Capital Budgeting: Cost of Equity, NPV, IRR, and MIRR Solutions

VerifiedAdded on 2022/09/06

|9

|1291

|22

Homework Assignment

AI Summary

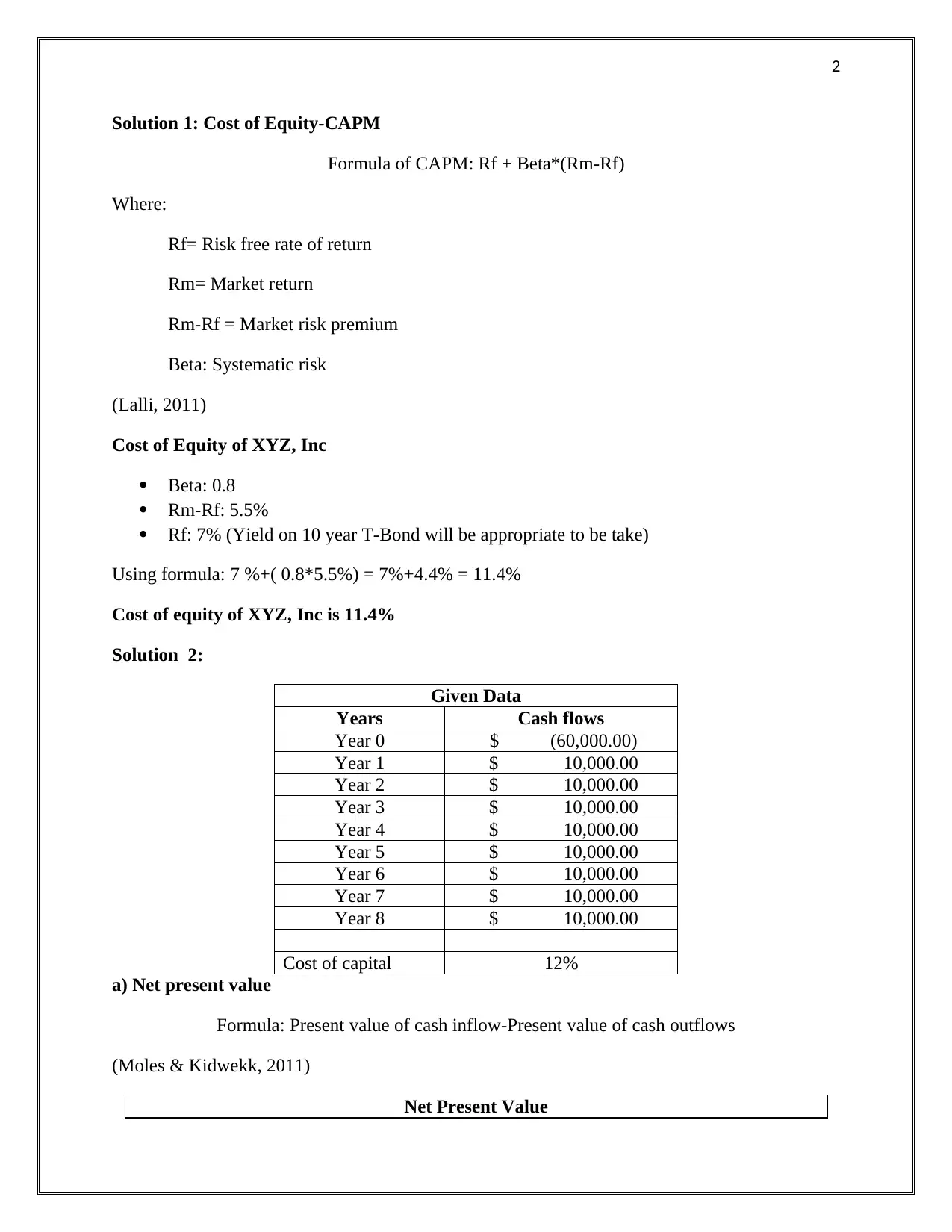

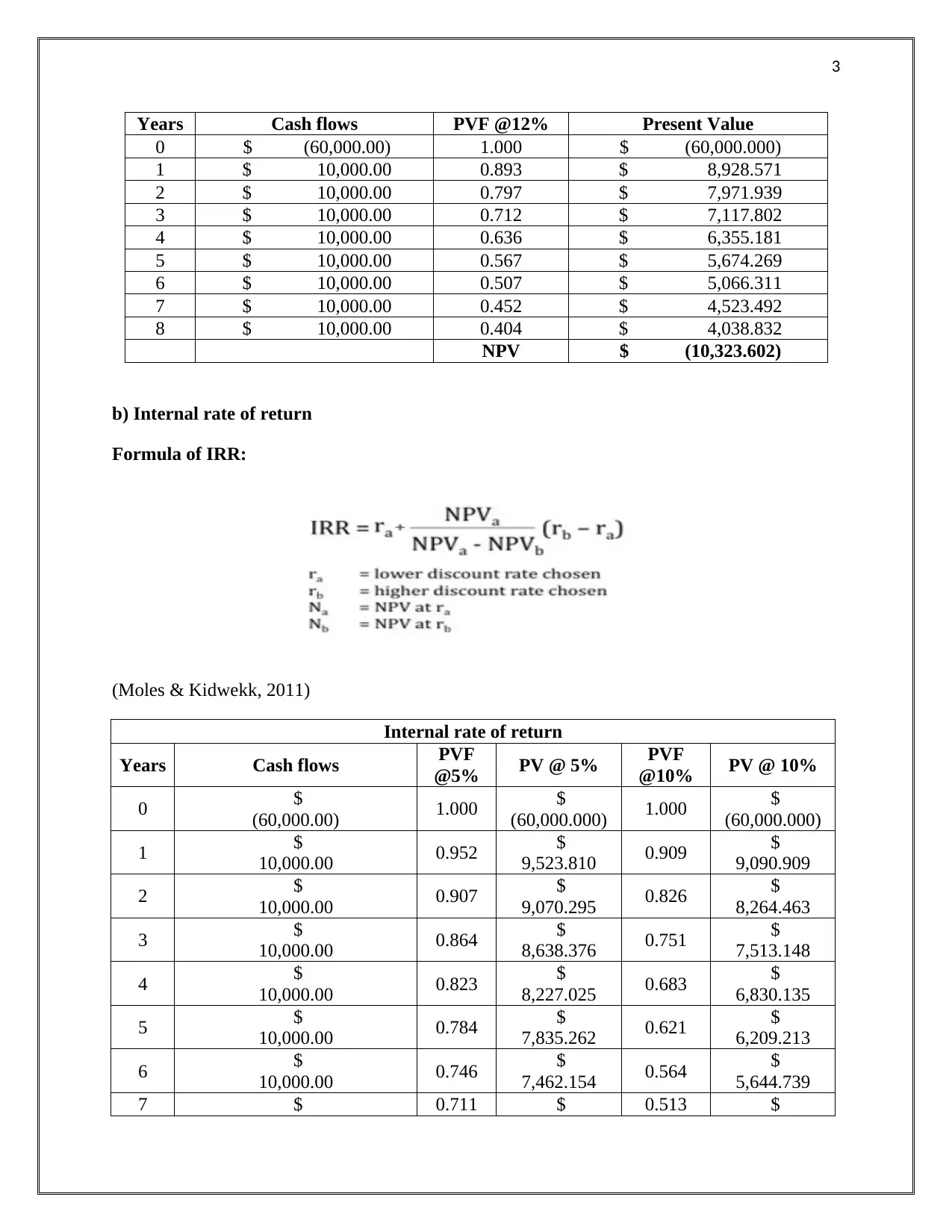

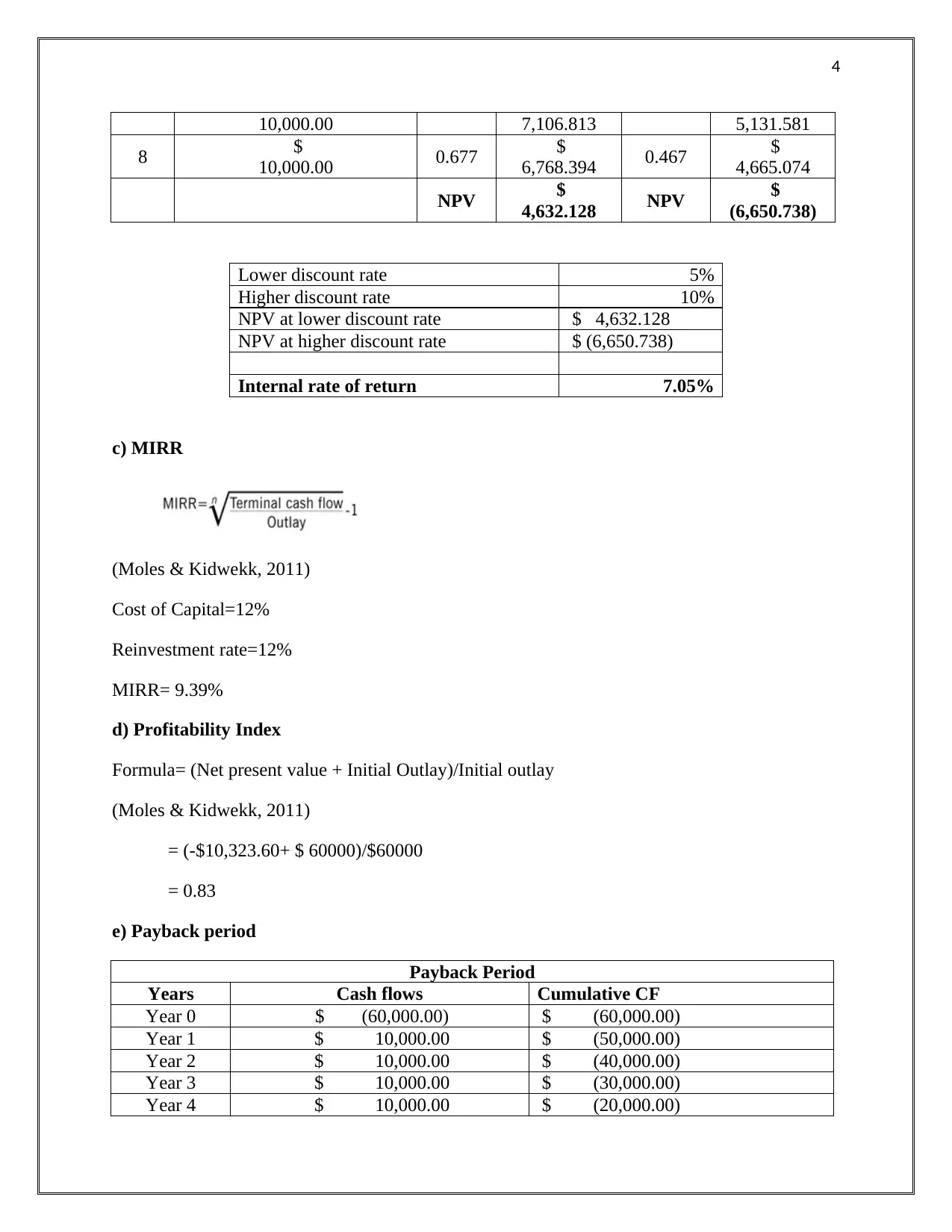

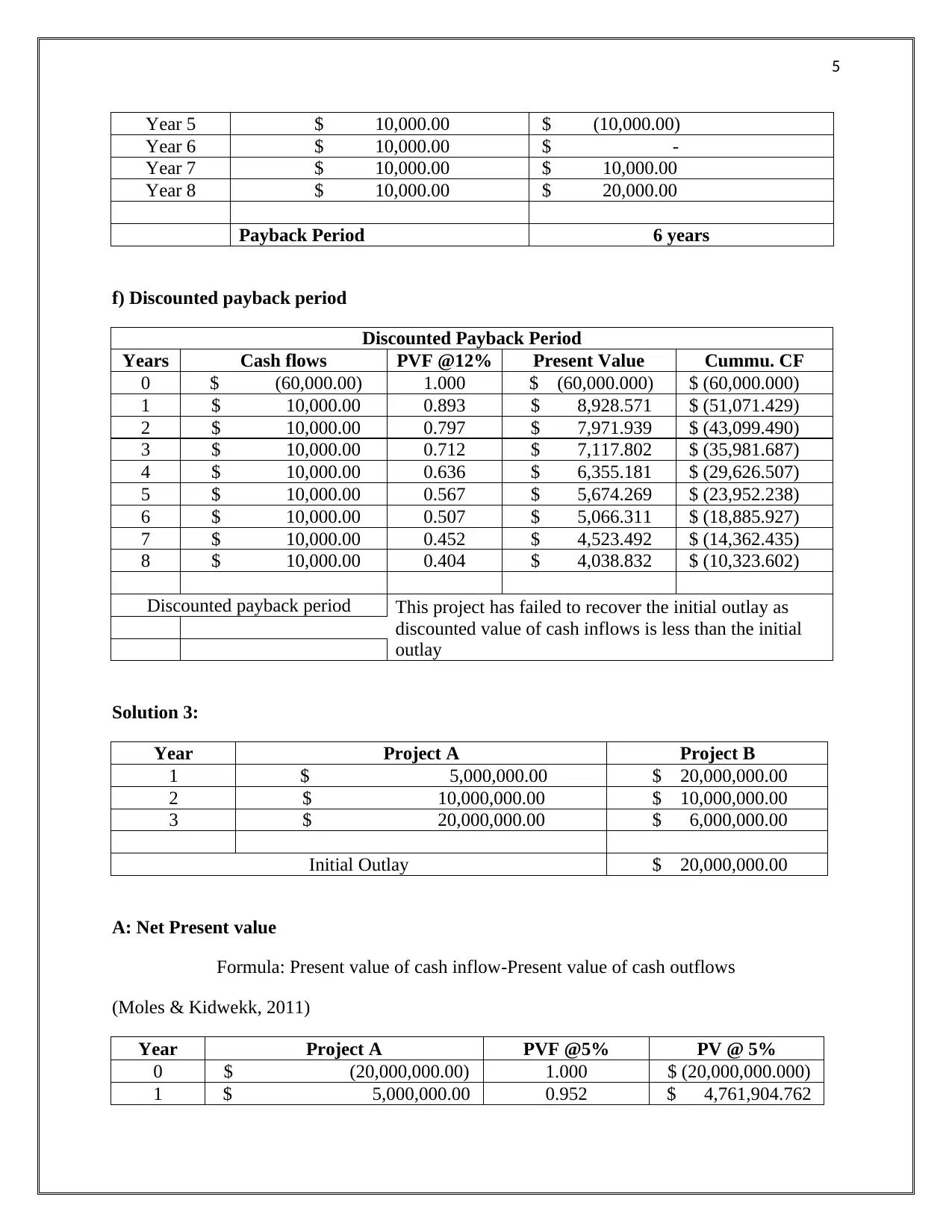

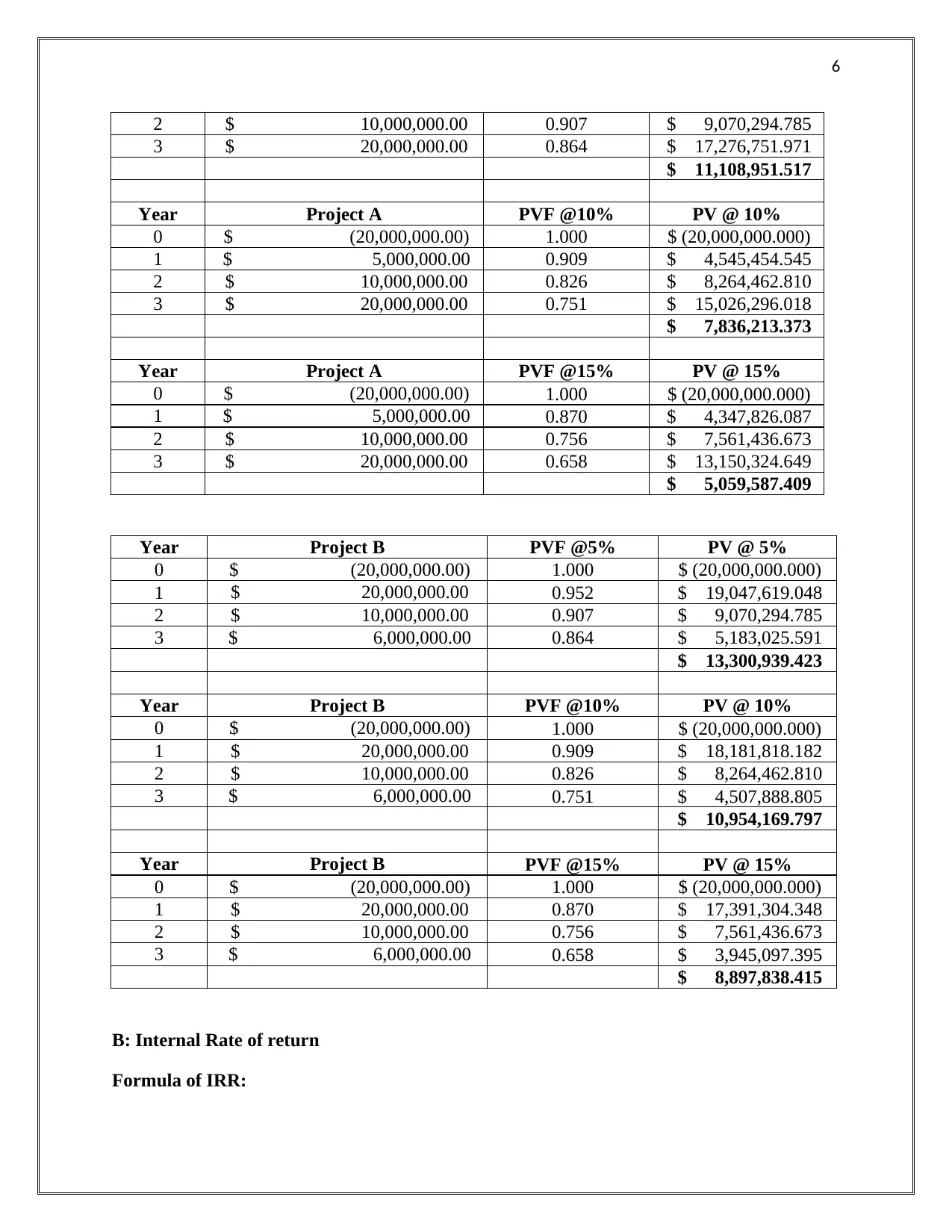

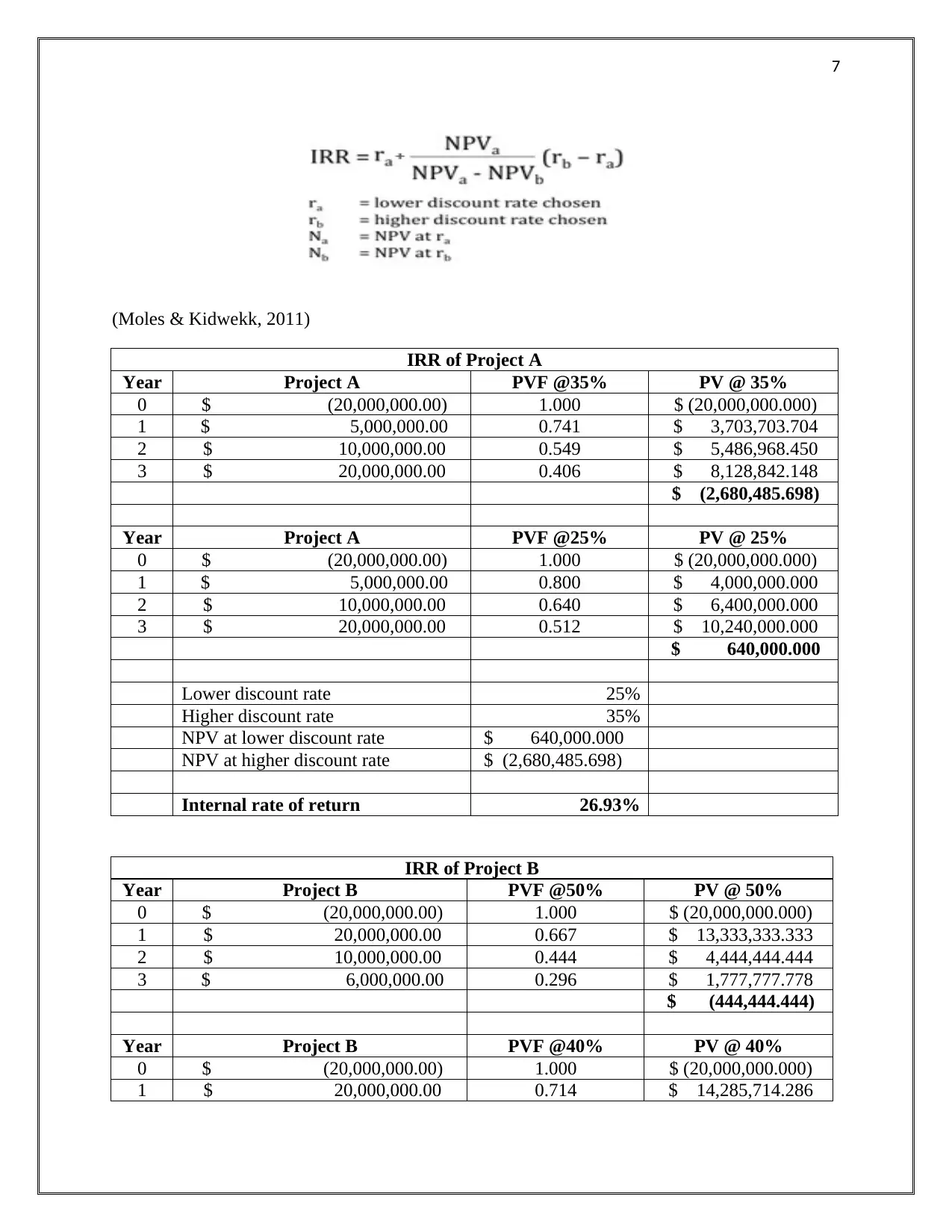

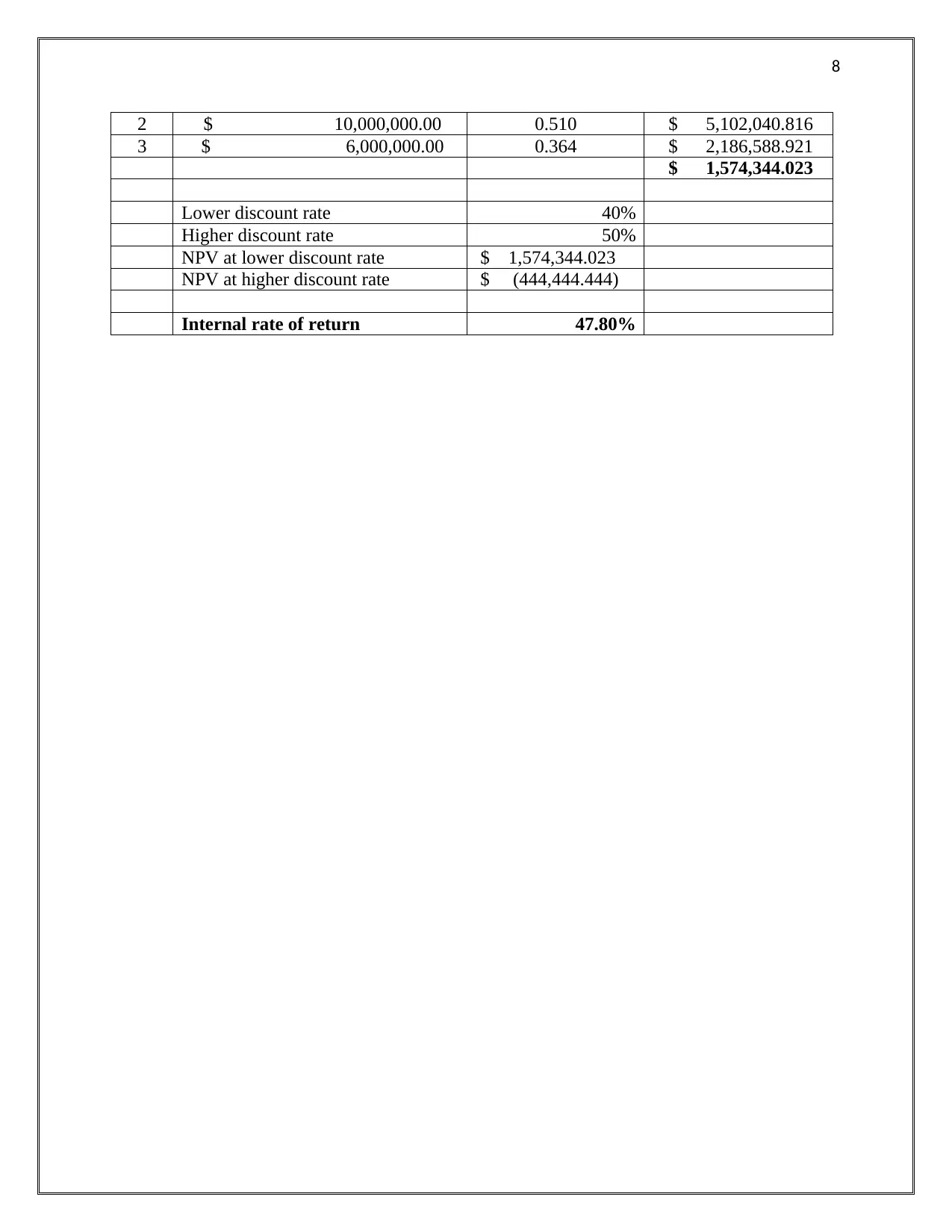

This document provides a comprehensive set of solutions for a capital budgeting assignment. The solutions cover various aspects of financial analysis and investment project evaluation. The document begins by calculating the cost of equity using the Capital Asset Pricing Model (CAPM). It then proceeds to analyze a project using Net Present Value (NPV), Internal Rate of Return (IRR), Modified Internal Rate of Return (MIRR), Profitability Index (PI), Payback Period, and Discounted Payback Period. The assignment also includes a comparative analysis of two projects, calculating NPV and IRR at different discount rates for each. The analysis includes formulas and step-by-step calculations to illustrate each concept. The document provides a clear understanding of capital budgeting techniques and their application in financial decision-making.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.