Fresnillo Plc: Assessment of Risk and Global Financial Strategies

VerifiedAdded on 2020/06/06

|27

|4334

|120

Report

AI Summary

This report offers a comprehensive analysis of Fresnillo Plc's financial strategy, focusing on risk management and global expansion. Part A examines key investment attractions in foreign countries like Indonesia, China, and Brazil, highlighting the benefits of economies of scale, skilled labor, and tax concessions. It then reviews Fresnillo's five-year performance across different geographic locations (Zacatecas, Durango, and Sonora), assessing revenue and profit trends to identify growth areas and potential risks. The report also explores how Fresnillo manages exchange rate, market, and commodity risks, with an analysis of GBP/MXN exchange rate fluctuations. Part B includes financial calculations related to net sterling receipts/payments and money market analysis. Overall, the report provides valuable insights into Fresnillo's financial performance, risk mitigation strategies, and future growth prospects within the precious metals mining industry. The competitor analysis included, compares Fresnillo with Barrick Gold Corporation and Dowa Holdings Co Ltd.

Fresnillo Risk & Global Financial Strategy

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART A...........................................................................................................................................3

INTRODUCTION...........................................................................................................................3

1. Assessing key attractions for Fresnillo investing in foreign countries....................................3

2. Reviewing 5 years trend of Fresnillo and presenting the areas of business which is likely to

grow.............................................................................................................................................4

3. Stating the manner in which company is managing its exchange, market and commodity

risk.............................................................................................................................................11

CONCLUSION..............................................................................................................................16

PART B.........................................................................................................................................16

a. Calculating net sterling receipts / payments..........................................................................16

2. Money market........................................................................................................................18

B.................................................................................................................................................19

b.................................................................................................................................................20

b: Computing forward and future value.....................................................................................20

REFERENCES..............................................................................................................................23

APPENDIX....................................................................................................................................25

1. Share prices of Fresnillo Plc..................................................................................................25

PART A...........................................................................................................................................3

INTRODUCTION...........................................................................................................................3

1. Assessing key attractions for Fresnillo investing in foreign countries....................................3

2. Reviewing 5 years trend of Fresnillo and presenting the areas of business which is likely to

grow.............................................................................................................................................4

3. Stating the manner in which company is managing its exchange, market and commodity

risk.............................................................................................................................................11

CONCLUSION..............................................................................................................................16

PART B.........................................................................................................................................16

a. Calculating net sterling receipts / payments..........................................................................16

2. Money market........................................................................................................................18

B.................................................................................................................................................19

b.................................................................................................................................................20

b: Computing forward and future value.....................................................................................20

REFERENCES..............................................................................................................................23

APPENDIX....................................................................................................................................25

1. Share prices of Fresnillo Plc..................................................................................................25

PART A

INTRODUCTION

In the present times, business units are encouraged to trade or perform activities at global

level with the motive to enhance customer base and profit margin. Hence, when business unit

operates globally then it has to face several risks in relation to exchange rate, commodity

fluctuations etc. In this, firm requires sound and strategic framework which provides assistance

to it in performing activities more effectually. Moreover, the main motive of company behind

global expansion is to enhance market share and profit margin. Thus, by preparing competent

framework company can make contribution in the attainment of goals. The present report is

based on Fresnillo Plc, Mexican company, which is one of the leading precious metal mining

firms incorporated in UK. Fresnillo has attained leading position in world under the category of

silver and gold mining. In this, report will shed light on the attraction points for Fresnillo in

relation to FDI. Besides this, it will also highlight the business segment of the company which is

highly growing. Along with this, report will provide deeper insight about how effectively

Fresnillo is managing risks.

1. Assessing key attractions for Fresnillo investing in foreign countries

From assessment, it has found that from investment perspective in the mining sector there

are several countries in which Fresnillo can invest such as Insdonesia, China, Brazil etc. All such

are the main countries in which Fresnillo can explore its business operations and functions.

When business unit expands its operations and functions at global level then it gets several

benefits in terms of high economies of scale, maximization of profitability, tax concessions and

availability of skilled personnel (Aliyu, Saleha, Jalila and Zunita, 2016). For mining activities

firm requires highly skilled and efficient individuals. Along with this, when business operates at

large level then it attains benefits in terms of cost reductions. All such aspects positively

contribute in the productivity and profitability aspect of firm. Countries which are recognized as

an attraction for foreign investment include following:

Indonesia: In Indonesia, political condition is highly stable which is one of the main

attraction point that entice foreign capital. Along with this, labour cost is also low in

INTRODUCTION

In the present times, business units are encouraged to trade or perform activities at global

level with the motive to enhance customer base and profit margin. Hence, when business unit

operates globally then it has to face several risks in relation to exchange rate, commodity

fluctuations etc. In this, firm requires sound and strategic framework which provides assistance

to it in performing activities more effectually. Moreover, the main motive of company behind

global expansion is to enhance market share and profit margin. Thus, by preparing competent

framework company can make contribution in the attainment of goals. The present report is

based on Fresnillo Plc, Mexican company, which is one of the leading precious metal mining

firms incorporated in UK. Fresnillo has attained leading position in world under the category of

silver and gold mining. In this, report will shed light on the attraction points for Fresnillo in

relation to FDI. Besides this, it will also highlight the business segment of the company which is

highly growing. Along with this, report will provide deeper insight about how effectively

Fresnillo is managing risks.

1. Assessing key attractions for Fresnillo investing in foreign countries

From assessment, it has found that from investment perspective in the mining sector there

are several countries in which Fresnillo can invest such as Insdonesia, China, Brazil etc. All such

are the main countries in which Fresnillo can explore its business operations and functions.

When business unit expands its operations and functions at global level then it gets several

benefits in terms of high economies of scale, maximization of profitability, tax concessions and

availability of skilled personnel (Aliyu, Saleha, Jalila and Zunita, 2016). For mining activities

firm requires highly skilled and efficient individuals. Along with this, when business operates at

large level then it attains benefits in terms of cost reductions. All such aspects positively

contribute in the productivity and profitability aspect of firm. Countries which are recognized as

an attraction for foreign investment include following:

Indonesia: In Indonesia, political condition is highly stable which is one of the main

attraction point that entice foreign capital. Along with this, labour cost is also low in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Indonesia which in turn places direct impact on profitability aspects in a positive manner.

Thus, by considering such aspects, it can be said that for the purpose of better mining and

maximizing profitability aspect Fresnillo should focus on expanding business operations

in such country.

China: From research, it has been asserted that China is number one producer of gold in

the world. Further, cost of labour is low in China as compared to other countries and it

also has identified that economy of China will grow by 6.5% in the year of 2017. Cost is

one of the main factors that place significant impact on the profit margin of firm. On the

basis of such aspect, by employing skilled and low salaries workers Fresnillo can gain

benefits in monetary terms.

Brazil: Mining sector of Brazil has made significant contribution in the economic growth

and development (What drives the price of gold?, 2017). Forecasted results or estimations

show that GDP of Brazil will increase or grow by 2.2% at the end of 2018. Along with

this, Brazil provides investors with easy access pertaining to raw material. Further,

diversified economy exists in such country which in turn less vulnerable to international

monetary crisis.

By taking into account all the above mentioned aspects it can be stated that through investing

money in the countries like Brazil, China and Indonesia firm can get benefit in term of both

financial as well as non-financial.

2. Reviewing 5 years trend of Fresnillo and presenting the areas of business which is likely to

grow

Financial evaluation as per geographic location and business segment: On the basis of

cited case situation, turnover and profitability aspect of each location has been evaluated with the

motive to assess risk as well as business area which is highly growing. Such assessment is highly

significant which in turn provides deeper insight about the business entity about the area which is

contributing in organizational profitability (Allen, Macalady, Chenchouni, Bachelet, McDowell,

Vennetier, Kitzberger, Rigling, Breshears, Hogg and Gonzalez, 2010). Besides this, such

evaluation also clearly indicates the areas of business that impose risk in front of Fresnillon in

both monetary and non-monetary aspects. On the basis of geographic location aspects firm is

operated in Zacatecas, Durango, aned Sonora.

Thus, by considering such aspects, it can be said that for the purpose of better mining and

maximizing profitability aspect Fresnillo should focus on expanding business operations

in such country.

China: From research, it has been asserted that China is number one producer of gold in

the world. Further, cost of labour is low in China as compared to other countries and it

also has identified that economy of China will grow by 6.5% in the year of 2017. Cost is

one of the main factors that place significant impact on the profit margin of firm. On the

basis of such aspect, by employing skilled and low salaries workers Fresnillo can gain

benefits in monetary terms.

Brazil: Mining sector of Brazil has made significant contribution in the economic growth

and development (What drives the price of gold?, 2017). Forecasted results or estimations

show that GDP of Brazil will increase or grow by 2.2% at the end of 2018. Along with

this, Brazil provides investors with easy access pertaining to raw material. Further,

diversified economy exists in such country which in turn less vulnerable to international

monetary crisis.

By taking into account all the above mentioned aspects it can be stated that through investing

money in the countries like Brazil, China and Indonesia firm can get benefit in term of both

financial as well as non-financial.

2. Reviewing 5 years trend of Fresnillo and presenting the areas of business which is likely to

grow

Financial evaluation as per geographic location and business segment: On the basis of

cited case situation, turnover and profitability aspect of each location has been evaluated with the

motive to assess risk as well as business area which is highly growing. Such assessment is highly

significant which in turn provides deeper insight about the business entity about the area which is

contributing in organizational profitability (Allen, Macalady, Chenchouni, Bachelet, McDowell,

Vennetier, Kitzberger, Rigling, Breshears, Hogg and Gonzalez, 2010). Besides this, such

evaluation also clearly indicates the areas of business that impose risk in front of Fresnillon in

both monetary and non-monetary aspects. On the basis of geographic location aspects firm is

operated in Zacatecas, Durango, aned Sonora.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

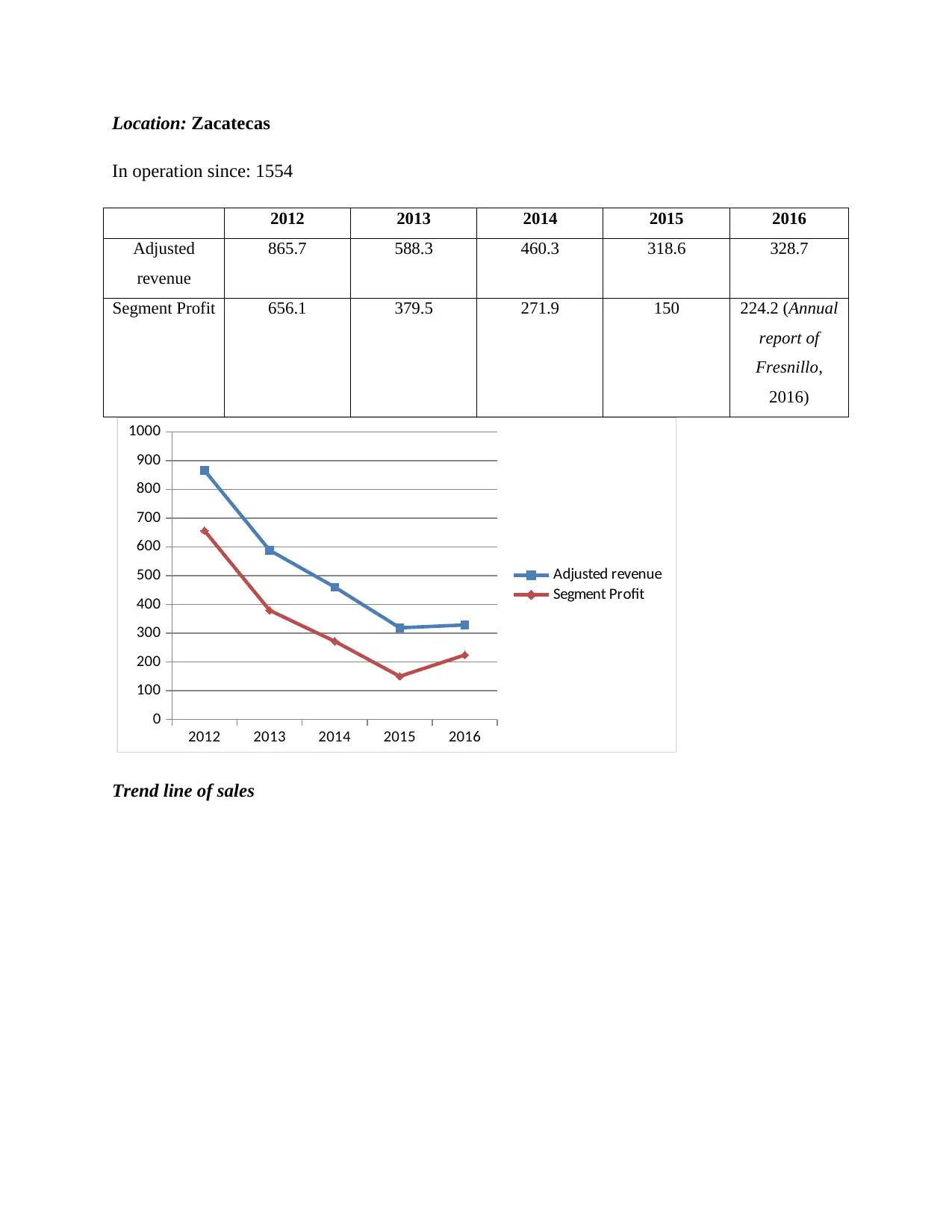

Location: Zacatecas

In operation since: 1554

2012 2013 2014 2015 2016

Adjusted

revenue

865.7 588.3 460.3 318.6 328.7

Segment Profit 656.1 379.5 271.9 150 224.2 (Annual

report of

Fresnillo,

2016)

2012 2013 2014 2015 2016

0

100

200

300

400

500

600

700

800

900

1000

Adjusted revenue

Segment Profit

Trend line of sales

In operation since: 1554

2012 2013 2014 2015 2016

Adjusted

revenue

865.7 588.3 460.3 318.6 328.7

Segment Profit 656.1 379.5 271.9 150 224.2 (Annual

report of

Fresnillo,

2016)

2012 2013 2014 2015 2016

0

100

200

300

400

500

600

700

800

900

1000

Adjusted revenue

Segment Profit

Trend line of sales

2012 2013 2014 2015 2016

0

100

200

300

400

500

600

700

800

900

1000

f(x) = − 134.37 x + 915.43

Adjusted revenue

Adjusted revenue

Linear (Adjusted revenue)

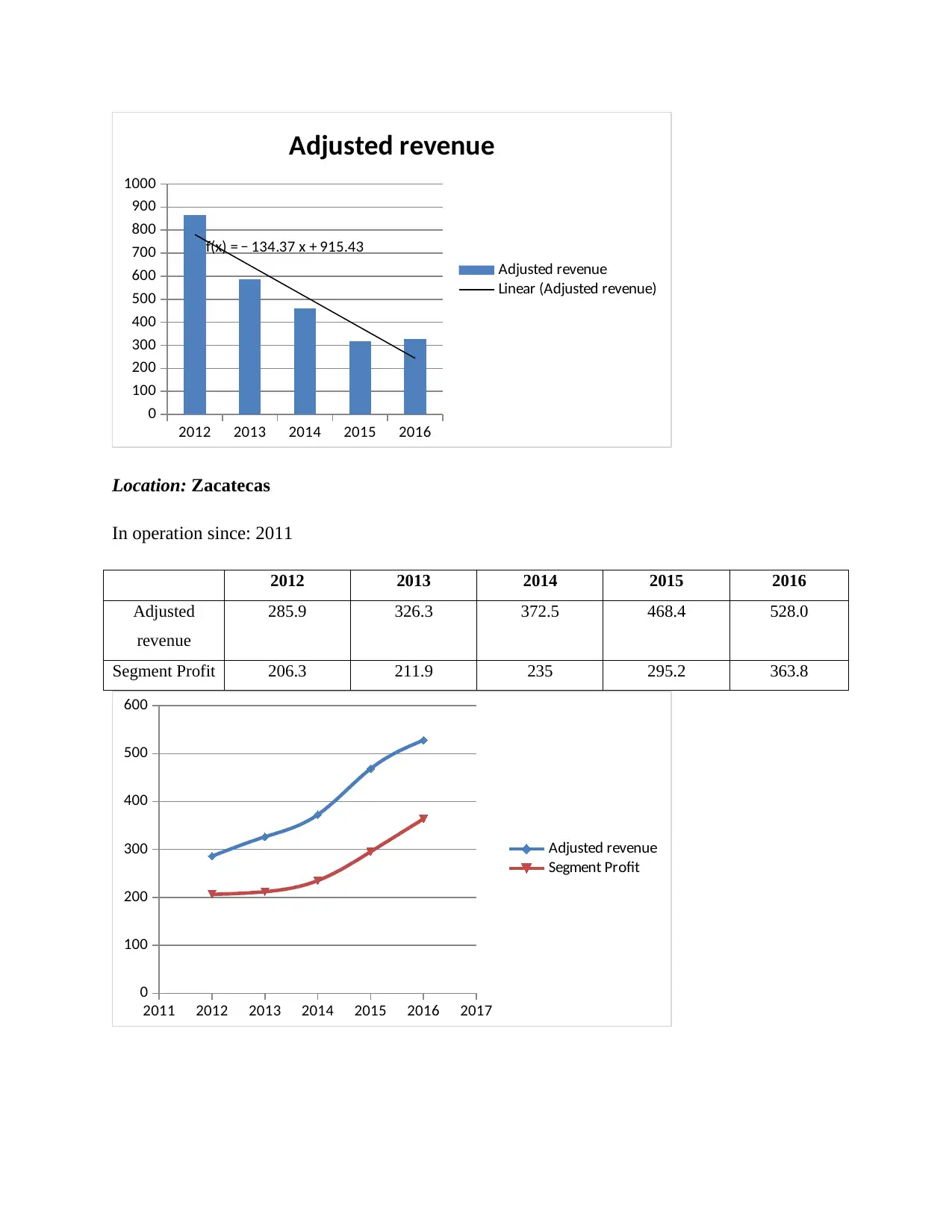

Location: Zacatecas

In operation since: 2011

2012 2013 2014 2015 2016

Adjusted

revenue

285.9 326.3 372.5 468.4 528.0

Segment Profit 206.3 211.9 235 295.2 363.8

2011 2012 2013 2014 2015 2016 2017

0

100

200

300

400

500

600

Adjusted revenue

Segment Profit

0

100

200

300

400

500

600

700

800

900

1000

f(x) = − 134.37 x + 915.43

Adjusted revenue

Adjusted revenue

Linear (Adjusted revenue)

Location: Zacatecas

In operation since: 2011

2012 2013 2014 2015 2016

Adjusted

revenue

285.9 326.3 372.5 468.4 528.0

Segment Profit 206.3 211.9 235 295.2 363.8

2011 2012 2013 2014 2015 2016 2017

0

100

200

300

400

500

600

Adjusted revenue

Segment Profit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2012 2013 2014 2015 2016

0

100

200

300

400

500

600

f(x) = 62.63 x + 208.33

Adjusted revenue

Adjusted revenue

Linear (Adjusted revenue)

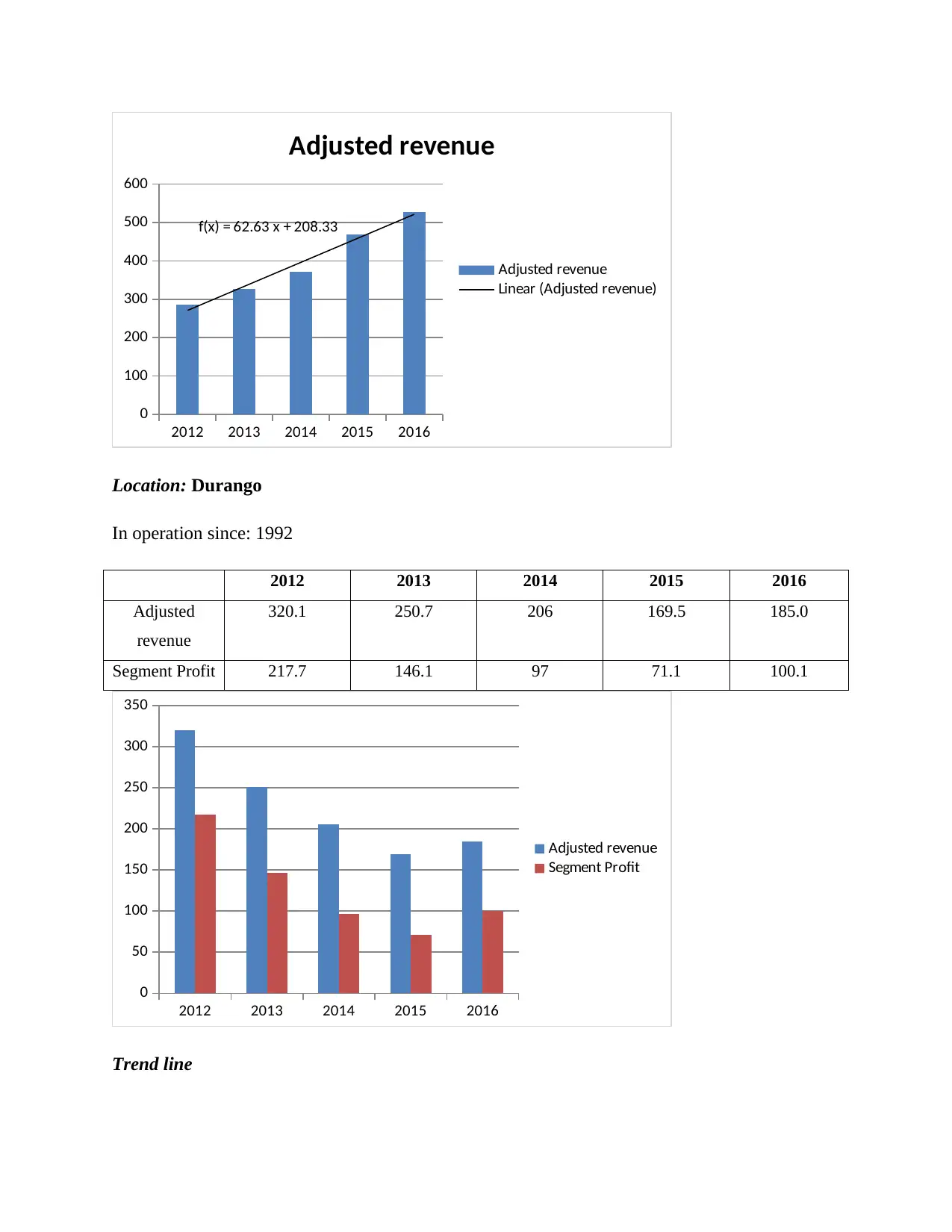

Location: Durango

In operation since: 1992

2012 2013 2014 2015 2016

Adjusted

revenue

320.1 250.7 206 169.5 185.0

Segment Profit 217.7 146.1 97 71.1 100.1

2012 2013 2014 2015 2016

0

50

100

150

200

250

300

350

Adjusted revenue

Segment Profit

Trend line

0

100

200

300

400

500

600

f(x) = 62.63 x + 208.33

Adjusted revenue

Adjusted revenue

Linear (Adjusted revenue)

Location: Durango

In operation since: 1992

2012 2013 2014 2015 2016

Adjusted

revenue

320.1 250.7 206 169.5 185.0

Segment Profit 217.7 146.1 97 71.1 100.1

2012 2013 2014 2015 2016

0

50

100

150

200

250

300

350

Adjusted revenue

Segment Profit

Trend line

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2012 2013 2014 2015 2016

0

50

100

150

200

250

300

350

f(x) = − 35.14 x + 331.68

Adjusted revenue

Adjusted revenue

Linear (Adjusted revenue)

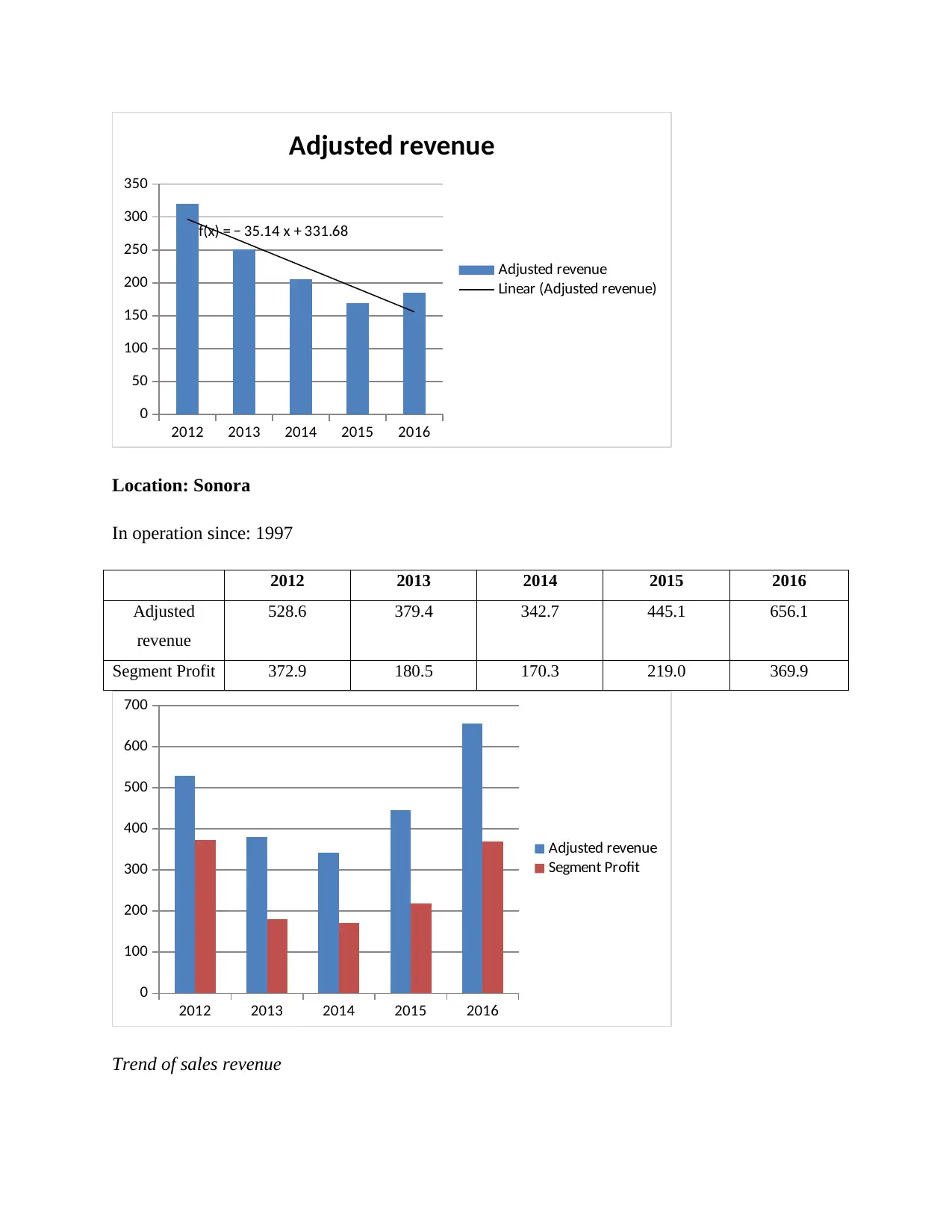

Location: Sonora

In operation since: 1997

2012 2013 2014 2015 2016

Adjusted

revenue

528.6 379.4 342.7 445.1 656.1

Segment Profit 372.9 180.5 170.3 219.0 369.9

2012 2013 2014 2015 2016

0

100

200

300

400

500

600

700

Adjusted revenue

Segment Profit

Trend of sales revenue

0

50

100

150

200

250

300

350

f(x) = − 35.14 x + 331.68

Adjusted revenue

Adjusted revenue

Linear (Adjusted revenue)

Location: Sonora

In operation since: 1997

2012 2013 2014 2015 2016

Adjusted

revenue

528.6 379.4 342.7 445.1 656.1

Segment Profit 372.9 180.5 170.3 219.0 369.9

2012 2013 2014 2015 2016

0

100

200

300

400

500

600

700

Adjusted revenue

Segment Profit

Trend of sales revenue

2012 2013 2014 2015 2016

0

100

200

300

400

500

600

700

f(x) = 32.07 x + 374.17

Adjusted revenue

Adjusted revenue

Linear (Adjusted revenue)

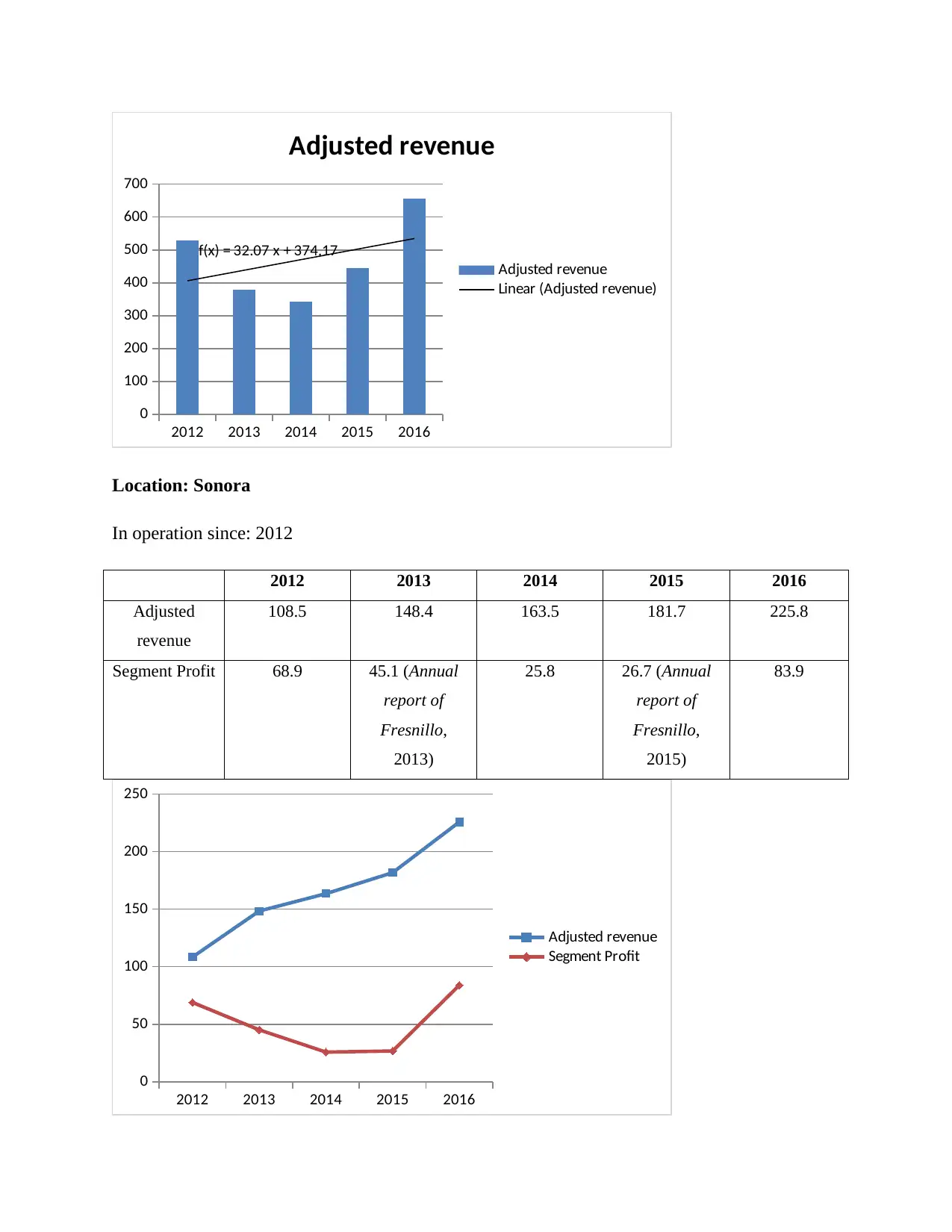

Location: Sonora

In operation since: 2012

2012 2013 2014 2015 2016

Adjusted

revenue

108.5 148.4 163.5 181.7 225.8

Segment Profit 68.9 45.1 (Annual

report of

Fresnillo,

2013)

25.8 26.7 (Annual

report of

Fresnillo,

2015)

83.9

2012 2013 2014 2015 2016

0

50

100

150

200

250

Adjusted revenue

Segment Profit

0

100

200

300

400

500

600

700

f(x) = 32.07 x + 374.17

Adjusted revenue

Adjusted revenue

Linear (Adjusted revenue)

Location: Sonora

In operation since: 2012

2012 2013 2014 2015 2016

Adjusted

revenue

108.5 148.4 163.5 181.7 225.8

Segment Profit 68.9 45.1 (Annual

report of

Fresnillo,

2013)

25.8 26.7 (Annual

report of

Fresnillo,

2015)

83.9

2012 2013 2014 2015 2016

0

50

100

150

200

250

Adjusted revenue

Segment Profit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

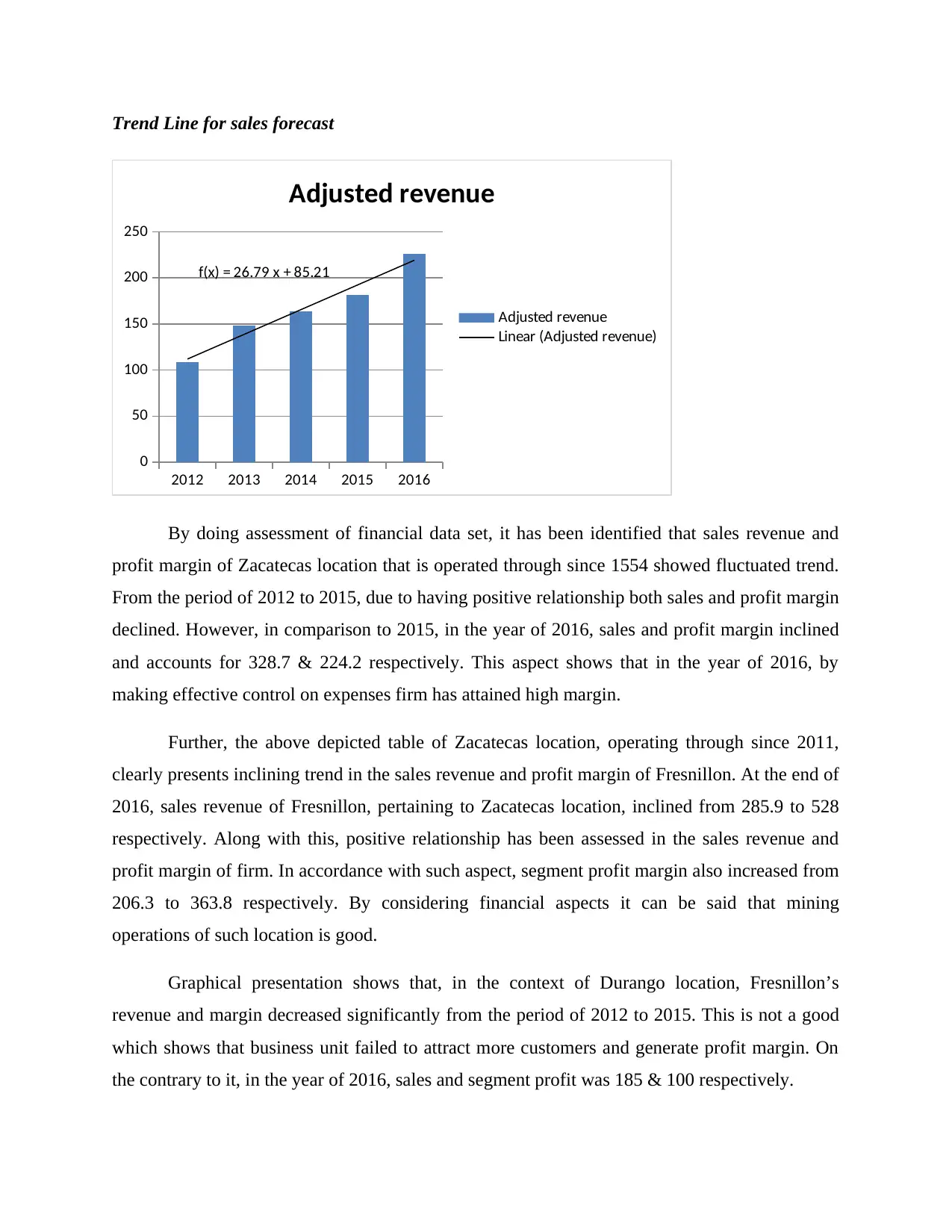

Trend Line for sales forecast

2012 2013 2014 2015 2016

0

50

100

150

200

250

f(x) = 26.79 x + 85.21

Adjusted revenue

Adjusted revenue

Linear (Adjusted revenue)

By doing assessment of financial data set, it has been identified that sales revenue and

profit margin of Zacatecas location that is operated through since 1554 showed fluctuated trend.

From the period of 2012 to 2015, due to having positive relationship both sales and profit margin

declined. However, in comparison to 2015, in the year of 2016, sales and profit margin inclined

and accounts for 328.7 & 224.2 respectively. This aspect shows that in the year of 2016, by

making effective control on expenses firm has attained high margin.

Further, the above depicted table of Zacatecas location, operating through since 2011,

clearly presents inclining trend in the sales revenue and profit margin of Fresnillon. At the end of

2016, sales revenue of Fresnillon, pertaining to Zacatecas location, inclined from 285.9 to 528

respectively. Along with this, positive relationship has been assessed in the sales revenue and

profit margin of firm. In accordance with such aspect, segment profit margin also increased from

206.3 to 363.8 respectively. By considering financial aspects it can be said that mining

operations of such location is good.

Graphical presentation shows that, in the context of Durango location, Fresnillon’s

revenue and margin decreased significantly from the period of 2012 to 2015. This is not a good

which shows that business unit failed to attract more customers and generate profit margin. On

the contrary to it, in the year of 2016, sales and segment profit was 185 & 100 respectively.

2012 2013 2014 2015 2016

0

50

100

150

200

250

f(x) = 26.79 x + 85.21

Adjusted revenue

Adjusted revenue

Linear (Adjusted revenue)

By doing assessment of financial data set, it has been identified that sales revenue and

profit margin of Zacatecas location that is operated through since 1554 showed fluctuated trend.

From the period of 2012 to 2015, due to having positive relationship both sales and profit margin

declined. However, in comparison to 2015, in the year of 2016, sales and profit margin inclined

and accounts for 328.7 & 224.2 respectively. This aspect shows that in the year of 2016, by

making effective control on expenses firm has attained high margin.

Further, the above depicted table of Zacatecas location, operating through since 2011,

clearly presents inclining trend in the sales revenue and profit margin of Fresnillon. At the end of

2016, sales revenue of Fresnillon, pertaining to Zacatecas location, inclined from 285.9 to 528

respectively. Along with this, positive relationship has been assessed in the sales revenue and

profit margin of firm. In accordance with such aspect, segment profit margin also increased from

206.3 to 363.8 respectively. By considering financial aspects it can be said that mining

operations of such location is good.

Graphical presentation shows that, in the context of Durango location, Fresnillon’s

revenue and margin decreased significantly from the period of 2012 to 2015. This is not a good

which shows that business unit failed to attract more customers and generate profit margin. On

the contrary to it, in the year of 2016, sales and segment profit was 185 & 100 respectively.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Annual reports of Fresnillon, from the period of 2012 to 2016, exhibits fluctuated trend in

both sales as well as profit margin of Sonora location, operating from since 1997. During the

time period of 5 years, performance of Fresnillon’s was good in financial terms in 2012 & 2016.

In the middle years such as 2013, 2014 & 2015, business unit failed to generate enough and high

margin due to increasing cost and decreasing revenue.

By doing assessment of financial statements, it has been identified that sales and profit

margin of Sonora location, which is operating from since 2012, increased significantly over the

years. This aspect indicates that business unit has exerted effectual control on cost and thereby

generated high margin.

Conclusive section: Considering the overall assessment, it can be presented that sales and

profitability of Fresnillon’s different locations such as Zacatecas (2011), Sonora (1997) and

Sonora (2012) is growing. Hence, by developing sound framework business unit can maximize

the level of both sales and profit margin. Thus, by exploring business at such location firm can

get the desired level of outcome or success. On the other side, financial performance of locations

such as Zacatecas (1554), Durango (1992), are imposing high level of risk in front of Fresnillon.

Moreover, decreasing trend of sales and profit shows management at such locations are not good.

Thus, business unit is required to identify the causes due to which at such location firm failed to

achieve objectives. By doing this, firm would become able to develop suitable strategies as well

as policies and thereby would become able to gain competitive edge over others.

Competitor analysis

Basis of difference Fresnillo Plc Barrick Gold

Corporation

Dowa Holdings Co

Ltd

Products It offers precious metals

to the customers.

Product portfolio of

Barrick Corporation

includes gold, silver and

copper.

It provides customers

with nonferrous metals

and electronic materials.

Revenue (2016 and in

millions)

1906 US $ 8588 US $ 406,598 JPY

both sales as well as profit margin of Sonora location, operating from since 1997. During the

time period of 5 years, performance of Fresnillon’s was good in financial terms in 2012 & 2016.

In the middle years such as 2013, 2014 & 2015, business unit failed to generate enough and high

margin due to increasing cost and decreasing revenue.

By doing assessment of financial statements, it has been identified that sales and profit

margin of Sonora location, which is operating from since 2012, increased significantly over the

years. This aspect indicates that business unit has exerted effectual control on cost and thereby

generated high margin.

Conclusive section: Considering the overall assessment, it can be presented that sales and

profitability of Fresnillon’s different locations such as Zacatecas (2011), Sonora (1997) and

Sonora (2012) is growing. Hence, by developing sound framework business unit can maximize

the level of both sales and profit margin. Thus, by exploring business at such location firm can

get the desired level of outcome or success. On the other side, financial performance of locations

such as Zacatecas (1554), Durango (1992), are imposing high level of risk in front of Fresnillon.

Moreover, decreasing trend of sales and profit shows management at such locations are not good.

Thus, business unit is required to identify the causes due to which at such location firm failed to

achieve objectives. By doing this, firm would become able to develop suitable strategies as well

as policies and thereby would become able to gain competitive edge over others.

Competitor analysis

Basis of difference Fresnillo Plc Barrick Gold

Corporation

Dowa Holdings Co

Ltd

Products It offers precious metals

to the customers.

Product portfolio of

Barrick Corporation

includes gold, silver and

copper.

It provides customers

with nonferrous metals

and electronic materials.

Revenue (2016 and in

millions)

1906 US $ 8588 US $ 406,598 JPY

Net income (2016 and

in millions)

427 US $ 655 US $ 21826 JPY

Pricing strategies Company employ either

competitive or

penetration pricing on

the basis of situation.

Competitive pricing Same as Barrick Co.

3. Stating the manner in which company is managing its exchange, market and commodity risk

Exchange rate risk: For assessing the risk level in relation to exchange rates such as

British Pound Mexican Peso has been evaluated. Moreover, main countries in which

Fresnillo operates include Mexico and UK. By taking into account such aspect

fluctuations pertaining to currency level has been evaluated. The below depicted table

presents that standard deviation in relation to the concerned currency accounts for 2.07

respectively. As compared to the global recessionary period and after such condition

fluctuation with takes place in exchange rate were not high. In accordance with all such

aspects, it can be presented that exchange rate does not impose high level of risk in front

of firm. Besides this, for dealing with the future exchange risk Fresnillo is required to lay

emphasis on undertaking derivative instruments. This in turn helps business unit in

hedging the risk in an effectual way. Moreover, foreign exchange market is uncertain and

it has direct impact on the financial aspects of firm. In this regard, by making focus on

undertaking derivative tools business unit can mitigate foreign exchange risk to a great

extent.

Date Price

17-Nov 25.29

17-Oct 25.44

17-Sep 24.46

17-Aug 23.13

17-Jul 23.52

17-Jun 23.62

17-May 24.00

17-Apr 24.37

in millions)

427 US $ 655 US $ 21826 JPY

Pricing strategies Company employ either

competitive or

penetration pricing on

the basis of situation.

Competitive pricing Same as Barrick Co.

3. Stating the manner in which company is managing its exchange, market and commodity risk

Exchange rate risk: For assessing the risk level in relation to exchange rates such as

British Pound Mexican Peso has been evaluated. Moreover, main countries in which

Fresnillo operates include Mexico and UK. By taking into account such aspect

fluctuations pertaining to currency level has been evaluated. The below depicted table

presents that standard deviation in relation to the concerned currency accounts for 2.07

respectively. As compared to the global recessionary period and after such condition

fluctuation with takes place in exchange rate were not high. In accordance with all such

aspects, it can be presented that exchange rate does not impose high level of risk in front

of firm. Besides this, for dealing with the future exchange risk Fresnillo is required to lay

emphasis on undertaking derivative instruments. This in turn helps business unit in

hedging the risk in an effectual way. Moreover, foreign exchange market is uncertain and

it has direct impact on the financial aspects of firm. In this regard, by making focus on

undertaking derivative tools business unit can mitigate foreign exchange risk to a great

extent.

Date Price

17-Nov 25.29

17-Oct 25.44

17-Sep 24.46

17-Aug 23.13

17-Jul 23.52

17-Jun 23.62

17-May 24.00

17-Apr 24.37

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.