Analysis of Financial Statements for Fraudulent Activities

VerifiedAdded on 2020/05/11

|19

|3492

|49

AI Summary

In this case study, students are tasked with analyzing financial data from three consecutive years to uncover any irregularities or signs of fraudulent activities within a company's financial reporting. The assignment requires examining changes in cash flow, receivables, inventories, liabilities, and equity positions over the period. Students will leverage insights from references such as forensic accounting techniques discussed by Bamberger et al., 'Forensic Accounting Investigation: A Practitioner’s Guide,' to apply theoretical knowledge practically. The goal is to develop a comprehensive understanding of financial anomalies that could indicate fraud, such as unusual fluctuations in asset valuations or liabilities and inconsistencies in reported earnings compared to cash flows. By cross-referencing the provided data with forensic accounting practices, students will prepare a detailed report highlighting their findings and suggesting potential areas for further investigation.

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Auditing

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Executive Summary:

The current report aims to evaluate the industry and the overall business environment of

the Bayou Hedge Fund Group from the perspective of a trainee auditor in an accounting firm. In

addition, it lays stress on the corporate governance practices, risk analysis, factors and issues

causing the collapse of the fund. It has been found that the primary reasons behind the inability

of the Bayou Hedge Fund Group to cope up with the situation unlike the other hedge funds

include the ineffective ethical practices, lack of core group of norms and strong ideology, which

promote the well-being of the stakeholders of the organisation.

The stock price of the organisation is highly overvalued and hence, the investors have

encountered massive losses due to the collapse of the same. From the ratio and trend analyses

conducted, it could be inferred that the accountants have manipulated the accounting figures and

the organisation had bribed the external auditing firm to certify its financial statements in

compliance with the then prevailing accounting norms of the nation.

Executive Summary:

The current report aims to evaluate the industry and the overall business environment of

the Bayou Hedge Fund Group from the perspective of a trainee auditor in an accounting firm. In

addition, it lays stress on the corporate governance practices, risk analysis, factors and issues

causing the collapse of the fund. It has been found that the primary reasons behind the inability

of the Bayou Hedge Fund Group to cope up with the situation unlike the other hedge funds

include the ineffective ethical practices, lack of core group of norms and strong ideology, which

promote the well-being of the stakeholders of the organisation.

The stock price of the organisation is highly overvalued and hence, the investors have

encountered massive losses due to the collapse of the same. From the ratio and trend analyses

conducted, it could be inferred that the accountants have manipulated the accounting figures and

the organisation had bribed the external auditing firm to certify its financial statements in

compliance with the then prevailing accounting norms of the nation.

2AUDITING

Table of Contents

1. Introduction:................................................................................................................................3

2. Industry and business environment:............................................................................................3

3. Corporate governance:.................................................................................................................4

4. Risk analysis:...............................................................................................................................5

5. Factors of collapse:......................................................................................................................6

6. Ratio, trend analysis or analytical procedures:............................................................................8

7. Conclusion:................................................................................................................................13

References:....................................................................................................................................15

Appendices:...................................................................................................................................17

Table of Contents

1. Introduction:................................................................................................................................3

2. Industry and business environment:............................................................................................3

3. Corporate governance:.................................................................................................................4

4. Risk analysis:...............................................................................................................................5

5. Factors of collapse:......................................................................................................................6

6. Ratio, trend analysis or analytical procedures:............................................................................8

7. Conclusion:................................................................................................................................13

References:....................................................................................................................................15

Appendices:...................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

1. Introduction:

In 1995, Samuel Israel III had established the Bayou Hedge Fund Group, termed as the

fund, in Stamford, Connecticut with the aim of producing greater returns for the investors. There

was absence of good intentions at the time the organisation had suffered losses immediately. Due

to this, Mr. Israel has adopted unscrupulous activities for keeping the view of success alive. The

resulting fund life was filled up with fraudulent, illicit and unethical activities, which has lead the

organisation to bankruptcy and Mr. Israel along with few of his key associates have been

imprisoned (Bodellini 2016).

This report aims to evaluate the industry and the overall business environment of the

Bayou Hedge Fund Group from the perspective of a trainee auditor in an accounting firm. In

addition, it lays stress on the corporate governance practices, risk analysis, factors and issues

causing the collapse of the fund. Finally, the report sheds light on conducting the ratio analysis

and trend analysis of the chosen organisation to depict the misleading financial statements, which

are prepared on the part of the unknown auditors.

2. Industry and business environment:

The industry and business environment of hedge fund could be characterised with the

help of the following features:

The industry is open to the qualified investors only, as hedge funds are allowed only to

obtain money from the accredited investors. The individuals having annual income of

above $200,000 for the last two years or net worth above 1 million excluding their

primary residences have the power to invest in hedge funds (Fishman 2014).

1. Introduction:

In 1995, Samuel Israel III had established the Bayou Hedge Fund Group, termed as the

fund, in Stamford, Connecticut with the aim of producing greater returns for the investors. There

was absence of good intentions at the time the organisation had suffered losses immediately. Due

to this, Mr. Israel has adopted unscrupulous activities for keeping the view of success alive. The

resulting fund life was filled up with fraudulent, illicit and unethical activities, which has lead the

organisation to bankruptcy and Mr. Israel along with few of his key associates have been

imprisoned (Bodellini 2016).

This report aims to evaluate the industry and the overall business environment of the

Bayou Hedge Fund Group from the perspective of a trainee auditor in an accounting firm. In

addition, it lays stress on the corporate governance practices, risk analysis, factors and issues

causing the collapse of the fund. Finally, the report sheds light on conducting the ratio analysis

and trend analysis of the chosen organisation to depict the misleading financial statements, which

are prepared on the part of the unknown auditors.

2. Industry and business environment:

The industry and business environment of hedge fund could be characterised with the

help of the following features:

The industry is open to the qualified investors only, as hedge funds are allowed only to

obtain money from the accredited investors. The individuals having annual income of

above $200,000 for the last two years or net worth above 1 million excluding their

primary residences have the power to invest in hedge funds (Fishman 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

Although the hedge funds provide broader investment latitude compared to other funds,

the mandate limits the investment of the funds. For instance, the investors in Bayou

Hedge Fund Group had invested in land, stocks, derivatives, currencies and real estate.

Since the hedge fund industry is involved in employing leverage, they often utilise

borrowed money for amplifying their overall returns (Gupta, Becam and Gregoriou

2016). However, leverage in financial crisis wipes out hedge funds and in case of Bayou

Hedge Fund Group, the occurrence is prior to the financial crisis.

The hedge funds often charge both performance fee and expense ratio, instead of

charging only expense ratio. The fee structure is termed as “Two and Twenty”, which is

2% fee related to asset management and 20% cut of any gains generated.

3. Corporate governance:

The management of Bayou Hedge Fund Group did not provide adequate respect to its

stakeholders. Mr. Israel and some of his associates have been greedy, as their main motive is to

make profit due to which they started to make poor or making one-sided decisions (Jaitly 2016).

The external pressure from the market, especially from the stock market of the nation, had lead

to the collapse of the organisation.

As pointed out by Jaitly (2016), the primary reasons behind the inability of the Bayou

Hedge Fund Group to cope up with the situation unlike the other hedge funds include the

ineffective ethical practices, lack of core group of norms and strong ideology, which promote the

well-being of the stakeholders of the organisation. The main stakeholders of the Bayou Hedge

Fund Group comprise of the insurers, investors, organisational staffs, government, lenders and

Although the hedge funds provide broader investment latitude compared to other funds,

the mandate limits the investment of the funds. For instance, the investors in Bayou

Hedge Fund Group had invested in land, stocks, derivatives, currencies and real estate.

Since the hedge fund industry is involved in employing leverage, they often utilise

borrowed money for amplifying their overall returns (Gupta, Becam and Gregoriou

2016). However, leverage in financial crisis wipes out hedge funds and in case of Bayou

Hedge Fund Group, the occurrence is prior to the financial crisis.

The hedge funds often charge both performance fee and expense ratio, instead of

charging only expense ratio. The fee structure is termed as “Two and Twenty”, which is

2% fee related to asset management and 20% cut of any gains generated.

3. Corporate governance:

The management of Bayou Hedge Fund Group did not provide adequate respect to its

stakeholders. Mr. Israel and some of his associates have been greedy, as their main motive is to

make profit due to which they started to make poor or making one-sided decisions (Jaitly 2016).

The external pressure from the market, especially from the stock market of the nation, had lead

to the collapse of the organisation.

As pointed out by Jaitly (2016), the primary reasons behind the inability of the Bayou

Hedge Fund Group to cope up with the situation unlike the other hedge funds include the

ineffective ethical practices, lack of core group of norms and strong ideology, which promote the

well-being of the stakeholders of the organisation. The main stakeholders of the Bayou Hedge

Fund Group comprise of the insurers, investors, organisational staffs, government, lenders and

5AUDITING

borrowers and these groups have been influenced adversely due to the unethical decisions made

on the part of the management.

In the words of Jorion and Schwarz (2014), the corporate governance of the Bayou

Hedge Fund Group could be considered as deontology, since in a business decision, it is not

possible for anyone to remain aware of the consequences in the beginning years. However, the

organisation could have adopted set of ethical policies and norms that it could follow in the

beginning years. These ethical norms would take care of the decisions automatically, since such

rules could not control the consequences of such decisions. Hence, Bayou Hedge Fund Group or

its executives could have undertaken ethical decisions from the initial stage that could have

saved the organisation from bankruptcy (Kaal 2013).

In addition, the board of directors of the Bayou Hedge Fund Group could have

concentrated on making ethical decisions and ethical theory decades ago. If such practice had

been adopted, it could have helped in protecting and navigating the fund from such illegal

activities (Pascalau 2014). However, the organisation has failed to manage the situation due to

the market deficiencies and greed had besieged the top executives.

4. Risk analysis:

The risk analysis of the Bayou Hedge Fund Group could be represented as follows:

Standard deviation:

It is the most common measure of risk used in hedge funds and it ascertains the volatility

level of returns expressed in percentage terms (Ang 2017). However, in case of the Bayou Hedge

borrowers and these groups have been influenced adversely due to the unethical decisions made

on the part of the management.

In the words of Jorion and Schwarz (2014), the corporate governance of the Bayou

Hedge Fund Group could be considered as deontology, since in a business decision, it is not

possible for anyone to remain aware of the consequences in the beginning years. However, the

organisation could have adopted set of ethical policies and norms that it could follow in the

beginning years. These ethical norms would take care of the decisions automatically, since such

rules could not control the consequences of such decisions. Hence, Bayou Hedge Fund Group or

its executives could have undertaken ethical decisions from the initial stage that could have

saved the organisation from bankruptcy (Kaal 2013).

In addition, the board of directors of the Bayou Hedge Fund Group could have

concentrated on making ethical decisions and ethical theory decades ago. If such practice had

been adopted, it could have helped in protecting and navigating the fund from such illegal

activities (Pascalau 2014). However, the organisation has failed to manage the situation due to

the market deficiencies and greed had besieged the top executives.

4. Risk analysis:

The risk analysis of the Bayou Hedge Fund Group could be represented as follows:

Standard deviation:

It is the most common measure of risk used in hedge funds and it ascertains the volatility

level of returns expressed in percentage terms (Ang 2017). However, in case of the Bayou Hedge

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING

Fund Group, standard deviation fails to provide a complete risk picture of the returns due to the

absence of normally distributed returns.

Value-at-risk (VaR):

VaR gauges the dollar-loss expectation, which could happen with a probability of 5%.

This measure provides additional overview into the past returns of a hedge fund, since it captures

the lower end of the returns to the down side (Li 2016). In the case of Bayou Hedge Fund Group,

this measure had not been used on the part of the management and thus, the investors could not

obtain an insight about the volatility of stocks. As a result, the risk had increased massively and

the investors had encountered severe losses after the collapse of the organisation.

Downside capture:

In association with hedge funds, the measure of downside capture could indicate the way

of correlation of a fund with a market at the time of decline. A lower downside capture is always

favourable, since the fund could preserve additional wealth during market downturns (Markham

2013). In the case of Bayou Hedge Fund Group, the downside capture is high, as Mr. Israel has

used the funds for personal purpose and this has resulted in the downfall of the organisation.

5. Factors of collapse:

The following are the main factors identified behind the collapse of the Bayou Hedge

Fund Group:

Board weaknesses:

Fund Group, standard deviation fails to provide a complete risk picture of the returns due to the

absence of normally distributed returns.

Value-at-risk (VaR):

VaR gauges the dollar-loss expectation, which could happen with a probability of 5%.

This measure provides additional overview into the past returns of a hedge fund, since it captures

the lower end of the returns to the down side (Li 2016). In the case of Bayou Hedge Fund Group,

this measure had not been used on the part of the management and thus, the investors could not

obtain an insight about the volatility of stocks. As a result, the risk had increased massively and

the investors had encountered severe losses after the collapse of the organisation.

Downside capture:

In association with hedge funds, the measure of downside capture could indicate the way

of correlation of a fund with a market at the time of decline. A lower downside capture is always

favourable, since the fund could preserve additional wealth during market downturns (Markham

2013). In the case of Bayou Hedge Fund Group, the downside capture is high, as Mr. Israel has

used the funds for personal purpose and this has resulted in the downfall of the organisation.

5. Factors of collapse:

The following are the main factors identified behind the collapse of the Bayou Hedge

Fund Group:

Board weaknesses:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

The main board members of the Bayou Hedge Fund Group comprised of Mr. Israel, the

co-founder, Mr. James Marquez and the Chief Financial Officer, Mr. Dan Morino. These

personnel were associated with the withdrawals and gross misappropriation of investor funds.

Since Mr. Israel enjoyed the maximum power in the shareholding of the fund, the personnel had

undertaken many independent decisions about the daily operations having no regulatory body in

checking the day-to-day activities. However, neither of the founders had experience or

qualification in managing the funds of the investors (Kaal 2016).

The criminal past of Mr. Israel had been unveiled during the public trial of the

organisation, which any investor could be able to find out with the help of legal arms. A former

staff had filed a federal lawsuit claiming breach of SEC norms of hedge funds and this has

placed the matter into arbitration. In addition, the corporate boards had failed to depict the

interests of the shareholders adequately along with exerting scrutiny over incumbent

management. The group board of the organisation depicts structural weaknesses comprising of

lack of autonomy and the positions.

Management weaknesses (fraudulent management practices):

The managers receive incentives in different types on accomplishing the performance

expectations, which often result in accounting fraud. This is because the non-financial intentions

are highly powerful and they are the strong reasons for conducting accounting fraud (Kokkila

2016). The scandal occurred at the time the regulators of Arizona seized $100 million from Karl

Johnson holding the money for Mr. Israel to invest in bank instruments yielding over $7.1 billion

in above 10 years. During seizure, the regulators did not have an insight of the ongoing situation.

The organisation had passed a board resolution that Mr. Israel should hold $100 million for

The main board members of the Bayou Hedge Fund Group comprised of Mr. Israel, the

co-founder, Mr. James Marquez and the Chief Financial Officer, Mr. Dan Morino. These

personnel were associated with the withdrawals and gross misappropriation of investor funds.

Since Mr. Israel enjoyed the maximum power in the shareholding of the fund, the personnel had

undertaken many independent decisions about the daily operations having no regulatory body in

checking the day-to-day activities. However, neither of the founders had experience or

qualification in managing the funds of the investors (Kaal 2016).

The criminal past of Mr. Israel had been unveiled during the public trial of the

organisation, which any investor could be able to find out with the help of legal arms. A former

staff had filed a federal lawsuit claiming breach of SEC norms of hedge funds and this has

placed the matter into arbitration. In addition, the corporate boards had failed to depict the

interests of the shareholders adequately along with exerting scrutiny over incumbent

management. The group board of the organisation depicts structural weaknesses comprising of

lack of autonomy and the positions.

Management weaknesses (fraudulent management practices):

The managers receive incentives in different types on accomplishing the performance

expectations, which often result in accounting fraud. This is because the non-financial intentions

are highly powerful and they are the strong reasons for conducting accounting fraud (Kokkila

2016). The scandal occurred at the time the regulators of Arizona seized $100 million from Karl

Johnson holding the money for Mr. Israel to invest in bank instruments yielding over $7.1 billion

in above 10 years. During seizure, the regulators did not have an insight of the ongoing situation.

The organisation had passed a board resolution that Mr. Israel should hold $100 million for

8AUDITING

offshore investments. The personnel had been involved in sending mails daily to the investors

along with informing them about the closure of the fund operations to devote time for family and

that the investors would receive funds in mid-August. This was the last communication made to

the clients and after that; the investors had not obtained their funds.

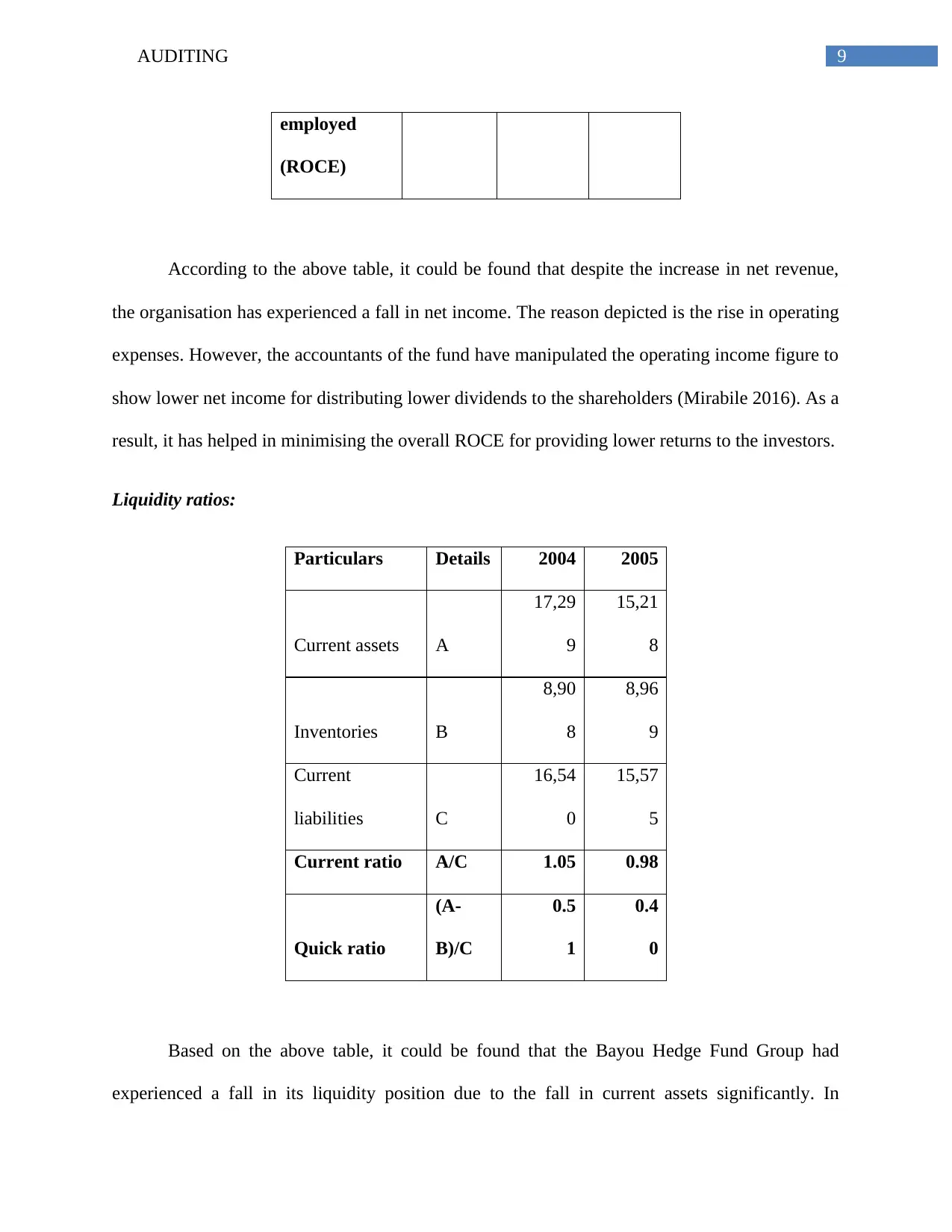

6. Ratio, trend analysis or analytical procedures:

The following ratios have been considered to evaluate the reasons behind the collapse of

the Bayou Hedge Fund Group:

Profitability ratios:

Particulars Details 2004 2005

Revenue A

1,16,19

9

1,18,71

9

Net income B

2,37

7

2,35

0

Operating

income C

3,62

4

3,67

2

Total assets D

33,44

0

33,16

3

Total current

liabilities E

16,54

0

15,57

5

Net margin B/A 2.05% 1.98%

Return on

capital

C/(D-E) 21.44% 20.88%

offshore investments. The personnel had been involved in sending mails daily to the investors

along with informing them about the closure of the fund operations to devote time for family and

that the investors would receive funds in mid-August. This was the last communication made to

the clients and after that; the investors had not obtained their funds.

6. Ratio, trend analysis or analytical procedures:

The following ratios have been considered to evaluate the reasons behind the collapse of

the Bayou Hedge Fund Group:

Profitability ratios:

Particulars Details 2004 2005

Revenue A

1,16,19

9

1,18,71

9

Net income B

2,37

7

2,35

0

Operating

income C

3,62

4

3,67

2

Total assets D

33,44

0

33,16

3

Total current

liabilities E

16,54

0

15,57

5

Net margin B/A 2.05% 1.98%

Return on

capital

C/(D-E) 21.44% 20.88%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING

employed

(ROCE)

According to the above table, it could be found that despite the increase in net revenue,

the organisation has experienced a fall in net income. The reason depicted is the rise in operating

expenses. However, the accountants of the fund have manipulated the operating income figure to

show lower net income for distributing lower dividends to the shareholders (Mirabile 2016). As a

result, it has helped in minimising the overall ROCE for providing lower returns to the investors.

Liquidity ratios:

Particulars Details 2004 2005

Current assets A

17,29

9

15,21

8

Inventories B

8,90

8

8,96

9

Current

liabilities C

16,54

0

15,57

5

Current ratio A/C 1.05 0.98

Quick ratio

(A-

B)/C

0.5

1

0.4

0

Based on the above table, it could be found that the Bayou Hedge Fund Group had

experienced a fall in its liquidity position due to the fall in current assets significantly. In

employed

(ROCE)

According to the above table, it could be found that despite the increase in net revenue,

the organisation has experienced a fall in net income. The reason depicted is the rise in operating

expenses. However, the accountants of the fund have manipulated the operating income figure to

show lower net income for distributing lower dividends to the shareholders (Mirabile 2016). As a

result, it has helped in minimising the overall ROCE for providing lower returns to the investors.

Liquidity ratios:

Particulars Details 2004 2005

Current assets A

17,29

9

15,21

8

Inventories B

8,90

8

8,96

9

Current

liabilities C

16,54

0

15,57

5

Current ratio A/C 1.05 0.98

Quick ratio

(A-

B)/C

0.5

1

0.4

0

Based on the above table, it could be found that the Bayou Hedge Fund Group had

experienced a fall in its liquidity position due to the fall in current assets significantly. In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING

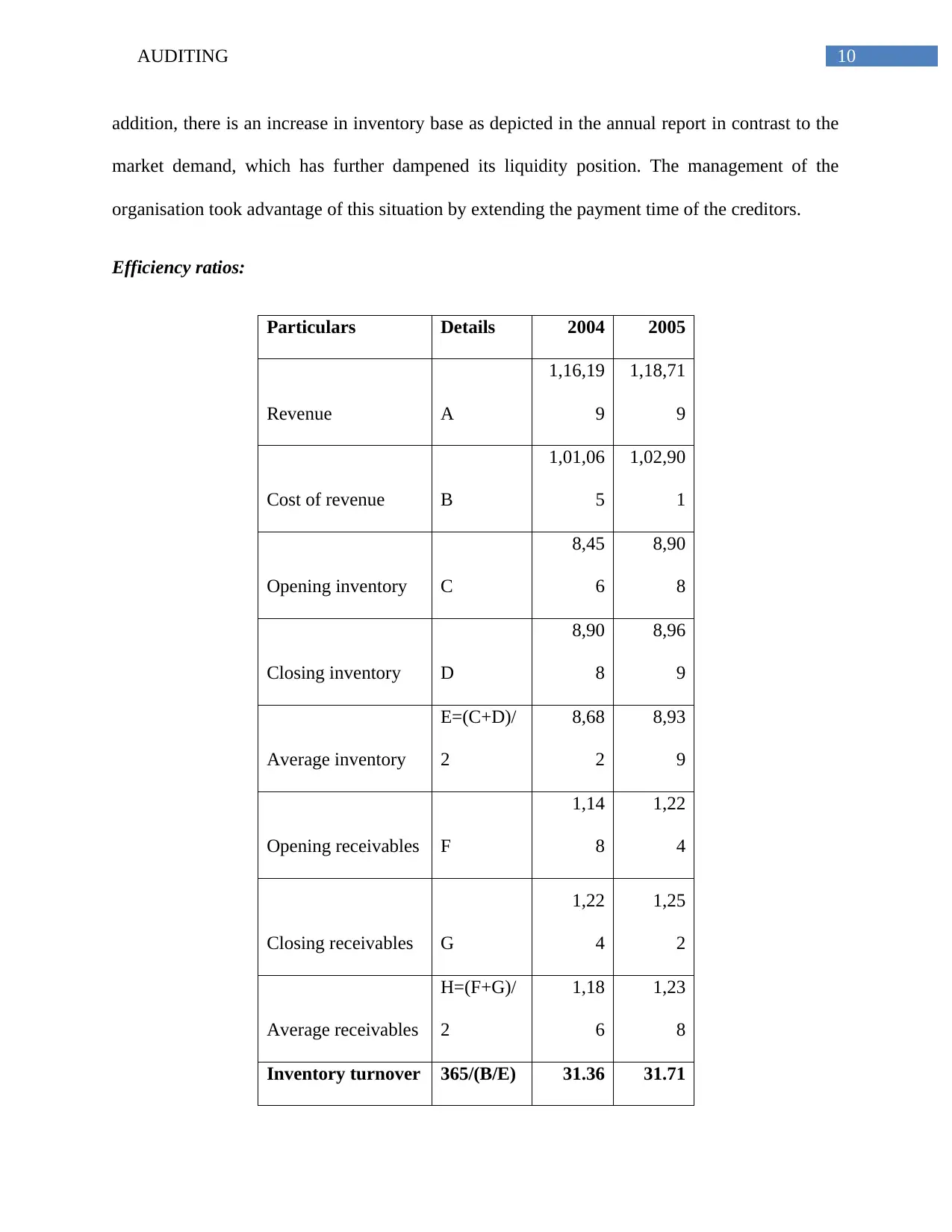

addition, there is an increase in inventory base as depicted in the annual report in contrast to the

market demand, which has further dampened its liquidity position. The management of the

organisation took advantage of this situation by extending the payment time of the creditors.

Efficiency ratios:

Particulars Details 2004 2005

Revenue A

1,16,19

9

1,18,71

9

Cost of revenue B

1,01,06

5

1,02,90

1

Opening inventory C

8,45

6

8,90

8

Closing inventory D

8,90

8

8,96

9

Average inventory

E=(C+D)/

2

8,68

2

8,93

9

Opening receivables F

1,14

8

1,22

4

Closing receivables G

1,22

4

1,25

2

Average receivables

H=(F+G)/

2

1,18

6

1,23

8

Inventory turnover 365/(B/E) 31.36 31.71

addition, there is an increase in inventory base as depicted in the annual report in contrast to the

market demand, which has further dampened its liquidity position. The management of the

organisation took advantage of this situation by extending the payment time of the creditors.

Efficiency ratios:

Particulars Details 2004 2005

Revenue A

1,16,19

9

1,18,71

9

Cost of revenue B

1,01,06

5

1,02,90

1

Opening inventory C

8,45

6

8,90

8

Closing inventory D

8,90

8

8,96

9

Average inventory

E=(C+D)/

2

8,68

2

8,93

9

Opening receivables F

1,14

8

1,22

4

Closing receivables G

1,22

4

1,25

2

Average receivables

H=(F+G)/

2

1,18

6

1,23

8

Inventory turnover 365/(B/E) 31.36 31.71

11AUDITING

Receivables

turnover 365/(A/H) 3.73 3.81

The above table clearly depicts that Bayou Hedge Fund Group had managed to increase

its inventory rate in 2005 by providing misleading information to the stakeholders. In addition,

the payment time of the debtors had been extremely low and this helped Mr. Israel to accumulate

sufficient amount of cash for conducting the fraudulent activity.

Investor ratios:

Particulars Details 2004 2005

Net income A

2,37

7

2,35

0

Opening

shareholders'

equity B

12,30

3

10,61

7

Closing

shareholders'

equity C

10,61

7

12,07

9

Average

shareholders'

equity

D=(B+C)/

2

11,46

0

11,34

8

Market price

per share E 29.38 36.78

Receivables

turnover 365/(A/H) 3.73 3.81

The above table clearly depicts that Bayou Hedge Fund Group had managed to increase

its inventory rate in 2005 by providing misleading information to the stakeholders. In addition,

the payment time of the debtors had been extremely low and this helped Mr. Israel to accumulate

sufficient amount of cash for conducting the fraudulent activity.

Investor ratios:

Particulars Details 2004 2005

Net income A

2,37

7

2,35

0

Opening

shareholders'

equity B

12,30

3

10,61

7

Closing

shareholders'

equity C

10,61

7

12,07

9

Average

shareholders'

equity

D=(B+C)/

2

11,46

0

11,34

8

Market price

per share E 29.38 36.78

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.