Financial Analysis and Budget Report for Gaia Ltd.

VerifiedAdded on 2023/06/08

|9

|1521

|142

Report

AI Summary

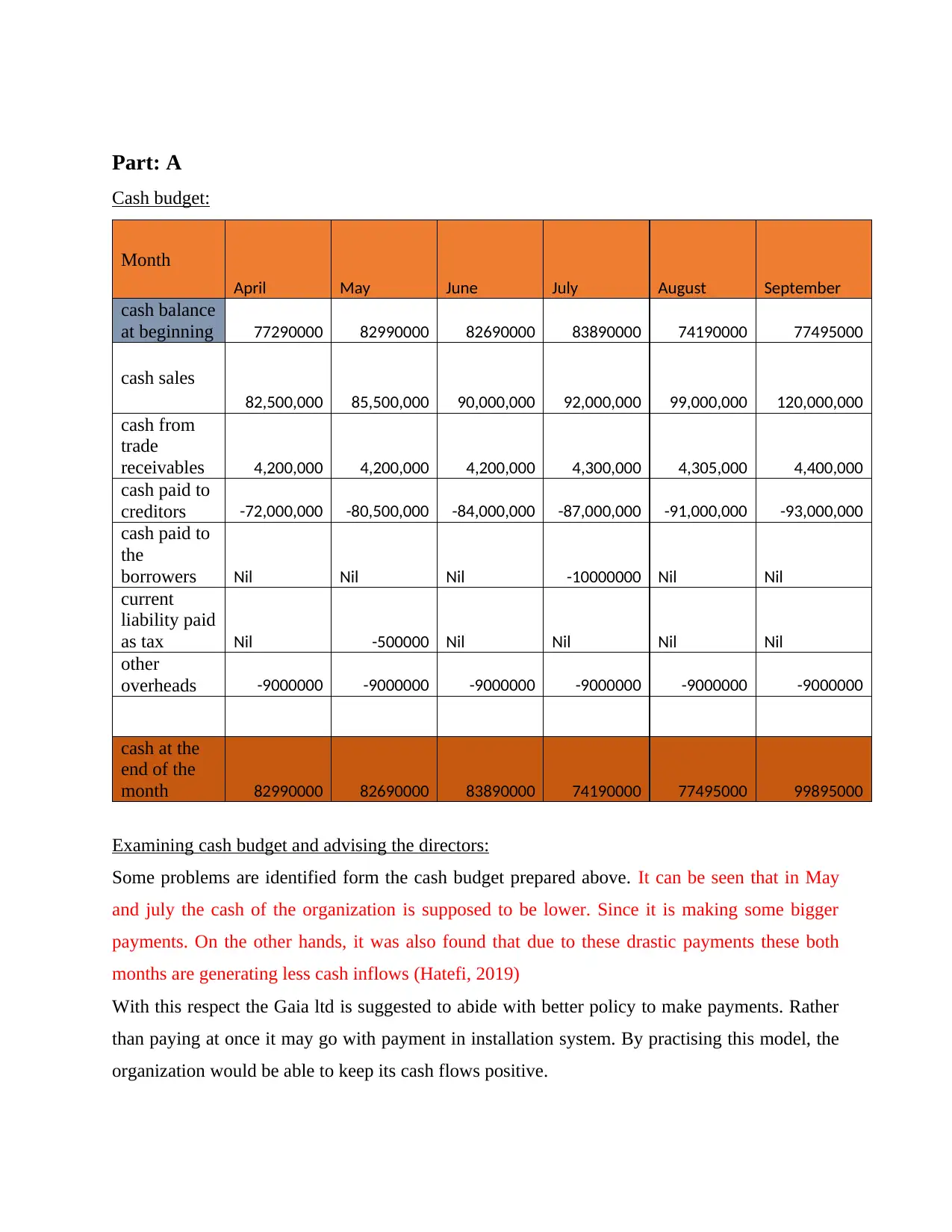

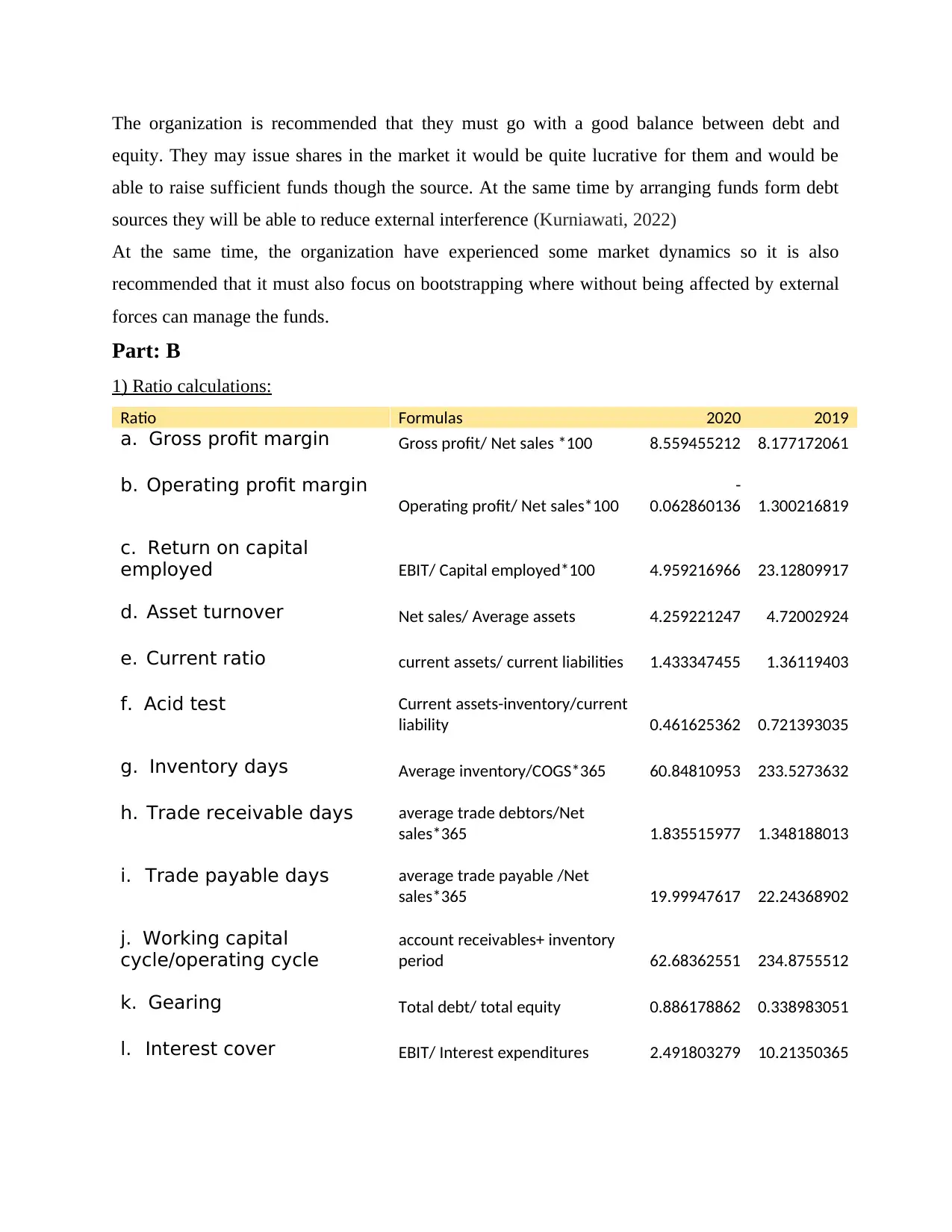

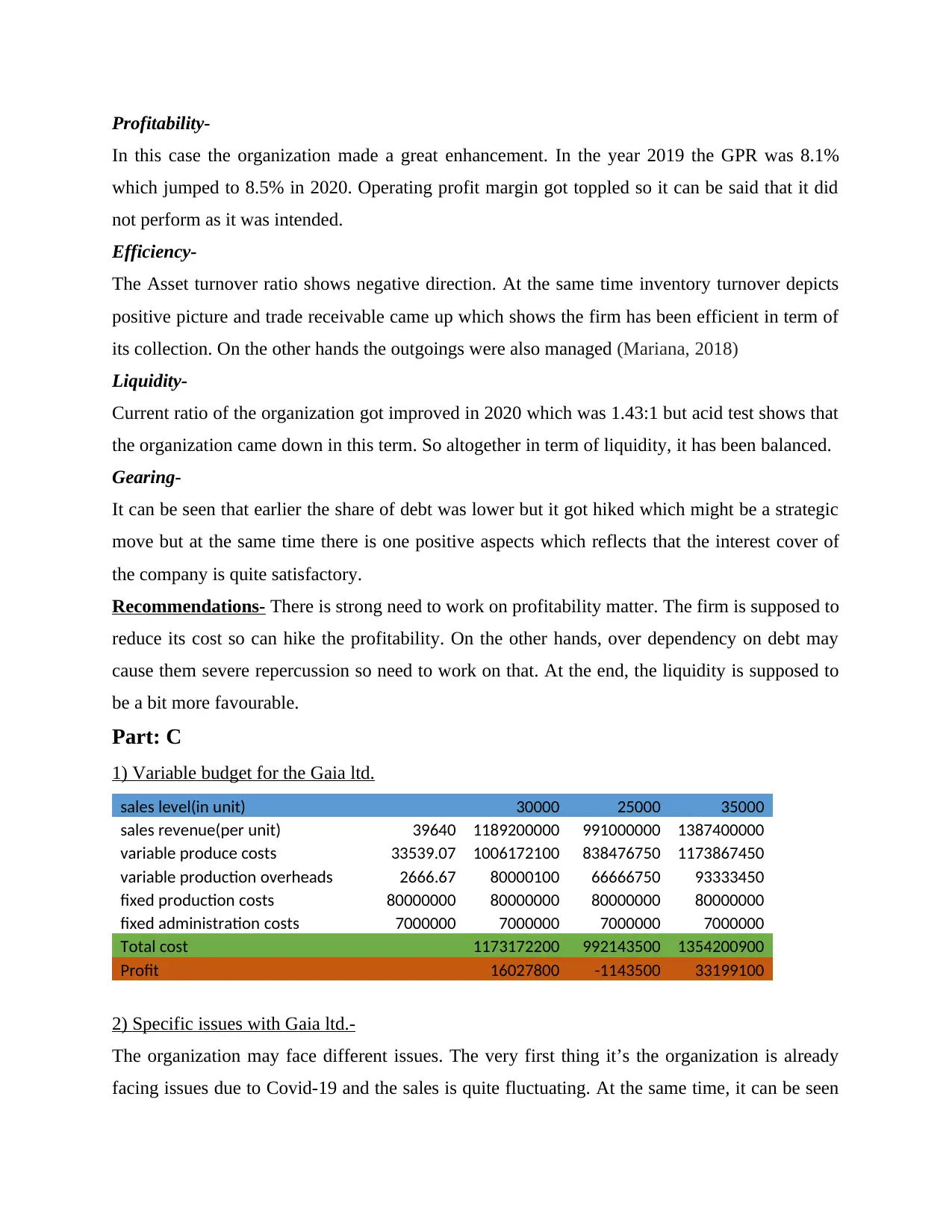

This report presents a detailed budget analysis for Gaia Ltd., encompassing a cash flow budget, ratio calculations, and a variable budget. The cash flow analysis identifies potential cash flow problems, particularly in May and July, and recommends payment strategies to maintain positive cash flow. The report explores various funding sources, including issuing shares, debt funds, and bootstrapping, evaluating their advantages and disadvantages. Ratio calculations assess profitability, efficiency, liquidity, and gearing, comparing 2019 and 2020 data to reveal performance trends. Recommendations are provided to improve profitability, manage debt, and enhance liquidity. The variable budget section examines different sales levels and their impact on profit, highlighting the challenges Gaia Ltd. faces, particularly regarding fluctuating sales and the sensitivity of profit to production levels. The report offers specific recommendations to address the issues, aiming to improve the company's financial stability and performance.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.