Analyzing Fraud Detection in Banking Sector Using Big Data Analytics

VerifiedAdded on 2023/06/14

|22

|4234

|421

Report

AI Summary

This report examines the use of Big Data analytics for fraud detection in the banking sector. It discusses data collection and storage methods, highlighting how banks can leverage large datasets to identify and prevent fraudulent activities in real-time. The report delves into practical applications of data, focusing on consumer-centric product design and recommendation systems tailored to customer needs. Furthermore, it addresses the importance of business continuity, exploring how online banking operations can withstand power outages and disasters. The analysis covers various data types collected by banks, including corrupted data, cash transactions, billing data, and indicators of skimming and larceny, alongside storage system requirements like statistical calculation, classification, and digital analysis. The study emphasizes the shift towards proactive risk identification and improved fraud prevention through enhanced analytic solutions.

Running head: FRAUD DETECTION IN BANKING SECTOR

Fraud Detection in Banking Sector

Name of the student:

Name of the university:

Author Note

Fraud Detection in Banking Sector

Name of the student:

Name of the university:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FRAUD DETECTION IN BANKING SECTOR

Executive summary

The report demonstrates the methods of data storage and collection for significant data application at

bank regarding fraudulent activities. Big data of the current era is highly useful to find out the fraud

and risks. The study analyzes the data in action keeping recommendation system and customer-

centric product design in mind. At last, a discussion is made about how the online business of today

can survive the power outrages and disasters.

Executive summary

The report demonstrates the methods of data storage and collection for significant data application at

bank regarding fraudulent activities. Big data of the current era is highly useful to find out the fraud

and risks. The study analyzes the data in action keeping recommendation system and customer-

centric product design in mind. At last, a discussion is made about how the online business of today

can survive the power outrages and disasters.

2FRAUD DETECTION IN BANKING SECTOR

Table of Contents

Introduction:..........................................................................................................................................3

Task 1: Data Collection and Storage through Big Data:.......................................................................3

1.1. Data collection system:...............................................................................................................3

1.2. Storage systems:.........................................................................................................................5

Task2. Data in action for banks:............................................................................................................6

2.1. Consumer-centric product design:..............................................................................................7

2.2. Recommendation system:...........................................................................................................8

Task 3. Business continuityfor banks using Big Data:........................................................................11

Conclusion:..........................................................................................................................................14

Recommendation:................................................................................................................................14

References:..........................................................................................................................................16

Table of Contents

Introduction:..........................................................................................................................................3

Task 1: Data Collection and Storage through Big Data:.......................................................................3

1.1. Data collection system:...............................................................................................................3

1.2. Storage systems:.........................................................................................................................5

Task2. Data in action for banks:............................................................................................................6

2.1. Consumer-centric product design:..............................................................................................7

2.2. Recommendation system:...........................................................................................................8

Task 3. Business continuityfor banks using Big Data:........................................................................11

Conclusion:..........................................................................................................................................14

Recommendation:................................................................................................................................14

References:..........................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FRAUD DETECTION IN BANKING SECTOR

Introduction:

Banks of the current era has been increasingly turning to analytics for predicting and

preventing fraud at real-time. It has been at many times inconvenience for their clients who have

been making massive purchases or undergoing travelling. However, the critical trouble for the banks

has been top decrease billions of losses because of that fraud.

Fraud detection at banks has been already looking at various factors like poor IP addresses

and unusual login times. On the other hand, Big Data application has been drastically altering the

approach with an enhanced analytic solution (Sobolevsky et al. 2014). They are fast and powerful

enough for detecting fraud in real time and identifying risks proactively.

The following report analyzes the data storage and collection for the current scenario. Then it

demonstrates the data in action regarding consumer-centric product design and a recommendation

system. Lastly, the business continuity is discussed regarding how today’s online business survives

the disasters and power outrages.

Task 1: Data Collection and Storage through Big Data:

1.1. Data collection system:

There are various kinds of data to be collected by banks through multiple processed. The examples

are encountered below.

The data to be

collected by banks

The processes

Corrupted data First of all the customers are to be found who have been appearing on

Introduction:

Banks of the current era has been increasingly turning to analytics for predicting and

preventing fraud at real-time. It has been at many times inconvenience for their clients who have

been making massive purchases or undergoing travelling. However, the critical trouble for the banks

has been top decrease billions of losses because of that fraud.

Fraud detection at banks has been already looking at various factors like poor IP addresses

and unusual login times. On the other hand, Big Data application has been drastically altering the

approach with an enhanced analytic solution (Sobolevsky et al. 2014). They are fast and powerful

enough for detecting fraud in real time and identifying risks proactively.

The following report analyzes the data storage and collection for the current scenario. Then it

demonstrates the data in action regarding consumer-centric product design and a recommendation

system. Lastly, the business continuity is discussed regarding how today’s online business survives

the disasters and power outrages.

Task 1: Data Collection and Storage through Big Data:

1.1. Data collection system:

There are various kinds of data to be collected by banks through multiple processed. The examples

are encountered below.

The data to be

collected by banks

The processes

Corrupted data First of all the customers are to be found who have been appearing on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FRAUD DETECTION IN BANKING SECTOR

treasury department of forensic assent control. Then the financial

Action Taskforce must be ensured over money laundering compliance.

Then a list of transactions must be produced with various agencies on

the list of different non-cooperative territories and countries.

Data about cash The transactions of money are to be identified below regulatory

thresholds of reporting. Then a series of cash disbursements are to be

determined through customer number that exceeds the statutory

reporting thresholds together. Then the statistically unusual amount of

transfer of cash is to identify done by customers or through bank

accounts (Chen, Mao and Liu 2014).

Billing data They are retrieved through a huge number of waved fees that are

transferred to bank account and customer.

Checking tampering The out of sequence, void, duplicate and missing check numbers are

to be identified. Then checks paid are to be determined that has never

been matching checks that are issued by check though banks. Then the

falsification and check forgery are to be located on various loan

applications (Martin 2015).

Skimming First of all the concise time deposits must be highlighted and the

withdrawal must be made on the similar account ny banls. Then the

indicators of the kiting checks are to be indications. The duplication of

skimming and credit card transactions are to be highlighted.

Larceny First of all the customer account takeover must be identified along

with co-opted information about customer account (Hilbert 2016).

Then the number of loans must be located by the bank employee or

treasury department of forensic assent control. Then the financial

Action Taskforce must be ensured over money laundering compliance.

Then a list of transactions must be produced with various agencies on

the list of different non-cooperative territories and countries.

Data about cash The transactions of money are to be identified below regulatory

thresholds of reporting. Then a series of cash disbursements are to be

determined through customer number that exceeds the statutory

reporting thresholds together. Then the statistically unusual amount of

transfer of cash is to identify done by customers or through bank

accounts (Chen, Mao and Liu 2014).

Billing data They are retrieved through a huge number of waved fees that are

transferred to bank account and customer.

Checking tampering The out of sequence, void, duplicate and missing check numbers are

to be identified. Then checks paid are to be determined that has never

been matching checks that are issued by check though banks. Then the

falsification and check forgery are to be located on various loan

applications (Martin 2015).

Skimming First of all the concise time deposits must be highlighted and the

withdrawal must be made on the similar account ny banls. Then the

indicators of the kiting checks are to be indications. The duplication of

skimming and credit card transactions are to be highlighted.

Larceny First of all the customer account takeover must be identified along

with co-opted information about customer account (Hilbert 2016).

Then the number of loans must be located by the bank employee or

5FRAUD DETECTION IN BANKING SECTOR

customer instead of repayments. Later it must be found that the

amount of investment has been higher that value of a particular item or

the collateral. Then the sudden activities are to highlighted under

dormant customer accounts. This involves the identification of the

person which has been processing transactions against those accounts.

Lastly, the mortgage fraud schemes are to be isolated through

determining straw buyer indicators of a plan.

Financial statement fraud For this, the suspense and dormant general ledger accounts must be

monitored. Then the journal entries are to be identified at suspicious

times.

1.2. Storage systems:

To understand the storage systems by big data , various factors are considered. The first one

is the area where the fraud takes place. The next one is the fraudulent activities that have been

looking like the data. The last one is the data source that is needed to test the indicators of fraud.

Requirements for

storage

Methods to achieve them

Calculating the statistical

parameters

These include high/low values, standard deviations and averages. The

calculation is done by identifying outliers indicating fraud.

Classification This is done through finding patterns among various data elements.

Stratification of numbers These are done through identifying unusual entries like excessively

low or high values (Kitchin 2014).

Digital analysis through This is done through identifying various occurrences of digits that

customer instead of repayments. Later it must be found that the

amount of investment has been higher that value of a particular item or

the collateral. Then the sudden activities are to highlighted under

dormant customer accounts. This involves the identification of the

person which has been processing transactions against those accounts.

Lastly, the mortgage fraud schemes are to be isolated through

determining straw buyer indicators of a plan.

Financial statement fraud For this, the suspense and dormant general ledger accounts must be

monitored. Then the journal entries are to be identified at suspicious

times.

1.2. Storage systems:

To understand the storage systems by big data , various factors are considered. The first one

is the area where the fraud takes place. The next one is the fraudulent activities that have been

looking like the data. The last one is the data source that is needed to test the indicators of fraud.

Requirements for

storage

Methods to achieve them

Calculating the statistical

parameters

These include high/low values, standard deviations and averages. The

calculation is done by identifying outliers indicating fraud.

Classification This is done through finding patterns among various data elements.

Stratification of numbers These are done through identifying unusual entries like excessively

low or high values (Kitchin 2014).

Digital analysis through This is done through identifying various occurrences of digits that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FRAUD DETECTION IN BANKING SECTOR

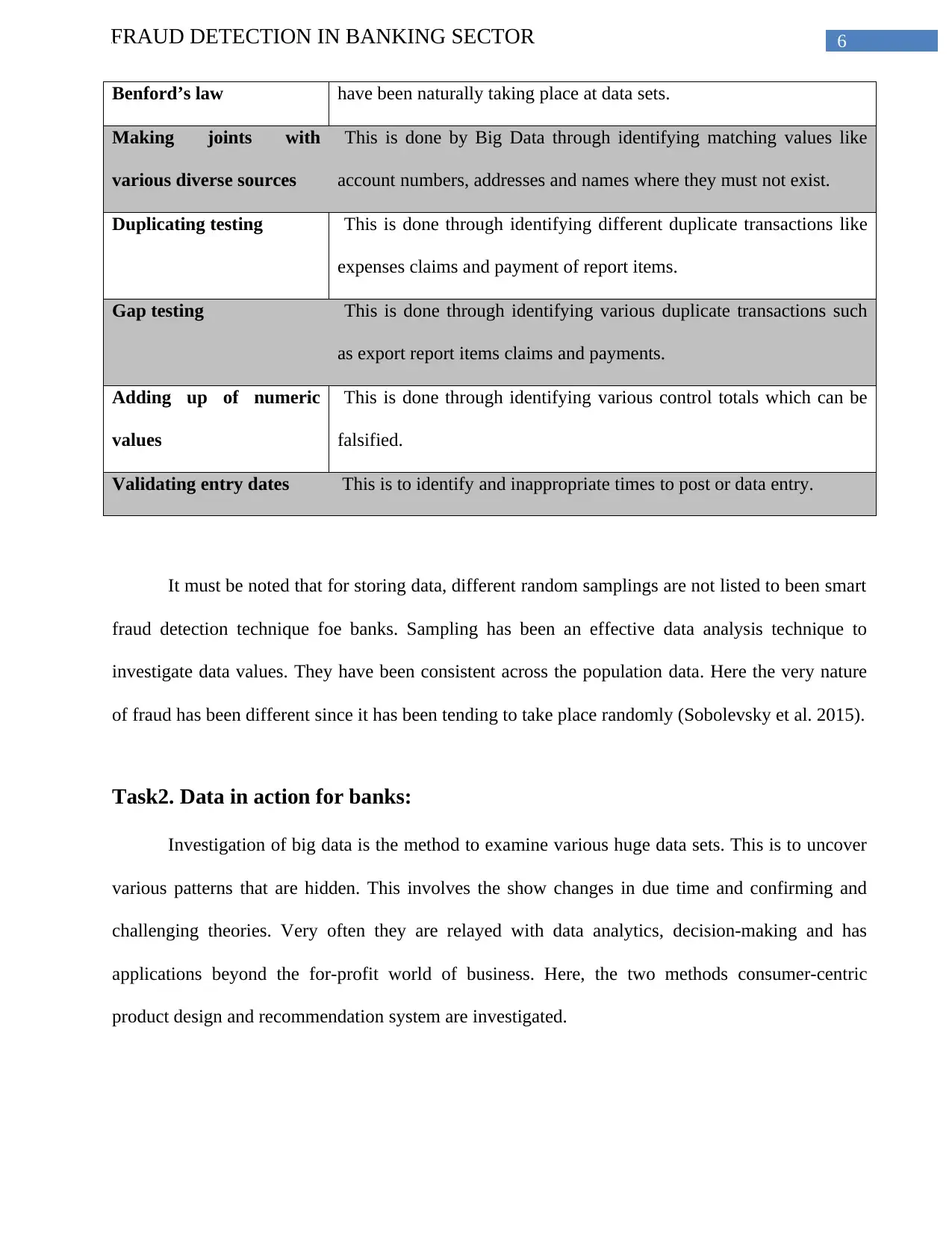

Benford’s law have been naturally taking place at data sets.

Making joints with

various diverse sources

This is done by Big Data through identifying matching values like

account numbers, addresses and names where they must not exist.

Duplicating testing This is done through identifying different duplicate transactions like

expenses claims and payment of report items.

Gap testing This is done through identifying various duplicate transactions such

as export report items claims and payments.

Adding up of numeric

values

This is done through identifying various control totals which can be

falsified.

Validating entry dates This is to identify and inappropriate times to post or data entry.

It must be noted that for storing data, different random samplings are not listed to been smart

fraud detection technique foe banks. Sampling has been an effective data analysis technique to

investigate data values. They have been consistent across the population data. Here the very nature

of fraud has been different since it has been tending to take place randomly (Sobolevsky et al. 2015).

Task2. Data in action for banks:

Investigation of big data is the method to examine various huge data sets. This is to uncover

various patterns that are hidden. This involves the show changes in due time and confirming and

challenging theories. Very often they are relayed with data analytics, decision-making and has

applications beyond the for-profit world of business. Here, the two methods consumer-centric

product design and recommendation system are investigated.

Benford’s law have been naturally taking place at data sets.

Making joints with

various diverse sources

This is done by Big Data through identifying matching values like

account numbers, addresses and names where they must not exist.

Duplicating testing This is done through identifying different duplicate transactions like

expenses claims and payment of report items.

Gap testing This is done through identifying various duplicate transactions such

as export report items claims and payments.

Adding up of numeric

values

This is done through identifying various control totals which can be

falsified.

Validating entry dates This is to identify and inappropriate times to post or data entry.

It must be noted that for storing data, different random samplings are not listed to been smart

fraud detection technique foe banks. Sampling has been an effective data analysis technique to

investigate data values. They have been consistent across the population data. Here the very nature

of fraud has been different since it has been tending to take place randomly (Sobolevsky et al. 2015).

Task2. Data in action for banks:

Investigation of big data is the method to examine various huge data sets. This is to uncover

various patterns that are hidden. This involves the show changes in due time and confirming and

challenging theories. Very often they are relayed with data analytics, decision-making and has

applications beyond the for-profit world of business. Here, the two methods consumer-centric

product design and recommendation system are investigated.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FRAUD DETECTION IN BANKING SECTOR

2.1. Consumer-centric product design:

It is also known as user-centric design. It is the process to frame services and products across

the various limitations and necessities of end users done by Big Data. It has both regarding designing

and quality of content, service and product (Varian 2014). For a bank, it indicates the entire

development and design process must take place keeping the user of a database in mind from the

step one. The various rules of customer-centric design involve the following.

Filling the reservoirs of bank’s customer knowledge:

For instance, the salespeople of a bank are accountable to send enquiries of customers on to

the support. Here, the support staffs have been responsible for funnelling the contents of various

customer conversations for the proper produce person. Here, the project managers are accountable to

decide what feedbacks must be acted upon (Chen and Lin 2014).

Using customer knowledge to make the banks customer-centric:

Here the customer-centric product team are attentive to the voice of customers at the early

stage of product development prior its development, during construction and after the expansion.

Next, the customer experiences and needs ate considerable factors to undertake decisions regarding

what latest features have been implemented, where to expand and push the vision forward (Cao

2015).

Prioritizing roadmaps for business and users:

This can be effectively done through using the formula (Value/Complexity)*Necessity^2.

2.1. Consumer-centric product design:

It is also known as user-centric design. It is the process to frame services and products across

the various limitations and necessities of end users done by Big Data. It has both regarding designing

and quality of content, service and product (Varian 2014). For a bank, it indicates the entire

development and design process must take place keeping the user of a database in mind from the

step one. The various rules of customer-centric design involve the following.

Filling the reservoirs of bank’s customer knowledge:

For instance, the salespeople of a bank are accountable to send enquiries of customers on to

the support. Here, the support staffs have been responsible for funnelling the contents of various

customer conversations for the proper produce person. Here, the project managers are accountable to

decide what feedbacks must be acted upon (Chen and Lin 2014).

Using customer knowledge to make the banks customer-centric:

Here the customer-centric product team are attentive to the voice of customers at the early

stage of product development prior its development, during construction and after the expansion.

Next, the customer experiences and needs ate considerable factors to undertake decisions regarding

what latest features have been implemented, where to expand and push the vision forward (Cao

2015).

Prioritizing roadmaps for business and users:

This can be effectively done through using the formula (Value/Complexity)*Necessity^2.

8FRAUD DETECTION IN BANKING SECTOR

This must be done regularly to weigh the long listing ideas and to pick the one that is needed

to be given the most priority. Here for all the ideas, a score from 1 to 10 must be assigned for every

variable. Next, the totals score must be calculated ranking every idea.

Solving issues for the user during the creation:

Here, the critical phase has been designing the user experience. As the implementation

process goes on, here, the customer-centric team focuses on developing and delivering a user

experience that has been easy and intuitive for customers to use (Hu et al. 2014). Further, the design

of user experience has been the design reframed. This term emphasizes solving problems for users.

This is the reminder that the model has not been making pretty. Besides, it is the process to craft the

holistic beginning-to-end experience accounting every detail of journey of users.

Communicating changes to a customer after the development is complete:

As the implementation is done, a new feature request is needed to be made. This is intended

to be accountable regarding communicating changes to customers. Here, the communication has

been the important method of establishing transparency and trust regarding delivering. It must be

reminded for banks that quick turnarounds over bank’s customer feature requests have been in a long

way to go. However, this has been a slower turnaround that must garner till there is any

communication (Stimmel 2016).

2.2. Recommendation system:

The recommender systems for banks are a complicated approach to achieve customer goals.

The various steps undertaken by Big Data analysis are analysed below.

Problem facing:

This must be done regularly to weigh the long listing ideas and to pick the one that is needed

to be given the most priority. Here for all the ideas, a score from 1 to 10 must be assigned for every

variable. Next, the totals score must be calculated ranking every idea.

Solving issues for the user during the creation:

Here, the critical phase has been designing the user experience. As the implementation

process goes on, here, the customer-centric team focuses on developing and delivering a user

experience that has been easy and intuitive for customers to use (Hu et al. 2014). Further, the design

of user experience has been the design reframed. This term emphasizes solving problems for users.

This is the reminder that the model has not been making pretty. Besides, it is the process to craft the

holistic beginning-to-end experience accounting every detail of journey of users.

Communicating changes to a customer after the development is complete:

As the implementation is done, a new feature request is needed to be made. This is intended

to be accountable regarding communicating changes to customers. Here, the communication has

been the important method of establishing transparency and trust regarding delivering. It must be

reminded for banks that quick turnarounds over bank’s customer feature requests have been in a long

way to go. However, this has been a slower turnaround that must garner till there is any

communication (Stimmel 2016).

2.2. Recommendation system:

The recommender systems for banks are a complicated approach to achieve customer goals.

The various steps undertaken by Big Data analysis are analysed below.

Problem facing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FRAUD DETECTION IN BANKING SECTOR

It includes the collection of expectations, requirements and issues from concerned employees

and business departments. Here, the interviews are conducted with stakeholders with various

clarified needs for the system and managing vision of clients.

Data processing and collection:

At this step, every necessary CRM and various transactional data for the clients of banks are

needed for subsequent data analysis and preprocessing. Here the data set includes social-

demographical data, purchase history of clients, history of balances, monthly payments and

information about the client. The step involves the checking of data consistency taking place among

various sources and treatment of inconsistencies. It further includes the handling of duplicates and

null values (Li, Cao and Yao 2015). Moreover, this provides dictionary transformation and forming

along with statistics calculation. Here, the problems detected and various solutions to it are reported

to clients.

Data processing and development of algorithms:

This stage starts with data augmentation actions that result in mining changes to spend speed

or growth of income and various client event triggers. For understanding the financial behaviour, the

banks must calculate the aggregate balances and outcome or income transfers for multiple periods.

Here the features are merged with different elements from CRM system like purchase history of

clients, social-demographic data and so on (Olson and Wu 2017). Here, various types of machine

algorithms are applicable on the features to predict best recommendations regarding products for

clients.

A/B testing:

It includes the collection of expectations, requirements and issues from concerned employees

and business departments. Here, the interviews are conducted with stakeholders with various

clarified needs for the system and managing vision of clients.

Data processing and collection:

At this step, every necessary CRM and various transactional data for the clients of banks are

needed for subsequent data analysis and preprocessing. Here the data set includes social-

demographical data, purchase history of clients, history of balances, monthly payments and

information about the client. The step involves the checking of data consistency taking place among

various sources and treatment of inconsistencies. It further includes the handling of duplicates and

null values (Li, Cao and Yao 2015). Moreover, this provides dictionary transformation and forming

along with statistics calculation. Here, the problems detected and various solutions to it are reported

to clients.

Data processing and development of algorithms:

This stage starts with data augmentation actions that result in mining changes to spend speed

or growth of income and various client event triggers. For understanding the financial behaviour, the

banks must calculate the aggregate balances and outcome or income transfers for multiple periods.

Here the features are merged with different elements from CRM system like purchase history of

clients, social-demographic data and so on (Olson and Wu 2017). Here, various types of machine

algorithms are applicable on the features to predict best recommendations regarding products for

clients.

A/B testing:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FRAUD DETECTION IN BANKING SECTOR

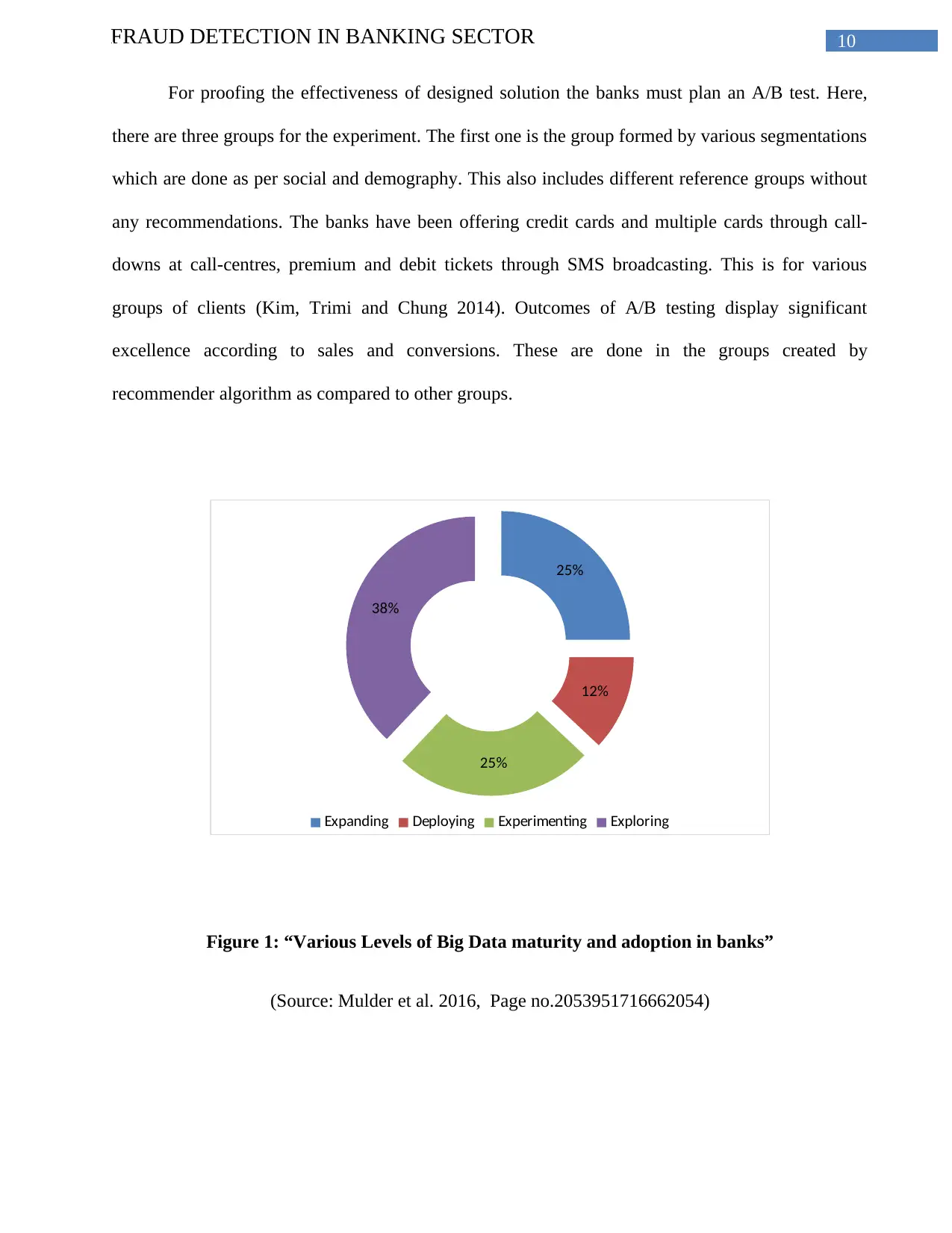

For proofing the effectiveness of designed solution the banks must plan an A/B test. Here,

there are three groups for the experiment. The first one is the group formed by various segmentations

which are done as per social and demography. This also includes different reference groups without

any recommendations. The banks have been offering credit cards and multiple cards through call-

downs at call-centres, premium and debit tickets through SMS broadcasting. This is for various

groups of clients (Kim, Trimi and Chung 2014). Outcomes of A/B testing display significant

excellence according to sales and conversions. These are done in the groups created by

recommender algorithm as compared to other groups.

25%

12%

25%

38%

Expanding Deploying Experimenting Exploring

Figure 1: “Various Levels of Big Data maturity and adoption in banks”

(Source: Mulder et al. 2016, Page no.2053951716662054)

For proofing the effectiveness of designed solution the banks must plan an A/B test. Here,

there are three groups for the experiment. The first one is the group formed by various segmentations

which are done as per social and demography. This also includes different reference groups without

any recommendations. The banks have been offering credit cards and multiple cards through call-

downs at call-centres, premium and debit tickets through SMS broadcasting. This is for various

groups of clients (Kim, Trimi and Chung 2014). Outcomes of A/B testing display significant

excellence according to sales and conversions. These are done in the groups created by

recommender algorithm as compared to other groups.

25%

12%

25%

38%

Expanding Deploying Experimenting Exploring

Figure 1: “Various Levels of Big Data maturity and adoption in banks”

(Source: Mulder et al. 2016, Page no.2053951716662054)

11FRAUD DETECTION IN BANKING SECTOR

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.