Economics Assignment on Microeconomic Principles and Analysis

VerifiedAdded on 2022/09/15

|10

|1430

|22

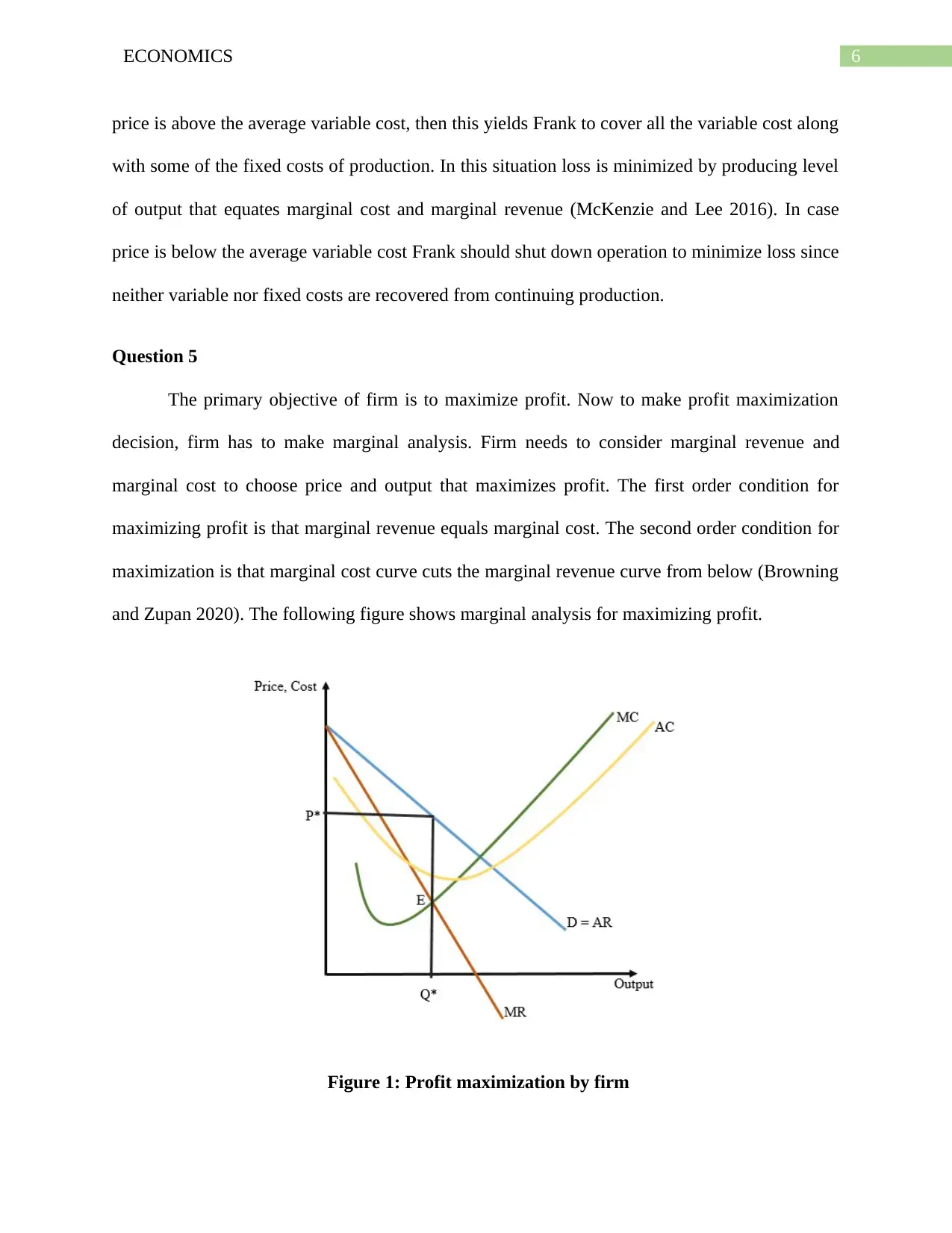

Homework Assignment

AI Summary

This economics assignment delves into several key microeconomic concepts. It begins by differentiating between explicit and implicit costs, crucial for understanding a firm's financial performance. The assignment then explores the relationship between marginal product and marginal cost, emphasizing how changes in these factors impact total and average costs, consequently affecting a firm's profit. It further examines market structures, contrasting price makers and price takers, and analyzing the characteristics of perfectly competitive and monopolistically competitive markets. The assignment also addresses profit maximization, detailing the conditions firms must meet to maximize profits and the decisions firms must make to minimize losses. Finally, it applies game theory to a real-world scenario, illustrating strategic decision-making through a payoff matrix and identifying Nash equilibria. The document provides a comprehensive overview of microeconomic principles and their practical applications.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.