Accounting Fundamentals: Financial Statement and Ratio Analysis Report

VerifiedAdded on 2023/06/18

|17

|2825

|153

Report

AI Summary

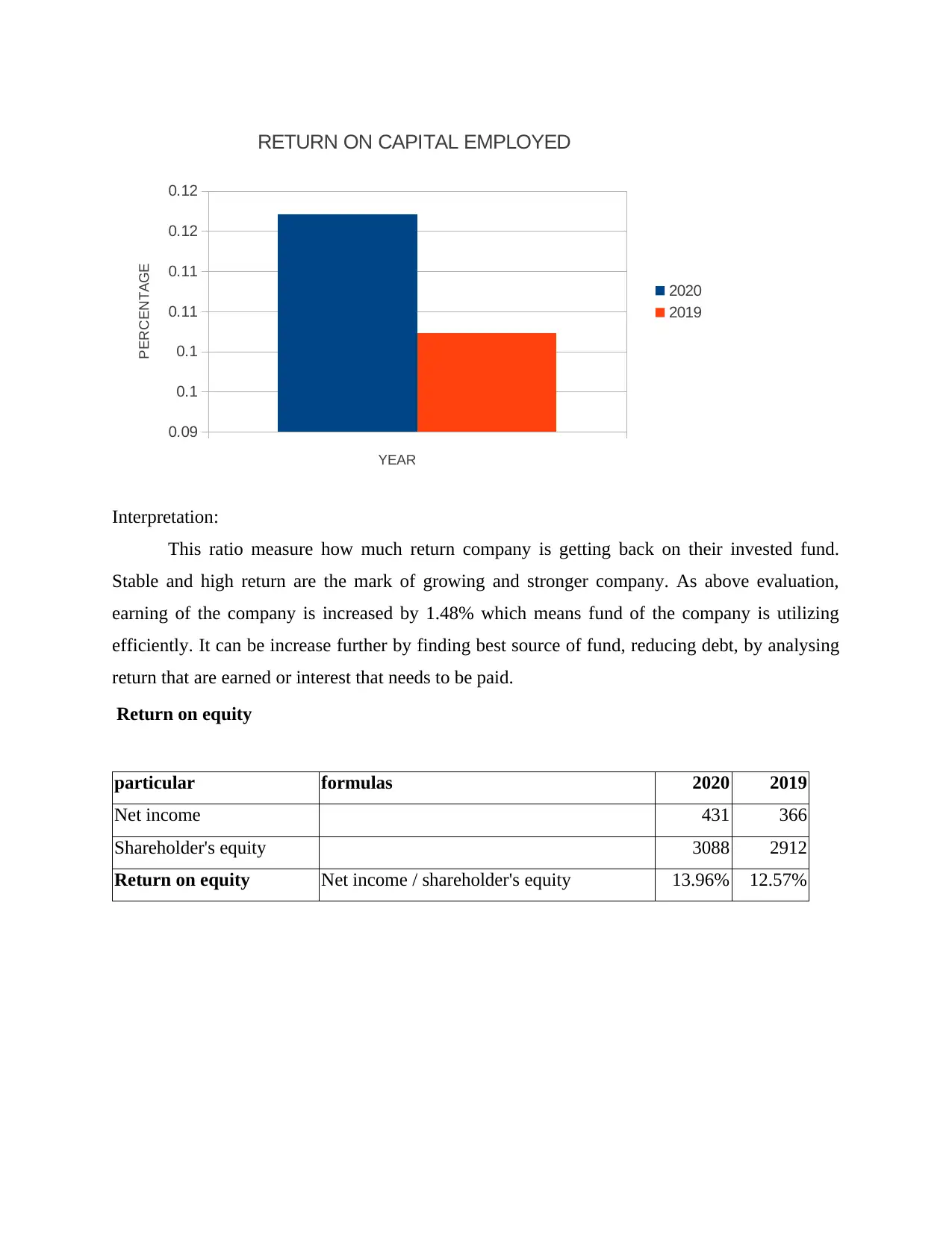

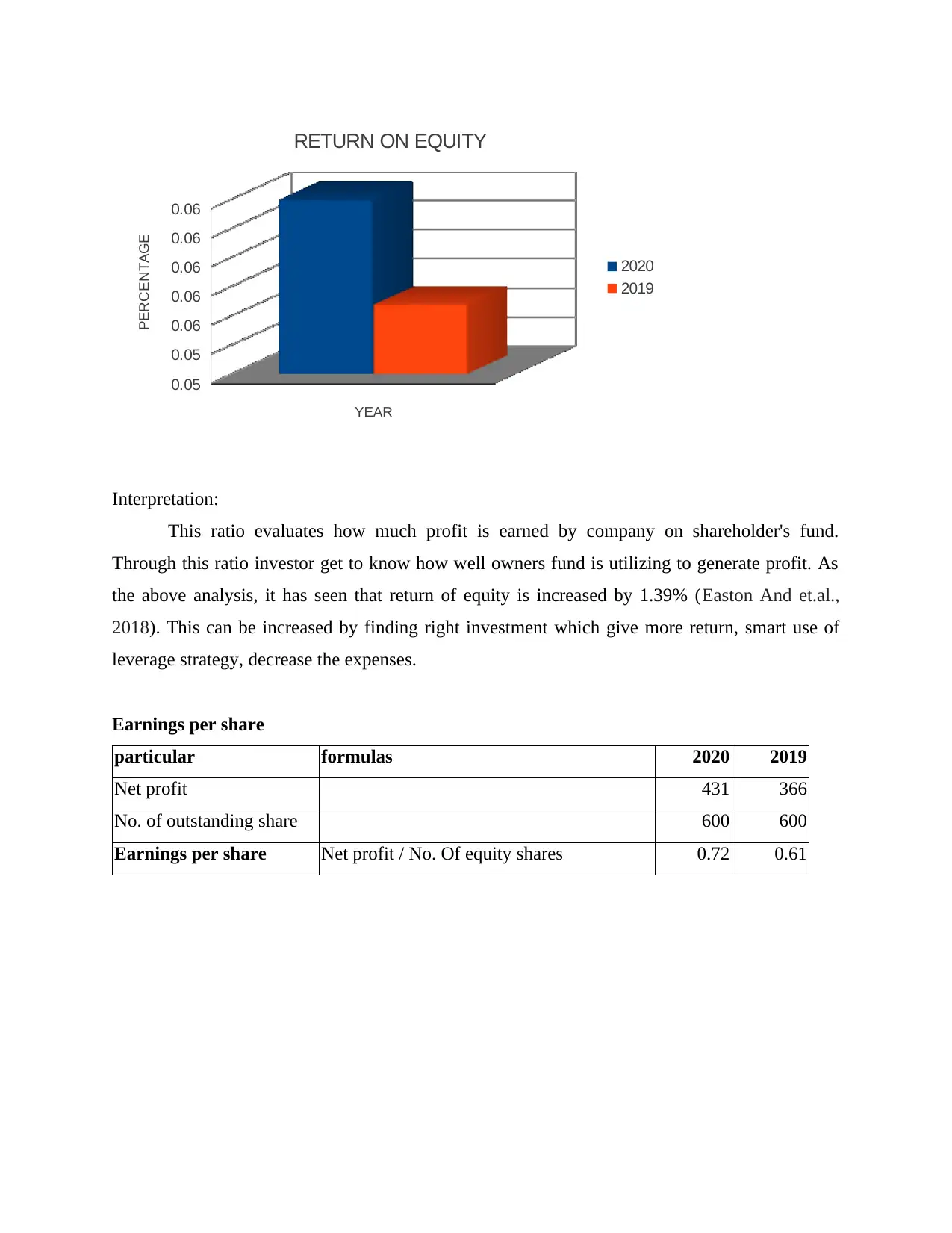

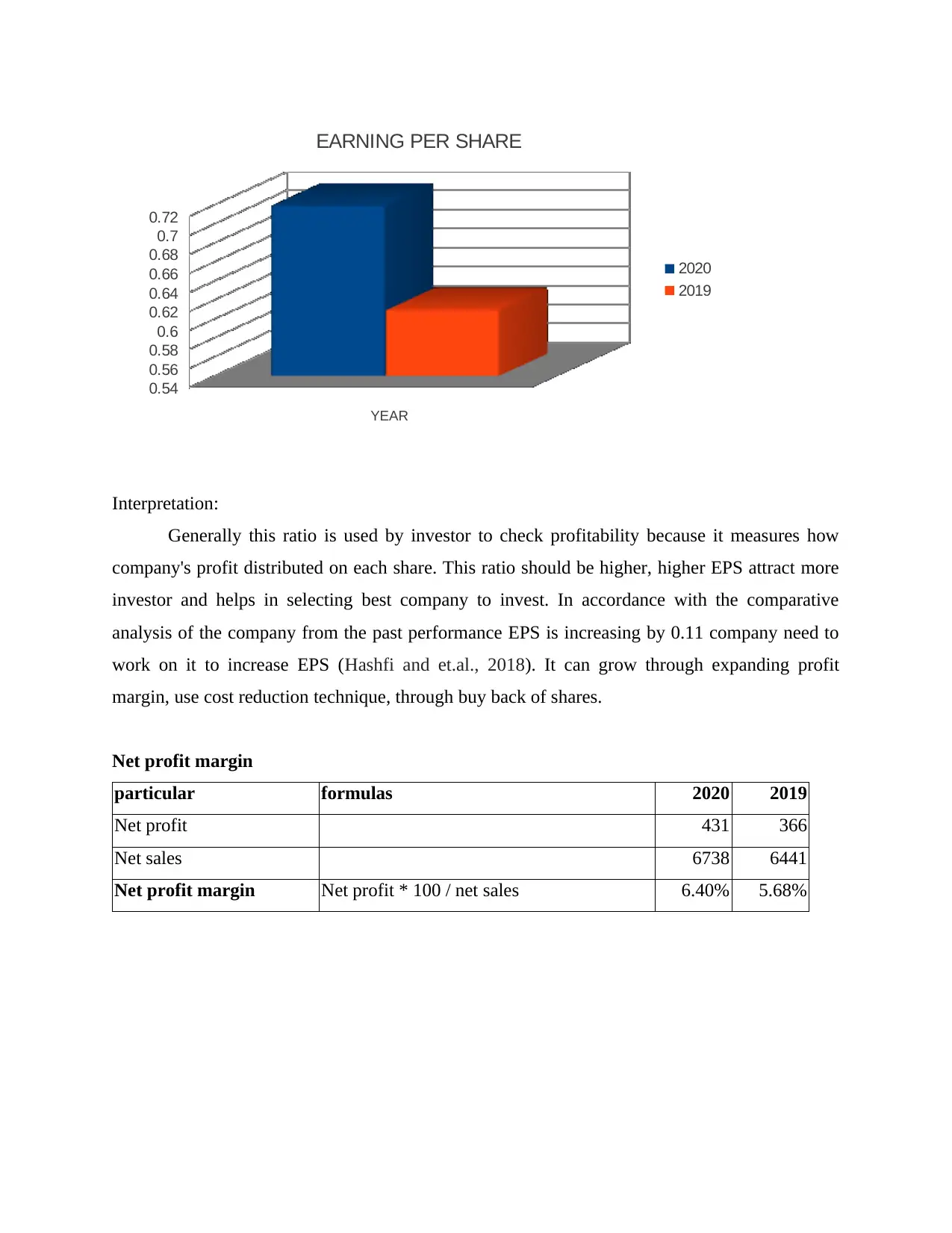

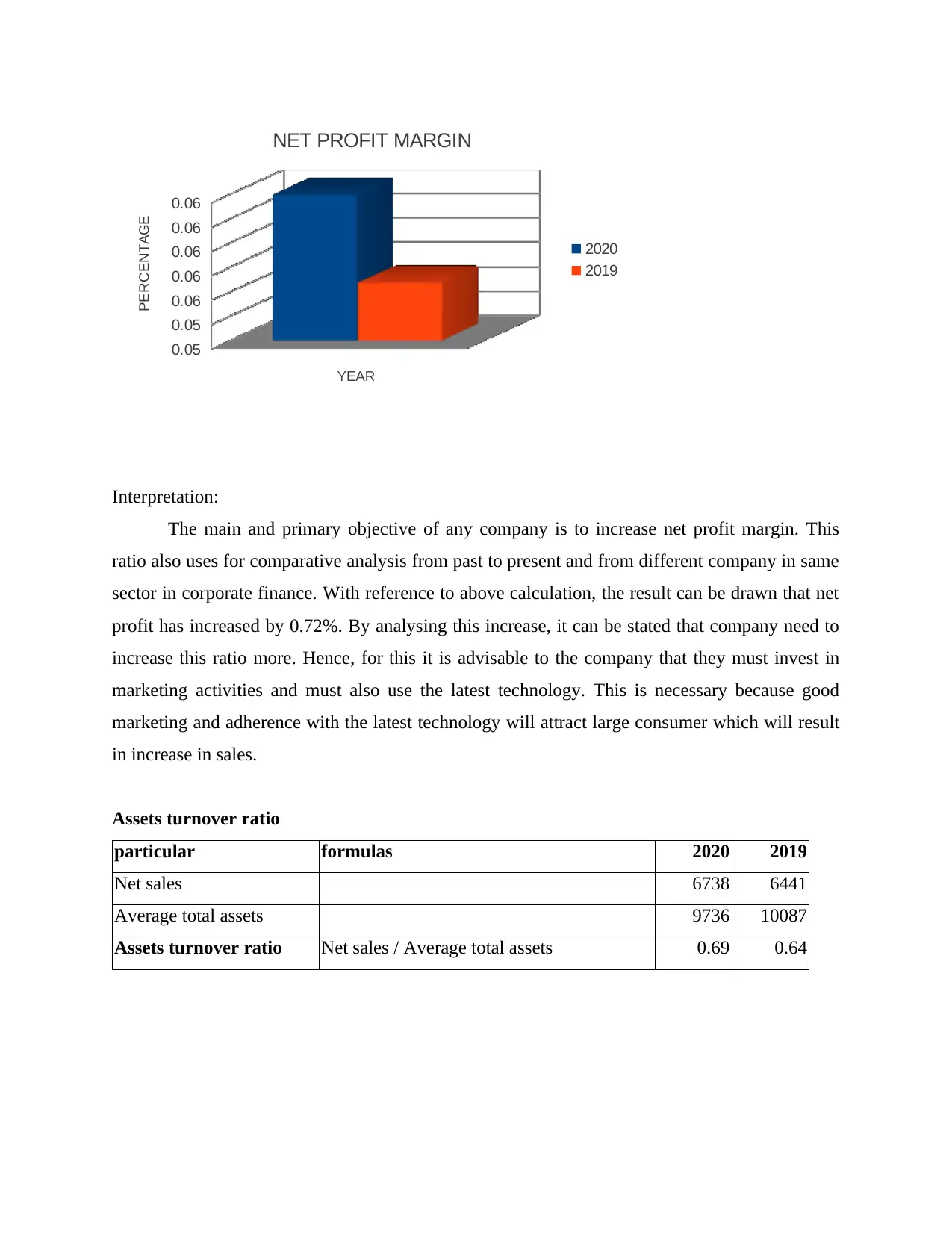

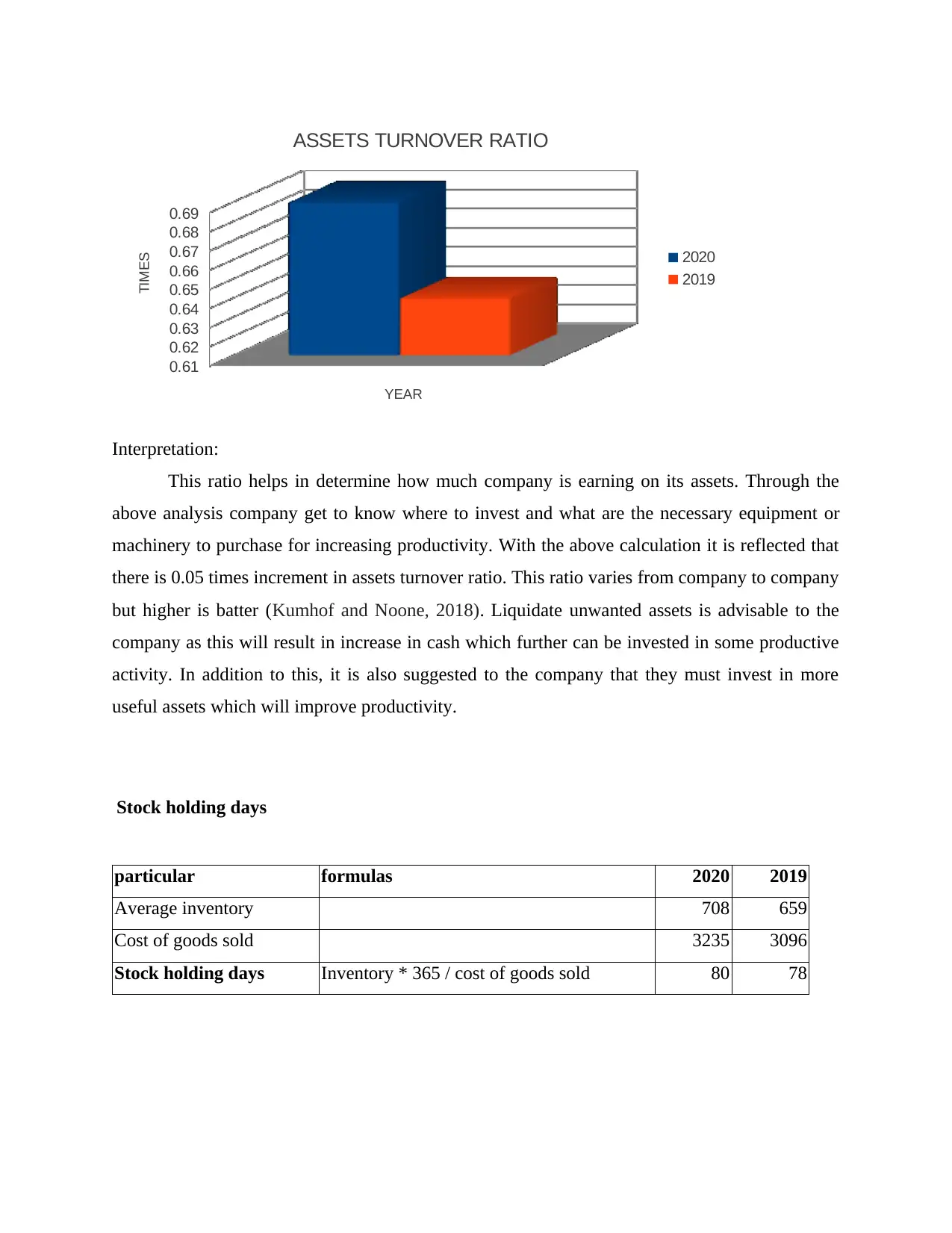

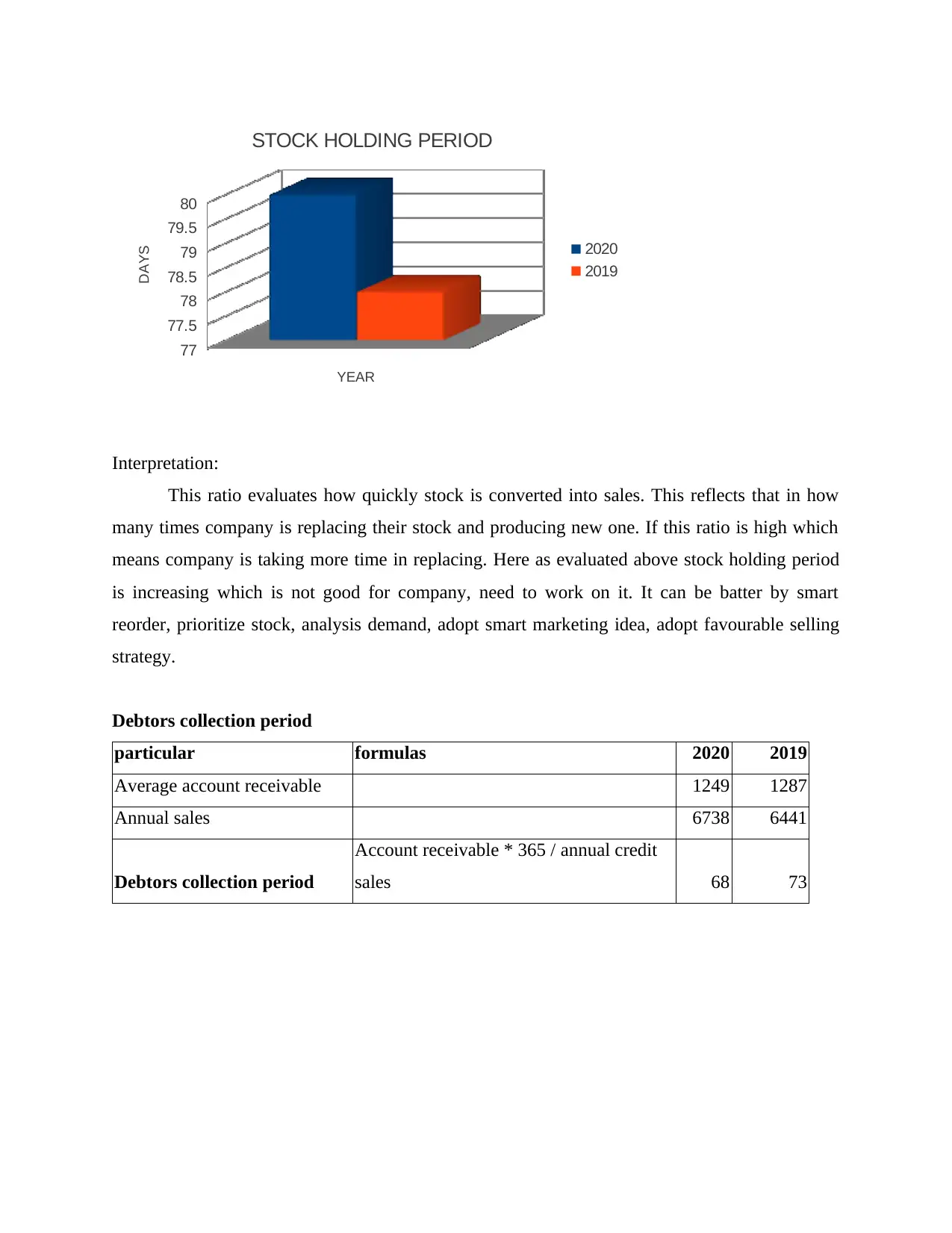

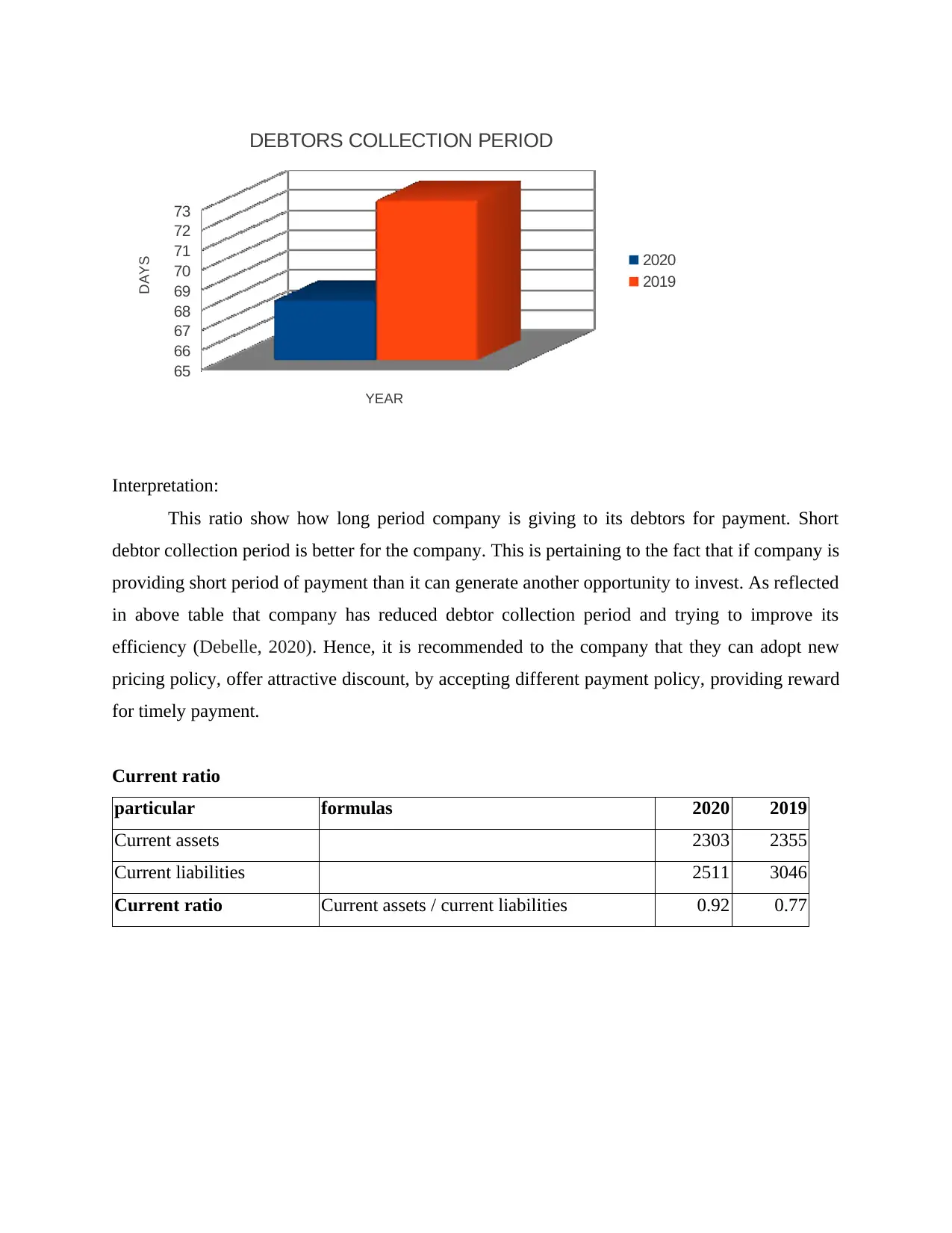

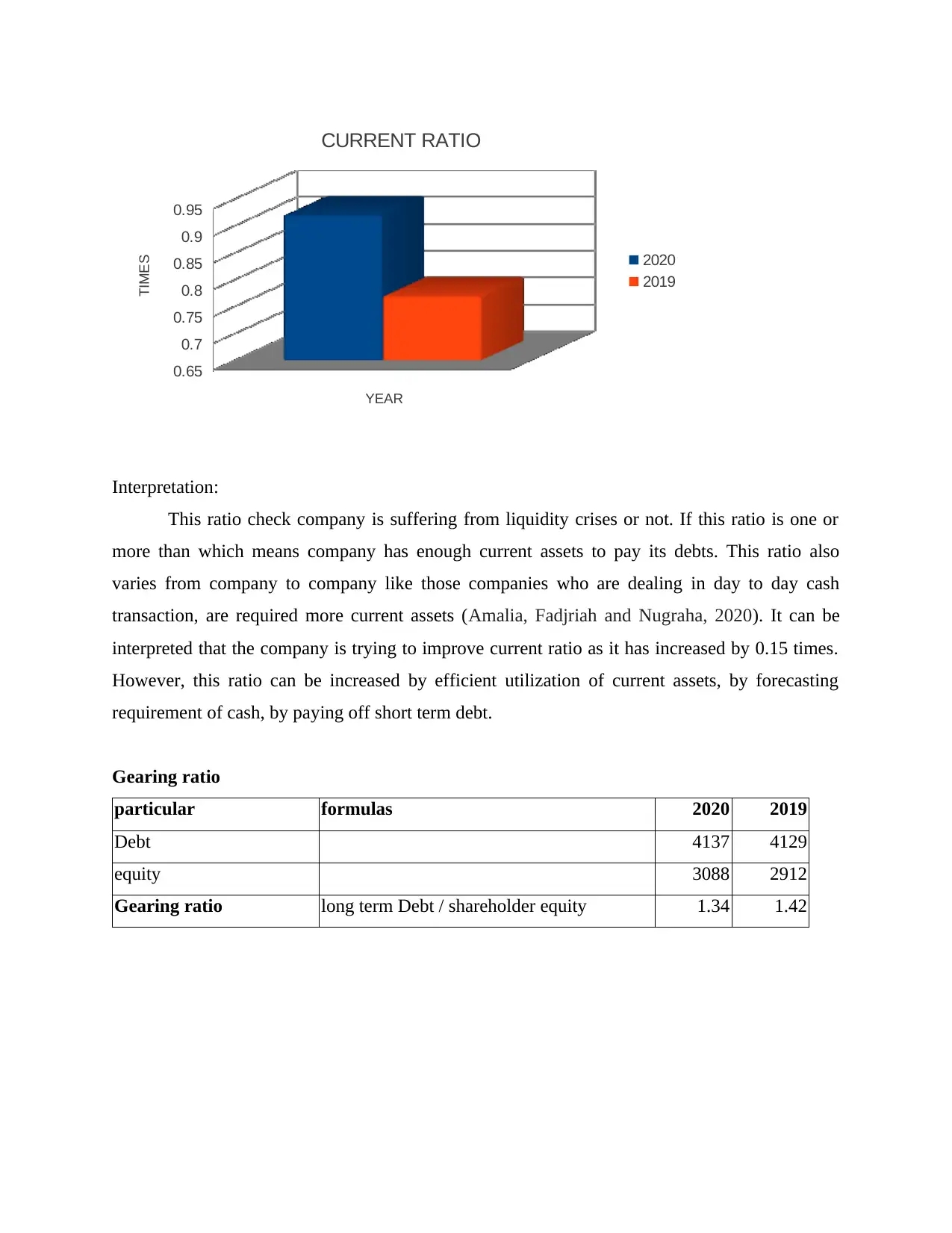

This report provides a detailed analysis of accounting fundamentals, focusing on the preparation and interpretation of financial statements. It includes an examination of Kedison PLC's financial statements, highlighting key adjustments and their impact on the balance sheet and income statement. The report further delves into financial ratio analysis of Chocco PLC, a chocolate and confectionery manufacturer, evaluating various ratios such as Return on Capital Employed, Return on Equity, Earnings per Share, Net Profit Margin, Assets Turnover Ratio, Stock Holding Days, Debtors Collection Period, Current Ratio, Gearing Ratio, and Inventory Turnover Ratio. Each ratio is calculated for the years 2020 and 2019, providing comparative insights into the company's performance and efficiency. The analysis aims to provide a comprehensive understanding of the company's financial health and operational effectiveness, with recommendations for improvement in areas such as inventory management, debt utilization, and profitability enhancement.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.