Corporate Accounting Report: Gazal Corp's Cash Flow and Balance Sheet

VerifiedAdded on 2021/05/31

|10

|884

|301

Report

AI Summary

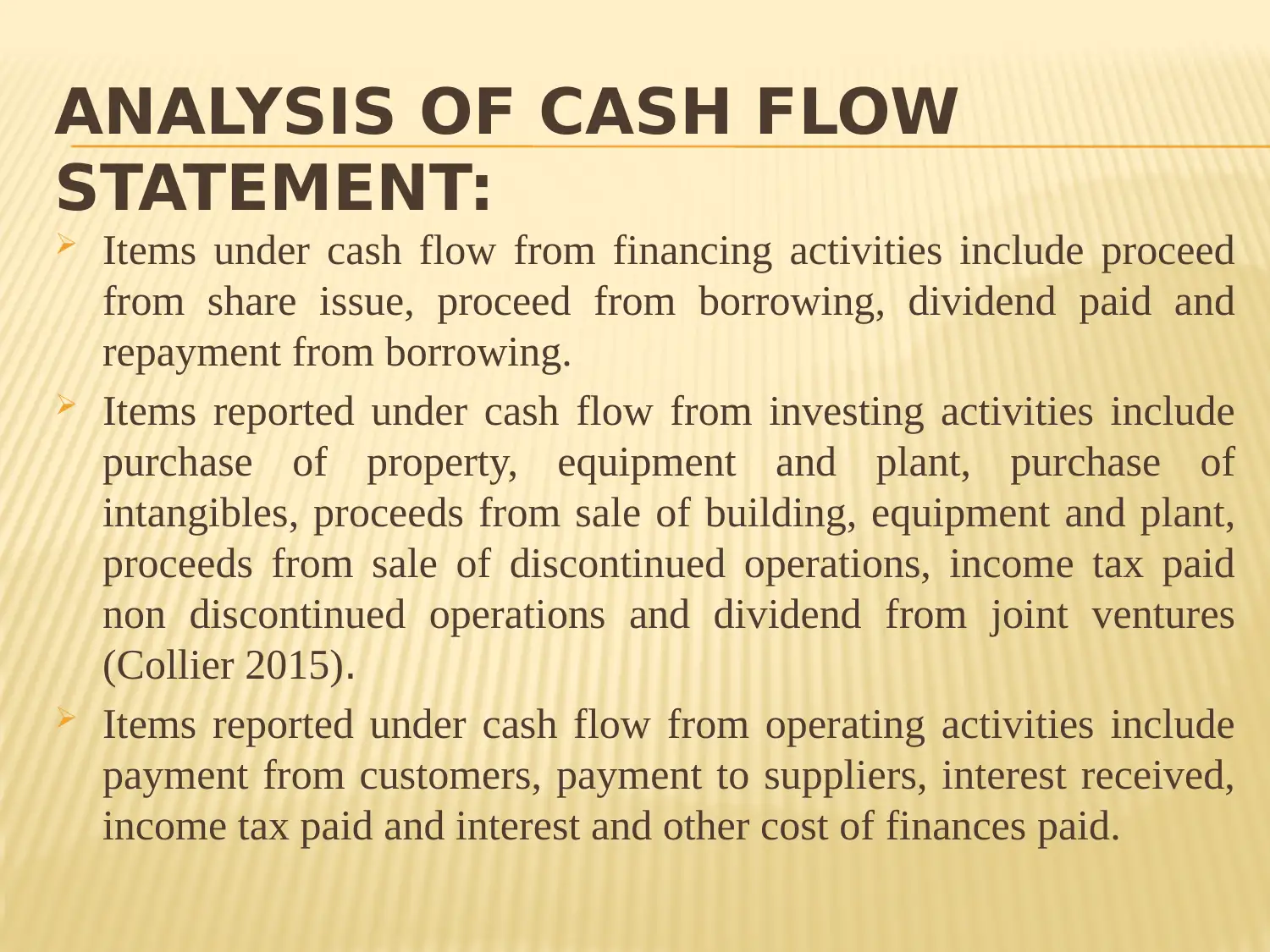

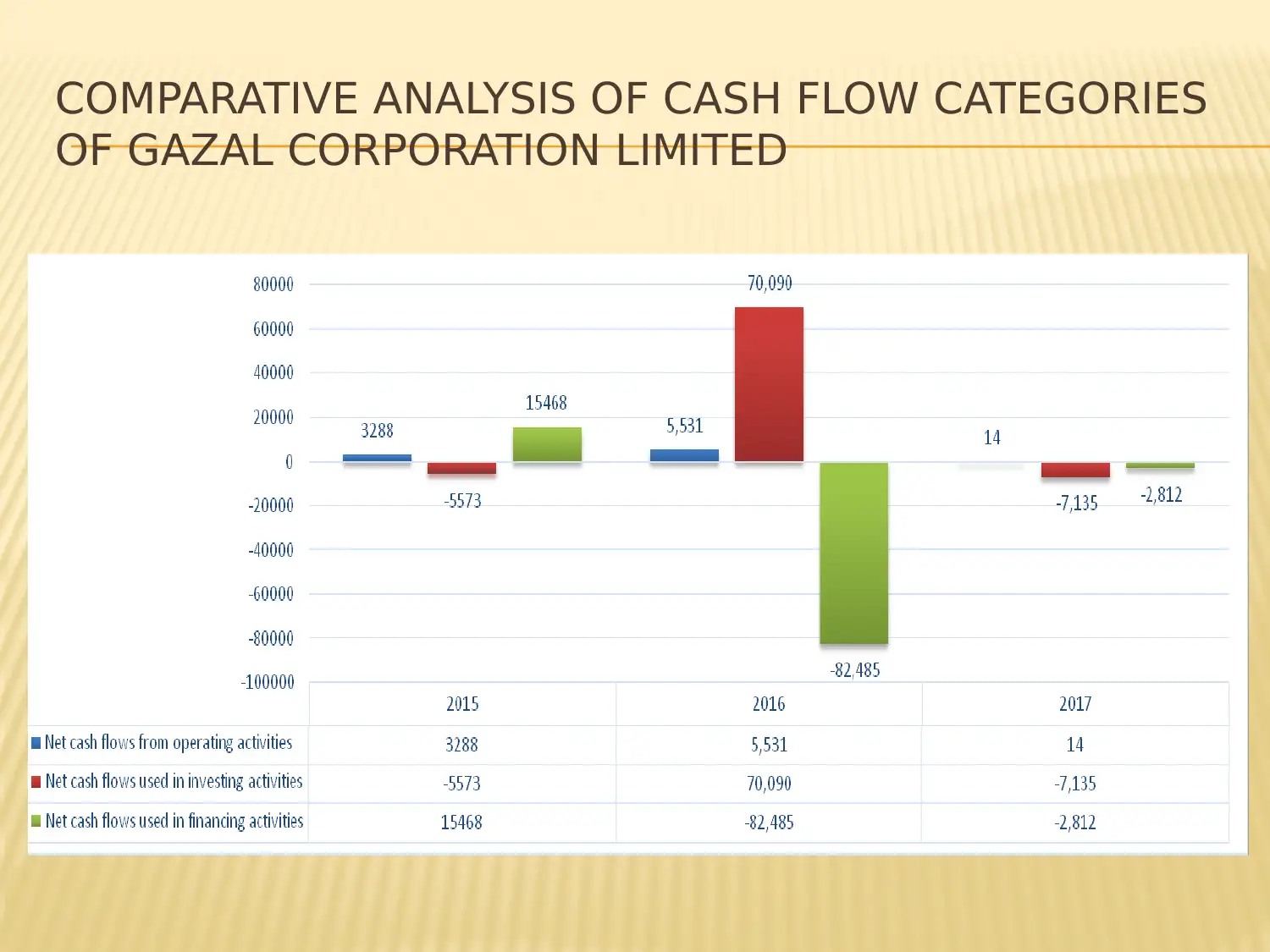

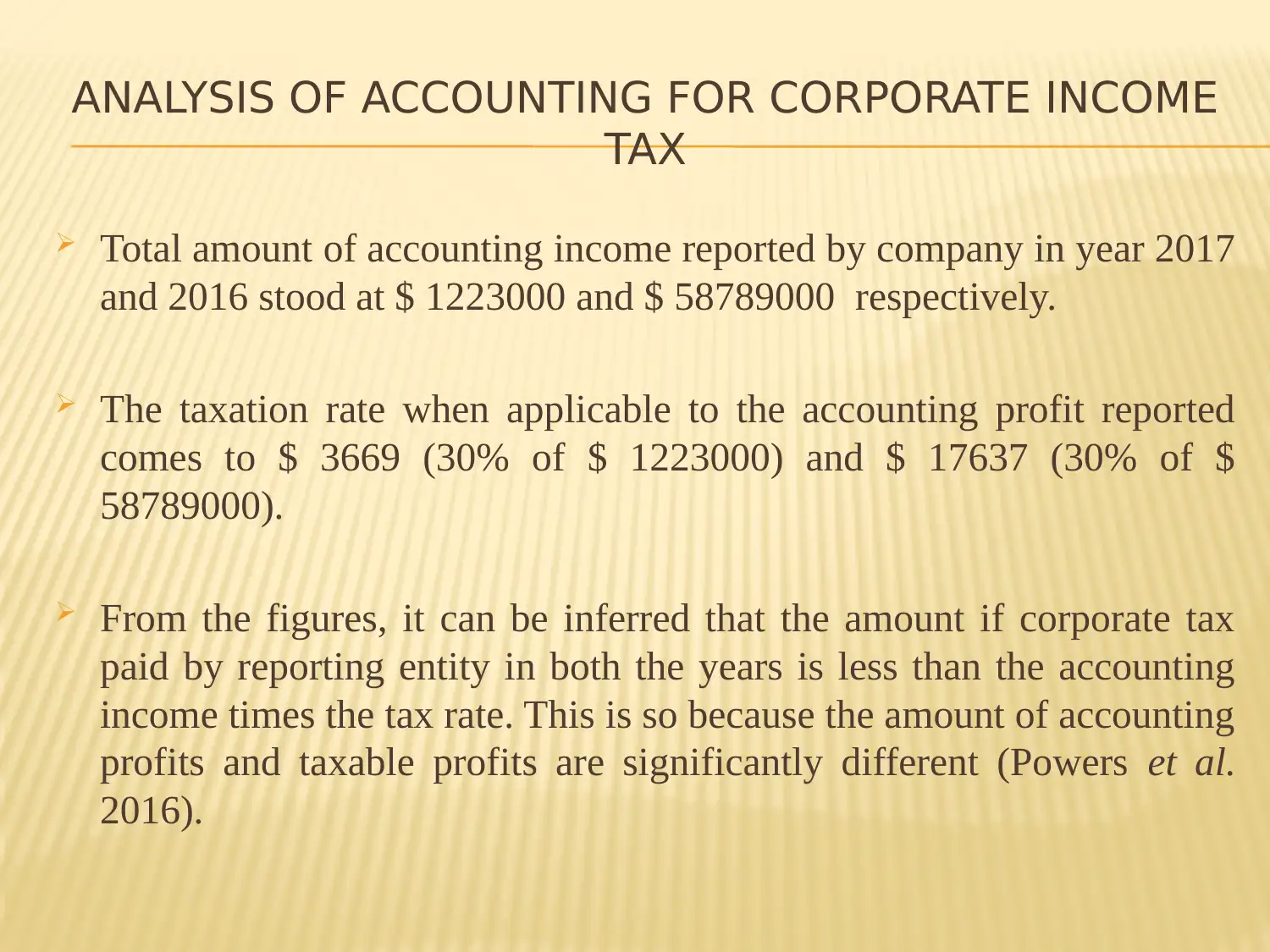

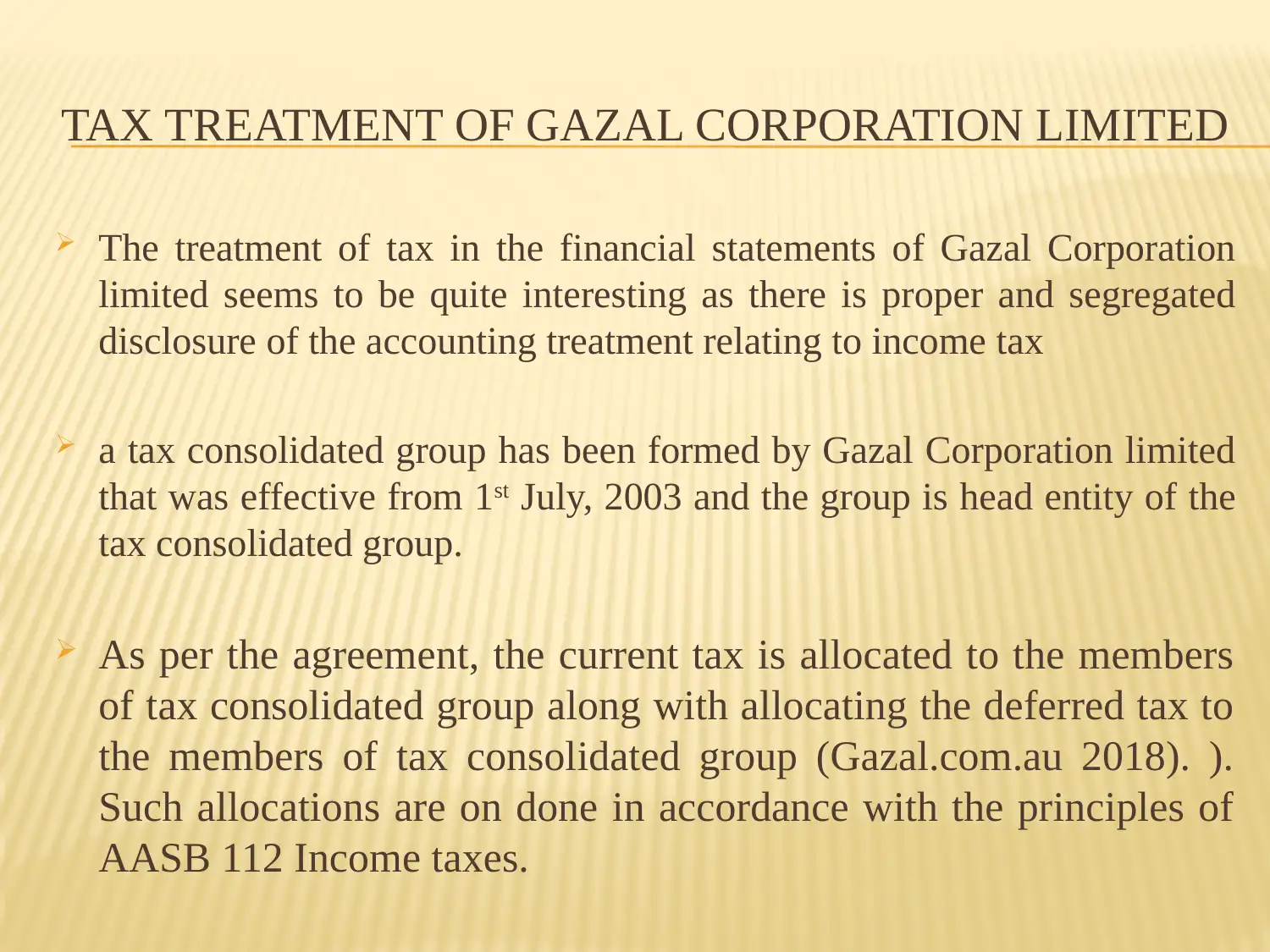

This report provides a comprehensive analysis of Gazal Corporation Limited's financial statements, focusing on the cash flow statement, balance sheet, and other comprehensive income statement. The analysis includes a breakdown of cash flow activities (operating, investing, and financing), a comparative analysis of cash flow categories, and an examination of items recorded in the comprehensive income statement, such as exchange differences and revaluation of assets. Furthermore, the report delves into the accounting treatment of corporate income tax, comparing tax expenses across different years and assessing the relationship between accounting income and taxable profits. The tax treatment of Gazal Corporation Limited is also examined, with a focus on its tax consolidated group structure and the allocation of current and deferred tax. The report concludes with a summary of key findings and references to relevant accounting standards and literature.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.