ACC102 Assignment: Financial Accounting for Depreciation and Inventory

VerifiedAdded on 2023/06/04

|10

|1204

|103

Homework Assignment

AI Summary

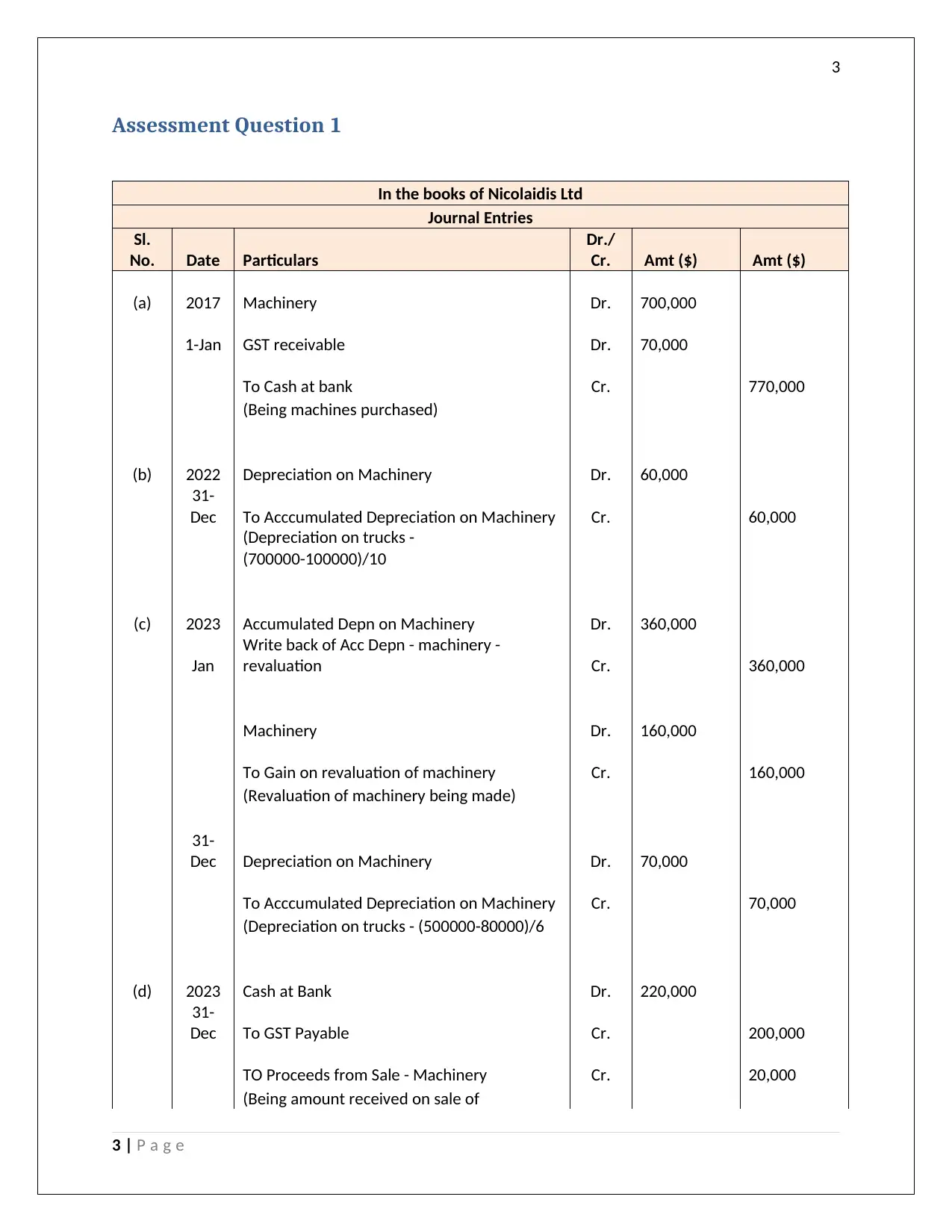

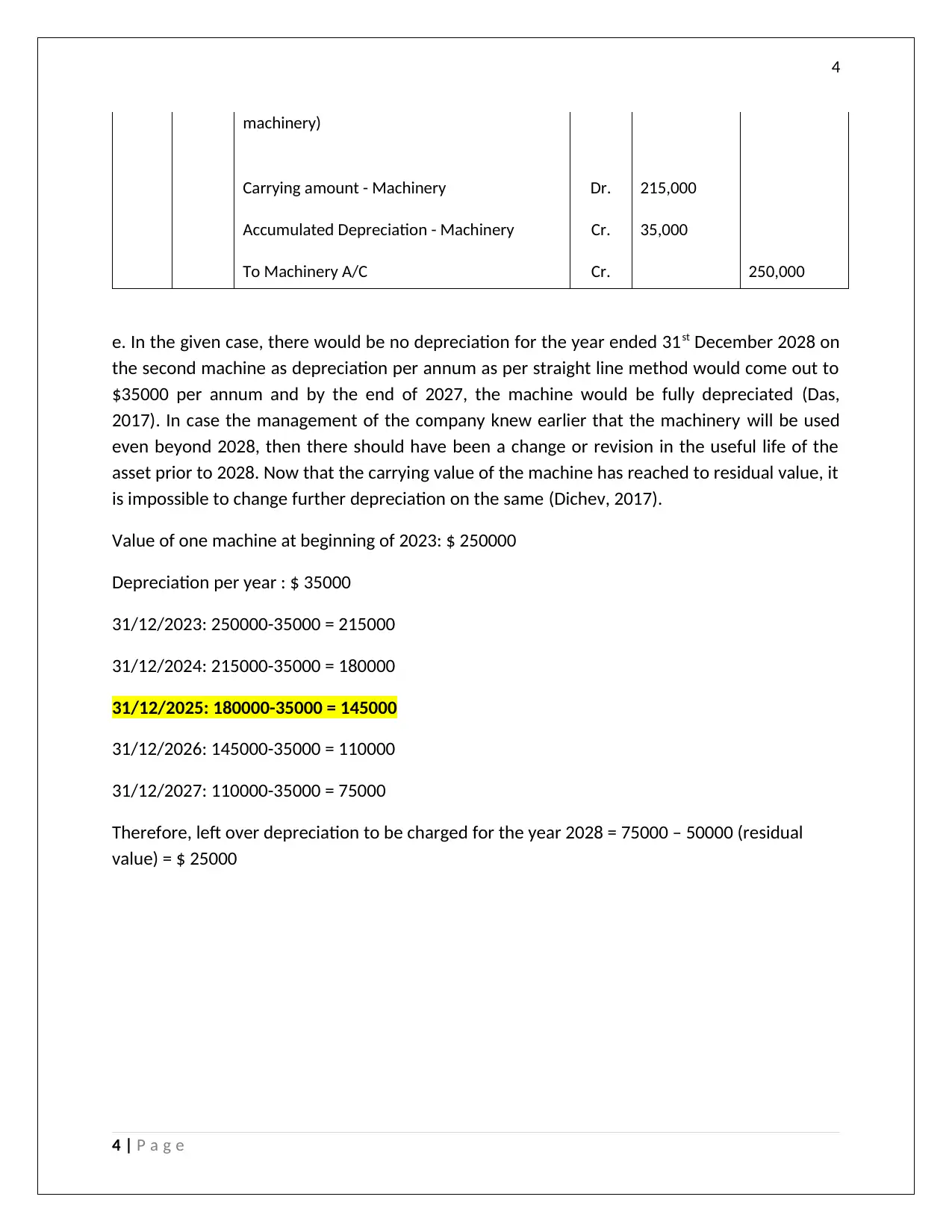

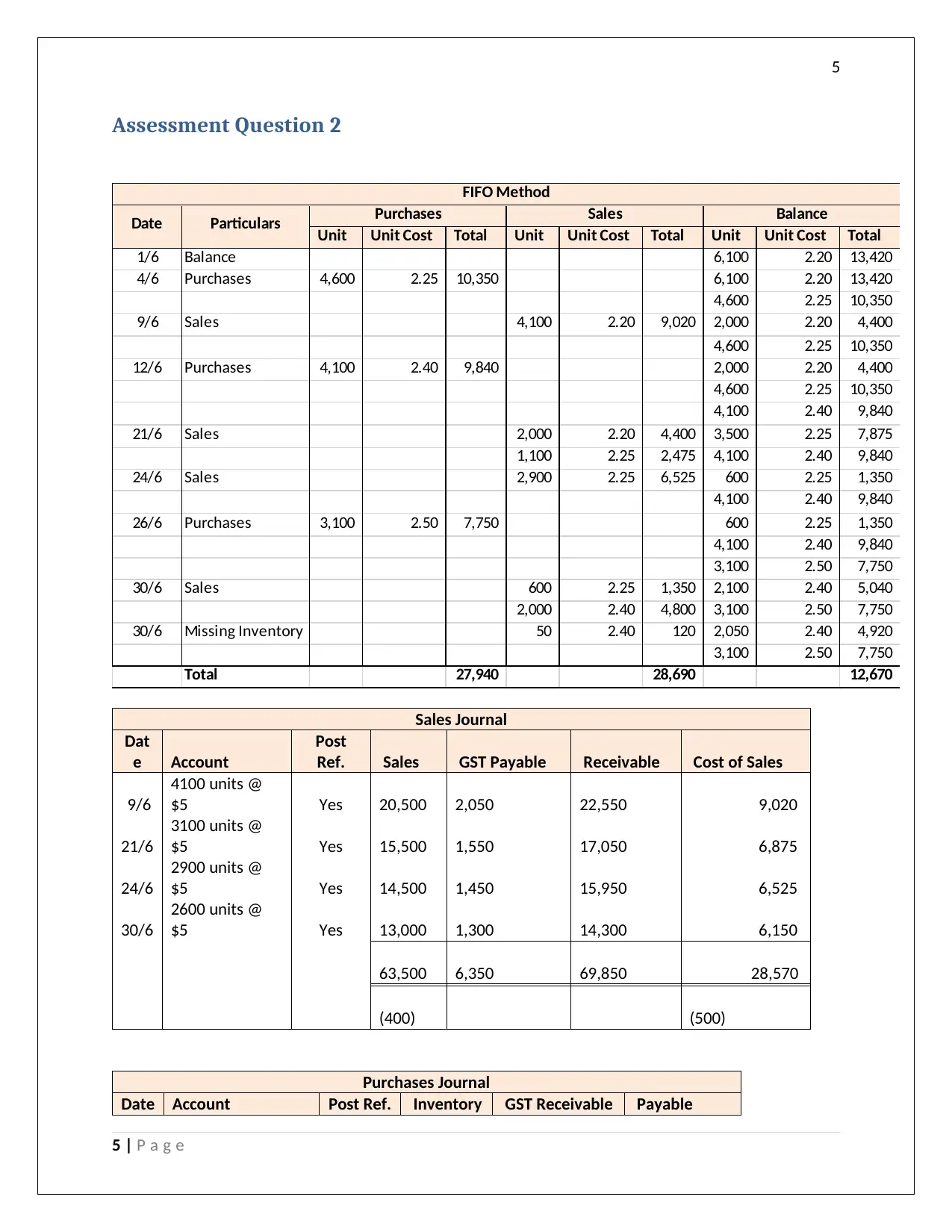

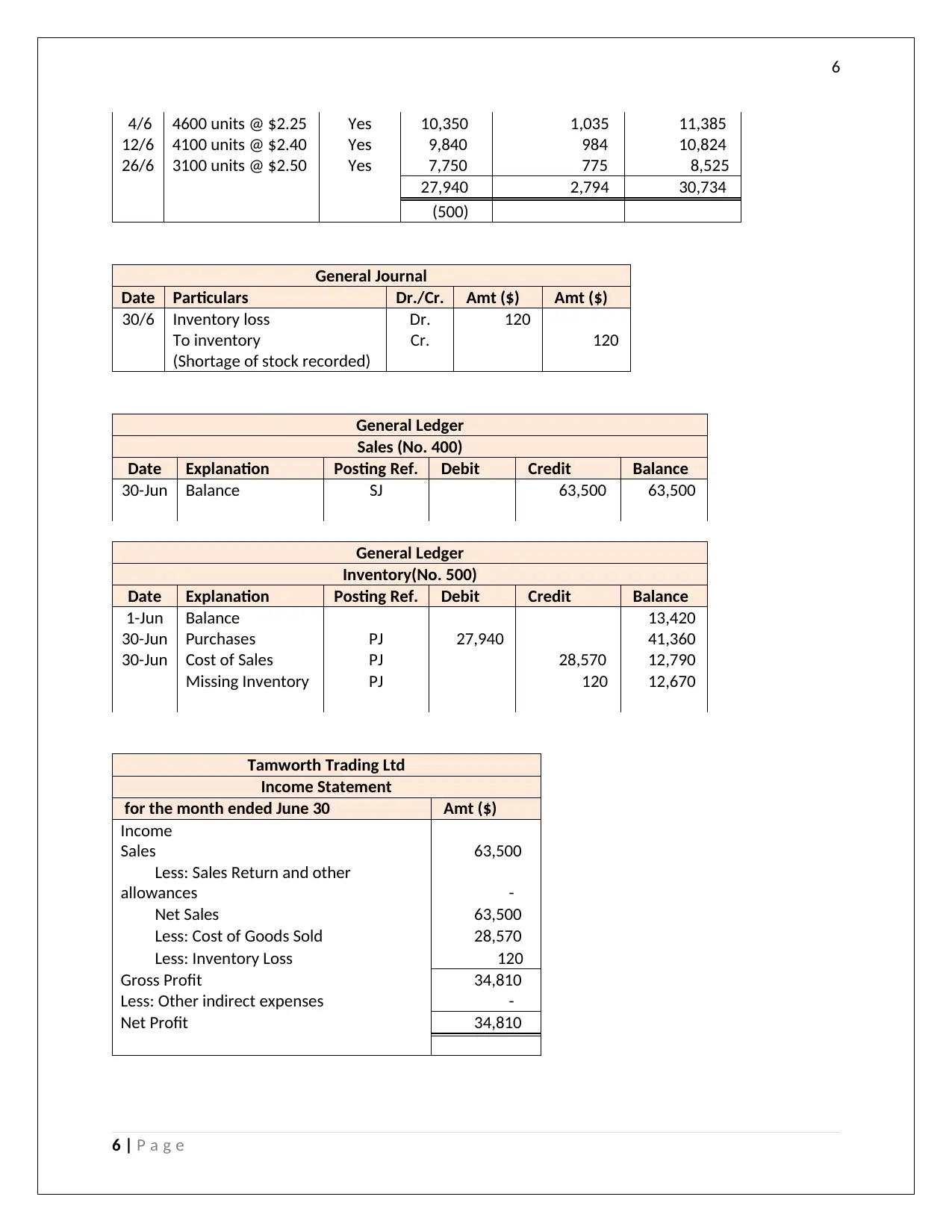

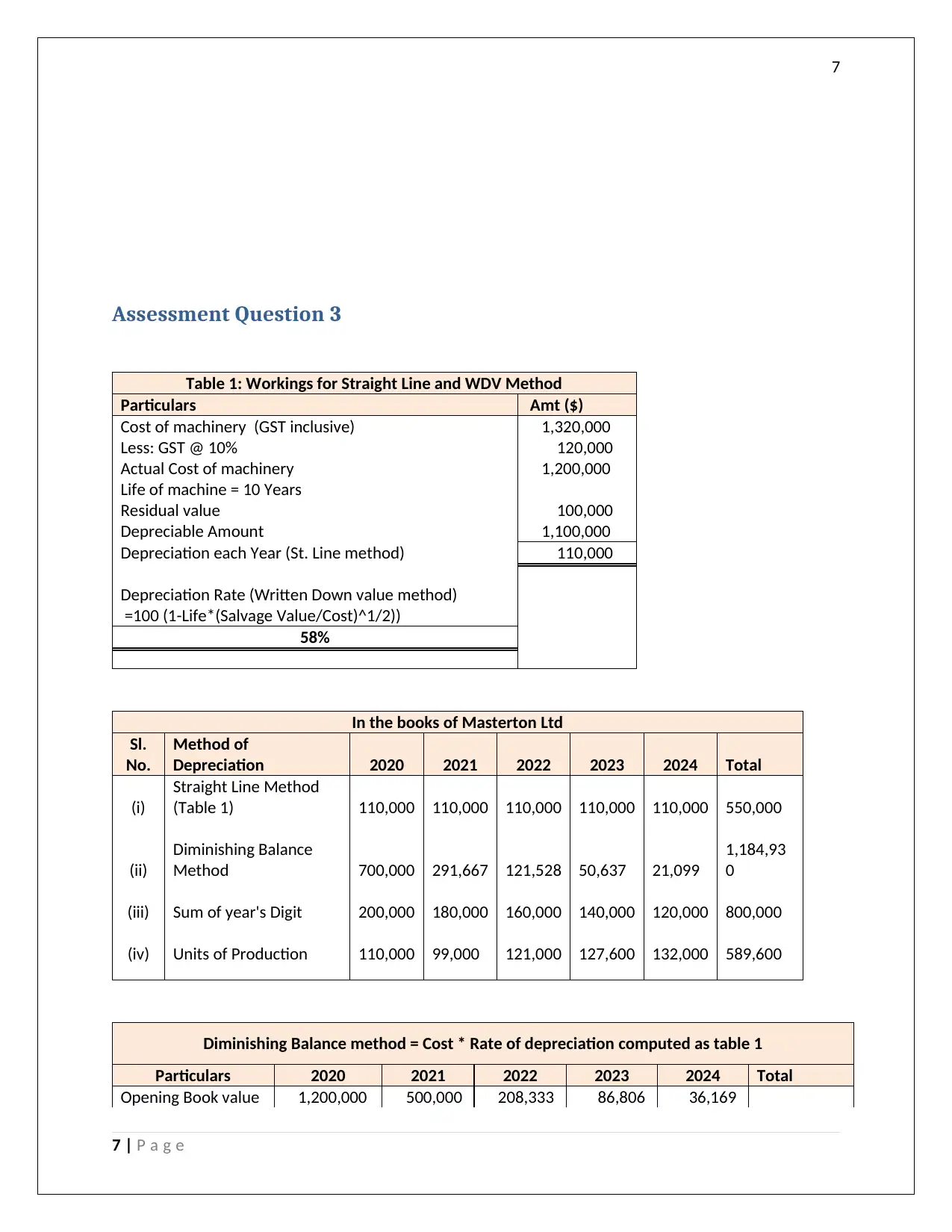

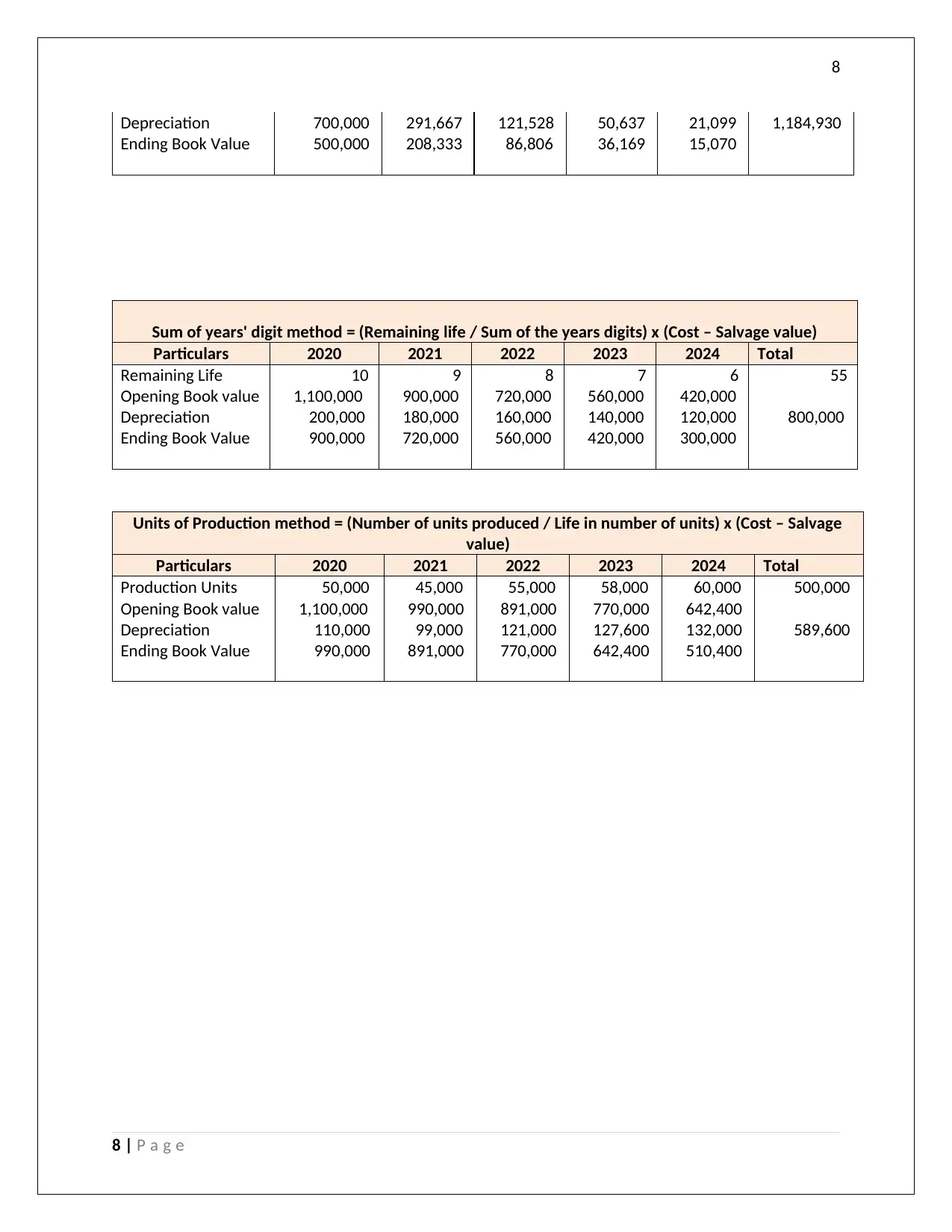

This document presents a comprehensive solution to an ACC102 assignment focusing on financial accounting principles. The assignment covers three key areas: journal entries related to machinery purchase, depreciation calculations, and revaluation; inventory valuation using the FIFO method, including purchases, sales, and cost of goods sold; and a comparison of depreciation methods, including straight-line, diminishing balance, sum-of-the-years' digits, and units of production. The solution provides detailed calculations, journal entries, and financial statements to illustrate the application of these accounting concepts. The document also includes supporting tables and references, providing a thorough understanding of the topics covered. The assignment is a valuable resource for students studying financial accounting and seeking to improve their understanding of depreciation, inventory management, and financial reporting.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.