Finance Assignment: Interest Compounding, Amortization, and Annuities

VerifiedAdded on 2023/06/15

|7

|1051

|352

Homework Assignment

AI Summary

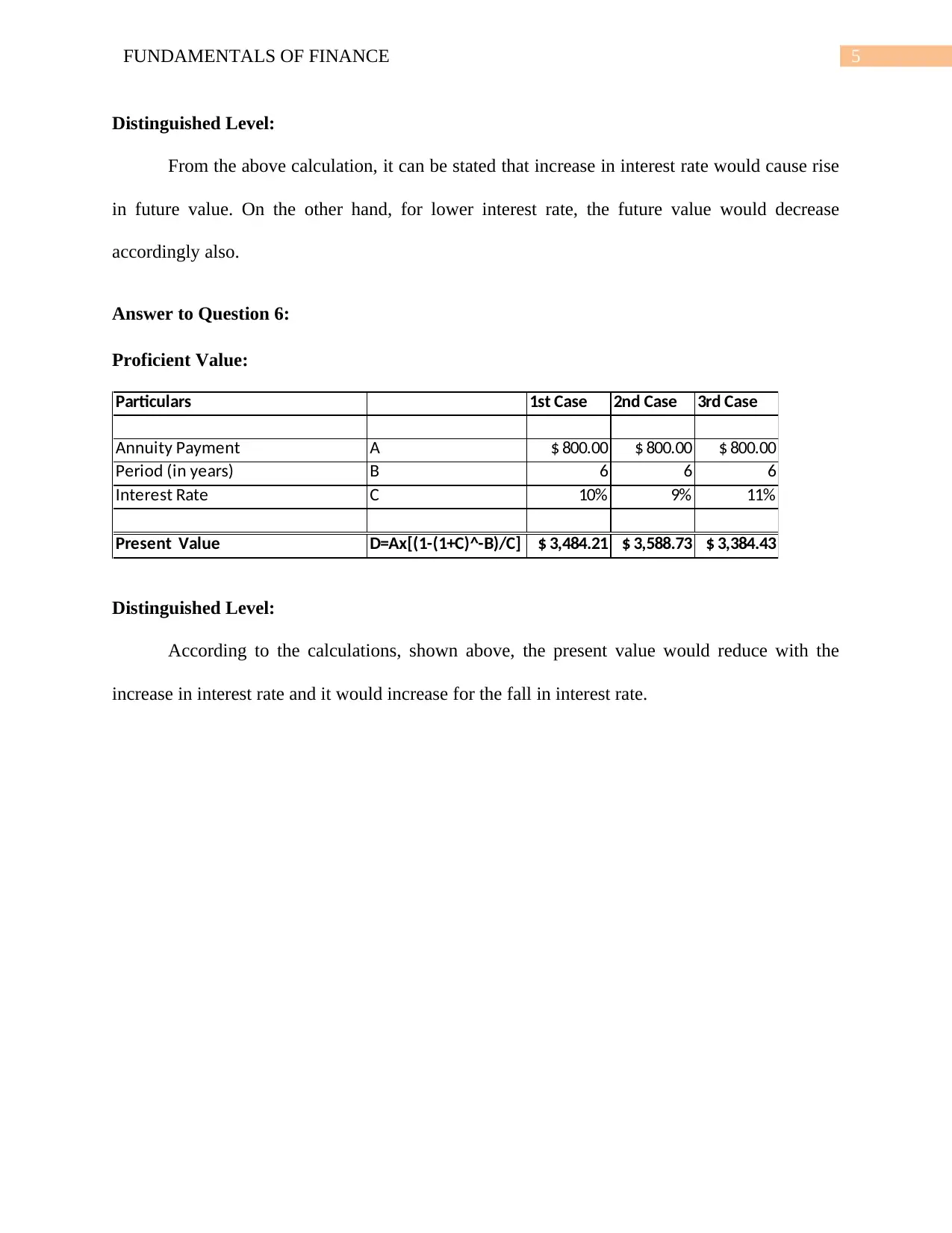

This assignment delves into the fundamentals of finance, addressing key concepts such as interest compounding, loan amortization, and annuity calculations. It explains the impact of compounding frequency on interest earned or paid, highlighting the preference for monthly compounding for savings and less frequent compounding for loans. The assignment also details the purpose and mechanics of amortization schedules, emphasizing the decreasing interest portion over time and its implications for tax deductions. Furthermore, it differentiates between ordinary annuities and annuities due, illustrating how payment timing affects future value. Numerical examples are provided to demonstrate the effects of varying interest rates on future and present values of annuities. Desklib offers comprehensive study tools and resources for students seeking a deeper understanding of these financial principles.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.