Comprehensive Analysis of Management Accounting for Galway Plc

VerifiedAdded on 2021/02/19

|14

|5174

|45

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and practices, focusing on their application within Galway Plc. It begins by defining management accounting and outlining its essential requirements, including cost accounting, inventory management, job costing, and price optimization systems. The report then explores various reporting methods used in management accounting, such as budget reports, performance reports, accounts receivable reports, and cost management reports. A significant portion of the report is dedicated to the calculation of income statements under both marginal and absorption costing methods, providing detailed examples for May and June. It also examines the advantages and disadvantages of different planning tools used for budgetary control and discusses how management accounting systems can be used to respond to financial problems. The report concludes by emphasizing the role of management accounting in achieving organizational success and includes detailed financial calculations and comparisons to illustrate key concepts.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P 1. Explaining the concept of management accounting and the essential requirements of its system

..........................................................................................................................................................3

P 2. Explaining several methods that are used for reporting under management accounting. .......4

LO 2.................................................................................................................................................5

P 3 Calculation of income statement under marginal and absorption costing.................................5

LO 3.................................................................................................................................................9

P 4 Advantages and Disadvantages of different types of planning tools used for budgetary control

.........................................................................................................................................................9

LO 4...............................................................................................................................................10

P 5. Discussing management accounting system for responding financial problems...................10

M 4. Analysing management accounting assist in achieving organisation success.......................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P 1. Explaining the concept of management accounting and the essential requirements of its system

..........................................................................................................................................................3

P 2. Explaining several methods that are used for reporting under management accounting. .......4

LO 2.................................................................................................................................................5

P 3 Calculation of income statement under marginal and absorption costing.................................5

LO 3.................................................................................................................................................9

P 4 Advantages and Disadvantages of different types of planning tools used for budgetary control

.........................................................................................................................................................9

LO 4...............................................................................................................................................10

P 5. Discussing management accounting system for responding financial problems...................10

M 4. Analysing management accounting assist in achieving organisation success.......................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management Accounting is the process where all the transactions are prepared for the

company for preparation of financial statements. It takes into account various accounting techniques

such as cost accounting, management accounting and financial accounting (Management

Accounting, 2019). Galway plc. Is the company which serves its clients in various sectors such as

hospitality, construction, retail etc. in order to make them decision making in particular area. This

report covers various planning tools for budgetary control. The application of various cost

ascertainment methods such as marginal costing and absorption method. Using these methods

company can come to financial problem of the company and how to respond those financial

problems. It also covers the need of management accounting and how it can be used in the

organisation and what are benefits if any company is using these tools. The company uses LIFO

method for the valuation of closing inventory which assumes that the goods brought by the

company are first sold out. Company also compare the budgeted performance and actual

performance of the company. It helps in knowing the company that the budget prepared is under

budgeted or over budgeted.

LO 1

P 1. Explaining the concept of management accounting and the essential requirements of its system

Management accounting refers to the presentation of the accounting information for

the purpose of formulating policies that are been adopted by management and in running the routine

activities (McLaren, Appleyard and Mitchell, 2016). It helps the management of the organization in

performing all its function effectively and efficiently that includes the planning, staffing,

controlling, organizing and directing. It is also called as cost accounting as it provides for the

analyses of business cost and the assessment of the operations in order to prepare the internal report

which in turn helps the management in making the decisions for achieving the goals of the business.

There are various management accounting systems that plays a vital role in smooth functioning of

the business as follows-

Cost accounting system- It refers to the system that estimate the product cost for making the

analysis of the profit, valuing the inventory and controlling the cost. This system is critical for the

company as it helps in ascertaining the accurate cost in producing the product. Cost accounting

system is classified into two major parts that include process costing and job order costing. The

former accumulates the manufacturing cost for each of the process separately and the latter

accumulates the cost for each of the job separately.

Inventory management system- It is the software system that maintains the record and the

Management Accounting is the process where all the transactions are prepared for the

company for preparation of financial statements. It takes into account various accounting techniques

such as cost accounting, management accounting and financial accounting (Management

Accounting, 2019). Galway plc. Is the company which serves its clients in various sectors such as

hospitality, construction, retail etc. in order to make them decision making in particular area. This

report covers various planning tools for budgetary control. The application of various cost

ascertainment methods such as marginal costing and absorption method. Using these methods

company can come to financial problem of the company and how to respond those financial

problems. It also covers the need of management accounting and how it can be used in the

organisation and what are benefits if any company is using these tools. The company uses LIFO

method for the valuation of closing inventory which assumes that the goods brought by the

company are first sold out. Company also compare the budgeted performance and actual

performance of the company. It helps in knowing the company that the budget prepared is under

budgeted or over budgeted.

LO 1

P 1. Explaining the concept of management accounting and the essential requirements of its system

Management accounting refers to the presentation of the accounting information for

the purpose of formulating policies that are been adopted by management and in running the routine

activities (McLaren, Appleyard and Mitchell, 2016). It helps the management of the organization in

performing all its function effectively and efficiently that includes the planning, staffing,

controlling, organizing and directing. It is also called as cost accounting as it provides for the

analyses of business cost and the assessment of the operations in order to prepare the internal report

which in turn helps the management in making the decisions for achieving the goals of the business.

There are various management accounting systems that plays a vital role in smooth functioning of

the business as follows-

Cost accounting system- It refers to the system that estimate the product cost for making the

analysis of the profit, valuing the inventory and controlling the cost. This system is critical for the

company as it helps in ascertaining the accurate cost in producing the product. Cost accounting

system is classified into two major parts that include process costing and job order costing. The

former accumulates the manufacturing cost for each of the process separately and the latter

accumulates the cost for each of the job separately.

Inventory management system- It is the software system that maintains the record and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

details relating to the inventory of the firm (Hoozée and Mitchell, 2018). It is important for every

organization to adopt this system as it helps in tracking or tracing the level of inventory, sales,

deliveries and the order. It could also be used by the industry for creating the work order, documents

relating to production and material bill.

Job costing system- It involves the accumulation of the information relating to the cost

attached with particular production or the service. Job costing system is essential for the

organization as it provides the vital information which is required for submitting the information in

relation to the cost to the customer under the contract where the cost are been reimbursed. This

information is also considered as useful in order to determine the accuracy in the estimating system

of an entity. This in turn helps in quoting and fixing the suitable price that generates larger profits. It

is also used for assigning the cost the goods manufactured within the premises of the enterprise.

Price optimization system- It is the mathematical tool that is used by the organization for

determining the response of the customers at different price level for the products and the services

through the different channels (Chenhall and Moers, 2015). It is important for the company to adopt

price optimization system as it is the best way to assess the demand and in fixing the price that is

best in meeting the objectives like profit maximization.

P 2. Explaining several methods that are used for reporting under management accounting.

Managerial accounting includes the preparation of the reports that are used as the base for

planning, decision making, regulating and in measuring the performance (Maas, Schaltegger and

Crutzen, 2016). Reports are been continuously generated for the overall accounting and the

bookkeeping period as per the requirements. Managers of the organization uses these reports for

highlighting certain patterns or translating it into the useful information for the enterprise. There are

various management accounting reports as follows-

Budget report- It means the report that describes the budget regarding the expenses so that

control over the spending can be attained. Budget report is critical for measuring the performance of

the company and in generating the higher profitability in the overall business. Estimations in this

report are made on the basis of the previous experiences. This helps the organization in meeting

with the unforeseen event or the conditions in the future.

Performance report- This report includes the information relating to the performance of the

employees and the organization. Managers uses this report for making the strategic decisions

relating to the future of company. It also provides the deep insights towards the working of the

enterprise. Performance report plays an essential role in keeping an accurate measure of the strategy

towards the mission.

Accounts receivable report- This management accounting report includes the information

organization to adopt this system as it helps in tracking or tracing the level of inventory, sales,

deliveries and the order. It could also be used by the industry for creating the work order, documents

relating to production and material bill.

Job costing system- It involves the accumulation of the information relating to the cost

attached with particular production or the service. Job costing system is essential for the

organization as it provides the vital information which is required for submitting the information in

relation to the cost to the customer under the contract where the cost are been reimbursed. This

information is also considered as useful in order to determine the accuracy in the estimating system

of an entity. This in turn helps in quoting and fixing the suitable price that generates larger profits. It

is also used for assigning the cost the goods manufactured within the premises of the enterprise.

Price optimization system- It is the mathematical tool that is used by the organization for

determining the response of the customers at different price level for the products and the services

through the different channels (Chenhall and Moers, 2015). It is important for the company to adopt

price optimization system as it is the best way to assess the demand and in fixing the price that is

best in meeting the objectives like profit maximization.

P 2. Explaining several methods that are used for reporting under management accounting.

Managerial accounting includes the preparation of the reports that are used as the base for

planning, decision making, regulating and in measuring the performance (Maas, Schaltegger and

Crutzen, 2016). Reports are been continuously generated for the overall accounting and the

bookkeeping period as per the requirements. Managers of the organization uses these reports for

highlighting certain patterns or translating it into the useful information for the enterprise. There are

various management accounting reports as follows-

Budget report- It means the report that describes the budget regarding the expenses so that

control over the spending can be attained. Budget report is critical for measuring the performance of

the company and in generating the higher profitability in the overall business. Estimations in this

report are made on the basis of the previous experiences. This helps the organization in meeting

with the unforeseen event or the conditions in the future.

Performance report- This report includes the information relating to the performance of the

employees and the organization. Managers uses this report for making the strategic decisions

relating to the future of company. It also provides the deep insights towards the working of the

enterprise. Performance report plays an essential role in keeping an accurate measure of the strategy

towards the mission.

Accounts receivable report- This management accounting report includes the information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

regarding the balances that need to be collected by the enterprise against the sales made by its to its

customers and the distributors (Stacchezzini, Melloni and Lai, 2016). It helps in finding out the

details regarding the defaulters for the purpose of tightening the credit policies because cash flow is

very critical for the efficient management of the business.

Cost management reports- This report computes the manufacturing cost of the articles. It

includes the cost of the raw material, labour cost, overhead cost or any other cost. Cost report

facilitates the information regarding these cost. It helps the managers in realizing the prices of the

cost against the selling price of the product. The margins of the profit are been estimated and are

monitored through the use of this report as it provides for the clear picture relating to each and

every cost that incurred in the process of the production and in procurement of the articles. This

report provides the exact understanding relating to all the expenses that is important for achieving

optimum utilization of the resources among the different departments.

LO 2

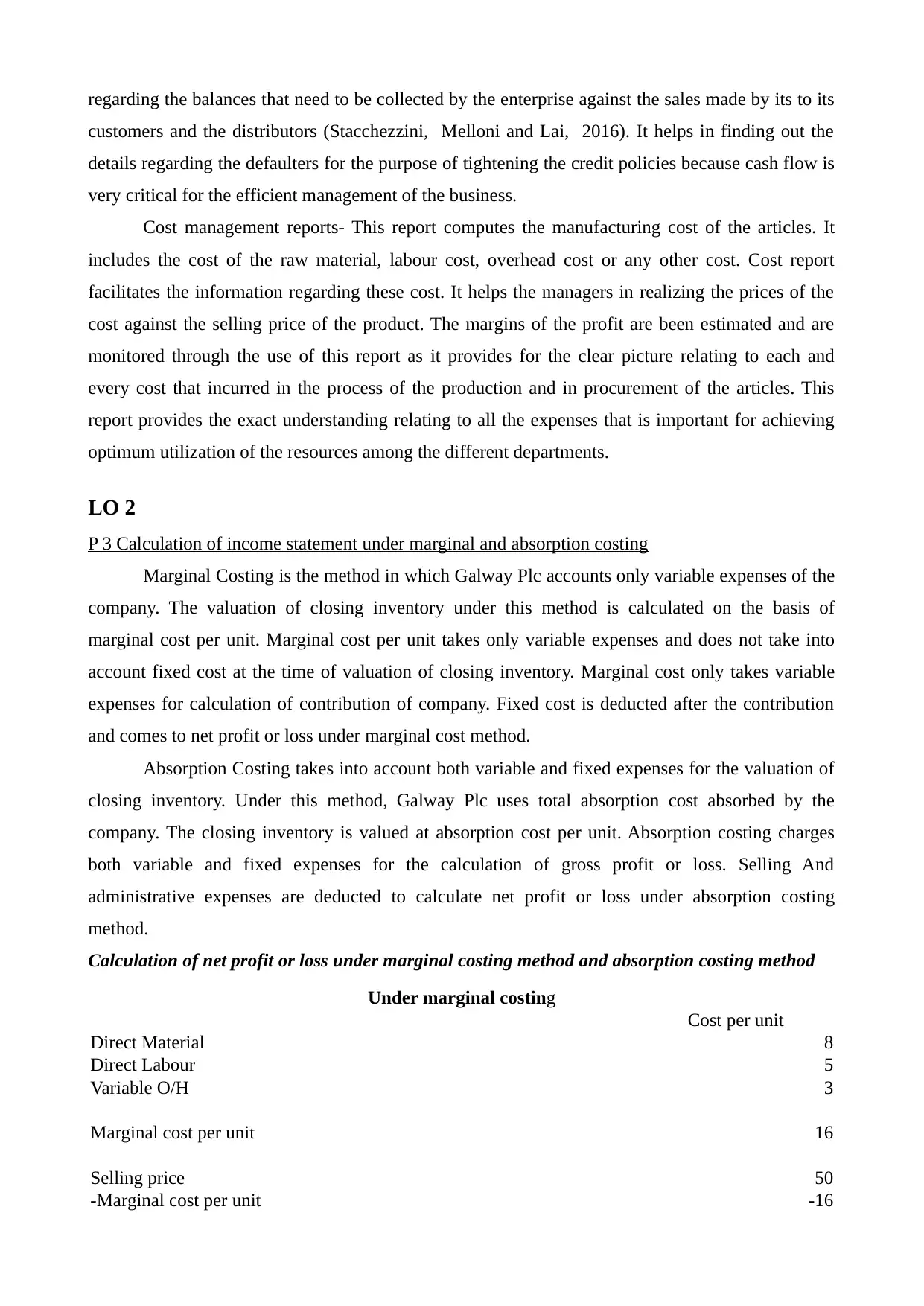

P 3 Calculation of income statement under marginal and absorption costing

Marginal Costing is the method in which Galway Plc accounts only variable expenses of the

company. The valuation of closing inventory under this method is calculated on the basis of

marginal cost per unit. Marginal cost per unit takes only variable expenses and does not take into

account fixed cost at the time of valuation of closing inventory. Marginal cost only takes variable

expenses for calculation of contribution of company. Fixed cost is deducted after the contribution

and comes to net profit or loss under marginal cost method.

Absorption Costing takes into account both variable and fixed expenses for the valuation of

closing inventory. Under this method, Galway Plc uses total absorption cost absorbed by the

company. The closing inventory is valued at absorption cost per unit. Absorption costing charges

both variable and fixed expenses for the calculation of gross profit or loss. Selling And

administrative expenses are deducted to calculate net profit or loss under absorption costing

method.

Calculation of net profit or loss under marginal costing method and absorption costing method

Under marginal costing

Cost per unit

Direct Material 8

Direct Labour 5

Variable O/H 3

Marginal cost per unit 16

Selling price 50

-Marginal cost per unit -16

customers and the distributors (Stacchezzini, Melloni and Lai, 2016). It helps in finding out the

details regarding the defaulters for the purpose of tightening the credit policies because cash flow is

very critical for the efficient management of the business.

Cost management reports- This report computes the manufacturing cost of the articles. It

includes the cost of the raw material, labour cost, overhead cost or any other cost. Cost report

facilitates the information regarding these cost. It helps the managers in realizing the prices of the

cost against the selling price of the product. The margins of the profit are been estimated and are

monitored through the use of this report as it provides for the clear picture relating to each and

every cost that incurred in the process of the production and in procurement of the articles. This

report provides the exact understanding relating to all the expenses that is important for achieving

optimum utilization of the resources among the different departments.

LO 2

P 3 Calculation of income statement under marginal and absorption costing

Marginal Costing is the method in which Galway Plc accounts only variable expenses of the

company. The valuation of closing inventory under this method is calculated on the basis of

marginal cost per unit. Marginal cost per unit takes only variable expenses and does not take into

account fixed cost at the time of valuation of closing inventory. Marginal cost only takes variable

expenses for calculation of contribution of company. Fixed cost is deducted after the contribution

and comes to net profit or loss under marginal cost method.

Absorption Costing takes into account both variable and fixed expenses for the valuation of

closing inventory. Under this method, Galway Plc uses total absorption cost absorbed by the

company. The closing inventory is valued at absorption cost per unit. Absorption costing charges

both variable and fixed expenses for the calculation of gross profit or loss. Selling And

administrative expenses are deducted to calculate net profit or loss under absorption costing

method.

Calculation of net profit or loss under marginal costing method and absorption costing method

Under marginal costing

Cost per unit

Direct Material 8

Direct Labour 5

Variable O/H 3

Marginal cost per unit 16

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.50

Contribution per unit 31.50

May

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable o/h (500*3) 1500

8000

-Closing inventory (200*16) -3200.00

-4800

10200

-Variable selling cost -750

Contribution 9450

-Fixed costs -4000

Actual Net profit/(Net Loss) 5450

June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs -4000

Actual Net profit/(Net Loss) 11750

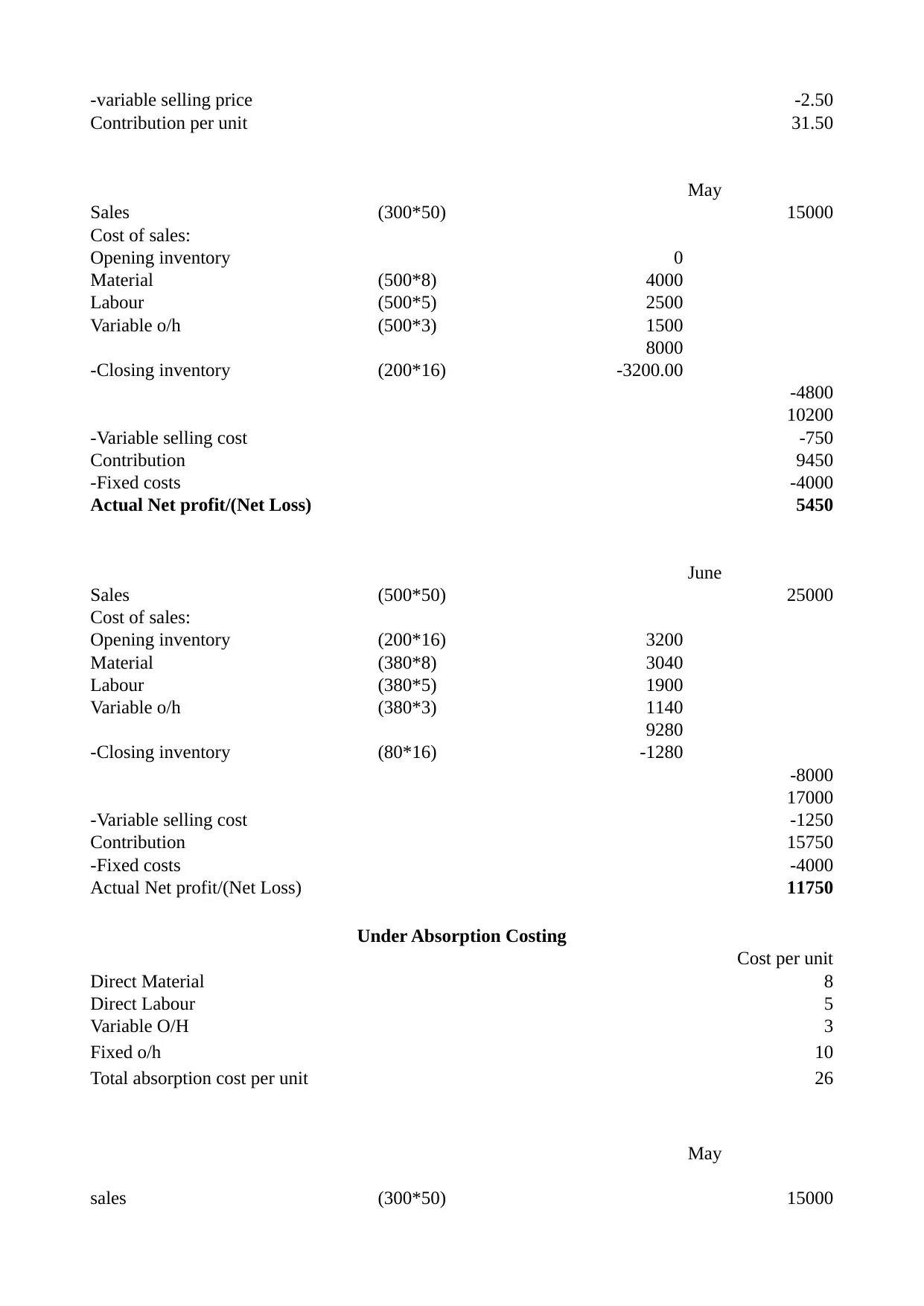

Under Absorption Costing

Cost per unit

Direct Material 8

Direct Labour 5

Variable O/H 3

Fixed o/h 10

Total absorption cost per unit 26

May

sales (300*50) 15000

Contribution per unit 31.50

May

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable o/h (500*3) 1500

8000

-Closing inventory (200*16) -3200.00

-4800

10200

-Variable selling cost -750

Contribution 9450

-Fixed costs -4000

Actual Net profit/(Net Loss) 5450

June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs -4000

Actual Net profit/(Net Loss) 11750

Under Absorption Costing

Cost per unit

Direct Material 8

Direct Labour 5

Variable O/H 3

Fixed o/h 10

Total absorption cost per unit 26

May

sales (300*50) 15000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed o/h 4000

Variable o/h (500*3) 1500

12000

-Closing inventory (200*26) -5200

-6800

Gross Profit/Loss 8200

-Variable selling cost -750

Actual Net profit/(Net Loss) 7450

June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*26) 5200

Material (380*8) 3040

Labour (380*5) 1900

Fixed o/h 4000

Variable o/h (380*3) 1140

15280

-Closing inventory (80*26) -2080

-13200

Gross Profit/Loss 11800

-Variable selling cost -1250

Actual Net profit/(Net Loss) 10550

Galway Plc use two methods for calculating cost and calculation of actual net profit/ (loss)

are also been calculated. Under this method in marginal costing fixed costs and fixed selling costs

both are deducted after the gross profit (Aleem and et.al., 2016). In month of may Galway Plc net

profit under absorption cost is more than the marginal costing. It is because of Fixed cost is allotted

at cost per unit whereas in marginal costing total fixed cost is allotted whether the total fixed cost is

allotted or not. In the month of June net profit under absorption costing is less than the net profit

under marginal costing. It is because of valuation of opening inventory under marginal costing is

undervalued than the valuation of opening inventory under absorption costing method. In

absorption costing fixed expenses are deducted before the gross profit (Fisher and et.al., 2015).

Company can use any method to calculate costs the actual profits calculated will be same only.

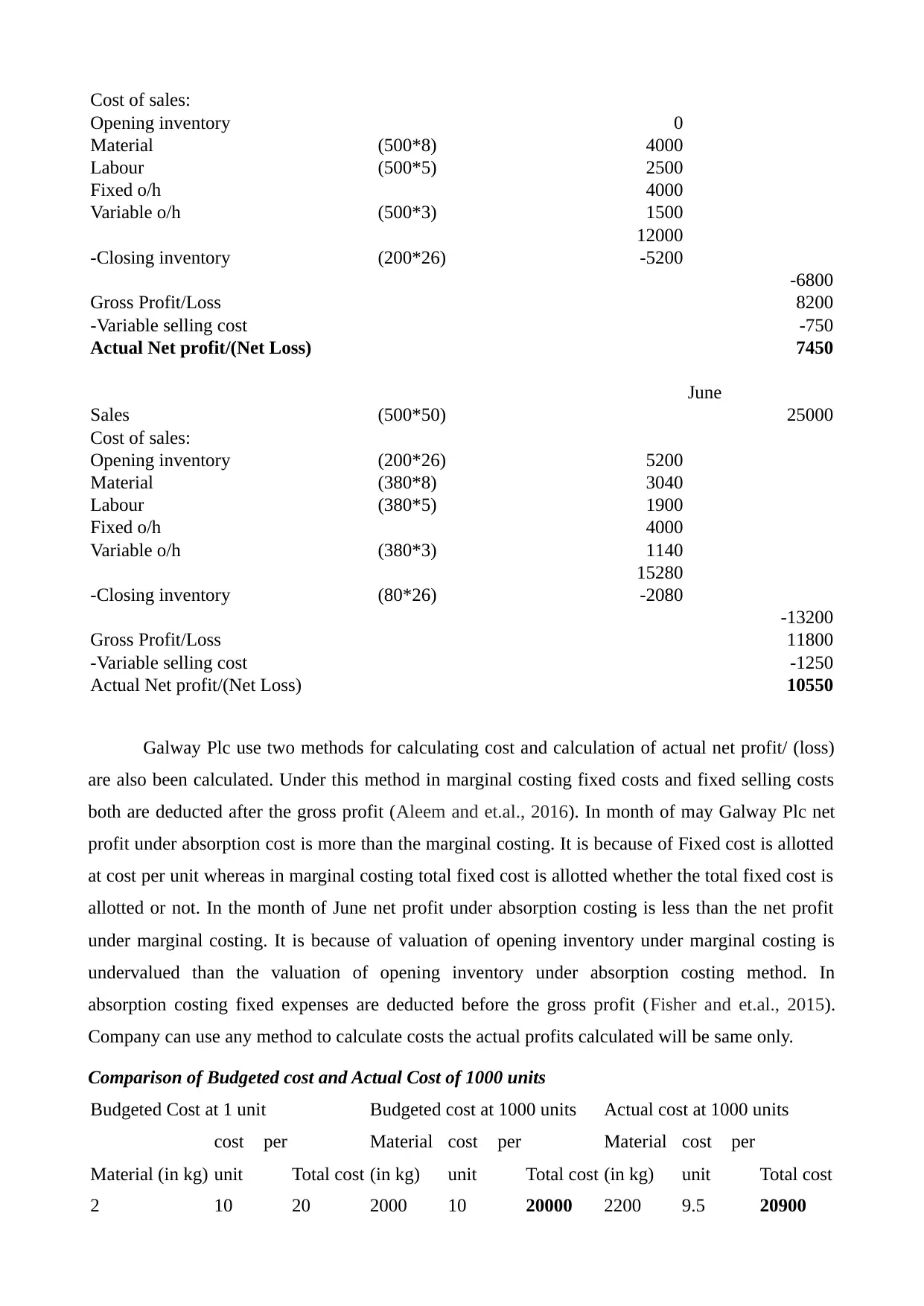

Comparison of Budgeted cost and Actual Cost of 1000 units

Budgeted Cost at 1 unit Budgeted cost at 1000 units Actual cost at 1000 units

Material (in kg)

cost per

unit Total cost

Material

(in kg)

cost per

unit Total cost

Material

(in kg)

cost per

unit Total cost

2 10 20 2000 10 20000 2200 9.5 20900

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed o/h 4000

Variable o/h (500*3) 1500

12000

-Closing inventory (200*26) -5200

-6800

Gross Profit/Loss 8200

-Variable selling cost -750

Actual Net profit/(Net Loss) 7450

June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*26) 5200

Material (380*8) 3040

Labour (380*5) 1900

Fixed o/h 4000

Variable o/h (380*3) 1140

15280

-Closing inventory (80*26) -2080

-13200

Gross Profit/Loss 11800

-Variable selling cost -1250

Actual Net profit/(Net Loss) 10550

Galway Plc use two methods for calculating cost and calculation of actual net profit/ (loss)

are also been calculated. Under this method in marginal costing fixed costs and fixed selling costs

both are deducted after the gross profit (Aleem and et.al., 2016). In month of may Galway Plc net

profit under absorption cost is more than the marginal costing. It is because of Fixed cost is allotted

at cost per unit whereas in marginal costing total fixed cost is allotted whether the total fixed cost is

allotted or not. In the month of June net profit under absorption costing is less than the net profit

under marginal costing. It is because of valuation of opening inventory under marginal costing is

undervalued than the valuation of opening inventory under absorption costing method. In

absorption costing fixed expenses are deducted before the gross profit (Fisher and et.al., 2015).

Company can use any method to calculate costs the actual profits calculated will be same only.

Comparison of Budgeted cost and Actual Cost of 1000 units

Budgeted Cost at 1 unit Budgeted cost at 1000 units Actual cost at 1000 units

Material (in kg)

cost per

unit Total cost

Material

(in kg)

cost per

unit Total cost

Material

(in kg)

cost per

unit Total cost

2 10 20 2000 10 20000 2200 9.5 20900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Galway plc budgeted and actual costs and material the cost absorbed for producing actual

units has been increased than the budgeted cost. Actual cost absorbed in purchasing raw material

was less but materials consumed were consumed more than the budgeted units for producing 1000

units. Budgeted cost for material was $10 but actual cost absorbed was to $9.5 which is less than the

budgeted cost. The actual material consumed were 2200 kg for producing 1000 units was more than

the budgeted raw material i.e. 2000 kg for 1000 units. Galway plc. Should focus on $900 cost

because it was more absorbed than the budgeted cost because of 200 kg. was more consumed.

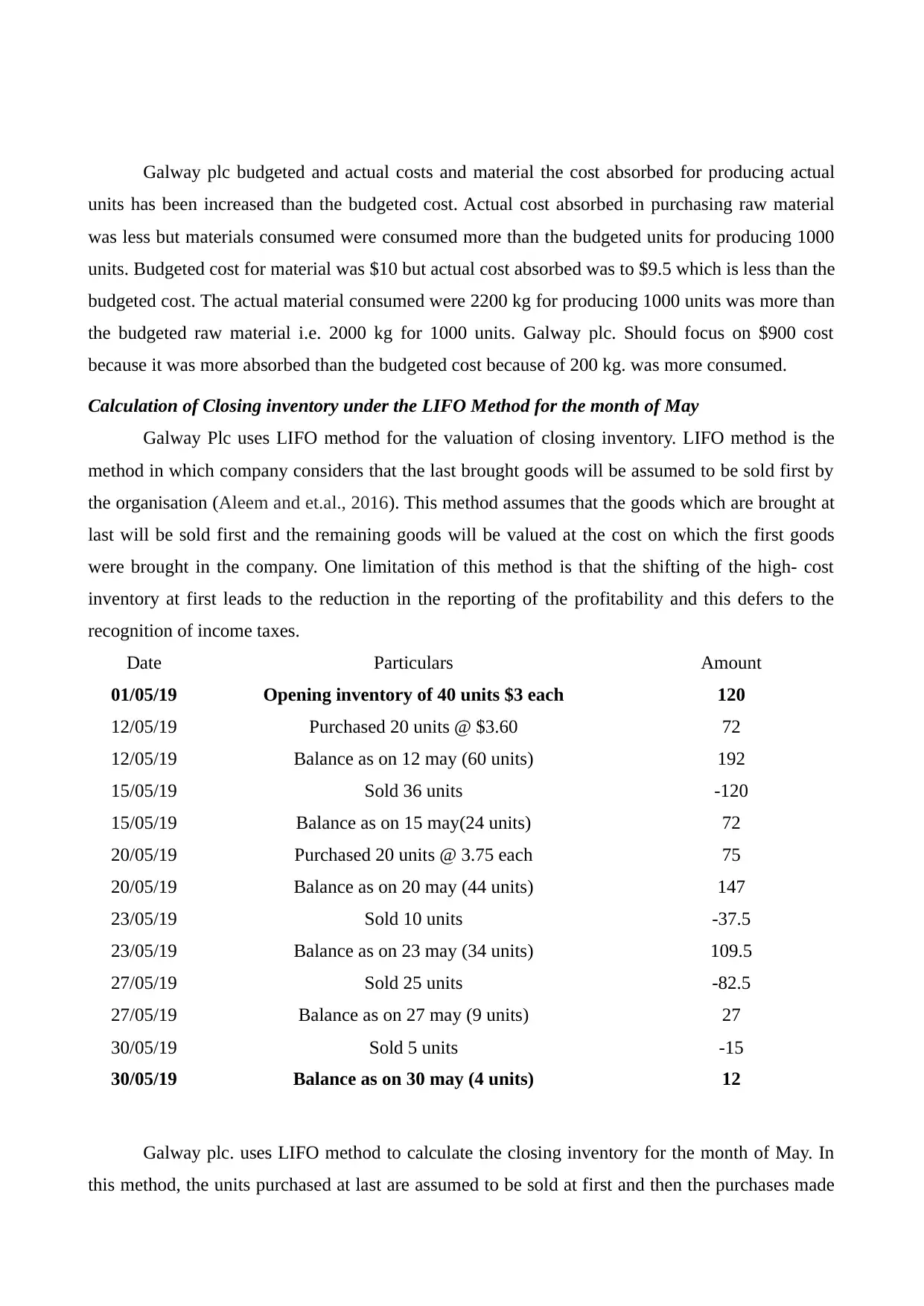

Calculation of Closing inventory under the LIFO Method for the month of May

Galway Plc uses LIFO method for the valuation of closing inventory. LIFO method is the

method in which company considers that the last brought goods will be assumed to be sold first by

the organisation (Aleem and et.al., 2016). This method assumes that the goods which are brought at

last will be sold first and the remaining goods will be valued at the cost on which the first goods

were brought in the company. One limitation of this method is that the shifting of the high- cost

inventory at first leads to the reduction in the reporting of the profitability and this defers to the

recognition of income taxes.

Date Particulars Amount

01/05/19 Opening inventory of 40 units $3 each 120

12/05/19 Purchased 20 units @ $3.60 72

12/05/19 Balance as on 12 may (60 units) 192

15/05/19 Sold 36 units -120

15/05/19 Balance as on 15 may(24 units) 72

20/05/19 Purchased 20 units @ 3.75 each 75

20/05/19 Balance as on 20 may (44 units) 147

23/05/19 Sold 10 units -37.5

23/05/19 Balance as on 23 may (34 units) 109.5

27/05/19 Sold 25 units -82.5

27/05/19 Balance as on 27 may (9 units) 27

30/05/19 Sold 5 units -15

30/05/19 Balance as on 30 may (4 units) 12

Galway plc. uses LIFO method to calculate the closing inventory for the month of May. In

this method, the units purchased at last are assumed to be sold at first and then the purchases made

units has been increased than the budgeted cost. Actual cost absorbed in purchasing raw material

was less but materials consumed were consumed more than the budgeted units for producing 1000

units. Budgeted cost for material was $10 but actual cost absorbed was to $9.5 which is less than the

budgeted cost. The actual material consumed were 2200 kg for producing 1000 units was more than

the budgeted raw material i.e. 2000 kg for 1000 units. Galway plc. Should focus on $900 cost

because it was more absorbed than the budgeted cost because of 200 kg. was more consumed.

Calculation of Closing inventory under the LIFO Method for the month of May

Galway Plc uses LIFO method for the valuation of closing inventory. LIFO method is the

method in which company considers that the last brought goods will be assumed to be sold first by

the organisation (Aleem and et.al., 2016). This method assumes that the goods which are brought at

last will be sold first and the remaining goods will be valued at the cost on which the first goods

were brought in the company. One limitation of this method is that the shifting of the high- cost

inventory at first leads to the reduction in the reporting of the profitability and this defers to the

recognition of income taxes.

Date Particulars Amount

01/05/19 Opening inventory of 40 units $3 each 120

12/05/19 Purchased 20 units @ $3.60 72

12/05/19 Balance as on 12 may (60 units) 192

15/05/19 Sold 36 units -120

15/05/19 Balance as on 15 may(24 units) 72

20/05/19 Purchased 20 units @ 3.75 each 75

20/05/19 Balance as on 20 may (44 units) 147

23/05/19 Sold 10 units -37.5

23/05/19 Balance as on 23 may (34 units) 109.5

27/05/19 Sold 25 units -82.5

27/05/19 Balance as on 27 may (9 units) 27

30/05/19 Sold 5 units -15

30/05/19 Balance as on 30 may (4 units) 12

Galway plc. uses LIFO method to calculate the closing inventory for the month of May. In

this method, the units purchased at last are assumed to be sold at first and then the purchases made

at first are assumed to be sold later on. In the above example, 4 units are remaining on 3 May for $3

each i.e. $12. Otherwise, all the units even came later are been sold as this method assumes that

later purchased items are sold first and then first purchased items are sold. LIFO means Last In First

out means that later purchased items are assumed to be sold first than those purchased later on

(Tinkelman and et.al., 2018).

LO 3

P 4 Advantages and Disadvantages of different types of planning tools used for budgetary control

Budgetary control is the process where the reports are prepared related to the various

budgets in order to know the various cost allocation in the various department. Budgets are prepared

to compare them with the actual performance of Galway Plc to know the loopholes in the company.

There are various types of planning tools of Budgetary Control are-

Zero Based Budgeting- Zero Based Budgeting is the process which starts from the “Zero Base”.

This method assumes that the Galway Plc will be analysing each and every expense in the company

by justifying what is the needs and costs of the relevant expense in the particular department. Each

expense is justified for each new preparation of budget.

Advantages Disadvantages

It is the cost effective method for the company

because it justifies each and every expense of

the company (Jermias, 2017).

This method too much costly for justifying each

and every expense of the company.

It takes into account the various expenses for the

Galway Plc such as inflation rates and interest

rates.

It takes too much time for analysing each and

every expense for every new preparation of

budget.

Incremental Budgeting- Incremental Budgeting is the method in which Galway Plc prepares the

budget on the basis of past year performance and budgets. It takes a small percentage and adds to

the previous years budget for computing the current years budget. The method leads to the

approach of “spend it or lose” mentality.

Advantages Disadvantages

This method is stable and gradual. It does not take into account the various

expenses such as inflation rates, interest rates

etc. in the preparation of budget (Modugno and

Di Carlo, 2019).

This method is simple to understand and easy to

operate in Galway Plc.

It assumes that there will be no change in the

activities and working will be continue in the

same manner in Galway Plc.

The impact of change of this method is quick The budget quickly become out of date even

each i.e. $12. Otherwise, all the units even came later are been sold as this method assumes that

later purchased items are sold first and then first purchased items are sold. LIFO means Last In First

out means that later purchased items are assumed to be sold first than those purchased later on

(Tinkelman and et.al., 2018).

LO 3

P 4 Advantages and Disadvantages of different types of planning tools used for budgetary control

Budgetary control is the process where the reports are prepared related to the various

budgets in order to know the various cost allocation in the various department. Budgets are prepared

to compare them with the actual performance of Galway Plc to know the loopholes in the company.

There are various types of planning tools of Budgetary Control are-

Zero Based Budgeting- Zero Based Budgeting is the process which starts from the “Zero Base”.

This method assumes that the Galway Plc will be analysing each and every expense in the company

by justifying what is the needs and costs of the relevant expense in the particular department. Each

expense is justified for each new preparation of budget.

Advantages Disadvantages

It is the cost effective method for the company

because it justifies each and every expense of

the company (Jermias, 2017).

This method too much costly for justifying each

and every expense of the company.

It takes into account the various expenses for the

Galway Plc such as inflation rates and interest

rates.

It takes too much time for analysing each and

every expense for every new preparation of

budget.

Incremental Budgeting- Incremental Budgeting is the method in which Galway Plc prepares the

budget on the basis of past year performance and budgets. It takes a small percentage and adds to

the previous years budget for computing the current years budget. The method leads to the

approach of “spend it or lose” mentality.

Advantages Disadvantages

This method is stable and gradual. It does not take into account the various

expenses such as inflation rates, interest rates

etc. in the preparation of budget (Modugno and

Di Carlo, 2019).

This method is simple to understand and easy to

operate in Galway Plc.

It assumes that there will be no change in the

activities and working will be continue in the

same manner in Galway Plc.

The impact of change of this method is quick The budget quickly become out of date even

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and easy to know the changes. with the small change in the activities.

Activity Based Budgeting- In this method, Galway Plc records, research about each and every

activity in the company. Every activity in the company is scrutinized and based on the results

company creates the new budget for the company. Activities are recognized in order to know the

efficiency of each activity. This method is highly rigorous than the traditional method because it

takes inflation rates also for scrutinizing each activity.

Advantages Disadvantages

This method checks the efficiency of each and

every activity in the company (Toussaint and

et.al., 2015).

It takes lot of time to check the efficiency of

each and every activity.

This method even takes the large expenses such

inflation rates for scrutinizing purpose.

It is not economical to practically apply this

method in the company.

This method helps Galway Plc in cost cutting of

the company.

This method needs the high level of professional

employees for scrutinizing each and every

employee in the company.

LO 4

P 5. Discussing management accounting system for responding financial problems.

Management accounting system is defined as a process of preparing internal managerial

report by considering both the financial as well as statistical information which aids the

management of the company in decision making process. It is concerned with formulation of plans,

strategies and policies which is required for successful accomplishment of business goals and

objectives. Further, the management accounting system assist in management in making strong and

influencing business strategy along with its proper implementation for the betterment of business

and employees as a whole. Following are the management accounting system which assist in

solving financial issues of Galway Plc:

1. Benchmarking – Is defined as a process of measuring the overall performance level of the

company and its employees as a whole. It is an approach which is related with comparing of

own business processes and concepts with those companies which is performing better

among every competitor. It helps in evaluating the performance level with the use of metrics

which indicates about best industry and its practices as it is adopted and used by them. It

helps Galway Plc in setting standards and norms for making high profitability. Also, by

matching the quality and standards as per the best performing industry, Galway Plc can

improves the performance level of its own as well as of its employees. By adopting business

practices, concepts and processes as per the best industry, Galway can overcome its issue

related to inefficient business operations and can thus increase its business efficiency and

Activity Based Budgeting- In this method, Galway Plc records, research about each and every

activity in the company. Every activity in the company is scrutinized and based on the results

company creates the new budget for the company. Activities are recognized in order to know the

efficiency of each activity. This method is highly rigorous than the traditional method because it

takes inflation rates also for scrutinizing each activity.

Advantages Disadvantages

This method checks the efficiency of each and

every activity in the company (Toussaint and

et.al., 2015).

It takes lot of time to check the efficiency of

each and every activity.

This method even takes the large expenses such

inflation rates for scrutinizing purpose.

It is not economical to practically apply this

method in the company.

This method helps Galway Plc in cost cutting of

the company.

This method needs the high level of professional

employees for scrutinizing each and every

employee in the company.

LO 4

P 5. Discussing management accounting system for responding financial problems.

Management accounting system is defined as a process of preparing internal managerial

report by considering both the financial as well as statistical information which aids the

management of the company in decision making process. It is concerned with formulation of plans,

strategies and policies which is required for successful accomplishment of business goals and

objectives. Further, the management accounting system assist in management in making strong and

influencing business strategy along with its proper implementation for the betterment of business

and employees as a whole. Following are the management accounting system which assist in

solving financial issues of Galway Plc:

1. Benchmarking – Is defined as a process of measuring the overall performance level of the

company and its employees as a whole. It is an approach which is related with comparing of

own business processes and concepts with those companies which is performing better

among every competitor. It helps in evaluating the performance level with the use of metrics

which indicates about best industry and its practices as it is adopted and used by them. It

helps Galway Plc in setting standards and norms for making high profitability. Also, by

matching the quality and standards as per the best performing industry, Galway Plc can

improves the performance level of its own as well as of its employees. By adopting business

practices, concepts and processes as per the best industry, Galway can overcome its issue

related to inefficient business operations and can thus increase its business efficiency and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

production level as well.

2. Key performance indicator – It is one of the best measures which is based on performance

evaluation in terms of quantifiable nature. With the help of this tool, Galway Plc can

evaluate the success journey of its own business processes and of its employees too in

meeting the set defined business goals and objectives. This tool helps the company in

accessing whether the company is making proper and effective use of its business as well as

financial resources towards the attainment of the set defined business goals and objectives. It

assists Galway in determining whether the company is performing as per the strategies

formulated or not for achieving key business objectives. With the help of this tool, company

can focus on improving its employees performance by reducing their turnover rate,

motivating them by satisfying their needs. By imparting training sessions and workshop, the

performance level of its employees and workers can be enhanced (Modugno and Di Carlo,

2019).

3. Balance scorecard – One of the most important management accounting system which

assist the company in identifying the factors which helps the business in achieving its

business aims. It is considered as a performance metrics use of which can help the

management in improving its internal business function and operations, along with its

external business results. Galway Plc can identify factors which is creating negative impact

on the process of attainment of business goals as it involves deep analysis of each strategies.

It is based on different perspectives for assessing the overall business health viz. financial,

customer, internal processes and learning and growth of organisation. These perspectives of

business made emphasis and provides a balanced view of the business operation to Galway

Plc. Business efficiency can be solved by improving all the internal process like reducing

wastage of resources etc.

4. Financial governance – The term financial governance is defined as a way and process in

which the company can manages all its financial information for a definite period of time. It

emphasizes on managing of performance by controlling data, financial information and

ensuring that proper compliance has been made while carrying on any business operations

and activities. It also ensures that proper, material and correct disclosures has been made in

the managerial report regarding the financial information which is of influencing nature and

having impact on the decision making process. It is a tool which assist Galway Plc in

monitoring, collecting, analysing and dealing with the financial information of the business.

Formulation of sound and effective financial policies, plans can help in proper and relevant

allocation of business & financial resources (Jermias, 2017). With the help of this tool,

2. Key performance indicator – It is one of the best measures which is based on performance

evaluation in terms of quantifiable nature. With the help of this tool, Galway Plc can

evaluate the success journey of its own business processes and of its employees too in

meeting the set defined business goals and objectives. This tool helps the company in

accessing whether the company is making proper and effective use of its business as well as

financial resources towards the attainment of the set defined business goals and objectives. It

assists Galway in determining whether the company is performing as per the strategies

formulated or not for achieving key business objectives. With the help of this tool, company

can focus on improving its employees performance by reducing their turnover rate,

motivating them by satisfying their needs. By imparting training sessions and workshop, the

performance level of its employees and workers can be enhanced (Modugno and Di Carlo,

2019).

3. Balance scorecard – One of the most important management accounting system which

assist the company in identifying the factors which helps the business in achieving its

business aims. It is considered as a performance metrics use of which can help the

management in improving its internal business function and operations, along with its

external business results. Galway Plc can identify factors which is creating negative impact

on the process of attainment of business goals as it involves deep analysis of each strategies.

It is based on different perspectives for assessing the overall business health viz. financial,

customer, internal processes and learning and growth of organisation. These perspectives of

business made emphasis and provides a balanced view of the business operation to Galway

Plc. Business efficiency can be solved by improving all the internal process like reducing

wastage of resources etc.

4. Financial governance – The term financial governance is defined as a way and process in

which the company can manages all its financial information for a definite period of time. It

emphasizes on managing of performance by controlling data, financial information and

ensuring that proper compliance has been made while carrying on any business operations

and activities. It also ensures that proper, material and correct disclosures has been made in

the managerial report regarding the financial information which is of influencing nature and

having impact on the decision making process. It is a tool which assist Galway Plc in

monitoring, collecting, analysing and dealing with the financial information of the business.

Formulation of sound and effective financial policies, plans can help in proper and relevant

allocation of business & financial resources (Jermias, 2017). With the help of this tool,

Galway Plc can make budget, financial plans and models which can assist in proper control

over the internal financial business processes.

M 4. Analysing management accounting assist in achieving organisation success.

By adopting proper and effective management accounting system, Galway Plc can overcome

its financial business issues and can achieve success in following manner:

1. Benchmarking -

Advantages Disadvantages

It ensures improvement in

performance level and foster

competitiveness.

It supports in making required

changes & suggest measures for

adoption of change process.

It only focuses on measuring of

performance of operational

nature and is not able to

evaluate the overall

effectiveness.

The main disadvantage is that

under this tool, the best

standards followed by

competitor is assessed

irrespective of its implications.

2. Key performance indicator -

Advantages Disadvantages

Identification of under performing

employees and department can be

done. Also, it provides accurate and

measurable outcome by tracking the

progress level.

It also enhances on increasing

overall business productivity by

improving communication flow.

It emphasizes on attainment of

outcomes from short term goals

resulting in decrease in the

quality of work of Galway Plc

(Toussaint and et.al., 2015).

3. Balance scorecard -

Advantages Disadvantages

This tool helps in controlling It focuses on four perspectives

over the internal financial business processes.

M 4. Analysing management accounting assist in achieving organisation success.

By adopting proper and effective management accounting system, Galway Plc can overcome

its financial business issues and can achieve success in following manner:

1. Benchmarking -

Advantages Disadvantages

It ensures improvement in

performance level and foster

competitiveness.

It supports in making required

changes & suggest measures for

adoption of change process.

It only focuses on measuring of

performance of operational

nature and is not able to

evaluate the overall

effectiveness.

The main disadvantage is that

under this tool, the best

standards followed by

competitor is assessed

irrespective of its implications.

2. Key performance indicator -

Advantages Disadvantages

Identification of under performing

employees and department can be

done. Also, it provides accurate and

measurable outcome by tracking the

progress level.

It also enhances on increasing

overall business productivity by

improving communication flow.

It emphasizes on attainment of

outcomes from short term goals

resulting in decrease in the

quality of work of Galway Plc

(Toussaint and et.al., 2015).

3. Balance scorecard -

Advantages Disadvantages

This tool helps in controlling It focuses on four perspectives

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.