Accounting Fundamentals: Analysis of Costing Models and Management

VerifiedAdded on 2023/06/18

|8

|1308

|374

Homework Assignment

AI Summary

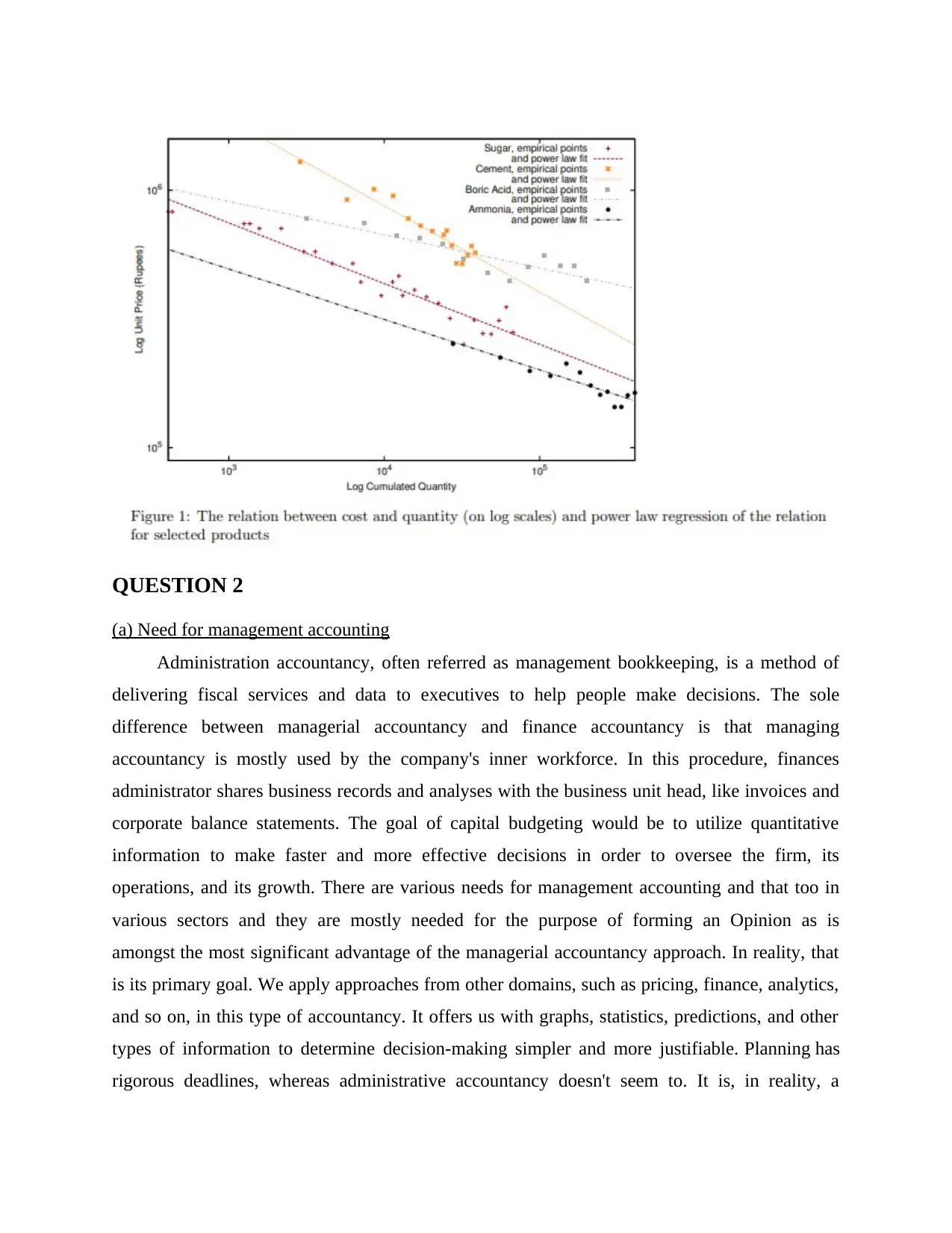

This assignment delves into the fundamentals of accounting, exploring the limitations of linear and non-linear costing models with a focus on the relationship between sales price and quantity. It highlights the significance of management accounting in providing financial data to aid managerial decision-making, emphasizing its role in planning, problem-solving, and strategic decision-making. Various management accounting techniques are discussed, including financial planning, financial report analysis, standard costing, and budgetary control, illustrating their importance in achieving organizational objectives and ensuring effective financial management. Desklib provides students access to this assignment and other resources.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.