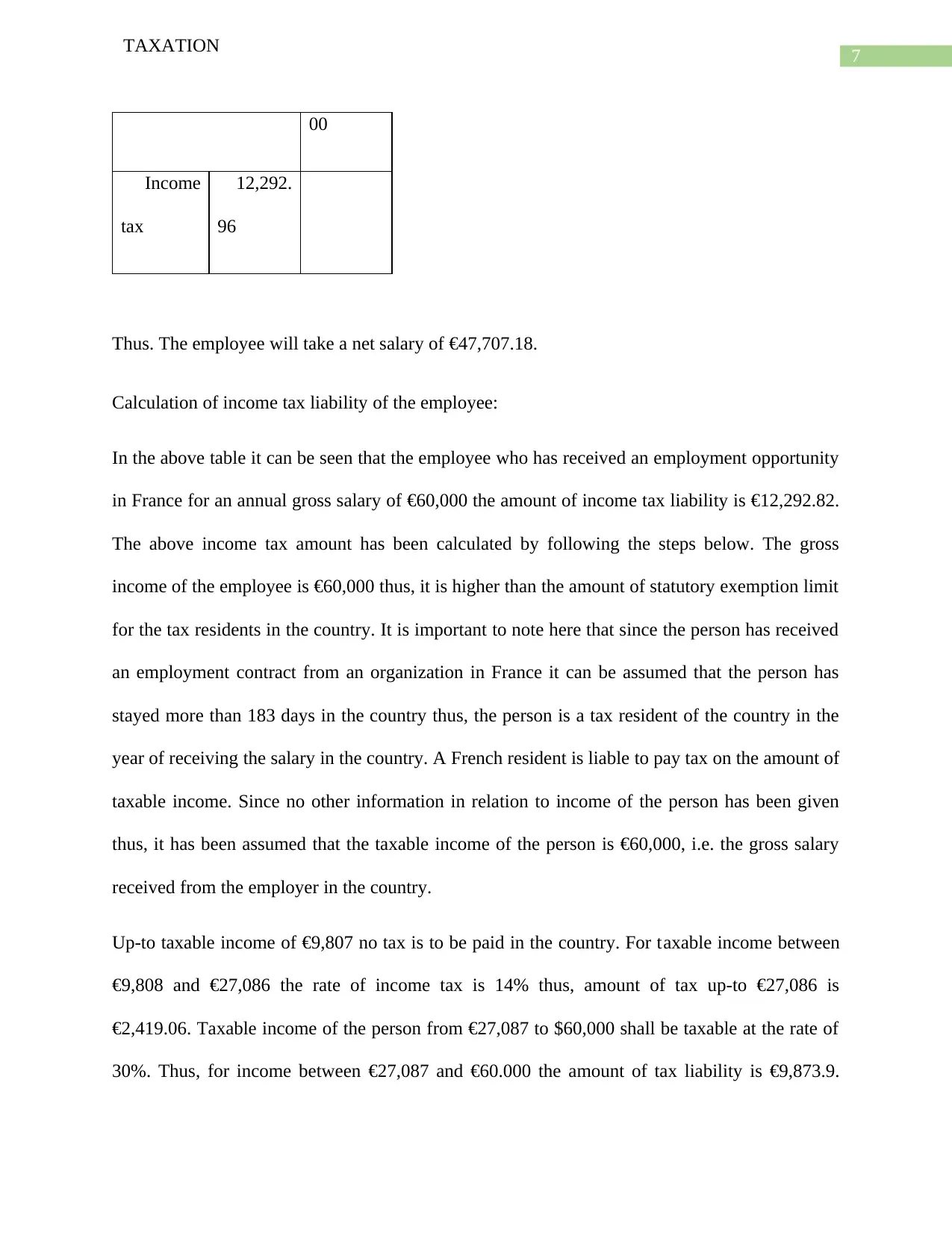

00

Income

tax

12,292.

96

Thus. The employee will take a net salary of €47,707.18.

Calculation of income tax liability of the employee:

In the above table it can be seen that the employee who has received an employment opportunity

in France for an annual gross salary of €60,000 the amount of income tax liability is €12,292.82.

The above income tax amount has been calculated by following the steps below. The gross

income of the employee is €60,000 thus, it is higher than the amount of statutory exemption limit

for the tax residents in the country. It is important to note here that since the person has received

an employment contract from an organization in France it can be assumed that the person has

stayed more than 183 days in the country thus, the person is a tax resident of the country in the

year of receiving the salary in the country. A French resident is liable to pay tax on the amount of

taxable income. Since no other information in relation to income of the person has been given

thus, it has been assumed that the taxable income of the person is €60,000, i.e. the gross salary

received from the employer in the country.

Up-to taxable income of €9,807 no tax is to be paid in the country. For taxable income between

€9,808 and €27,086 the rate of income tax is 14% thus, amount of tax up-to €27,086 is

€2,419.06. Taxable income of the person from €27,087 to $60,000 shall be taxable at the rate of

30%. Thus, for income between €27,087 and €60.000 the amount of tax liability is €9,873.9.

TAXATION

00

Income

tax

12,292.

96

Thus. The employee will take a net salary of €47,707.18.

Calculation of income tax liability of the employee:

In the above table it can be seen that the employee who has received an employment opportunity

in France for an annual gross salary of €60,000 the amount of income tax liability is €12,292.82.

The above income tax amount has been calculated by following the steps below. The gross

income of the employee is €60,000 thus, it is higher than the amount of statutory exemption limit

for the tax residents in the country. It is important to note here that since the person has received

an employment contract from an organization in France it can be assumed that the person has

stayed more than 183 days in the country thus, the person is a tax resident of the country in the

year of receiving the salary in the country. A French resident is liable to pay tax on the amount of

taxable income. Since no other information in relation to income of the person has been given

thus, it has been assumed that the taxable income of the person is €60,000, i.e. the gross salary

received from the employer in the country.

Up-to taxable income of €9,807 no tax is to be paid in the country. For taxable income between

€9,808 and €27,086 the rate of income tax is 14% thus, amount of tax up-to €27,086 is

€2,419.06. Taxable income of the person from €27,087 to $60,000 shall be taxable at the rate of

30%. Thus, for income between €27,087 and €60.000 the amount of tax liability is €9,873.9.

8

TAXATION

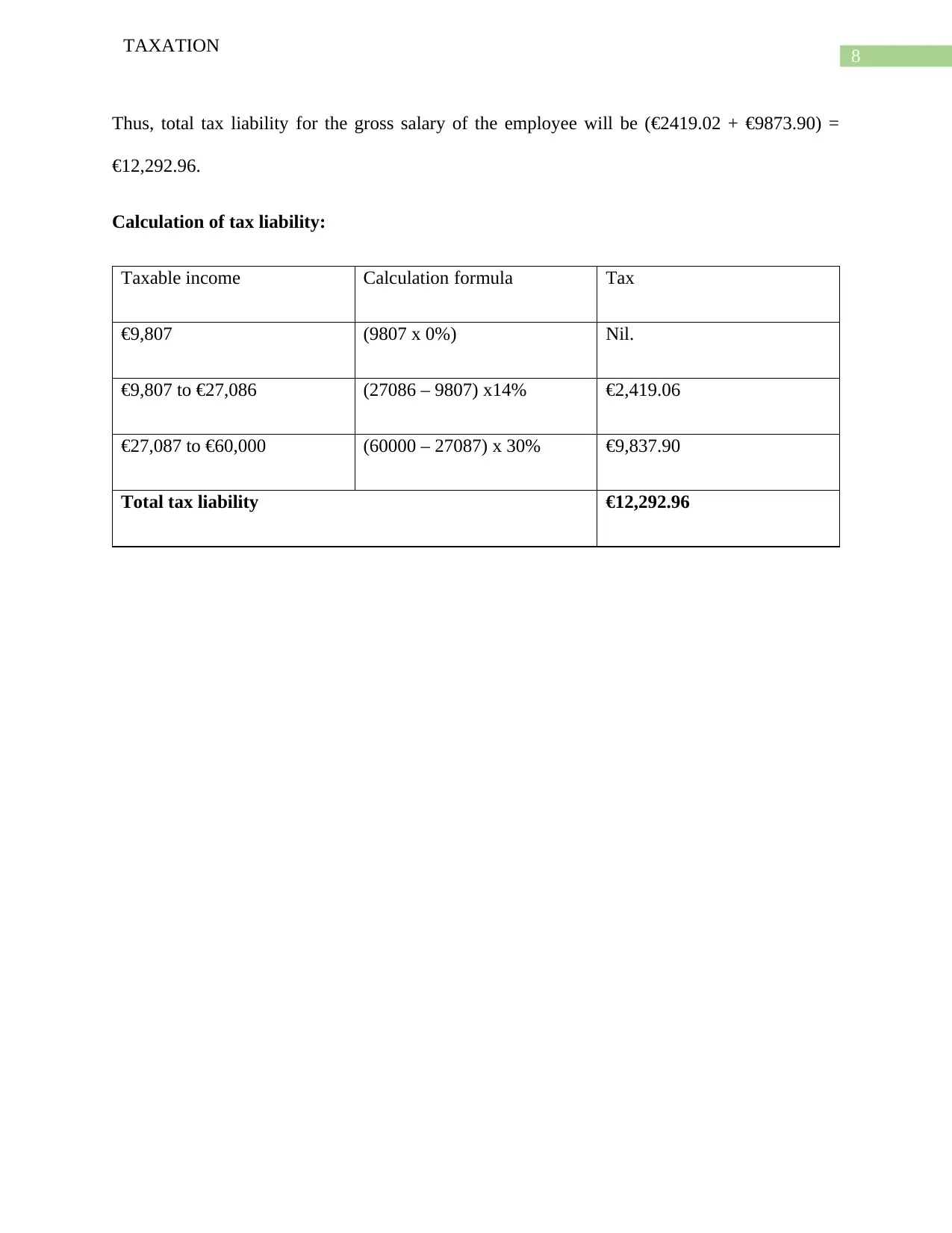

Thus, total tax liability for the gross salary of the employee will be (€2419.02 + €9873.90) =

€12,292.96.

Calculation of tax liability:

Taxable income Calculation formula Tax

€9,807 (9807 x 0%) Nil.

€9,807 to €27,086 (27086 – 9807) x14% €2,419.06

€27,087 to €60,000 (60000 – 27087) x 30% €9,837.90

Total tax liability €12,292.96

TAXATION

Thus, total tax liability for the gross salary of the employee will be (€2419.02 + €9873.90) =

€12,292.96.

Calculation of tax liability:

Taxable income Calculation formula Tax

€9,807 (9807 x 0%) Nil.

€9,807 to €27,086 (27086 – 9807) x14% €2,419.06

€27,087 to €60,000 (60000 – 27087) x 30% €9,837.90

Total tax liability €12,292.96

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION

Summary:

Taking into consideration the discussion about the Income tax and other personal taxes

applicable to the tax payers in the country, it is clear that the residential status of an individual is

key determinant to the amount of income tax liability of such individual. Thus, primary

consideration is to be given to the residential status of an individual as a French resident is

responsible to pay taxes on worldwide income of his whereas a non-resident individual in France

is only liable to pay tax accruing or receiving or both in the country.

TAXATION

Summary:

Taking into consideration the discussion about the Income tax and other personal taxes

applicable to the tax payers in the country, it is clear that the residential status of an individual is

key determinant to the amount of income tax liability of such individual. Thus, primary

consideration is to be given to the residential status of an individual as a French resident is

responsible to pay taxes on worldwide income of his whereas a non-resident individual in France

is only liable to pay tax accruing or receiving or both in the country.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION

References:

Benzarti, Y. and Carloni, D., 2017. Who Really Benefits from Consumption Tax Cuts? Evidence

from a Large VAT Reform in France (No. w23848). National Bureau of Economic Research, pp.

7-21.

Benzarti, Y. and Carloni, D., 2016. Who Really Benefits From Consumption Tax Cuts? Evidence

From a Large VAT Cut in France. Working Paper, 11(1), pp.117-132.

Blanchet, T., Fournier, J. and Piketty, T., 2017. Generalized Pareto curves: Theory and

applications to income and wealth tax data for France and the United States, 1800-2014. WID.

world WorkingPaper, (2017/3).

Evers, L., Miller, H. and Spengel, C., 2015. Intellectual property box regimes: effective tax rates

and tax policy considerations. International Tax and Public Finance, 22(3), pp.502-530.

Hoynes, H., Miller, D. and Simon, D., 2015. Income, the earned income tax credit, and infant

health. American Economic Journal: Economic Policy, 7(1), pp.172-211.

Lefebvre, M., Pestieau, P., Riedl, A. and Villeval, M.C., 2015. Tax evasion and social

information: an experiment in Belgium, France, and the Netherlands. International Tax and

Public Finance, 22(3), pp.401-425.

Markle, K., 2016. A comparison of the tax‐motivated income shifting of multinationals in

territorial and worldwide countries. Contemporary Accounting Research, 33(1), pp.7-43.

Piketty, T., 2015. About capital in the twenty-first century. American Economic Review, 105(5),

pp.48-53.

TAXATION

References:

Benzarti, Y. and Carloni, D., 2017. Who Really Benefits from Consumption Tax Cuts? Evidence

from a Large VAT Reform in France (No. w23848). National Bureau of Economic Research, pp.

7-21.

Benzarti, Y. and Carloni, D., 2016. Who Really Benefits From Consumption Tax Cuts? Evidence

From a Large VAT Cut in France. Working Paper, 11(1), pp.117-132.

Blanchet, T., Fournier, J. and Piketty, T., 2017. Generalized Pareto curves: Theory and

applications to income and wealth tax data for France and the United States, 1800-2014. WID.

world WorkingPaper, (2017/3).

Evers, L., Miller, H. and Spengel, C., 2015. Intellectual property box regimes: effective tax rates

and tax policy considerations. International Tax and Public Finance, 22(3), pp.502-530.

Hoynes, H., Miller, D. and Simon, D., 2015. Income, the earned income tax credit, and infant

health. American Economic Journal: Economic Policy, 7(1), pp.172-211.

Lefebvre, M., Pestieau, P., Riedl, A. and Villeval, M.C., 2015. Tax evasion and social

information: an experiment in Belgium, France, and the Netherlands. International Tax and

Public Finance, 22(3), pp.401-425.

Markle, K., 2016. A comparison of the tax‐motivated income shifting of multinationals in

territorial and worldwide countries. Contemporary Accounting Research, 33(1), pp.7-43.

Piketty, T., 2015. About capital in the twenty-first century. American Economic Review, 105(5),

pp.48-53.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.