Financial Performance and Position of G8 Education: Accounting Report

VerifiedAdded on 2022/08/26

|10

|1669

|19

Report

AI Summary

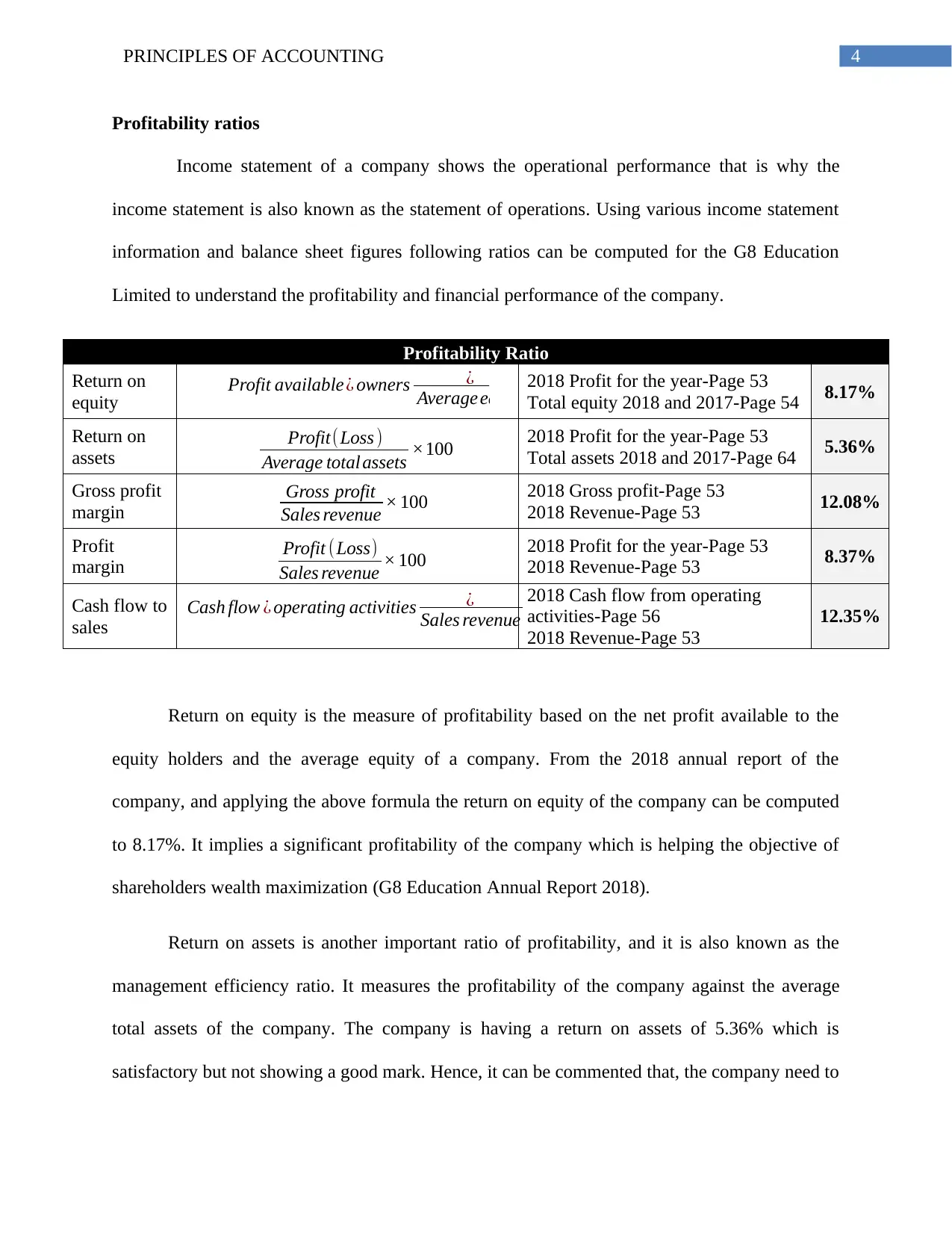

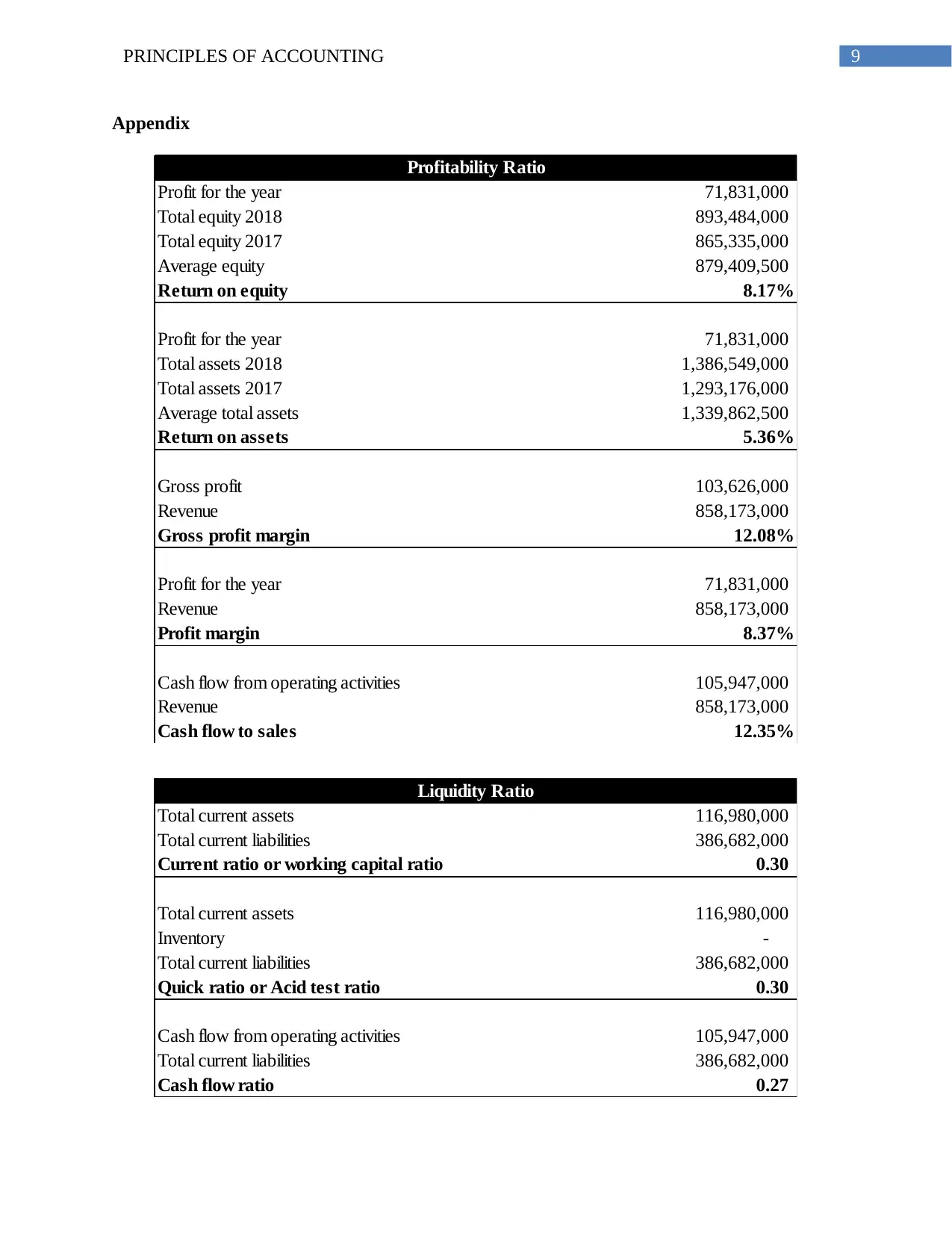

This report provides a financial analysis of G8 Education, focusing on its performance and position. It utilizes ratio analysis, specifically examining profitability and liquidity. Profitability ratios, including return on equity, return on assets, gross profit margin, profit margin, and cash flow to sales, are computed and analyzed to assess the company's operational efficiency and shareholder returns. Liquidity ratios, such as current ratio, quick ratio, and cash flow ratio, are used to evaluate the company's short-term solvency and ability to meet its obligations. The analysis reveals insights into G8 Education's strengths, weaknesses, and overall financial health, concluding with recommendations for improvement. The report highlights the company's sustainable growth and revenue increase, but also points out areas where enhanced financial management could improve profitability and liquidity, ultimately contributing to shareholder wealth maximization.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.