Comprehensive Analysis of Partnership Taxation and Fringe Benefit Tax

VerifiedAdded on 2019/09/30

|8

|1766

|213

Homework Assignment

AI Summary

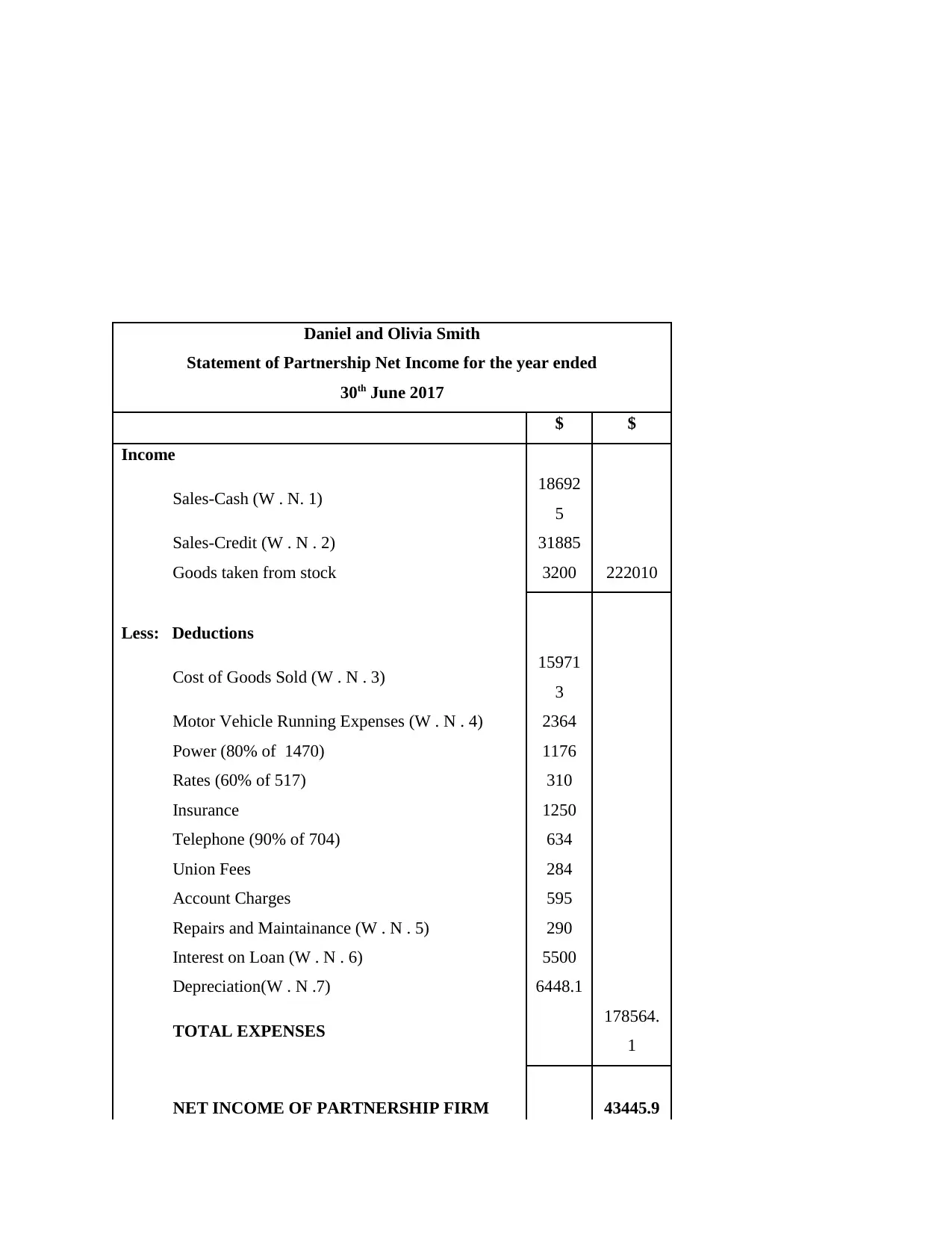

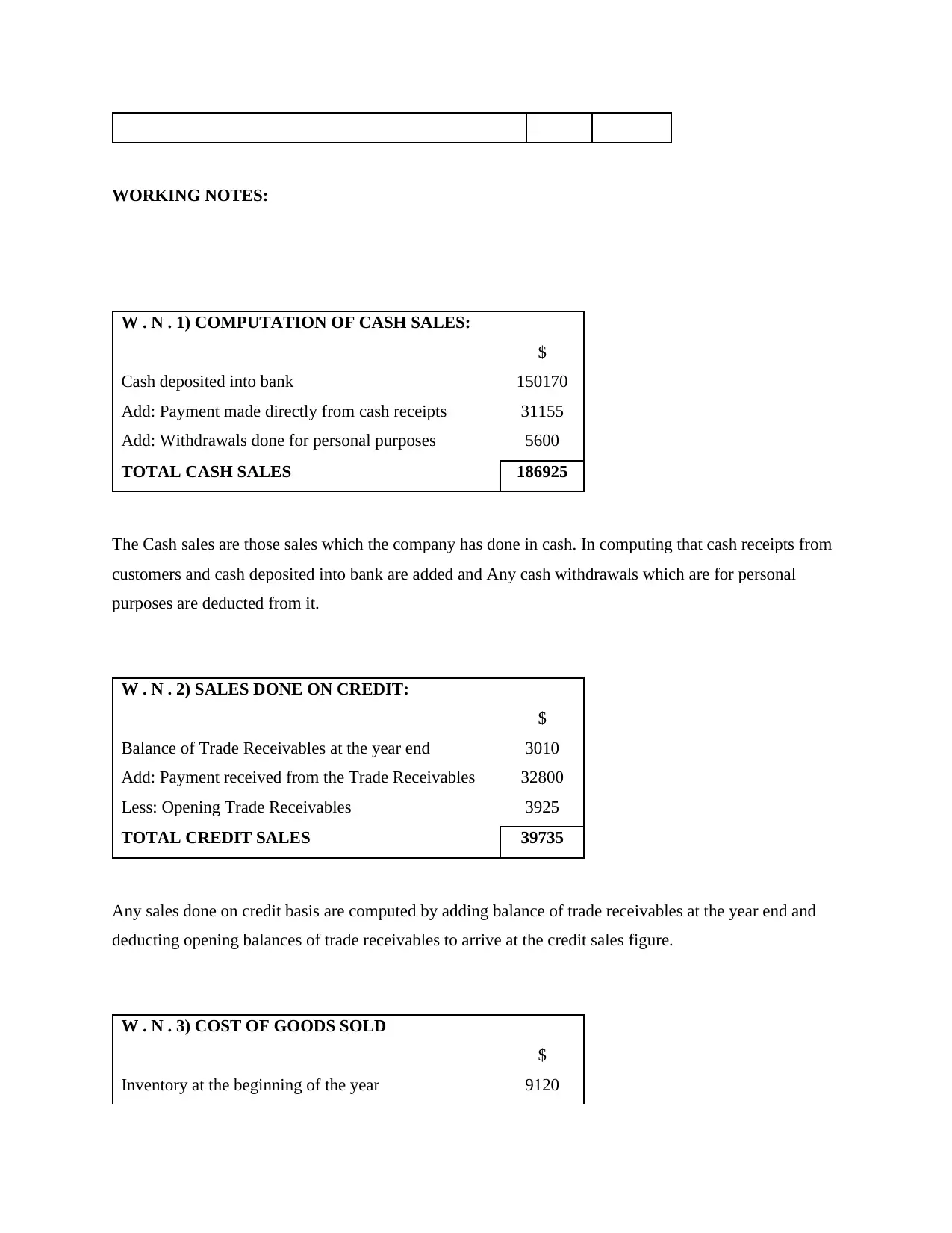

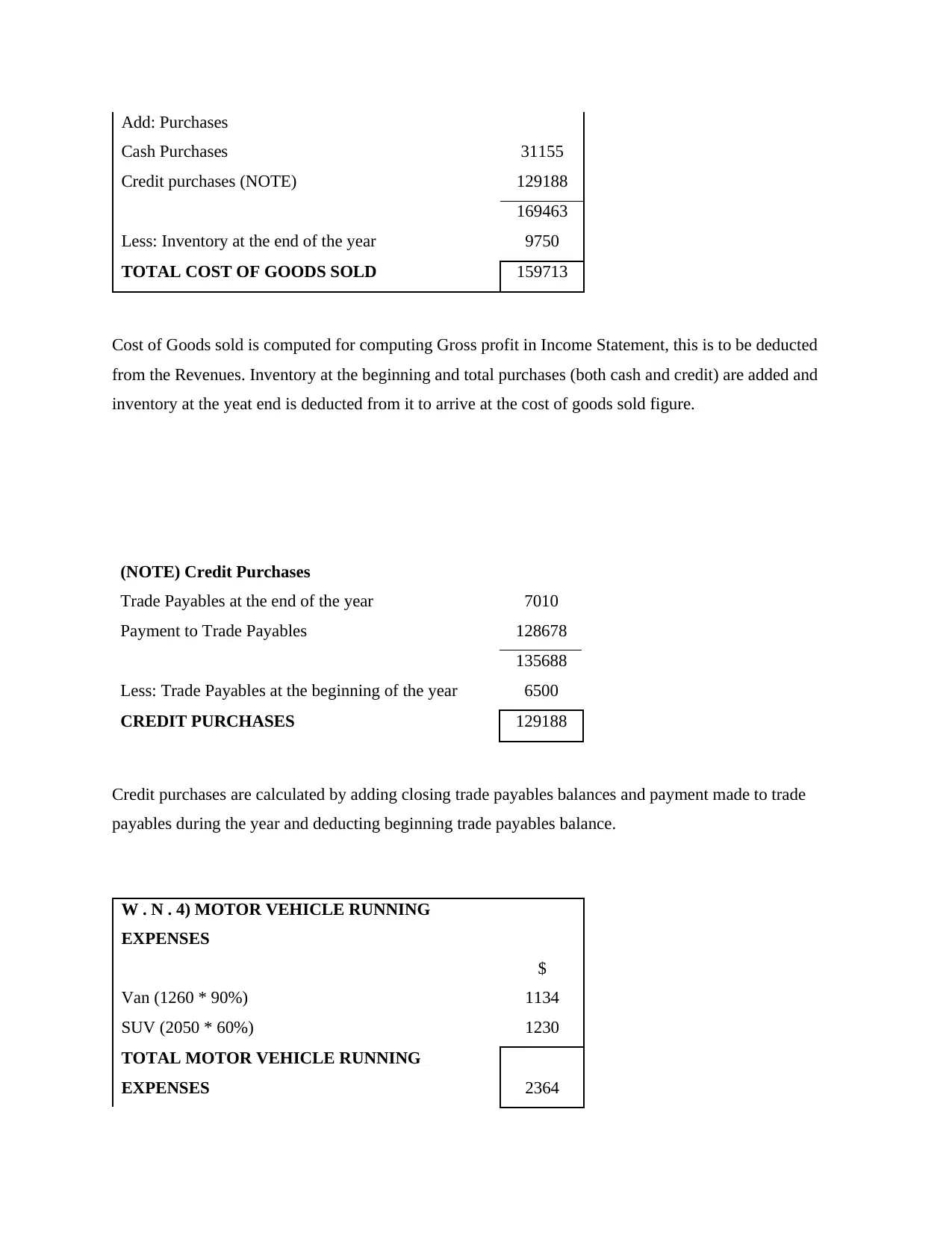

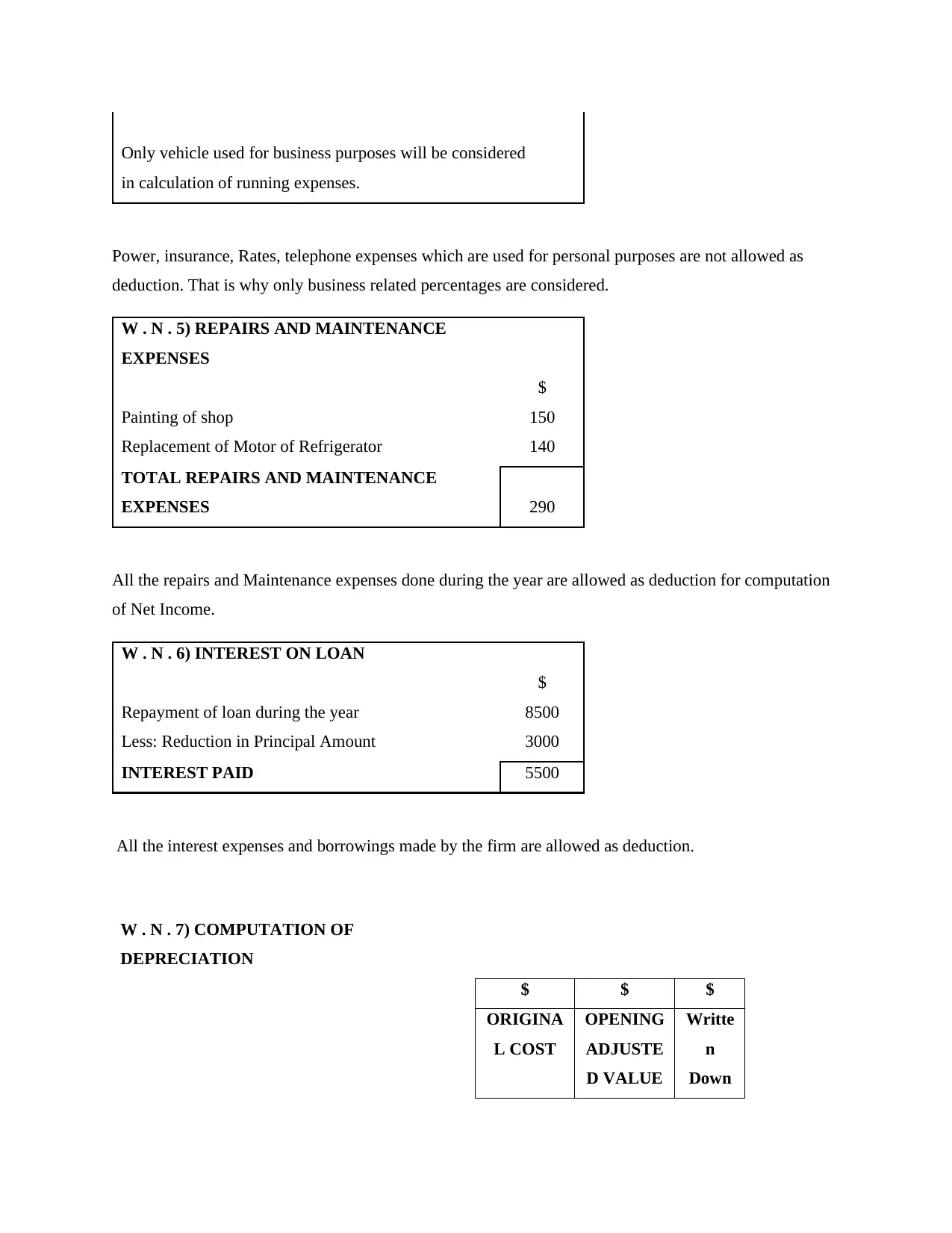

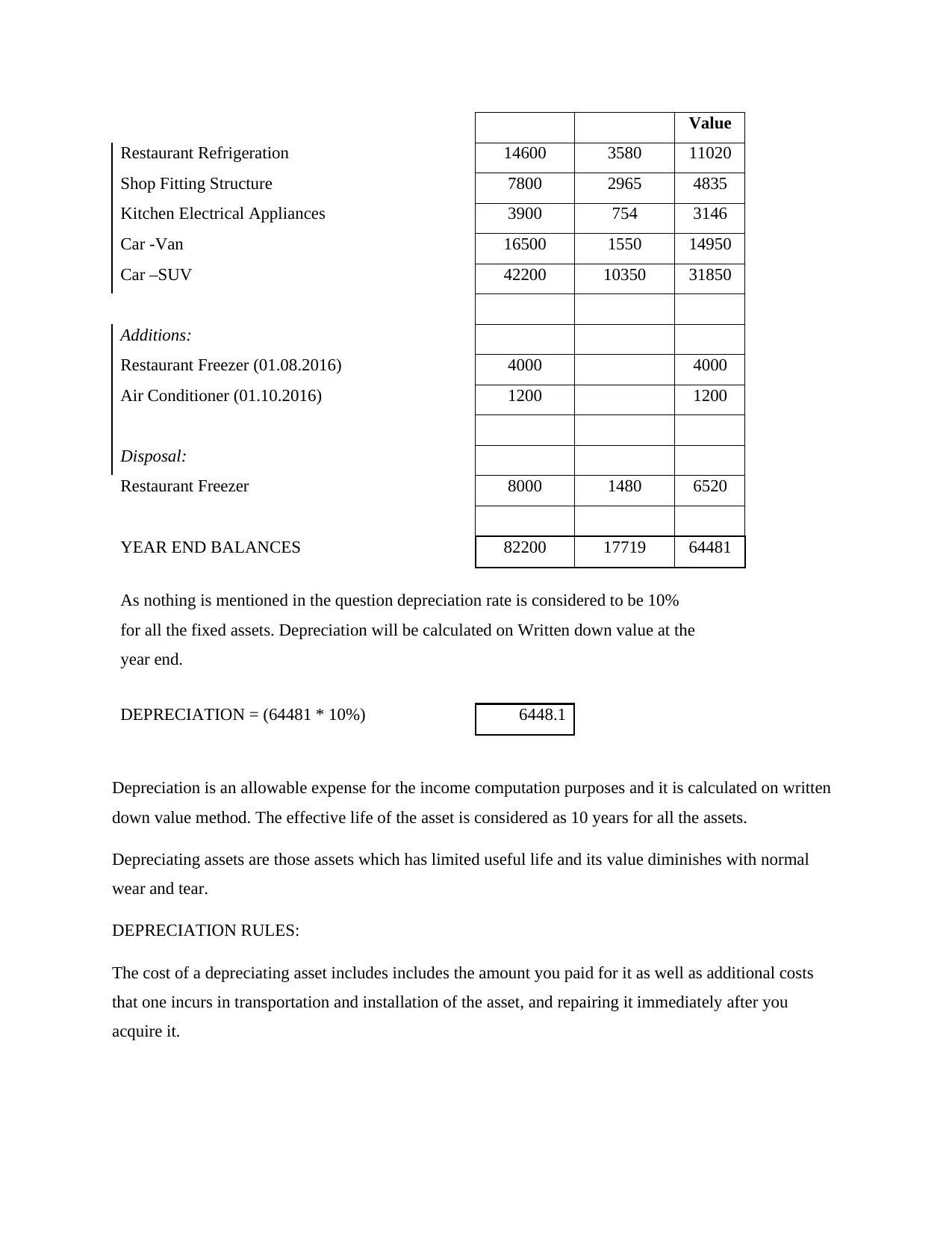

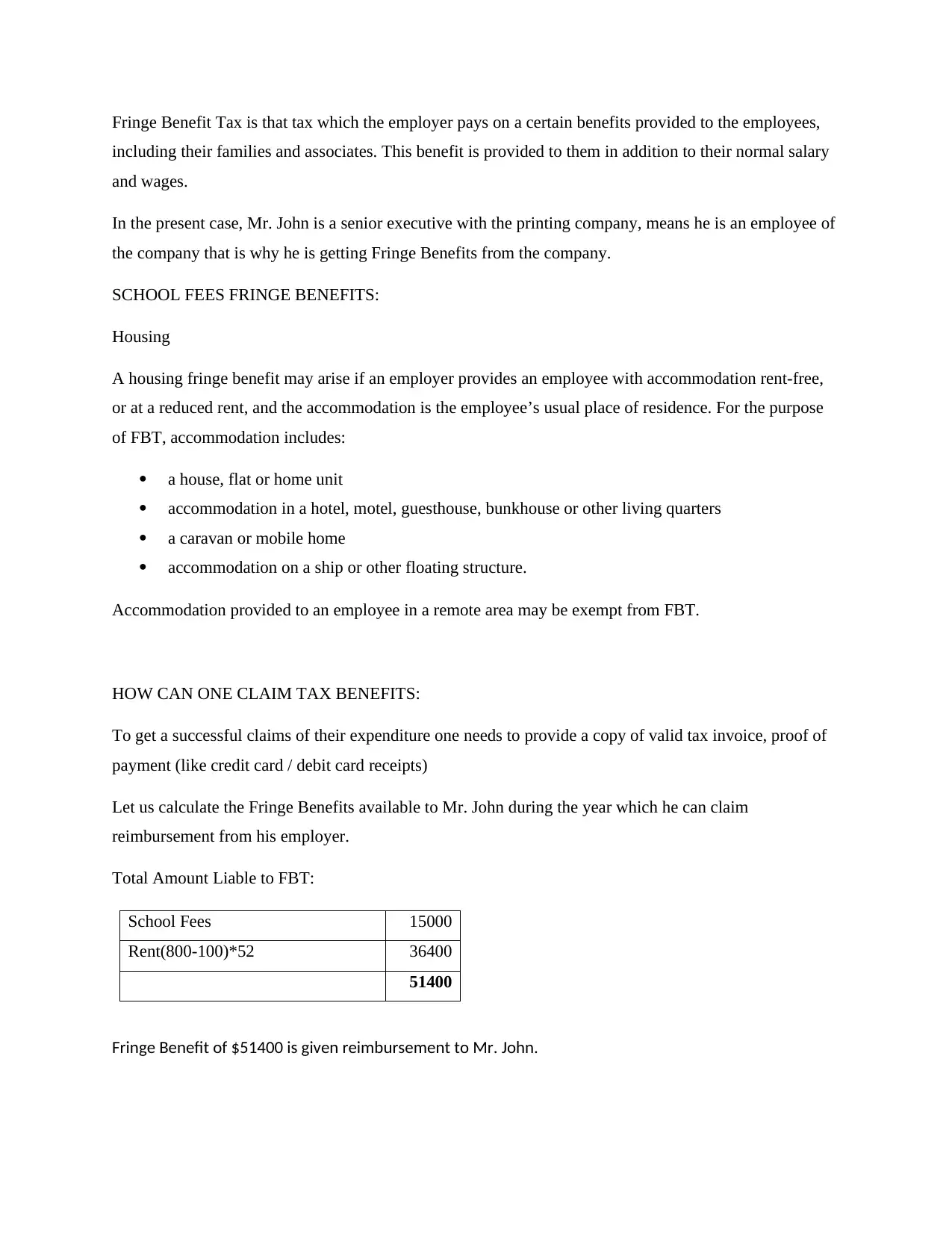

This assignment provides a comprehensive analysis of partnership taxation and fringe benefit tax (FBT). It begins with a detailed income statement for a partnership firm, calculating net income by considering various revenue streams, deductions such as cost of goods sold, motor vehicle expenses, power, rates, insurance, telephone, union fees, account charges, repairs and maintenance, interest on loans, and depreciation. The assignment includes detailed working notes for each calculation, such as cash and credit sales, cost of goods sold, and depreciation calculations. The second part of the assignment focuses on FBT, specifically analyzing benefits provided to a senior executive, Mr. John, including school fees and rent. It calculates the total amount liable for FBT, providing a clear understanding of how fringe benefits are taxed. The assignment references relevant tax resources and provides a practical application of tax principles in a business context. This assignment is valuable for students studying finance and taxation, offering practical insights into financial statement analysis and fringe benefit tax calculations. The assignment showcases how to calculate net income, cost of goods sold, and depreciation and how to determine FBT liabilities. The assignment concludes with a detailed discussion of the various aspects of taxation and how they affect businesses and employees.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.