TAXATION 1: Analysis of Fringe Benefits and Income Tax in Australia

VerifiedAdded on 2020/05/16

|12

|2474

|56

Report

AI Summary

This report provides a comprehensive analysis of fringe benefits and income tax in Australia, addressing key concepts and practical applications. The report begins by defining fringe benefits, emphasizing the relationship between employers and employees, and specifically focuses on car fringe benefits under the Fringe Benefit Tax Assessment Act 1986. It outlines the statutory and operating cost methods for assessing fringe benefit tax, comparing their methodologies and implications. The report then delves into a case study involving Allan and Betty, evaluating their income tax liabilities, including the tax implications of gifts, wine bottles, and the distinction between hobbies and businesses as per the Taxation Ruling TR 97/11. The analysis extends to the concept of barter systems and their treatment under the Income Tax Assessment Act 1997, including the application of GST. The report concludes by discussing the assessment of tax liabilities within the barter system and its similarities to cash and credit systems.

Running head: TAXATION

Taxation

Name of the student:

Name of the university:

Author note

Taxation

Name of the student:

Name of the university:

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION

Table of Contents

Answer to question 1..................................................................................................................2

Answer to question 2..................................................................................................................6

Part (a) answer:.......................................................................................................................6

Part (b) answer:.......................................................................................................................7

Part (c) answer:.......................................................................................................................8

Part (d) answer:.......................................................................................................................9

Reference:................................................................................................................................10

Table of Contents

Answer to question 1..................................................................................................................2

Answer to question 2..................................................................................................................6

Part (a) answer:.......................................................................................................................6

Part (b) answer:.......................................................................................................................7

Part (c) answer:.......................................................................................................................8

Part (d) answer:.......................................................................................................................9

Reference:................................................................................................................................10

2TAXATION

Answer to question 1

The term Fringe benefit can be defined as an additional amount that can be

provided to the employee or to the worker except their salary or remuneration. These extra

amounts are helping the employers to recruit more employees and motivate the old

employees. Taxes on the basis of these fringe benefits are assessed by Fringe Benefit Tax

Assessment Act 1986. It is obvious to state that there must be certain employee and employer

relation in between the beneficiary and benefit provider. However, it should be understood

that there are various kinds of fringe benefits present under the law. This case study is

depending on the car related fringe benefit.

Car fringe benefits are provided under section 7 of the Fringe Benefit Tax

Assessment Act 1986. If a car is given to an employee for use it for his or her professional

use, it can be called as professional benefits. On the contrary, if the employer allows an

employee to use that car for his personal use, that will be termed as fringe benefit and the car

will come under the parlance of the fringe tax benefit. In certain circumstances, if the

employee does not use the car personally, but the car is available for the personal or private

use, that will also count as fringe benefit and tax will also assess in that case (Braverman et

al., 2015).

There are two methods by which a fringe benefit tax can be assessed such as

statutory method and operating cost process. The process of statutory method has been

prescribed under the Fringe Benefit Tax Assessment Act 1986 and section 9 of the Act has

provided all the calculating process of the methods. However, the tax rate for the car under

the statutory formula depends on the cost of the car. On the other hand, the operating cost

formula has been stated under section 10A and 10B of the Act. The main considerable

portion under this process is the taxable value of the cost that has been spent for the

Answer to question 1

The term Fringe benefit can be defined as an additional amount that can be

provided to the employee or to the worker except their salary or remuneration. These extra

amounts are helping the employers to recruit more employees and motivate the old

employees. Taxes on the basis of these fringe benefits are assessed by Fringe Benefit Tax

Assessment Act 1986. It is obvious to state that there must be certain employee and employer

relation in between the beneficiary and benefit provider. However, it should be understood

that there are various kinds of fringe benefits present under the law. This case study is

depending on the car related fringe benefit.

Car fringe benefits are provided under section 7 of the Fringe Benefit Tax

Assessment Act 1986. If a car is given to an employee for use it for his or her professional

use, it can be called as professional benefits. On the contrary, if the employer allows an

employee to use that car for his personal use, that will be termed as fringe benefit and the car

will come under the parlance of the fringe tax benefit. In certain circumstances, if the

employee does not use the car personally, but the car is available for the personal or private

use, that will also count as fringe benefit and tax will also assess in that case (Braverman et

al., 2015).

There are two methods by which a fringe benefit tax can be assessed such as

statutory method and operating cost process. The process of statutory method has been

prescribed under the Fringe Benefit Tax Assessment Act 1986 and section 9 of the Act has

provided all the calculating process of the methods. However, the tax rate for the car under

the statutory formula depends on the cost of the car. On the other hand, the operating cost

formula has been stated under section 10A and 10B of the Act. The main considerable

portion under this process is the taxable value of the cost that has been spent for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION

operational purpose of this car. The rate of the tax is being determined on the basis of the

lowest taxable values of the fringe benefits. However, in case of both the methods, all the

related documents are to be maintained properly to avoid all the future dilemmas.

It has been learnt from the case that the car given to Charlie are being used for

private use also besides the professional purpose and according to the provision of the Fringe

Benefit Tax Assessment Act 1986, Charlie is liable to pay fringe benefit tax for the sedan

therefore. The car has been provided to him by the Shiny Homes Pty Ltd and therefore, there

is fair provision to include the car under the fringe benefit tax.

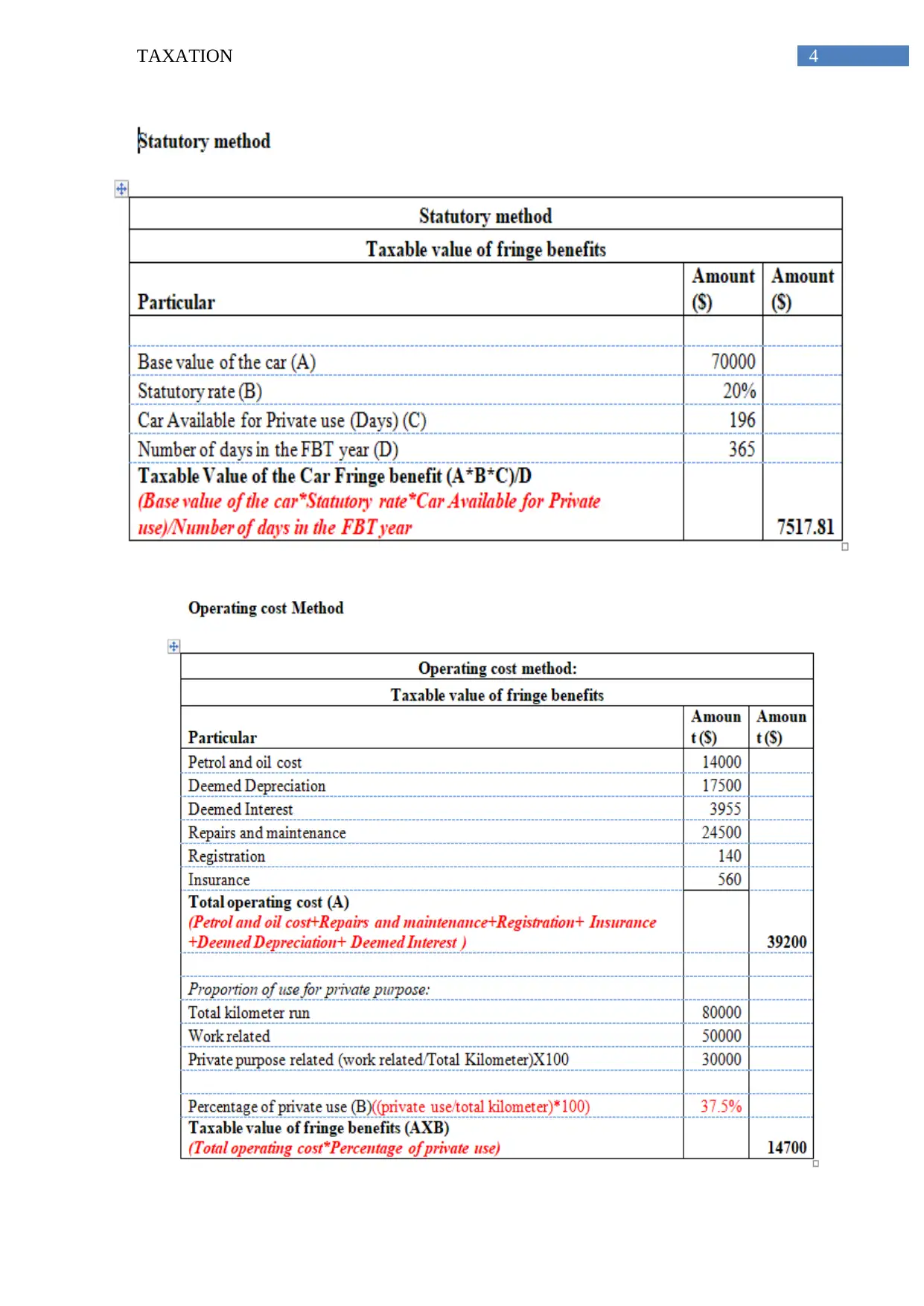

Based on the above mentioned facts, it can be stated that both the methods will be

applied on the car to evaluate its taxation rates as per the provision of the Fringe Benefit Tax

Assessment Act 1986. The taxable value of the car should be calculated by assuming the

statutory rate as 20% and this percentage should be treated as the base value of the car and

the figure should be resulted after multiply the percentage with the rear base value of the car.

However, certain kilometres has been mentioned in this case that is covered by the car is not

at all reliable in case of statutory method. In case of operating cost method, the operating cost

of the car should be separated in case of the work related matters and private use of the car.

Therefore, the taxable values in both the cases should be different in nature.

operational purpose of this car. The rate of the tax is being determined on the basis of the

lowest taxable values of the fringe benefits. However, in case of both the methods, all the

related documents are to be maintained properly to avoid all the future dilemmas.

It has been learnt from the case that the car given to Charlie are being used for

private use also besides the professional purpose and according to the provision of the Fringe

Benefit Tax Assessment Act 1986, Charlie is liable to pay fringe benefit tax for the sedan

therefore. The car has been provided to him by the Shiny Homes Pty Ltd and therefore, there

is fair provision to include the car under the fringe benefit tax.

Based on the above mentioned facts, it can be stated that both the methods will be

applied on the car to evaluate its taxation rates as per the provision of the Fringe Benefit Tax

Assessment Act 1986. The taxable value of the car should be calculated by assuming the

statutory rate as 20% and this percentage should be treated as the base value of the car and

the figure should be resulted after multiply the percentage with the rear base value of the car.

However, certain kilometres has been mentioned in this case that is covered by the car is not

at all reliable in case of statutory method. In case of operating cost method, the operating cost

of the car should be separated in case of the work related matters and private use of the car.

Therefore, the taxable values in both the cases should be different in nature.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION

5TAXATION

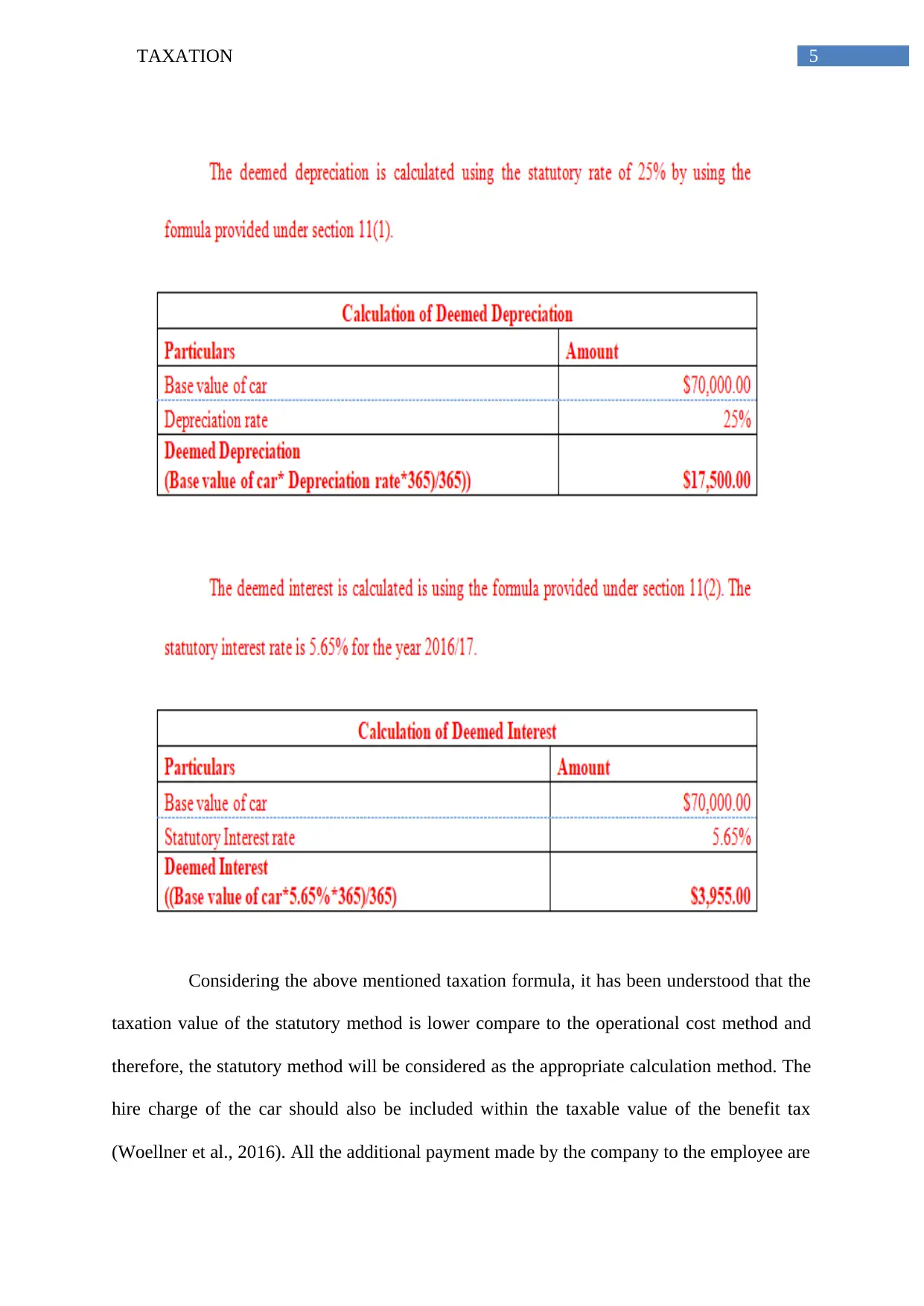

Considering the above mentioned taxation formula, it has been understood that the

taxation value of the statutory method is lower compare to the operational cost method and

therefore, the statutory method will be considered as the appropriate calculation method. The

hire charge of the car should also be included within the taxable value of the benefit tax

(Woellner et al., 2016). All the additional payment made by the company to the employee are

Considering the above mentioned taxation formula, it has been understood that the

taxation value of the statutory method is lower compare to the operational cost method and

therefore, the statutory method will be considered as the appropriate calculation method. The

hire charge of the car should also be included within the taxable value of the benefit tax

(Woellner et al., 2016). All the additional payment made by the company to the employee are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION

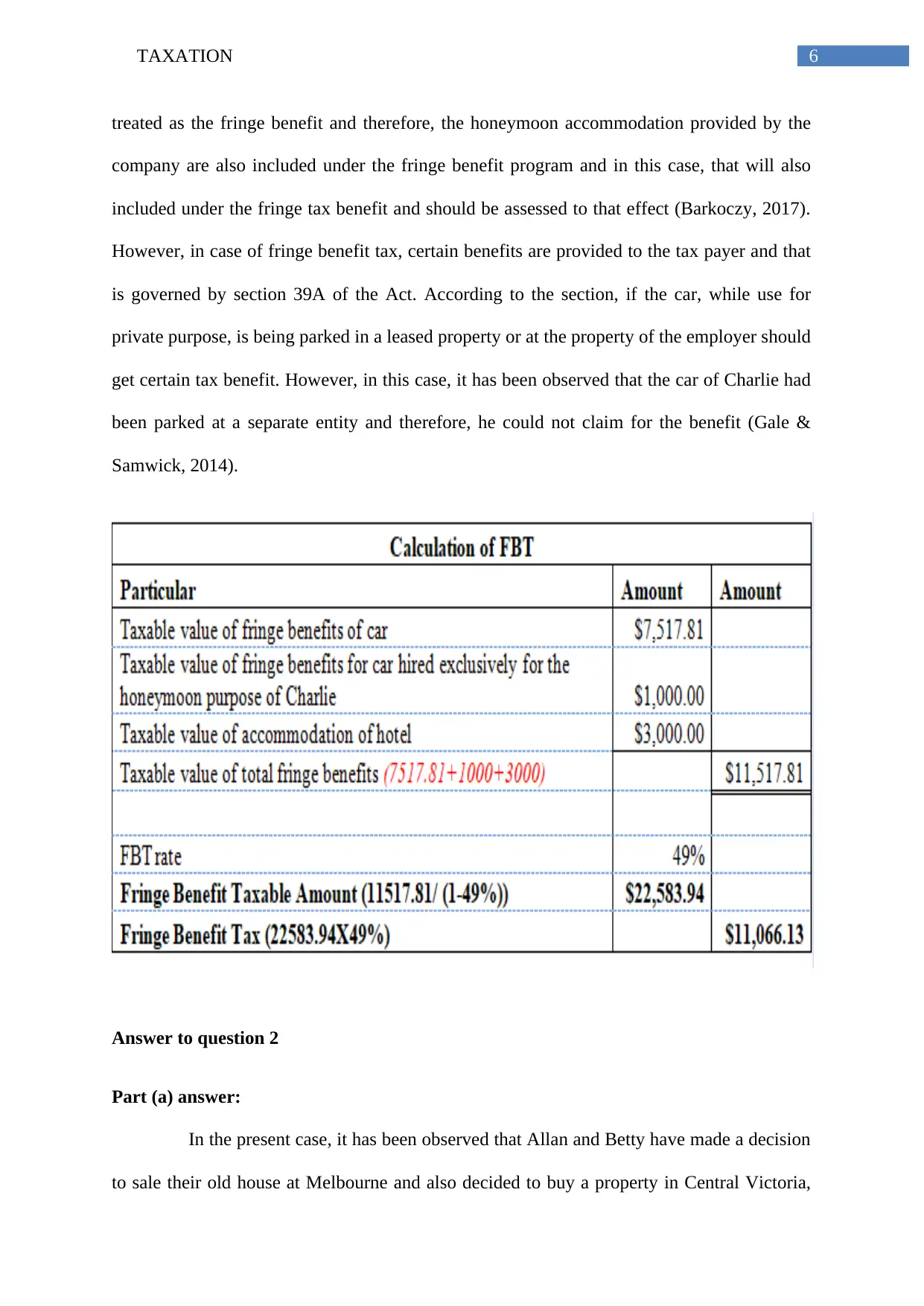

treated as the fringe benefit and therefore, the honeymoon accommodation provided by the

company are also included under the fringe benefit program and in this case, that will also

included under the fringe tax benefit and should be assessed to that effect (Barkoczy, 2017).

However, in case of fringe benefit tax, certain benefits are provided to the tax payer and that

is governed by section 39A of the Act. According to the section, if the car, while use for

private purpose, is being parked in a leased property or at the property of the employer should

get certain tax benefit. However, in this case, it has been observed that the car of Charlie had

been parked at a separate entity and therefore, he could not claim for the benefit (Gale &

Samwick, 2014).

Answer to question 2

Part (a) answer:

In the present case, it has been observed that Allan and Betty have made a decision

to sale their old house at Melbourne and also decided to buy a property in Central Victoria,

treated as the fringe benefit and therefore, the honeymoon accommodation provided by the

company are also included under the fringe benefit program and in this case, that will also

included under the fringe tax benefit and should be assessed to that effect (Barkoczy, 2017).

However, in case of fringe benefit tax, certain benefits are provided to the tax payer and that

is governed by section 39A of the Act. According to the section, if the car, while use for

private purpose, is being parked in a leased property or at the property of the employer should

get certain tax benefit. However, in this case, it has been observed that the car of Charlie had

been parked at a separate entity and therefore, he could not claim for the benefit (Gale &

Samwick, 2014).

Answer to question 2

Part (a) answer:

In the present case, it has been observed that Allan and Betty have made a decision

to sale their old house at Melbourne and also decided to buy a property in Central Victoria,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

which is far better and bigger compared to their current house. It has also been learnt from the

facts that Allan is a Locum doctor and Betty is working as a part time accountant. Therefore,

their income should be calculated under the Income Tax Assessment Act 1997 (Hodgson &

Pearce, 2015). Allan, who is the Locum doctor, is very popular because of his healing power

and the elderly people of the city are very much depended on him and many of his patients

are given certain confectionery items to him which can be termed as token of appreciation. It

can clearly be stated that these gifts are not commercial products and therefore, the question

of additional tax consequence will not be cropped up. On the other hand, it has been observed

that Allan also get certain wine bottle worth $36 from one of his clients and that bottle is of

commercial value. Therefore, Allan has to pay tax for the bottle as the item will be assessed

as a taxable income and therefore, such item will be included under the income tax liability

program and the provisions of Income Tax Assessment Act will be imposed in this case.

Part (b) answer:

There are certain differences can be pointed out in between the hobby and

business (Maurer Maurer et al., 2017). Under the provision of the Taxation Ruling TR 97/11,

all the related indicators of a business have been prescribed and therefore, certain differences

have made in between hobby and business which can be classified as follows:

The first difference can be made from the perspective of activities. In an activity,

where there is major mercantile purpose present, can be called as business activity.

The next difference can be taken from the object portion. The main object of business

activity is to earn more profit, whereas in case of hobby, there is no such purpose

present.

The most common relationship under the business activity is the employer and

employee relationship. There is no such relationship present in case of hobbies.

which is far better and bigger compared to their current house. It has also been learnt from the

facts that Allan is a Locum doctor and Betty is working as a part time accountant. Therefore,

their income should be calculated under the Income Tax Assessment Act 1997 (Hodgson &

Pearce, 2015). Allan, who is the Locum doctor, is very popular because of his healing power

and the elderly people of the city are very much depended on him and many of his patients

are given certain confectionery items to him which can be termed as token of appreciation. It

can clearly be stated that these gifts are not commercial products and therefore, the question

of additional tax consequence will not be cropped up. On the other hand, it has been observed

that Allan also get certain wine bottle worth $36 from one of his clients and that bottle is of

commercial value. Therefore, Allan has to pay tax for the bottle as the item will be assessed

as a taxable income and therefore, such item will be included under the income tax liability

program and the provisions of Income Tax Assessment Act will be imposed in this case.

Part (b) answer:

There are certain differences can be pointed out in between the hobby and

business (Maurer Maurer et al., 2017). Under the provision of the Taxation Ruling TR 97/11,

all the related indicators of a business have been prescribed and therefore, certain differences

have made in between hobby and business which can be classified as follows:

The first difference can be made from the perspective of activities. In an activity,

where there is major mercantile purpose present, can be called as business activity.

The next difference can be taken from the object portion. The main object of business

activity is to earn more profit, whereas in case of hobby, there is no such purpose

present.

The most common relationship under the business activity is the employer and

employee relationship. There is no such relationship present in case of hobbies.

8TAXATION

A huge amount of investment is involved in the set up of business activities, however,

there is no such investment involved in case of hobbies (Barrett & Veal, 2016).

Premises are playing an important role in case of the business. on the other hand,

separate premises is not mandatory in case of hobby.

There have certain cases been filed to determine the differences in between the

business activities and hobbies. However, in Cooper Books Pty Ltd vs. Commissioner of

Taxation of Commonwealth of Australia, the court has pleased to make certain differences

in between business activities and hobbies.

Part (c) answer:

In case of hobby, there is no question of commercial interest exists. Therefore,

hobbies can be exempted from tax liabilities to that extent until any commercial interests are

being gained by this. However, if the hobby becomes the profession of someone, then taxes

could be imposed and that hobby will become a business activity (Pearce & Pinto, 2015).

From the given perspective, it can be seen that gardening was the hobby of Allan and Betty.

However, at the point of time when Allan and Betty had made certain profits from the hobby

and started to earn $500 to $600 from the hobby, it becomes business activity. Additionally,

barter system should also be included under the Income Tax Assessment Act 1997.

Therefore, all the income shall be assessed under the income tax system in this case.

Barter is an example of exchange system and in this case, all the transactions are

made without any monetary means. Under this system, certain things are transferred in lieu of

other thing. However, in Australia, the process of barter system is also included under the

Income Tax Assessment Act 1997 (Gitman, Juchau & Flanagan, 2015). Certain provisions of

the barter system are included under the Goods and Service Tax system. However, that

system should be involved with certain commercial transactional. In case of any commercial

A huge amount of investment is involved in the set up of business activities, however,

there is no such investment involved in case of hobbies (Barrett & Veal, 2016).

Premises are playing an important role in case of the business. on the other hand,

separate premises is not mandatory in case of hobby.

There have certain cases been filed to determine the differences in between the

business activities and hobbies. However, in Cooper Books Pty Ltd vs. Commissioner of

Taxation of Commonwealth of Australia, the court has pleased to make certain differences

in between business activities and hobbies.

Part (c) answer:

In case of hobby, there is no question of commercial interest exists. Therefore,

hobbies can be exempted from tax liabilities to that extent until any commercial interests are

being gained by this. However, if the hobby becomes the profession of someone, then taxes

could be imposed and that hobby will become a business activity (Pearce & Pinto, 2015).

From the given perspective, it can be seen that gardening was the hobby of Allan and Betty.

However, at the point of time when Allan and Betty had made certain profits from the hobby

and started to earn $500 to $600 from the hobby, it becomes business activity. Additionally,

barter system should also be included under the Income Tax Assessment Act 1997.

Therefore, all the income shall be assessed under the income tax system in this case.

Barter is an example of exchange system and in this case, all the transactions are

made without any monetary means. Under this system, certain things are transferred in lieu of

other thing. However, in Australia, the process of barter system is also included under the

Income Tax Assessment Act 1997 (Gitman, Juchau & Flanagan, 2015). Certain provisions of

the barter system are included under the Goods and Service Tax system. However, that

system should be involved with certain commercial transactional. In case of any commercial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION

transaction, barter system will be regarded as a part of the cash and credit system. in the

given case, it has been observed that both Allen and Betty has decided to develop barter

system regarding their business and also earns money from that system. Therefore, the barter

system involves commercialisation and therefore is a subject of tax and GST system (Saad,

2014).

Part (d) answer:

Barter system is quite similar to the cash and credit system and all the taxes that are

assessable or deductable similar to that of cash and credit option. When a person makes

certain commercial exchange will become a part of the taxable sale and will become a part of

the tax liability. However, in case of the commercial barter process, the exchangeable thing

can be money. If the values of the barter system are included under the GST entity,

registration of the process is needed. The market value of the goods will help to assess the tax

liability under the barter system (Tran-Nam, 2016).

transaction, barter system will be regarded as a part of the cash and credit system. in the

given case, it has been observed that both Allen and Betty has decided to develop barter

system regarding their business and also earns money from that system. Therefore, the barter

system involves commercialisation and therefore is a subject of tax and GST system (Saad,

2014).

Part (d) answer:

Barter system is quite similar to the cash and credit system and all the taxes that are

assessable or deductable similar to that of cash and credit option. When a person makes

certain commercial exchange will become a part of the taxable sale and will become a part of

the tax liability. However, in case of the commercial barter process, the exchangeable thing

can be money. If the values of the barter system are included under the GST entity,

registration of the process is needed. The market value of the goods will help to assess the tax

liability under the barter system (Tran-Nam, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION

Reference:

Akins, B.W., Chapman, J.L. & Gordon, J.M., 2014. A whole new world: Income tax

considerations of the Bitcoin economy. Pitt. Tax Rev., 12, p.25.

Barkoczy, S., 2017. Core Tax Legislation and Study Guide. OUP Catalogue.

Barrett, J. M., & Veal, J. A. (2016). Tax Rationality, Politics, and Media Spin: A Case Study

of the Failed ‘Car Park Tax’Proposal.

Braverman, D., Marsden, S. & Sadiq, K., 2015. Assessing Taxpayer Response to Legislative

Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl. Tax'n, 17, p.1.

Braverman, D., Marsden, S., & Sadiq, K. (2015). Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl.

Tax'n, 17, 1.

Gale, W.G. & Samwick, A.A., 2014. Effects of income tax changes on economic growth.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Hodgson, H., & Pearce, P. (2015). TravelSmart or travel tax breaks: is the fringe benefits tax

a barrier to active commuting in Australia? 1. eJournal of Tax Research, 13(3), 819.

Kim, P.H., Longest, K.C. & Lippmann, S., 2015. The tortoise versus the hare: Progress and

business viability differences between conventional and leisure-based

founders. Journal of Business Venturing, 30(2), pp.185-204.

Reference:

Akins, B.W., Chapman, J.L. & Gordon, J.M., 2014. A whole new world: Income tax

considerations of the Bitcoin economy. Pitt. Tax Rev., 12, p.25.

Barkoczy, S., 2017. Core Tax Legislation and Study Guide. OUP Catalogue.

Barrett, J. M., & Veal, J. A. (2016). Tax Rationality, Politics, and Media Spin: A Case Study

of the Failed ‘Car Park Tax’Proposal.

Braverman, D., Marsden, S. & Sadiq, K., 2015. Assessing Taxpayer Response to Legislative

Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl. Tax'n, 17, p.1.

Braverman, D., Marsden, S., & Sadiq, K. (2015). Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl.

Tax'n, 17, 1.

Gale, W.G. & Samwick, A.A., 2014. Effects of income tax changes on economic growth.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Hodgson, H., & Pearce, P. (2015). TravelSmart or travel tax breaks: is the fringe benefits tax

a barrier to active commuting in Australia? 1. eJournal of Tax Research, 13(3), 819.

Kim, P.H., Longest, K.C. & Lippmann, S., 2015. The tortoise versus the hare: Progress and

business viability differences between conventional and leisure-based

founders. Journal of Business Venturing, 30(2), pp.185-204.

11TAXATION

Maurer, L., Port, C., Roth, T., & Walker, J. (2017). A Brave New Post-BEPS World: New

Double Tax Treaty Between Germany and Australia Implements BEPS

Measures. Intertax, 45(4), 310-321.

Nijland, L. & Dijst, M., 2015. Commuting-related fringe benefits in the Netherlands:

Interrelationships and company, employee and location

characteristics. Transportation Research Part A: Policy and Practice, 77, pp.358-371.

Pearce, P., & Pinto, D. (2015). An evaluation of the case for a congestion tax in

Australia. The Tax Specialist, 18(4), 146-153.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Tran-Nam, B. (2016). Tax Reform and Tax Simplification: Conceptual and Measurement

Issues and Australian Experiences. In The Complexity of Tax Simplification (pp. 11-

44). Palgrave Macmillan UK.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Maurer, L., Port, C., Roth, T., & Walker, J. (2017). A Brave New Post-BEPS World: New

Double Tax Treaty Between Germany and Australia Implements BEPS

Measures. Intertax, 45(4), 310-321.

Nijland, L. & Dijst, M., 2015. Commuting-related fringe benefits in the Netherlands:

Interrelationships and company, employee and location

characteristics. Transportation Research Part A: Policy and Practice, 77, pp.358-371.

Pearce, P., & Pinto, D. (2015). An evaluation of the case for a congestion tax in

Australia. The Tax Specialist, 18(4), 146-153.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Tran-Nam, B. (2016). Tax Reform and Tax Simplification: Conceptual and Measurement

Issues and Australian Experiences. In The Complexity of Tax Simplification (pp. 11-

44). Palgrave Macmillan UK.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.