Fundamentals of Income Tax: Tax Reconciliation and Liability Analysis

VerifiedAdded on 2022/11/29

|11

|2517

|112

Homework Assignment

AI Summary

This assignment solution addresses the income tax return preparation for Bend-it Physio Limited for the year ended March 31, 20X8. The solution begins with an analysis of non-allowable expenses, including entertainment expenditure, which is subject to specific deduction limitations. It then details adjustments to the accounting profit for items like depreciation, fines, and donations to determine the adjusted tax profit. The solution covers the treatment of company losses, provisional tax payments, and legal fees related to capital expenditure. It explains the impact of dividends from wholly owned companies and the application of imputation credits and RWT credits. Finally, the solution provides a tax reconciliation statement, a computation of tax liability, and the final tax payable, explaining the need for reconciliation due to differences between accounting and tax regulations. The solution follows the Income Tax Act 2007 and IRD guidelines.

Fundamentals of Income Tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income tax

Answer to the 1st part of Note 1:

The non-allowable expense is $3,250. Entertainment expenditure is subject to a special set of

rules that limits the deduction of business entertainment expenditure to 50% of the amount of the

expenditure. As per IRD guide on Entertainment Expense Food/drink consumed off premises &

Food/drink consumed in the course of client meetings are specified entertainment and eligible for

only 50% deduction thereof, so 50% of $6,500 is disallowed. Further Food/drink consumed in

course of a conference (4+ hours) & Entertainment consumed outside NZ falls under Excluded

entertainment as per IRD and eligible for a 100% deduction.

Answer to the 2nd part of Note 1:

This will increase the adjusted tax profit by $3,250 for the purpose of income tax. Since we are

disallowing a part of entertainment expense, the accounting profit shall have to be adjusted and

such disallowed portion shall be added back to the accounting profit to get adjusted tax profit for

the purpose of income tax (Wells, 2011).

Answer to the 1st part of the Note 2:

This will increase the adjusted tax profit by $1200 because the allowed depreciation as per IRD

is lower than that calculated as per Accounting Records. The income tax act has specified a

method for depreciation, and we shall follow that particular method to compute depreciation

instead of using Accounting method, therefore, any difference between these two shall be

adjusted and shall reflect in the tax reconciliation statement (ATO, 2018).

Answer to the 1st part of the Note 3:

Fines fall under the Non-Deductible Expenses. As per IRD, there is no deduction allowed for the

fines paid when a law has been broken (ATO, 2018). In the given case the Speeding Tickets are

paid on behalf of directors speeding on his way to the office. Hence a part of the non-deductible

expense and shall be disallowed and therefore shall be added back to the accounting profit.

2

Answer to the 1st part of Note 1:

The non-allowable expense is $3,250. Entertainment expenditure is subject to a special set of

rules that limits the deduction of business entertainment expenditure to 50% of the amount of the

expenditure. As per IRD guide on Entertainment Expense Food/drink consumed off premises &

Food/drink consumed in the course of client meetings are specified entertainment and eligible for

only 50% deduction thereof, so 50% of $6,500 is disallowed. Further Food/drink consumed in

course of a conference (4+ hours) & Entertainment consumed outside NZ falls under Excluded

entertainment as per IRD and eligible for a 100% deduction.

Answer to the 2nd part of Note 1:

This will increase the adjusted tax profit by $3,250 for the purpose of income tax. Since we are

disallowing a part of entertainment expense, the accounting profit shall have to be adjusted and

such disallowed portion shall be added back to the accounting profit to get adjusted tax profit for

the purpose of income tax (Wells, 2011).

Answer to the 1st part of the Note 2:

This will increase the adjusted tax profit by $1200 because the allowed depreciation as per IRD

is lower than that calculated as per Accounting Records. The income tax act has specified a

method for depreciation, and we shall follow that particular method to compute depreciation

instead of using Accounting method, therefore, any difference between these two shall be

adjusted and shall reflect in the tax reconciliation statement (ATO, 2018).

Answer to the 1st part of the Note 3:

Fines fall under the Non-Deductible Expenses. As per IRD, there is no deduction allowed for the

fines paid when a law has been broken (ATO, 2018). In the given case the Speeding Tickets are

paid on behalf of directors speeding on his way to the office. Hence a part of the non-deductible

expense and shall be disallowed and therefore shall be added back to the accounting profit.

2

Income tax

So even the Speeding tickets fines were paid when the director was speeding his way to the

office, such expense is not as a deduction.

Answer to the 2nd part of the Note 3:

Since fines are non-deductible expenses, such expenses will be added back to the adjusted tax

profit and this will increase the adjusted tax profit because we are disallowing the Speeding

tickets expenses (Wells, 2011). IRD has specified to disallow the payments of any fines because

the law has been broken which shall not be allowed as a deduction (Nethercott, Richardson &

Devos, 2013).

So this amount of $120 shall be added back to the accounting profit and will result in increased

adjusted profit.

Answer to the 1st part of the Note 4:

A “donee organization” is a special type of organization, considered by the Inland Revenue to

have met the requirements as set out in the Income Tax Act 2007. Any organizations other than a

Donee organisation are a non-donee organization (Mayo, 2018).

Any donations made to donee organizations are eligible for 100% deductions, whereas donations

made to non-donee organizations are considered as disallowed expenses. Individuals, certain

companies and Māori authorities can get tax benefits by making gifts of money to donee

organizations (Nethercott, Richardson & Devos, 2013). Contrast this to donations made to Non-

Donee Organizations, which are not permitted, basically clients will get any tax benefits

Also, the maximum allowed deduction that a company can claim is limited to the amount of its

net income, calculated before taking into account the deduction (i.e. tax profit + donations

expense). If the tax profit before donations was less than the allowed amount, the maximum

amount claimed will be reduced (ATO, 2018).

Answer to the 2nd part of the Note 4:

3

So even the Speeding tickets fines were paid when the director was speeding his way to the

office, such expense is not as a deduction.

Answer to the 2nd part of the Note 3:

Since fines are non-deductible expenses, such expenses will be added back to the adjusted tax

profit and this will increase the adjusted tax profit because we are disallowing the Speeding

tickets expenses (Wells, 2011). IRD has specified to disallow the payments of any fines because

the law has been broken which shall not be allowed as a deduction (Nethercott, Richardson &

Devos, 2013).

So this amount of $120 shall be added back to the accounting profit and will result in increased

adjusted profit.

Answer to the 1st part of the Note 4:

A “donee organization” is a special type of organization, considered by the Inland Revenue to

have met the requirements as set out in the Income Tax Act 2007. Any organizations other than a

Donee organisation are a non-donee organization (Mayo, 2018).

Any donations made to donee organizations are eligible for 100% deductions, whereas donations

made to non-donee organizations are considered as disallowed expenses. Individuals, certain

companies and Māori authorities can get tax benefits by making gifts of money to donee

organizations (Nethercott, Richardson & Devos, 2013). Contrast this to donations made to Non-

Donee Organizations, which are not permitted, basically clients will get any tax benefits

Also, the maximum allowed deduction that a company can claim is limited to the amount of its

net income, calculated before taking into account the deduction (i.e. tax profit + donations

expense). If the tax profit before donations was less than the allowed amount, the maximum

amount claimed will be reduced (ATO, 2018).

Answer to the 2nd part of the Note 4:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Income tax

This will increase the adjusted tax profit because of the disallowance of donations of $1,500

made to non-donee organizations and hence shall be added back to the accounting profit to get

the adjusted tax profit for the purpose of income tax. Only donations made to Donee organization

shall be allowed as a deduction, any other donations will be disallowed and shall be added back

to the accounting profits and hence will increase the adjusted tax profit.

Answer to the 1st part of Note 5:

Company losses can be carried forward. If a company’s total expenses exceed its total income a

loss will be made. A company in a loss position does not have to pay an income. The loss can be

carried forward to be offset against future profits.

In the given case Bend-it-Physio has Brought forward profit of $1,080. To bring in the Effect of

the same we have to decrease the brought forward losses from the adjusted tax profit as the

brought forward losses are fully deductible from current year profits and hence $1,080 shall be

deducted from final adjusted tax profit of the company so calculated.

Answer to the 1st part of Note 6:

Provisional tax is a method of paying tax in installments during the year. A business is required

to pay provisional tax if the current year’s residual income tax is more than $2,500. It is a kind of

payment of tax by estimating the total income before actually earning it. Further the credit of

same shall be available to the payer and also a refund shall be granted if the provisional tax paid

is greater than the assessed tax (Mayo, 2018).

Provisional tax payments are due at different dates depending on whether a business is GST

registered and the provisional tax option they choose (Nethercott, Richardson & Devos, 2013).

So in the current case, the residual tax of the company exceeds $2,500 hence it is required to pay

provisional Tax.

Answer to the 2nd part of Note 6:

The Provisional tax is adjusted with the Actual tax liability, and any Refund/Payable is computed

thereon. If the provisional tax paid is greater than the assessed tax liability than the balance of the

4

This will increase the adjusted tax profit because of the disallowance of donations of $1,500

made to non-donee organizations and hence shall be added back to the accounting profit to get

the adjusted tax profit for the purpose of income tax. Only donations made to Donee organization

shall be allowed as a deduction, any other donations will be disallowed and shall be added back

to the accounting profits and hence will increase the adjusted tax profit.

Answer to the 1st part of Note 5:

Company losses can be carried forward. If a company’s total expenses exceed its total income a

loss will be made. A company in a loss position does not have to pay an income. The loss can be

carried forward to be offset against future profits.

In the given case Bend-it-Physio has Brought forward profit of $1,080. To bring in the Effect of

the same we have to decrease the brought forward losses from the adjusted tax profit as the

brought forward losses are fully deductible from current year profits and hence $1,080 shall be

deducted from final adjusted tax profit of the company so calculated.

Answer to the 1st part of Note 6:

Provisional tax is a method of paying tax in installments during the year. A business is required

to pay provisional tax if the current year’s residual income tax is more than $2,500. It is a kind of

payment of tax by estimating the total income before actually earning it. Further the credit of

same shall be available to the payer and also a refund shall be granted if the provisional tax paid

is greater than the assessed tax (Mayo, 2018).

Provisional tax payments are due at different dates depending on whether a business is GST

registered and the provisional tax option they choose (Nethercott, Richardson & Devos, 2013).

So in the current case, the residual tax of the company exceeds $2,500 hence it is required to pay

provisional Tax.

Answer to the 2nd part of Note 6:

The Provisional tax is adjusted with the Actual tax liability, and any Refund/Payable is computed

thereon. If the provisional tax paid is greater than the assessed tax liability than the balance of the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income tax

excess provisional tax paid shall be refunded to the payer, and if the assessed tax is greater than

the provisional tax paid then the balance amount of assessed tax shall be payable.

In the given case for bend-it-physio had paid a provisional tax of $2,775, the same amount shall

be available as a tax credit and it shall be adjusted with the actual tax liability of $6,917 resulting

in reduced final tax liability for the company.

Answer to the 1st part of Note 7:

Legal fees relating to revenue expense or day to day activities are allowed fully as a deduction

whereas legal fees relating to capital expenditure are totally disallowed as per the Income Tax

Act (ATO, 2017). However, if the legal fees so paid for Capital Expenditure does not exceed

$10,000 then such amount is fully allowable as a deduction under the Income Tax Act and will

require no adjustment if such legal expenses do not exceed $10,000 in total for capital

expenditure.

So as per IRD, only payments up to $10,000 are allowed as a deduction for Capital Expenditure.

Answer to the 2nd part of Note 7:

Legal fees relating to capital expenditure for your business is not allowed in general, but since

the payment made is less than $10,000 when purchasing capital assets for your business such

expenditure is allowed as a deduction and hence we have to do no adjustments in the adjusted tax

profits therefore it will have no effect in the reconciliation. Since IRD has specified that legal

expense for capital expenditure purpose up to $10,000 are allowed and require no adjustments

for computing adjusted tax profit for the purpose of income tax.

Answer to the 1st part of the Note 8:

No, Dividends paid between NZ wholly owned companies fall under the Exempt income

category as per the Income Tax Act and shall not be forming a part of assessable income and

shall be reduced from accounting profit to eliminate the excessive profit due to such dividends.

5

excess provisional tax paid shall be refunded to the payer, and if the assessed tax is greater than

the provisional tax paid then the balance amount of assessed tax shall be payable.

In the given case for bend-it-physio had paid a provisional tax of $2,775, the same amount shall

be available as a tax credit and it shall be adjusted with the actual tax liability of $6,917 resulting

in reduced final tax liability for the company.

Answer to the 1st part of Note 7:

Legal fees relating to revenue expense or day to day activities are allowed fully as a deduction

whereas legal fees relating to capital expenditure are totally disallowed as per the Income Tax

Act (ATO, 2017). However, if the legal fees so paid for Capital Expenditure does not exceed

$10,000 then such amount is fully allowable as a deduction under the Income Tax Act and will

require no adjustment if such legal expenses do not exceed $10,000 in total for capital

expenditure.

So as per IRD, only payments up to $10,000 are allowed as a deduction for Capital Expenditure.

Answer to the 2nd part of Note 7:

Legal fees relating to capital expenditure for your business is not allowed in general, but since

the payment made is less than $10,000 when purchasing capital assets for your business such

expenditure is allowed as a deduction and hence we have to do no adjustments in the adjusted tax

profits therefore it will have no effect in the reconciliation. Since IRD has specified that legal

expense for capital expenditure purpose up to $10,000 are allowed and require no adjustments

for computing adjusted tax profit for the purpose of income tax.

Answer to the 1st part of the Note 8:

No, Dividends paid between NZ wholly owned companies fall under the Exempt income

category as per the Income Tax Act and shall not be forming a part of assessable income and

shall be reduced from accounting profit to eliminate the excessive profit due to such dividends.

5

Income tax

The act specifically states that such dividends are non-assessable and hence will not be included

in total adjusted tax profit (ATO, 2017).

Answer to the 2nd part of the Note 8:

This will decrease the adjusted tax profit by $9,600 as of this Dividend from the wholly owned

organization is an exempt income and such dividend is not assessable as per the Income Tax Act

2007. Such amount shall be deducted from the Accounting profit and shall be reflected in the

reconciliation statement.

Answer to the 1st part of Note 9:

A person is required to include as assessable income any imputation credits received and is

entitled to a tax credit equal to the amount of the imputation credit. Where a shareholder that is a

company, has excess imputation credits for an income year, the excess credits convert into a loss

to carry forward (Sadiq et. al, 2014. Where an individual shareholder has excess imputation

credits for an income year, the excess credits are carried forward in their current form to the

following income year (ATO, 2018).

In the given case the imputation credits are $1,338 and such credits shall have to be deducted

from the tax liability computed thereon.

Answer to the 2nd part of Note 9:

Refundable tax credits are those that arise from tax payments made by or on behalf of the

taxpayer (including payments for PAYE tax, provisional tax, RWT and non-resident withholding

tax (NRWT)). The full list of refundable tax credits is found within section YA 1 of the Income

Tax Act. Also included are tax credits for families under the Working for Families package, and

tax credits for retirement scheme contribution tax paid (RSCT credits). Some refundable tax

credits are also subject to an ordering rule, such as those arising from PAYE and RWT (ATO,

2017).

In the given case Bend-it-Physio has an RWT credit of $239 on dividends which is included in

the dividend amount. Such amount shall be adjusted towards the total tax payable and hence the

6

The act specifically states that such dividends are non-assessable and hence will not be included

in total adjusted tax profit (ATO, 2017).

Answer to the 2nd part of the Note 8:

This will decrease the adjusted tax profit by $9,600 as of this Dividend from the wholly owned

organization is an exempt income and such dividend is not assessable as per the Income Tax Act

2007. Such amount shall be deducted from the Accounting profit and shall be reflected in the

reconciliation statement.

Answer to the 1st part of Note 9:

A person is required to include as assessable income any imputation credits received and is

entitled to a tax credit equal to the amount of the imputation credit. Where a shareholder that is a

company, has excess imputation credits for an income year, the excess credits convert into a loss

to carry forward (Sadiq et. al, 2014. Where an individual shareholder has excess imputation

credits for an income year, the excess credits are carried forward in their current form to the

following income year (ATO, 2018).

In the given case the imputation credits are $1,338 and such credits shall have to be deducted

from the tax liability computed thereon.

Answer to the 2nd part of Note 9:

Refundable tax credits are those that arise from tax payments made by or on behalf of the

taxpayer (including payments for PAYE tax, provisional tax, RWT and non-resident withholding

tax (NRWT)). The full list of refundable tax credits is found within section YA 1 of the Income

Tax Act. Also included are tax credits for families under the Working for Families package, and

tax credits for retirement scheme contribution tax paid (RSCT credits). Some refundable tax

credits are also subject to an ordering rule, such as those arising from PAYE and RWT (ATO,

2017).

In the given case Bend-it-Physio has an RWT credit of $239 on dividends which is included in

the dividend amount. Such amount shall be adjusted towards the total tax payable and hence the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Income tax

RWT will decrease our tax liability by $239. And this will reflect in our reconciliation after

computing the tax liability.

7

RWT will decrease our tax liability by $239. And this will reflect in our reconciliation after

computing the tax liability.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income tax

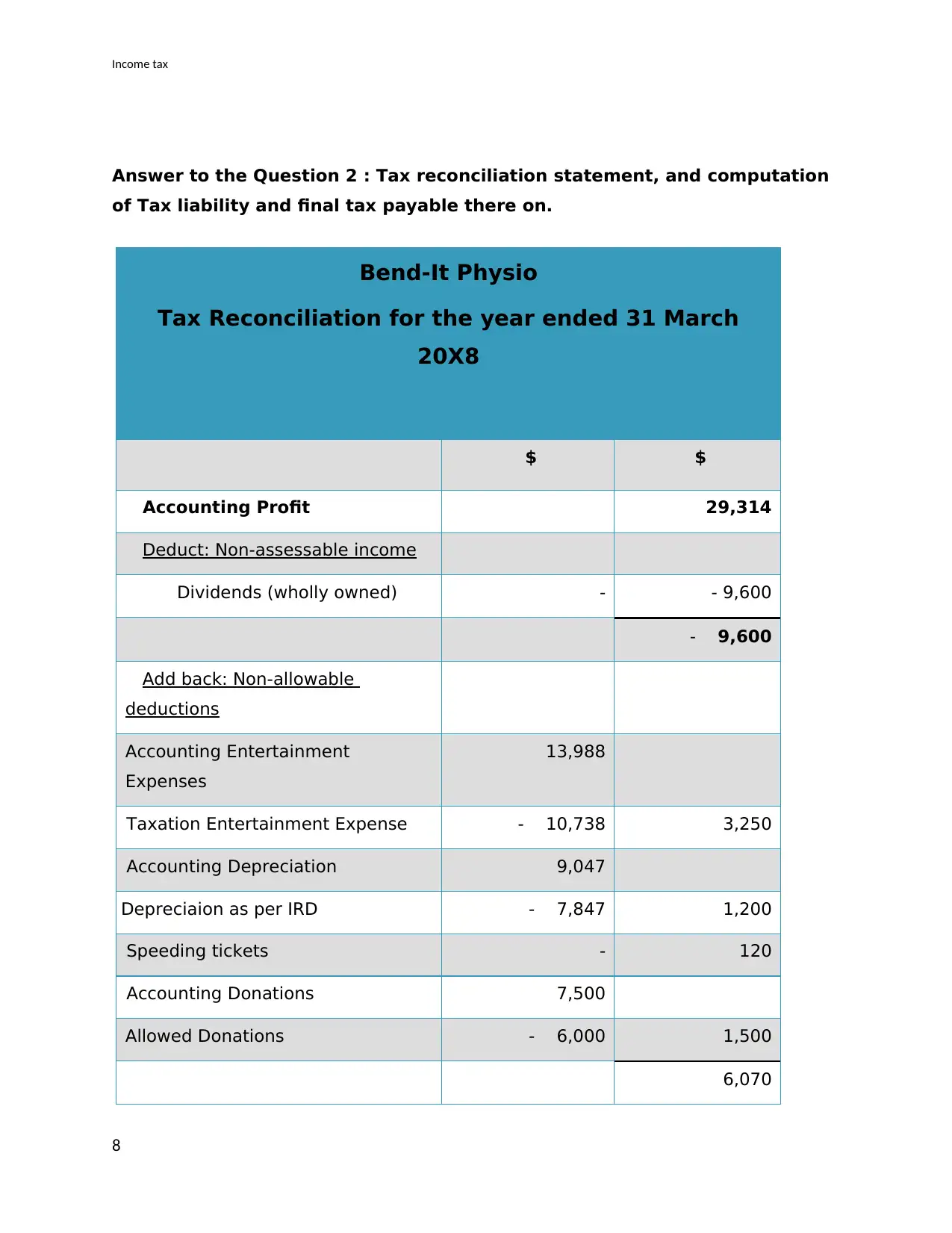

Answer to the Question 2 : Tax reconciliation statement, and computation

of Tax liability and final tax payable there on.

Bend-It Physio

Tax Reconciliation for the year ended 31 March

20X8

$ $

Accounting Profit 29,314

Deduct: Non-assessable income

Dividends (wholly owned) - - 9,600

- 9,600

Add back: Non-allowable

deductions

Accounting Entertainment

Expenses

13,988

Taxation Entertainment Expense - 10,738 3,250

Accounting Depreciation 9,047

Depreciaion as per IRD - 7,847 1,200

Speeding tickets - 120

Accounting Donations 7,500

Allowed Donations - 6,000 1,500

6,070

8

Answer to the Question 2 : Tax reconciliation statement, and computation

of Tax liability and final tax payable there on.

Bend-It Physio

Tax Reconciliation for the year ended 31 March

20X8

$ $

Accounting Profit 29,314

Deduct: Non-assessable income

Dividends (wholly owned) - - 9,600

- 9,600

Add back: Non-allowable

deductions

Accounting Entertainment

Expenses

13,988

Taxation Entertainment Expense - 10,738 3,250

Accounting Depreciation 9,047

Depreciaion as per IRD - 7,847 1,200

Speeding tickets - 120

Accounting Donations 7,500

Allowed Donations - 6,000 1,500

6,070

8

Income tax

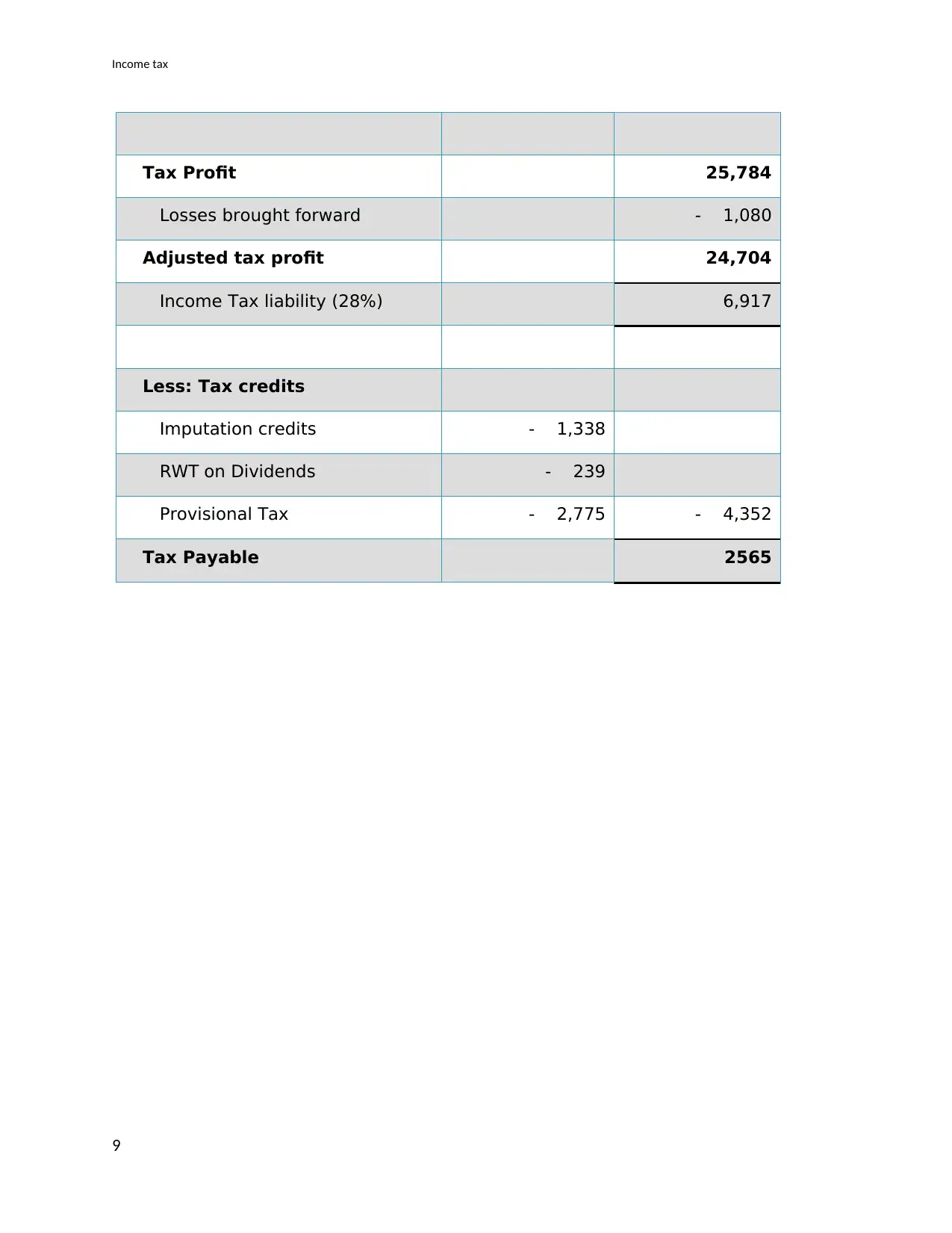

Tax Profit 25,784

Losses brought forward - 1,080

Adjusted tax profit 24,704

Income Tax liability (28%) 6,917

Less: Tax credits

Imputation credits - 1,338

RWT on Dividends - 239

Provisional Tax - 2,775 - 4,352

Tax Payable 2565

9

Tax Profit 25,784

Losses brought forward - 1,080

Adjusted tax profit 24,704

Income Tax liability (28%) 6,917

Less: Tax credits

Imputation credits - 1,338

RWT on Dividends - 239

Provisional Tax - 2,775 - 4,352

Tax Payable 2565

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Income tax

Answer 3

Reconciliation is needed because accounting profit takes into account the different items and

uses different amounts than that permissible by the Income Tax Act 2007 and IRD. The

difference between accounting profit before tax in the income statement and the adjusted tax

profit relates to the non-assessable income items and the non-allowable expenses that shall be

adjusted (Pratt & Kulsrud, 2013). Rather than creating a whole new income statement following

taxation rules, we work backward from the current Accounting Profit before tax to work out the

taxable profit. So effectively we calculate the tax profit by reversing out the income and

expenses that are not allowed for tax purposes (ATO, 2018).

Thus a process of reconciliation is required. This entails a series of adjustments. The process,

simply put, is one of deciding what is to be included in the profit and what should be put out of

the profit (Pratt & Kulsrud, 2013). The result is a series of increasing and decreasing the

adjustments from the Accounting profits to get the adjusted profit for the purpose of tax

computation as per the Income Tax Act, 2007.

Importantly, it is an accounting profit that is modified to get to taxable income. This means that

any adjustments must work with items set out in the profit and loss account or statement to arrive

the adjusted tax profit which is basically the purpose of Reconciliation Statement.

10

Answer 3

Reconciliation is needed because accounting profit takes into account the different items and

uses different amounts than that permissible by the Income Tax Act 2007 and IRD. The

difference between accounting profit before tax in the income statement and the adjusted tax

profit relates to the non-assessable income items and the non-allowable expenses that shall be

adjusted (Pratt & Kulsrud, 2013). Rather than creating a whole new income statement following

taxation rules, we work backward from the current Accounting Profit before tax to work out the

taxable profit. So effectively we calculate the tax profit by reversing out the income and

expenses that are not allowed for tax purposes (ATO, 2018).

Thus a process of reconciliation is required. This entails a series of adjustments. The process,

simply put, is one of deciding what is to be included in the profit and what should be put out of

the profit (Pratt & Kulsrud, 2013). The result is a series of increasing and decreasing the

adjustments from the Accounting profits to get the adjusted profit for the purpose of tax

computation as per the Income Tax Act, 2007.

Importantly, it is an accounting profit that is modified to get to taxable income. This means that

any adjustments must work with items set out in the profit and loss account or statement to arrive

the adjusted tax profit which is basically the purpose of Reconciliation Statement.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income tax

References

ATO. (2017) Reducing the Corporate rate tax. Available from

https://www.ato.gov.au/General/New-legislation/In-detail/Direct-taxes/Income-tax-for-

businesses/Reducing-the-corporate-tax-rate/ [Accessed 30 June 2019]

ATO. (2018) Accessing your payment summary. Available from:

https://www.ato.gov.au/Individuals/Working/Working-as-an-employee/Accessing-your-

payment-summary/ [Accessed 30 June 2019]

Mayo, W. (2018) Time to Upgrade Australia’s Company Tax System From Imputation to

Integration. Australian Tax Forum, 33(4), 1-57. Available from:

https://ssrn.com/abstract=3311250 [Accessed 30 June 2019]

Nethercott, L., Richardson, G.,& Devos,K. (2013) Australian Taxation Study Manual. Oxford

university Press

Pratt, J. W. and Kulsrud, W. N. (2013) Federal Taxation. Penguin Publishers

Sadiq,K., Coleman, C., Hanegbi, R., Jogarajan,S., Krever, R.,Obst, W., & Ting, A. (2014)

Principles of Taxation Law. Sydney.

Wells, J.T. (2011), Corporate Fraud Handbook: Prevention and Detection; John Wiley & Sons,

Hoboken, NJ.

11

References

ATO. (2017) Reducing the Corporate rate tax. Available from

https://www.ato.gov.au/General/New-legislation/In-detail/Direct-taxes/Income-tax-for-

businesses/Reducing-the-corporate-tax-rate/ [Accessed 30 June 2019]

ATO. (2018) Accessing your payment summary. Available from:

https://www.ato.gov.au/Individuals/Working/Working-as-an-employee/Accessing-your-

payment-summary/ [Accessed 30 June 2019]

Mayo, W. (2018) Time to Upgrade Australia’s Company Tax System From Imputation to

Integration. Australian Tax Forum, 33(4), 1-57. Available from:

https://ssrn.com/abstract=3311250 [Accessed 30 June 2019]

Nethercott, L., Richardson, G.,& Devos,K. (2013) Australian Taxation Study Manual. Oxford

university Press

Pratt, J. W. and Kulsrud, W. N. (2013) Federal Taxation. Penguin Publishers

Sadiq,K., Coleman, C., Hanegbi, R., Jogarajan,S., Krever, R.,Obst, W., & Ting, A. (2014)

Principles of Taxation Law. Sydney.

Wells, J.T. (2011), Corporate Fraud Handbook: Prevention and Detection; John Wiley & Sons,

Hoboken, NJ.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.