Management Accounting Report: Gartner Financial Consultancy Analysis

VerifiedAdded on 2021/02/19

|18

|4313

|52

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and practices, tailored for a financial consultancy firm, Gartner. It begins by defining management accounting, its essential features, and its distinctions from financial accounting, emphasizing the importance of providing relevant information for decision-making. The report then delves into various management accounting methods, including budget reports, cash managerial accounting, cost reports, account receivable reports, and performance reports. It also covers key costing techniques like marginal costing, absorption costing, LIFO, and weighted average methods for inventory valuation. Furthermore, the report examines different planning tools within the budgetary control system, discussing their advantages and disadvantages. Finally, it explores how organizations can leverage management accounting to address financial challenges and uncertainties, concluding with a summary of the benefits of a robust management accounting system.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION......................................................................................................................3

MAIN BODY.............................................................................................................................3

LO 1...........................................................................................................................................3

P1 Management accounting system and essential features of different management

accounting systems.................................................................................................................3

P2 different methods used for management accounting.........................................................5

Benefits of management accounting system...........................................................................6

LO 2...........................................................................................................................................7

P3 Calculation.........................................................................................................................7

LO 3..........................................................................................................................................12

P4 Different planning tools of budgetary control system with their advantages and

disadvantages........................................................................................................................12

LO4...........................................................................................................................................15

P5 organization adopting management accounting system to respond financial problems. 15

CONCLUSION........................................................................................................................18

REFERENCES.........................................................................................................................19

INTRODUCTION......................................................................................................................3

MAIN BODY.............................................................................................................................3

LO 1...........................................................................................................................................3

P1 Management accounting system and essential features of different management

accounting systems.................................................................................................................3

P2 different methods used for management accounting.........................................................5

Benefits of management accounting system...........................................................................6

LO 2...........................................................................................................................................7

P3 Calculation.........................................................................................................................7

LO 3..........................................................................................................................................12

P4 Different planning tools of budgetary control system with their advantages and

disadvantages........................................................................................................................12

LO4...........................................................................................................................................15

P5 organization adopting management accounting system to respond financial problems. 15

CONCLUSION........................................................................................................................18

REFERENCES.........................................................................................................................19

INTRODUCTION

Management accounting is technique that helps managers in formulation of different

strategies and plans for the company so that the overall financial position and financial

performance of the company could be improved. This system provides appropriate

information to managers regarding financial position and performance of the company

through which they formulated their plans for the company Gartner is UK based medium

sized financial consultancy firm. It was founded in the year 1979. In the present study, there

is report of trainee of the country that shows meaning of management accounting and their

essential features for the company along with different methods of management accounting

reporting. Further it shows, different budgetary control tools that helps managers in their

planning function. It also has a practical part that shows preparation of income statement on

the basis of different techniques of management accounting and statement showing inventory

held by company by using different methods. At the end of report, it explains different

management accounting systems that can be used by different organisations in order to

improve its efficiency of responding to different financial uncertainties of the company.

MAIN BODY

LO 1

P1 Management accounting system and essential features of different management

accounting systems

Management accounting

Management accounting term refers to the advice and financial data of the company

which has been using development of the organization. It has been using the provisions for all

the accounting information for identifying the better information. It is basically a profession

which has been involved the partnering the management decisions making process, system of

performance management and also the devising planning process (Kaplan and

Atkinson, 2015). It generally provides the experts for making the financial reporting & also

controlling for assisting the management for the implementation and formulation of the

Gartner strategy.

Essential requirements of different management accounting

Management accounting system

Management accounting is technique that helps managers in formulation of different

strategies and plans for the company so that the overall financial position and financial

performance of the company could be improved. This system provides appropriate

information to managers regarding financial position and performance of the company

through which they formulated their plans for the company Gartner is UK based medium

sized financial consultancy firm. It was founded in the year 1979. In the present study, there

is report of trainee of the country that shows meaning of management accounting and their

essential features for the company along with different methods of management accounting

reporting. Further it shows, different budgetary control tools that helps managers in their

planning function. It also has a practical part that shows preparation of income statement on

the basis of different techniques of management accounting and statement showing inventory

held by company by using different methods. At the end of report, it explains different

management accounting systems that can be used by different organisations in order to

improve its efficiency of responding to different financial uncertainties of the company.

MAIN BODY

LO 1

P1 Management accounting system and essential features of different management

accounting systems

Management accounting

Management accounting term refers to the advice and financial data of the company

which has been using development of the organization. It has been using the provisions for all

the accounting information for identifying the better information. It is basically a profession

which has been involved the partnering the management decisions making process, system of

performance management and also the devising planning process (Kaplan and

Atkinson, 2015). It generally provides the experts for making the financial reporting & also

controlling for assisting the management for the implementation and formulation of the

Gartner strategy.

Essential requirements of different management accounting

Management accounting system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is generally a process that includes the partnering in with all the situations of the

organization. It is a procedure of identifying, analysing, communicating and interpreting all

the financial information which is helpful in achieving the goals and objectives.

Cost-accounting system

The term cost accounting refers to the framework which has been applied by all the

corporation to identify the approximate cost to producing the profitability analysis, cost

control, valuation of inventory. This system has been performed the allocation of the cost

based on performance and also on activities (Otley, 2016).

Job costing system

The term job costing relates to the allocation of the manufacturing cost where the

individual items and batches. It generally applied on the processed goods which is different

from another. It includes all the practices which has been accumulating the data of the cost

that is related to the specific services and production of the job in Gartner. This job costing

system has been applied when management has to track the different types of direct expenses.

It assesses all the amount and cost which has been included in the construction of the job.

Price-optimisation system

The system of the price optimization is generally an application where all the

mathematical analysis for the corporation has been determined the consumers react on the

various price process for its products and services. Basically, it has been applied for analysing

the pricing strategy that the Gartner determine the best way to full fill the goals for

maximizing all the operating profits (Schaltegger and Burritt, 2017).

Inventory management system

Inventory management system refers to the method of overseeing and controlling the use,

storage of all components where the corporation has been applied for the manufacturing of

the goods which is on sale. It oversees the practice of all the quality of the finished goods.

Inventory management system is a key element of the business where it is tied of producing

the sales of goods and services.

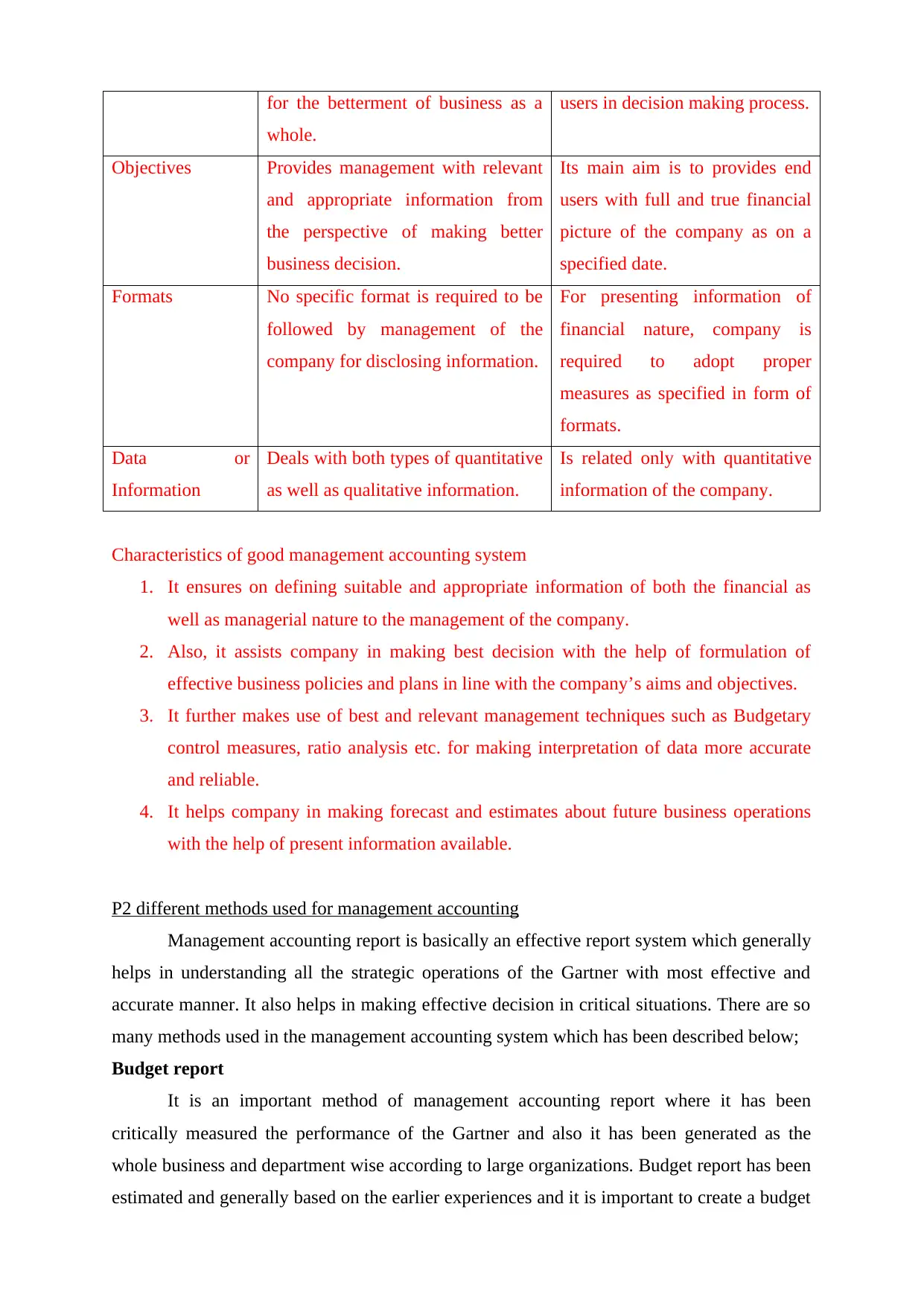

Difference between Management Accounting and Financial Accounting

Basis Management Accounting Financial Accounting

Meaning It is a term which is related with the

process of providing important as

well as crucial information of

managerial needs to the management

of the company in making decision

Is associated with recording,

summarizing, analysing and

preparation of financial reports

on the basis of financial

transactions for assisting its end

organization. It is a procedure of identifying, analysing, communicating and interpreting all

the financial information which is helpful in achieving the goals and objectives.

Cost-accounting system

The term cost accounting refers to the framework which has been applied by all the

corporation to identify the approximate cost to producing the profitability analysis, cost

control, valuation of inventory. This system has been performed the allocation of the cost

based on performance and also on activities (Otley, 2016).

Job costing system

The term job costing relates to the allocation of the manufacturing cost where the

individual items and batches. It generally applied on the processed goods which is different

from another. It includes all the practices which has been accumulating the data of the cost

that is related to the specific services and production of the job in Gartner. This job costing

system has been applied when management has to track the different types of direct expenses.

It assesses all the amount and cost which has been included in the construction of the job.

Price-optimisation system

The system of the price optimization is generally an application where all the

mathematical analysis for the corporation has been determined the consumers react on the

various price process for its products and services. Basically, it has been applied for analysing

the pricing strategy that the Gartner determine the best way to full fill the goals for

maximizing all the operating profits (Schaltegger and Burritt, 2017).

Inventory management system

Inventory management system refers to the method of overseeing and controlling the use,

storage of all components where the corporation has been applied for the manufacturing of

the goods which is on sale. It oversees the practice of all the quality of the finished goods.

Inventory management system is a key element of the business where it is tied of producing

the sales of goods and services.

Difference between Management Accounting and Financial Accounting

Basis Management Accounting Financial Accounting

Meaning It is a term which is related with the

process of providing important as

well as crucial information of

managerial needs to the management

of the company in making decision

Is associated with recording,

summarizing, analysing and

preparation of financial reports

on the basis of financial

transactions for assisting its end

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

for the betterment of business as a

whole.

users in decision making process.

Objectives Provides management with relevant

and appropriate information from

the perspective of making better

business decision.

Its main aim is to provides end

users with full and true financial

picture of the company as on a

specified date.

Formats No specific format is required to be

followed by management of the

company for disclosing information.

For presenting information of

financial nature, company is

required to adopt proper

measures as specified in form of

formats.

Data or

Information

Deals with both types of quantitative

as well as qualitative information.

Is related only with quantitative

information of the company.

Characteristics of good management accounting system

1. It ensures on defining suitable and appropriate information of both the financial as

well as managerial nature to the management of the company.

2. Also, it assists company in making best decision with the help of formulation of

effective business policies and plans in line with the company’s aims and objectives.

3. It further makes use of best and relevant management techniques such as Budgetary

control measures, ratio analysis etc. for making interpretation of data more accurate

and reliable.

4. It helps company in making forecast and estimates about future business operations

with the help of present information available.

P2 different methods used for management accounting

Management accounting report is basically an effective report system which generally

helps in understanding all the strategic operations of the Gartner with most effective and

accurate manner. It also helps in making effective decision in critical situations. There are so

many methods used in the management accounting system which has been described below;

Budget report

It is an important method of management accounting report where it has been

critically measured the performance of the Gartner and also it has been generated as the

whole business and department wise according to large organizations. Budget report has been

estimated and generally based on the earlier experiences and it is important to create a budget

whole.

users in decision making process.

Objectives Provides management with relevant

and appropriate information from

the perspective of making better

business decision.

Its main aim is to provides end

users with full and true financial

picture of the company as on a

specified date.

Formats No specific format is required to be

followed by management of the

company for disclosing information.

For presenting information of

financial nature, company is

required to adopt proper

measures as specified in form of

formats.

Data or

Information

Deals with both types of quantitative

as well as qualitative information.

Is related only with quantitative

information of the company.

Characteristics of good management accounting system

1. It ensures on defining suitable and appropriate information of both the financial as

well as managerial nature to the management of the company.

2. Also, it assists company in making best decision with the help of formulation of

effective business policies and plans in line with the company’s aims and objectives.

3. It further makes use of best and relevant management techniques such as Budgetary

control measures, ratio analysis etc. for making interpretation of data more accurate

and reliable.

4. It helps company in making forecast and estimates about future business operations

with the help of present information available.

P2 different methods used for management accounting

Management accounting report is basically an effective report system which generally

helps in understanding all the strategic operations of the Gartner with most effective and

accurate manner. It also helps in making effective decision in critical situations. There are so

many methods used in the management accounting system which has been described below;

Budget report

It is an important method of management accounting report where it has been

critically measured the performance of the Gartner and also it has been generated as the

whole business and department wise according to large organizations. Budget report has been

estimated and generally based on the earlier experiences and it is important to create a budget

according to the cost and amount of the company (Maas, Schaltegger and Crutzen, 2016). For

finding the marginal accounting reports it is related to the budget which can guide the top-

level management of the company for offering the better incentives to the employees in terms

with the suppliers and vendors.

Cash managerial accounting

Management accounting reports also refers to the cash flow statements where it

computes about the cost of all the articles which has been manufactured. In this all the

overhead, raw material cost and any other added cost has been deliberations. The sum of total

has been divided to the amount and cost of the products which has been produced. Cost

report is generally a summary of all the information. All the profits margins & revenues has

been monitored & estimated through the reports and having a clear picture of all the cost

which went in the procurement and production of the articles.

Account receivable report

This account receivable reports playing a vital role in the management accounting

reports where all the breakdown structure and remaining balance of the customers into

particular time allowing the managers for identifying the defaulters for finding the problems

in Gartner for the collection process (Quattrone, 2016).

Performance report

It is one of the most important method of the management accounting report where the

review of the performance has been credited of the Gartner. Performance report has been

generated in the Gartner where the managers can use the performance reports to making the

strategic decisions for the future of the company. From making the performance reports

awards has been given to the employees for their better performing. Performance report

management accounting refers to the insight into working of the organization. The main

purpose of the performance reports is to measure the accurate strategies towards the mission

of the Gartner.

Benefits of management accounting system

Management accounting is generally a process for managing all the accounting system

of the organization. There are so many benefits from management accounting system such as

the effective control on management, there are so much useful coordination, it easily

increases the profitability and productivity, it makes the proper planning of all the activities

that has been runs on the organization, it evaluates the performance of the employees and get

the final reports (Weetman, 2019).

finding the marginal accounting reports it is related to the budget which can guide the top-

level management of the company for offering the better incentives to the employees in terms

with the suppliers and vendors.

Cash managerial accounting

Management accounting reports also refers to the cash flow statements where it

computes about the cost of all the articles which has been manufactured. In this all the

overhead, raw material cost and any other added cost has been deliberations. The sum of total

has been divided to the amount and cost of the products which has been produced. Cost

report is generally a summary of all the information. All the profits margins & revenues has

been monitored & estimated through the reports and having a clear picture of all the cost

which went in the procurement and production of the articles.

Account receivable report

This account receivable reports playing a vital role in the management accounting

reports where all the breakdown structure and remaining balance of the customers into

particular time allowing the managers for identifying the defaulters for finding the problems

in Gartner for the collection process (Quattrone, 2016).

Performance report

It is one of the most important method of the management accounting report where the

review of the performance has been credited of the Gartner. Performance report has been

generated in the Gartner where the managers can use the performance reports to making the

strategic decisions for the future of the company. From making the performance reports

awards has been given to the employees for their better performing. Performance report

management accounting refers to the insight into working of the organization. The main

purpose of the performance reports is to measure the accurate strategies towards the mission

of the Gartner.

Benefits of management accounting system

Management accounting is generally a process for managing all the accounting system

of the organization. There are so many benefits from management accounting system such as

the effective control on management, there are so much useful coordination, it easily

increases the profitability and productivity, it makes the proper planning of all the activities

that has been runs on the organization, it evaluates the performance of the employees and get

the final reports (Weetman, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

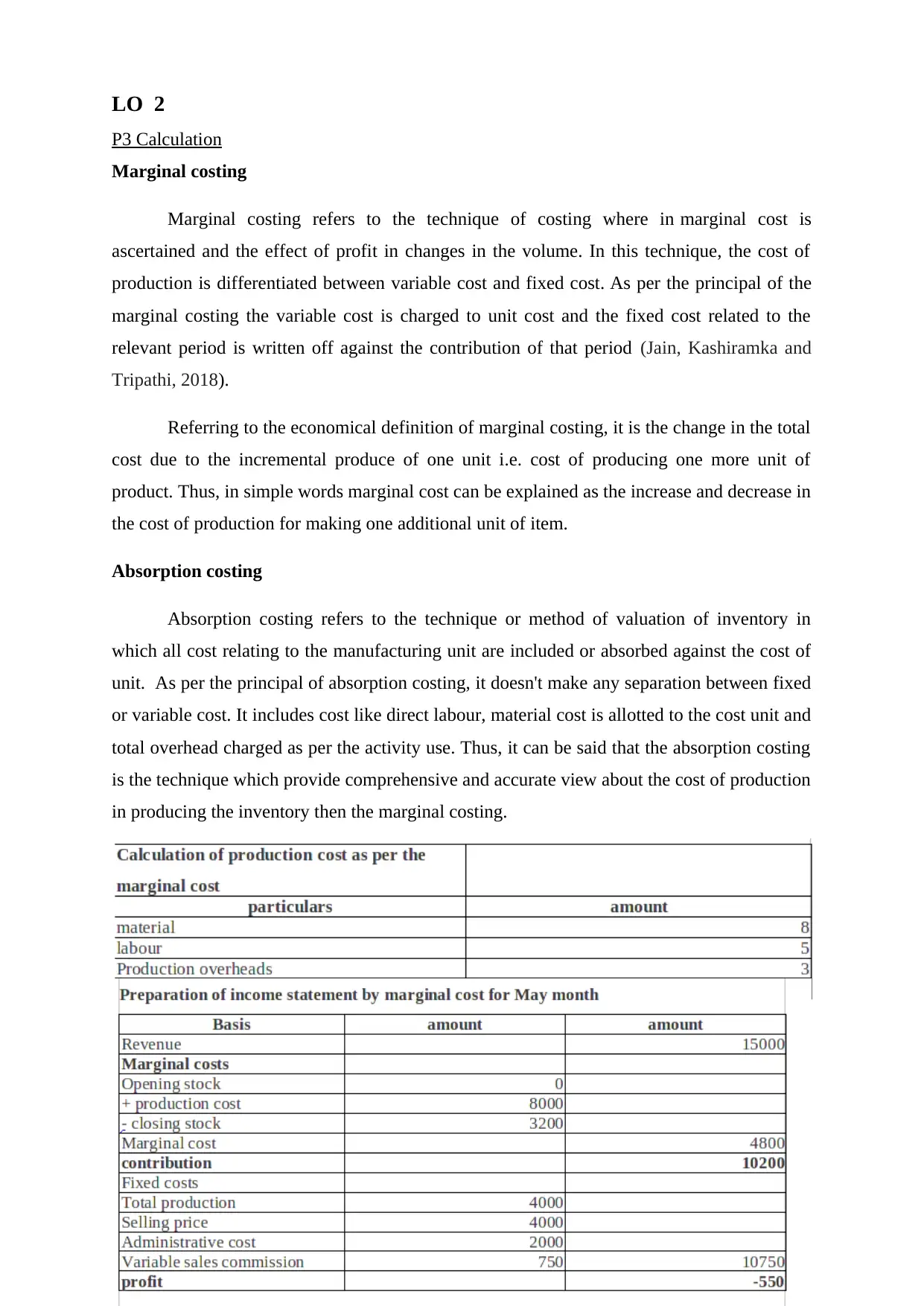

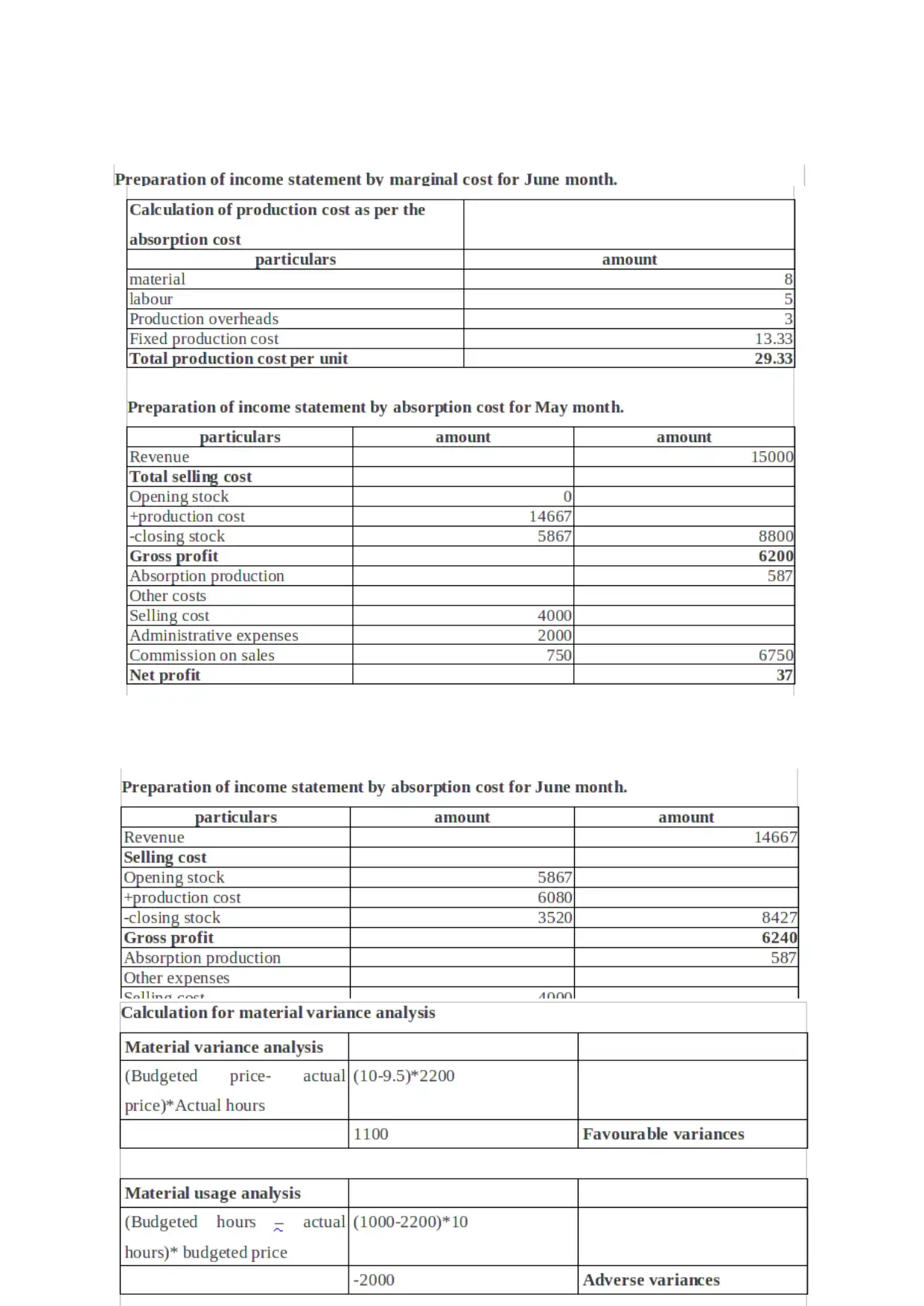

LO 2

P3 Calculation

Marginal costing

Marginal costing refers to the technique of costing where in marginal cost is

ascertained and the effect of profit in changes in the volume. In this technique, the cost of

production is differentiated between variable cost and fixed cost. As per the principal of the

marginal costing the variable cost is charged to unit cost and the fixed cost related to the

relevant period is written off against the contribution of that period (Jain, Kashiramka and

Tripathi, 2018).

Referring to the economical definition of marginal costing, it is the change in the total

cost due to the incremental produce of one unit i.e. cost of producing one more unit of

product. Thus, in simple words marginal cost can be explained as the increase and decrease in

the cost of production for making one additional unit of item.

Absorption costing

Absorption costing refers to the technique or method of valuation of inventory in

which all cost relating to the manufacturing unit are included or absorbed against the cost of

unit. As per the principal of absorption costing, it doesn't make any separation between fixed

or variable cost. It includes cost like direct labour, material cost is allotted to the cost unit and

total overhead charged as per the activity use. Thus, it can be said that the absorption costing

is the technique which provide comprehensive and accurate view about the cost of production

in producing the inventory then the marginal costing.

P3 Calculation

Marginal costing

Marginal costing refers to the technique of costing where in marginal cost is

ascertained and the effect of profit in changes in the volume. In this technique, the cost of

production is differentiated between variable cost and fixed cost. As per the principal of the

marginal costing the variable cost is charged to unit cost and the fixed cost related to the

relevant period is written off against the contribution of that period (Jain, Kashiramka and

Tripathi, 2018).

Referring to the economical definition of marginal costing, it is the change in the total

cost due to the incremental produce of one unit i.e. cost of producing one more unit of

product. Thus, in simple words marginal cost can be explained as the increase and decrease in

the cost of production for making one additional unit of item.

Absorption costing

Absorption costing refers to the technique or method of valuation of inventory in

which all cost relating to the manufacturing unit are included or absorbed against the cost of

unit. As per the principal of absorption costing, it doesn't make any separation between fixed

or variable cost. It includes cost like direct labour, material cost is allotted to the cost unit and

total overhead charged as per the activity use. Thus, it can be said that the absorption costing

is the technique which provide comprehensive and accurate view about the cost of production

in producing the inventory then the marginal costing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

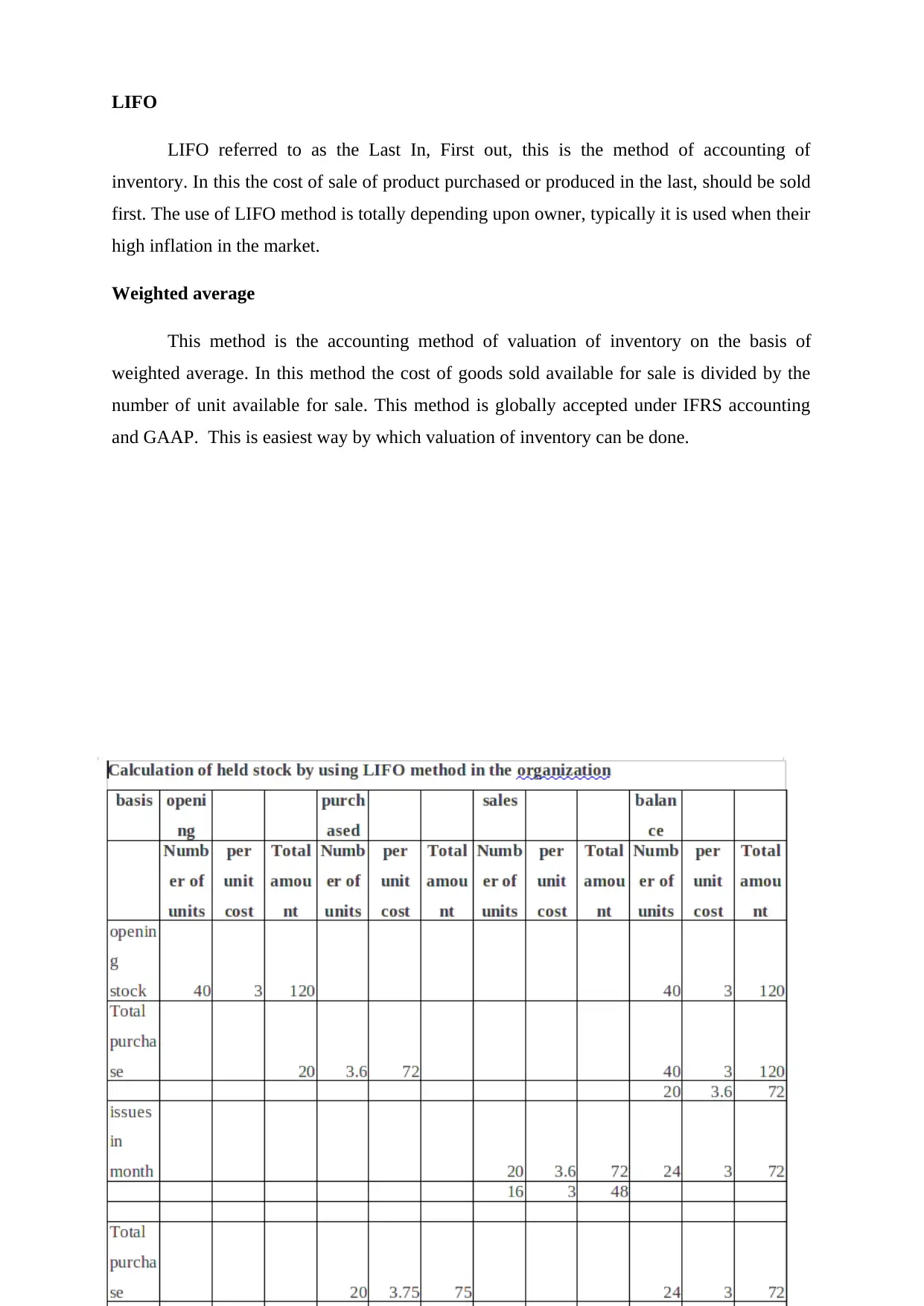

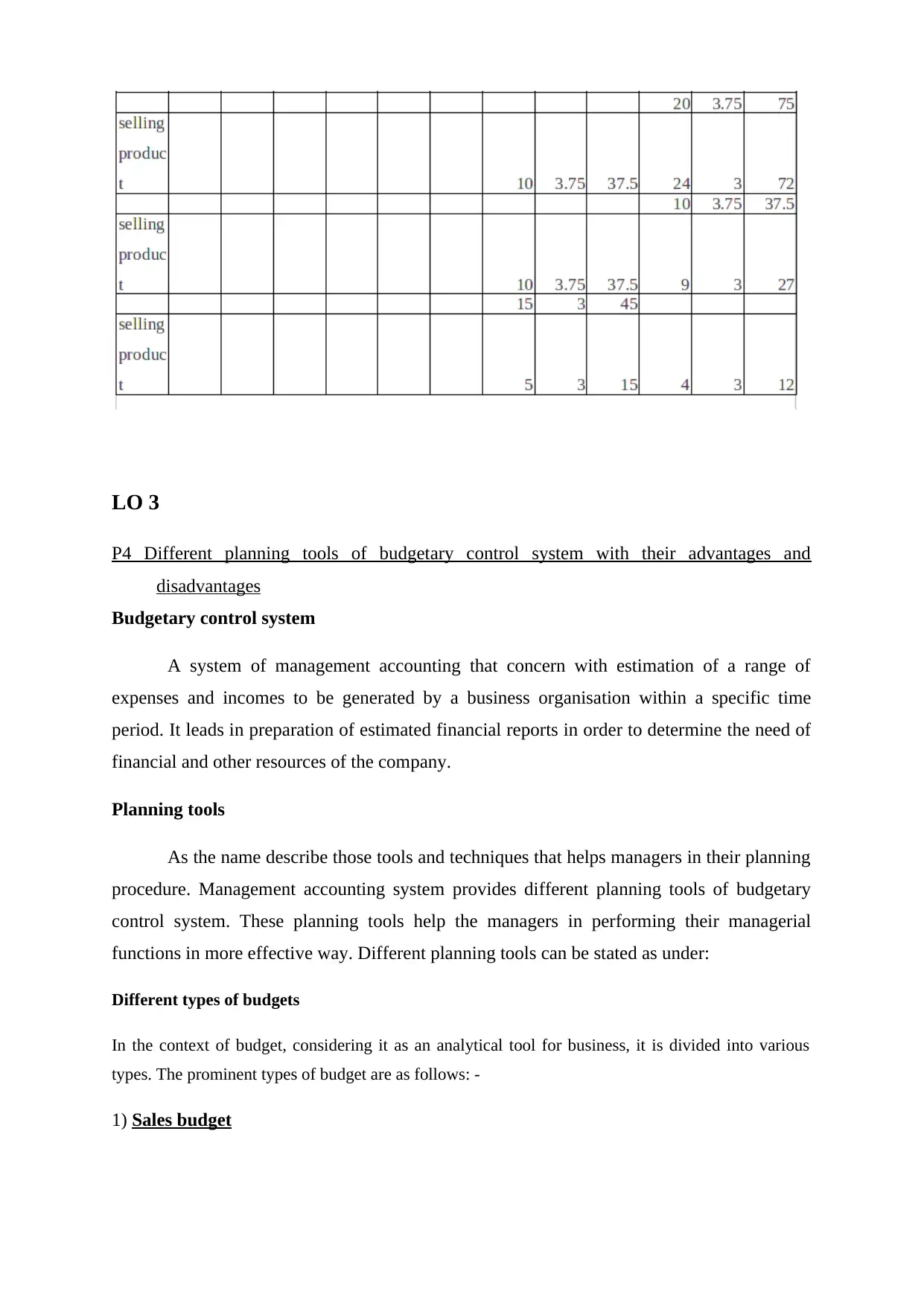

LIFO

LIFO referred to as the Last In, First out, this is the method of accounting of

inventory. In this the cost of sale of product purchased or produced in the last, should be sold

first. The use of LIFO method is totally depending upon owner, typically it is used when their

high inflation in the market.

Weighted average

This method is the accounting method of valuation of inventory on the basis of

weighted average. In this method the cost of goods sold available for sale is divided by the

number of unit available for sale. This method is globally accepted under IFRS accounting

and GAAP. This is easiest way by which valuation of inventory can be done.

LIFO referred to as the Last In, First out, this is the method of accounting of

inventory. In this the cost of sale of product purchased or produced in the last, should be sold

first. The use of LIFO method is totally depending upon owner, typically it is used when their

high inflation in the market.

Weighted average

This method is the accounting method of valuation of inventory on the basis of

weighted average. In this method the cost of goods sold available for sale is divided by the

number of unit available for sale. This method is globally accepted under IFRS accounting

and GAAP. This is easiest way by which valuation of inventory can be done.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO 3

P4 Different planning tools of budgetary control system with their advantages and

disadvantages

Budgetary control system

A system of management accounting that concern with estimation of a range of

expenses and incomes to be generated by a business organisation within a specific time

period. It leads in preparation of estimated financial reports in order to determine the need of

financial and other resources of the company.

Planning tools

As the name describe those tools and techniques that helps managers in their planning

procedure. Management accounting system provides different planning tools of budgetary

control system. These planning tools help the managers in performing their managerial

functions in more effective way. Different planning tools can be stated as under:

Different types of budgets

In the context of budget, considering it as an analytical tool for business, it is divided into various

types. The prominent types of budget are as follows: -

1) Sales budget

P4 Different planning tools of budgetary control system with their advantages and

disadvantages

Budgetary control system

A system of management accounting that concern with estimation of a range of

expenses and incomes to be generated by a business organisation within a specific time

period. It leads in preparation of estimated financial reports in order to determine the need of

financial and other resources of the company.

Planning tools

As the name describe those tools and techniques that helps managers in their planning

procedure. Management accounting system provides different planning tools of budgetary

control system. These planning tools help the managers in performing their managerial

functions in more effective way. Different planning tools can be stated as under:

Different types of budgets

In the context of budget, considering it as an analytical tool for business, it is divided into various

types. The prominent types of budget are as follows: -

1) Sales budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This budget refers to budget based on the company' s sale relating activities. It determines

the future sales of company, targeted gross sales per annum, sales of specified products and

many more. This budget can be prepared or can be break down into units. Further it

determines the sale goal of the company.

Contribution of sales budget towards management in planning: -

Helps management in deciding the sales goal by considering the several factors like

capacity, human resource, investment, technology etc. This sale goal plays vital role

in the planning.

Also analyse the variances found in comparison between actual and standards as

mention in the sales budget, this helps management in planning accordingly (Shil and

Das, 2018).

This budget provides units information or several other major information about profit

margin in sales, past records or trends in sales of the company and many more. By

using this, management formulate its planning to achieve goals of the company.

Advantages:-

It focuses on the improving selling efficiency and reducing the selling cost of the

company.

It allocates the resources to the different products and areas related to sales, so that

predetermined goal can be achieved.

Provide assistance framing the sale programs and plan to achieve the goals of the

business.

Disadvantage:-

Framing of such type budget requires too managerial skill and time to make it

effective and as per need of business.

Such budget is accepted by all in the business, this means universal acceptance of this

budget is harder.

The expense over sales budget preparation are heavy and further it can't depict the

future trend of sales of the company.

2) Capital budget

the future sales of company, targeted gross sales per annum, sales of specified products and

many more. This budget can be prepared or can be break down into units. Further it

determines the sale goal of the company.

Contribution of sales budget towards management in planning: -

Helps management in deciding the sales goal by considering the several factors like

capacity, human resource, investment, technology etc. This sale goal plays vital role

in the planning.

Also analyse the variances found in comparison between actual and standards as

mention in the sales budget, this helps management in planning accordingly (Shil and

Das, 2018).

This budget provides units information or several other major information about profit

margin in sales, past records or trends in sales of the company and many more. By

using this, management formulate its planning to achieve goals of the company.

Advantages:-

It focuses on the improving selling efficiency and reducing the selling cost of the

company.

It allocates the resources to the different products and areas related to sales, so that

predetermined goal can be achieved.

Provide assistance framing the sale programs and plan to achieve the goals of the

business.

Disadvantage:-

Framing of such type budget requires too managerial skill and time to make it

effective and as per need of business.

Such budget is accepted by all in the business, this means universal acceptance of this

budget is harder.

The expense over sales budget preparation are heavy and further it can't depict the

future trend of sales of the company.

2) Capital budget

This budget depicts the real picture of company's assets and the capital expenditure. This

budget use to getting assurance about whether the company's long term investment in the

assets, new plant, research and development project are worthy enough or not (Booth, 2018).

Contribution of capital budget towards management in planning

This budget analyses all factors and suggest the business about the investment in long

run or not. It helps management accordingly in planning.

This provide information about the future benefit in long run related to the business,

so that management plans future projects accordingly.

Advantages:-

Helps the business while choosing the investment decisions wisely by considering all

the major affecting factors.

Provide vital information about the investment which will provide adequate return or

not in future.

Helps the business in understanding the investment opportunities and risk related

associated with it. Also abstain management from over investing and under investing.

Disadvantage:-

This budget can't depict the future of investment i.e. the estimation regarding

investment may be wrong (Budgetary Controlling Techniques. 2018).

It requires major time and the decision related to investment in long run can't be easily

revoked.

3) Production budget

This budget is directly linked with the production of business to achieve the sale goal of the

business. In this budget estimation of manufacturing unit is determined and cost relating to

such manufacturing is also analysed including material cost and labour cost. Main aim of this

budget to provide manufacturing unit which can meet the sales goal.

Contribution of production budget towards management in planning

It helps management in deciding the cost of production including labour and material,

so that sale goal can be achieved effectively.

budget use to getting assurance about whether the company's long term investment in the

assets, new plant, research and development project are worthy enough or not (Booth, 2018).

Contribution of capital budget towards management in planning

This budget analyses all factors and suggest the business about the investment in long

run or not. It helps management accordingly in planning.

This provide information about the future benefit in long run related to the business,

so that management plans future projects accordingly.

Advantages:-

Helps the business while choosing the investment decisions wisely by considering all

the major affecting factors.

Provide vital information about the investment which will provide adequate return or

not in future.

Helps the business in understanding the investment opportunities and risk related

associated with it. Also abstain management from over investing and under investing.

Disadvantage:-

This budget can't depict the future of investment i.e. the estimation regarding

investment may be wrong (Budgetary Controlling Techniques. 2018).

It requires major time and the decision related to investment in long run can't be easily

revoked.

3) Production budget

This budget is directly linked with the production of business to achieve the sale goal of the

business. In this budget estimation of manufacturing unit is determined and cost relating to

such manufacturing is also analysed including material cost and labour cost. Main aim of this

budget to provide manufacturing unit which can meet the sales goal.

Contribution of production budget towards management in planning

It helps management in deciding the cost of production including labour and material,

so that sale goal can be achieved effectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.