Polytechnic Institute Australia: Exhibition Furniture Case Study

VerifiedAdded on 2023/06/15

|12

|825

|54

Case Study

AI Summary

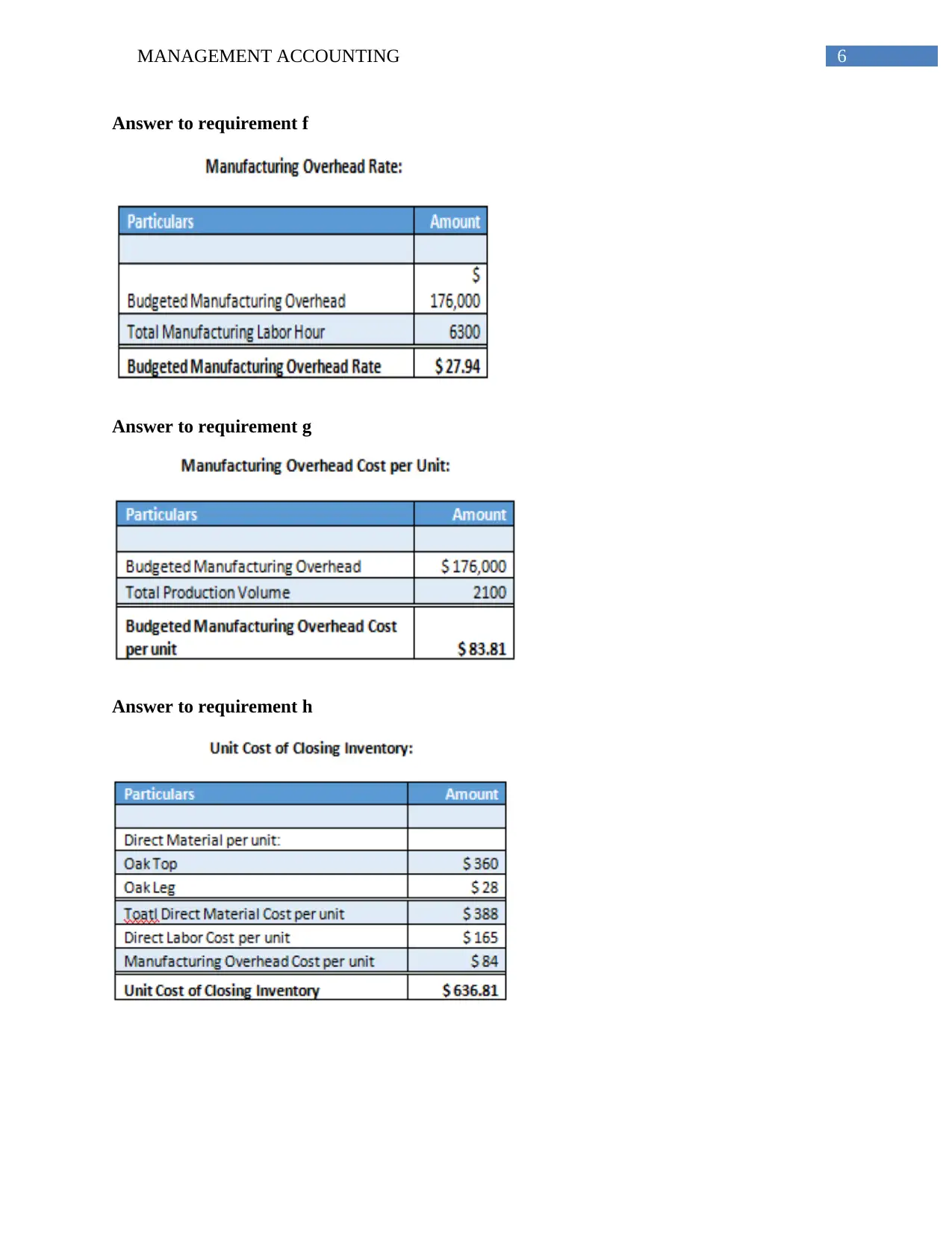

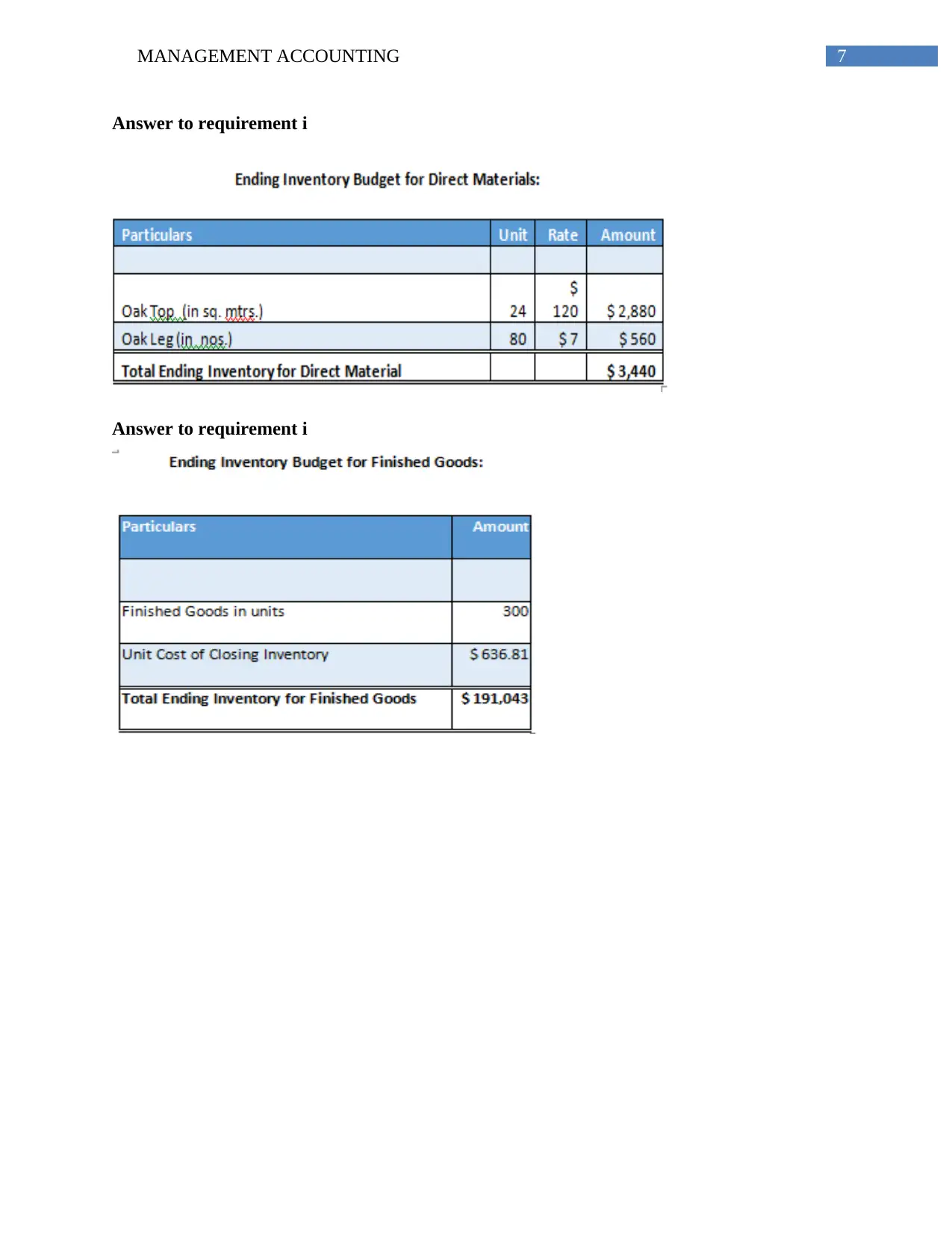

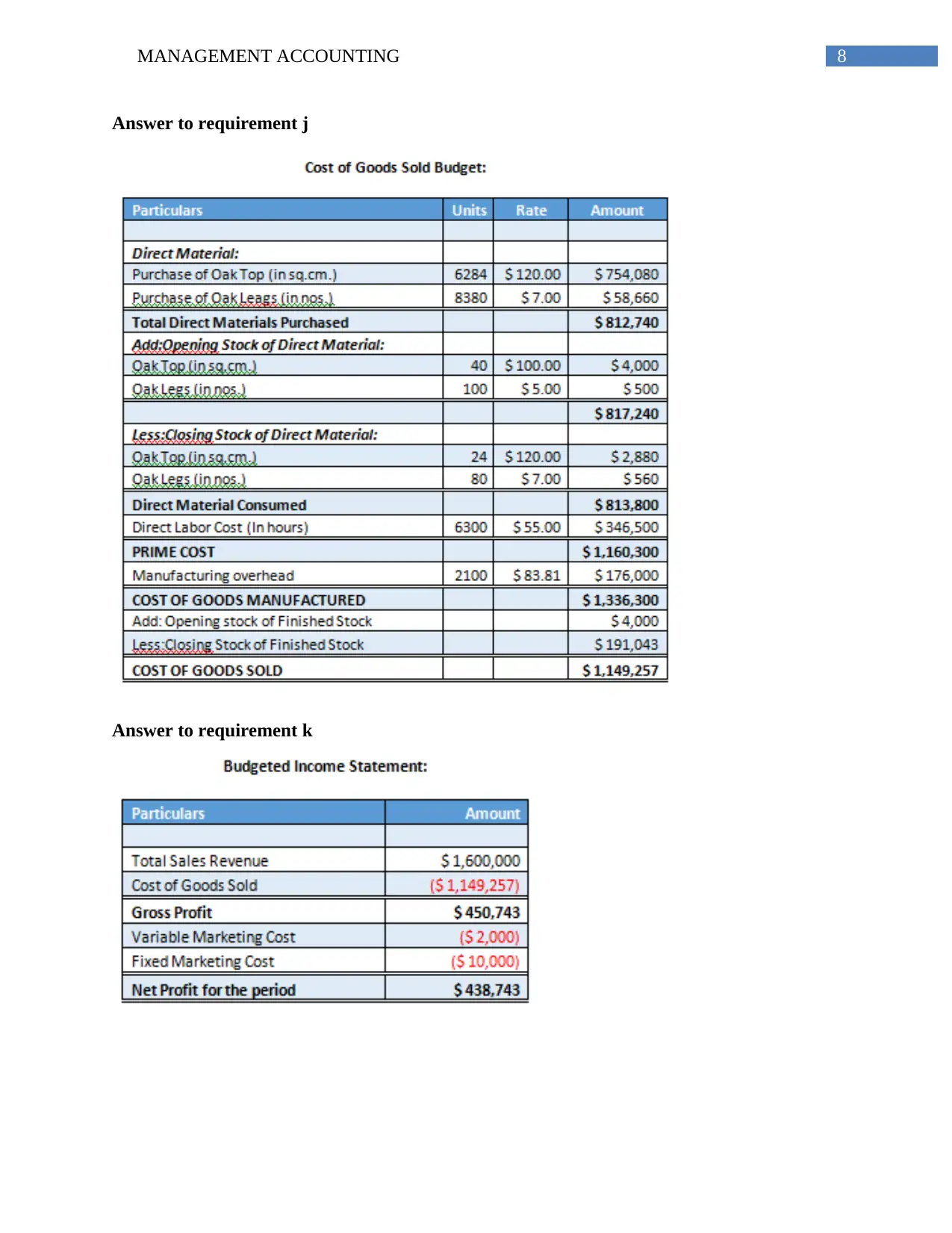

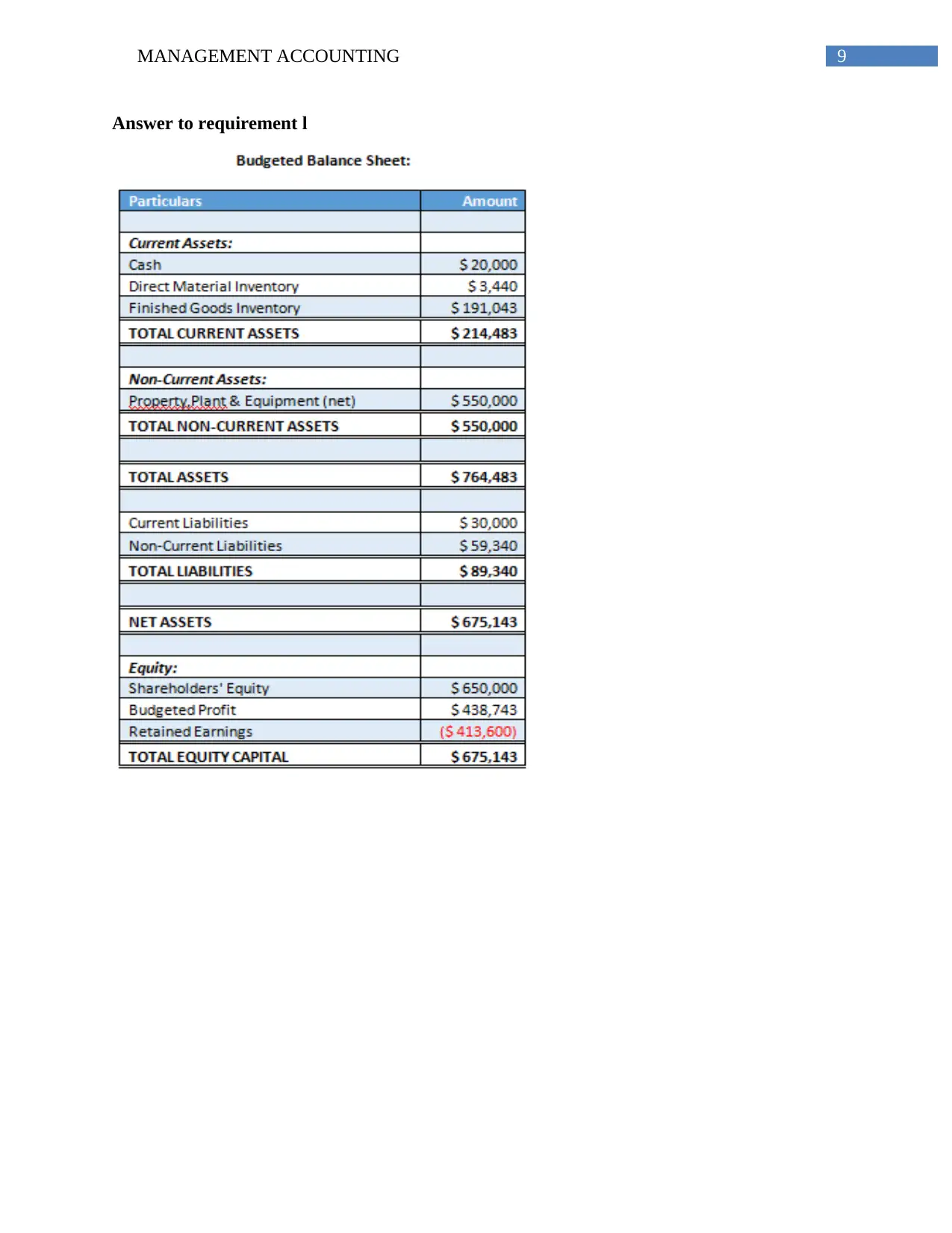

This document presents a comprehensive solution to a management accounting case study focused on Exhibition Furniture. The solution includes an analysis of the company's budget, recommendations for continuous improvement, and a business memorandum addressed to the CEO. The memorandum suggests implementing quarterly budgets for better short-term goal management and conducting variance analysis to identify areas for cost reduction and improved financial performance. The analysis covers various aspects of management accounting, providing a detailed understanding of the company's financial situation and potential strategies for enhancement. Desklib offers a platform for students to access similar solved assignments and past papers.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.