Finance and Decision-Making Report: GEC and SIG Plc Analysis, 2016

VerifiedAdded on 2020/02/05

|9

|2583

|72

Report

AI Summary

This report presents a financial analysis of General Electronic Company (GEC) and SIG Plc, focusing on profitability and liquidity. The first part of the report examines GEC's financial performance through ratio analysis, revealing trends in gross profit, net profit, current ratio, and quick ratio over several years. The analysis highlights the importance of financial ratios for decision-making and acknowledges their limitations. The second part evaluates an investment opportunity for SIG Plc, employing Net Present Value (NPV) and Internal Rate of Return (IRR) to assess the project's viability. The report suggests investment based on positive NPV and a higher IRR than the cost of capital. It also discusses financing options and critically analyzes the challenges in mergers and acquisitions (M&A), particularly cultural differences, employee retention, and the impact of technological advancements on the M&A process. The report concludes that the proposed project for SIG Plc is a viable investment opportunity.

FINANCE AND DECISION-MAKING

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

ASSESSMENT 1..................................................................................................................................3

1. Profitability and liquidity ratios...................................................................................................3

2. Analysis and interpretation..........................................................................................................3

3. Critically evaluate the use and limitations of financial ratios......................................................4

ASSESSMENT 2..................................................................................................................................4

Project evaluation............................................................................................................................5

Appraising the financing section.....................................................................................................6

Critically analysing the challenges in M&A....................................................................................6

CONCLUSION....................................................................................................................................7

REFERENCES.....................................................................................................................................8

APPENDIX..........................................................................................................................................9

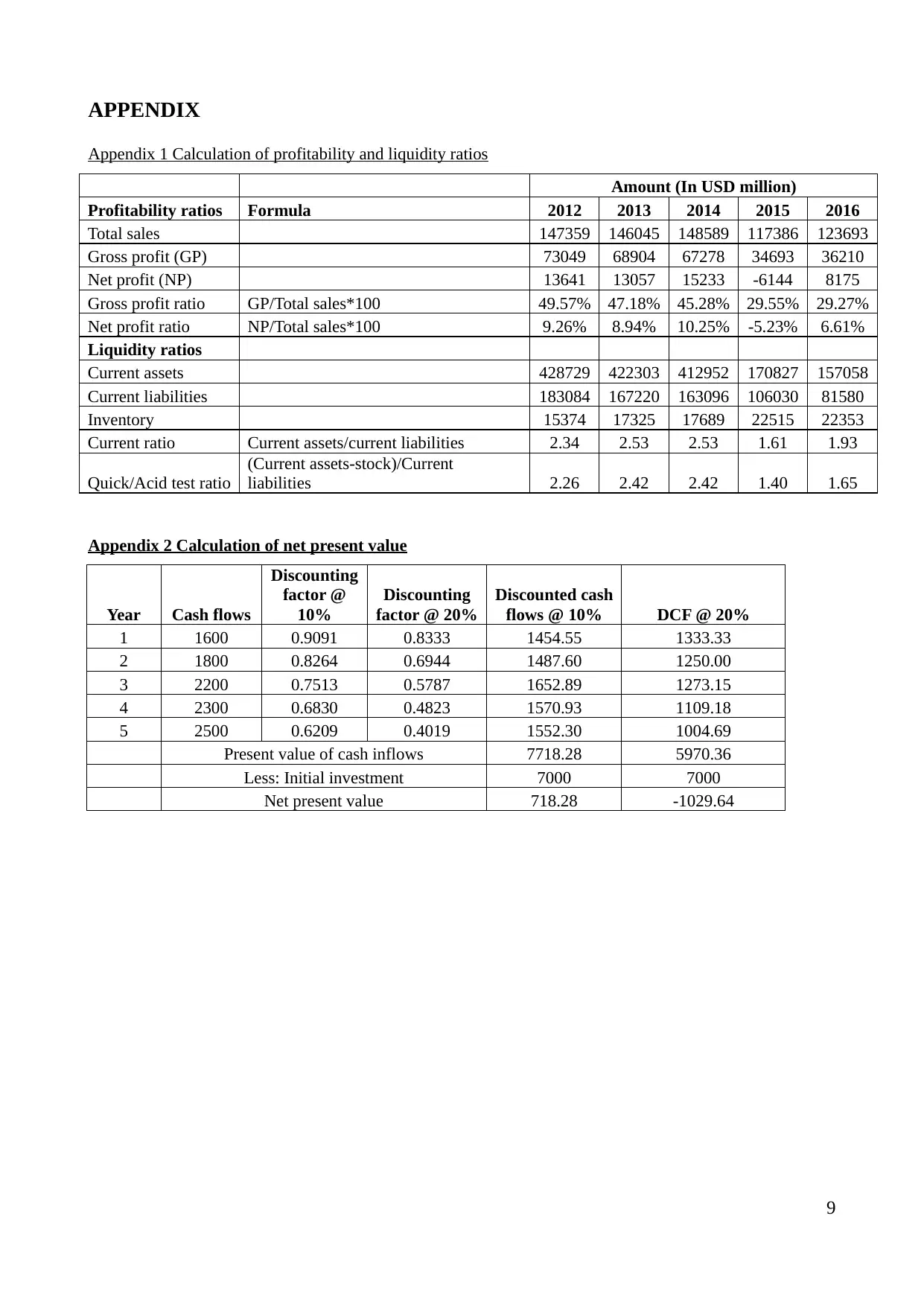

Appendix 1 Calculation of profitability and liquidity ratios............................................................9

Appendix 2 Calculation of net present value...................................................................................9

2

INTRODUCTION................................................................................................................................3

ASSESSMENT 1..................................................................................................................................3

1. Profitability and liquidity ratios...................................................................................................3

2. Analysis and interpretation..........................................................................................................3

3. Critically evaluate the use and limitations of financial ratios......................................................4

ASSESSMENT 2..................................................................................................................................4

Project evaluation............................................................................................................................5

Appraising the financing section.....................................................................................................6

Critically analysing the challenges in M&A....................................................................................6

CONCLUSION....................................................................................................................................7

REFERENCES.....................................................................................................................................8

APPENDIX..........................................................................................................................................9

Appendix 1 Calculation of profitability and liquidity ratios............................................................9

Appendix 2 Calculation of net present value...................................................................................9

2

INTRODUCTION

In the highly uncertain and competitive market place, companies directors and managers are

require to analyze the financial position and performance of the business so as to make right

decisions at right time for deriving success. The present report aims at making profitability and

liquidity analysis of GEC (General Electronic Company) through ratio analysis. Moreover, it will

also apply modern discounted capital budgeting techniques like NPV and IRR for the project

evaluation to assess viability.

ASSESSMENT 1

1. Profitability and liquidity ratios

Ratio analysis is an strategic financial analysis (SFA) technique that indicates magnitude of

relationship between two components of the financial accounts. As per the scenario, GEC Plc is a

leading company that is involved in supplying electronics and engineering goods to the consumers.

Its manager can examine the financial performance of the firms through interpreting various ratios.

Profitability ratios are the measurement of percentage of return on total sales revenues and enable

managers to determine that whether business performed well or not (Hwang and Yoon, 2012). In

this, gross profit percentage is often used to measure the percentage of GP on total turnover whereas

net profit percentage is used to determine the NP % on total sales revenue. On the contrary, liquidity

ratios are used to quantify GEC Plc’s capability to pay suppliers and other short-term liabilities on

right time. Current ratio measure relationship between current assets and current liabilities whereas

quick/acid test ratio measures liquidity performance of the firm ignoring inventory balances.

2. Analysis and interpretation

Profitability ratios

Gross profit ratio: GEC’s GP ratio shows a continuous decreasing trend from 49.57% to

29.27% in the year 2016. High fluctuations in the turnover over the period due to volatile consumer

demand, inflation and competitors offerings is the main reason behind decreasing net profitability.

Although, cost of the goods sold shows a declined trend, still, high % fall in turnover decreased the

gross profitability of the firm and indicates that GEC gained less gross return on total sales.

Net profit ratio: In 2014, firm’s NP ratio got up to 10.25% indicates that company generated

better return on sales, however, thereafter it dropped down to -5.23% exhibit loss due to excessive

overheads because of poor control (Financial ratio of General Electronic Company, 2013). After

this, in 2016, it rose up to 6.61% demonstrates that firm gathered high return this year on total sales

revenue and indicates good performance.

3

In the highly uncertain and competitive market place, companies directors and managers are

require to analyze the financial position and performance of the business so as to make right

decisions at right time for deriving success. The present report aims at making profitability and

liquidity analysis of GEC (General Electronic Company) through ratio analysis. Moreover, it will

also apply modern discounted capital budgeting techniques like NPV and IRR for the project

evaluation to assess viability.

ASSESSMENT 1

1. Profitability and liquidity ratios

Ratio analysis is an strategic financial analysis (SFA) technique that indicates magnitude of

relationship between two components of the financial accounts. As per the scenario, GEC Plc is a

leading company that is involved in supplying electronics and engineering goods to the consumers.

Its manager can examine the financial performance of the firms through interpreting various ratios.

Profitability ratios are the measurement of percentage of return on total sales revenues and enable

managers to determine that whether business performed well or not (Hwang and Yoon, 2012). In

this, gross profit percentage is often used to measure the percentage of GP on total turnover whereas

net profit percentage is used to determine the NP % on total sales revenue. On the contrary, liquidity

ratios are used to quantify GEC Plc’s capability to pay suppliers and other short-term liabilities on

right time. Current ratio measure relationship between current assets and current liabilities whereas

quick/acid test ratio measures liquidity performance of the firm ignoring inventory balances.

2. Analysis and interpretation

Profitability ratios

Gross profit ratio: GEC’s GP ratio shows a continuous decreasing trend from 49.57% to

29.27% in the year 2016. High fluctuations in the turnover over the period due to volatile consumer

demand, inflation and competitors offerings is the main reason behind decreasing net profitability.

Although, cost of the goods sold shows a declined trend, still, high % fall in turnover decreased the

gross profitability of the firm and indicates that GEC gained less gross return on total sales.

Net profit ratio: In 2014, firm’s NP ratio got up to 10.25% indicates that company generated

better return on sales, however, thereafter it dropped down to -5.23% exhibit loss due to excessive

overheads because of poor control (Financial ratio of General Electronic Company, 2013). After

this, in 2016, it rose up to 6.61% demonstrates that firm gathered high return this year on total sales

revenue and indicates good performance.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Liquidity ratios

Current ratio: GEC’s CR got up from 2.34:1 to 2.53:1 in 2014 due to increased inventory,

receivables and other current assets, still, as the ratio is greater than the target ratio of 2:1 indicates

ineffective use of CA in productive functions. However, in 2016, it came down to 1.93:1 near to the

standard ratio exhibits that firm strengthen their position to make deferral payments of short-term

liabilities on due date.

Quick ratio: In 2016, the ratio dropped down from 2.26:1 to 1.65:1, but still, it is above the

target ratio of 1:1 shows that GEC has enough or sufficient resources available to pay creditors

timely without having inventory balance in the business (Provost and Fawcett, 2013).

3. Critically evaluate the use and limitations of financial ratios

Importance:

Financial ratios enable GEC’s managers to determine and examine their profitability

performance, as a result, managers can make smarter choices and rational decisions like cost-

controlling, pricing & marketing decisions to minimize expenditures and maximize revenue results

in high return. However, by evaluating the liquidity performance, directors can determine the

availability of current assets in comparison to the short-term obligations and manage resources

optimally for making payment to the suppliers and manage liquidity.

Limitations:

Change in the accounting policies, rules & regulations over the year may mislead the results

derived through ratio analysis. Moreover, incorrect figures reported in the final accounts also

provide misleading interpretation and leads to take inappropriate decisions (Newell, Lagnado and

Shanks, 2015). Further, it is based on historical analysis and numerical values, and does not provide

any assistance to examine and evaluate the qualitative performance of the business.

ASSESSMENT 2

4

Current ratio: GEC’s CR got up from 2.34:1 to 2.53:1 in 2014 due to increased inventory,

receivables and other current assets, still, as the ratio is greater than the target ratio of 2:1 indicates

ineffective use of CA in productive functions. However, in 2016, it came down to 1.93:1 near to the

standard ratio exhibits that firm strengthen their position to make deferral payments of short-term

liabilities on due date.

Quick ratio: In 2016, the ratio dropped down from 2.26:1 to 1.65:1, but still, it is above the

target ratio of 1:1 shows that GEC has enough or sufficient resources available to pay creditors

timely without having inventory balance in the business (Provost and Fawcett, 2013).

3. Critically evaluate the use and limitations of financial ratios

Importance:

Financial ratios enable GEC’s managers to determine and examine their profitability

performance, as a result, managers can make smarter choices and rational decisions like cost-

controlling, pricing & marketing decisions to minimize expenditures and maximize revenue results

in high return. However, by evaluating the liquidity performance, directors can determine the

availability of current assets in comparison to the short-term obligations and manage resources

optimally for making payment to the suppliers and manage liquidity.

Limitations:

Change in the accounting policies, rules & regulations over the year may mislead the results

derived through ratio analysis. Moreover, incorrect figures reported in the final accounts also

provide misleading interpretation and leads to take inappropriate decisions (Newell, Lagnado and

Shanks, 2015). Further, it is based on historical analysis and numerical values, and does not provide

any assistance to examine and evaluate the qualitative performance of the business.

ASSESSMENT 2

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To: BOD, SIG Plc

From: Financial controller

Date: 7th March 2016

Subject: Investment appraisal and challenges in merger and acquisition

Project evaluation

SIG Plc is a leading supplier of special building products in Europe and in the current

market, there are two investment opportunities is considering by the firm for the investment in SIG

interior and acquisition purpose. The projected life time of the project is expected to 5 year at an

initial investment of £7,000,000. Investment appraisal techniques are the best way that suggest

investor whether to invest money or not to get an enough or adequate amount of return over the cost

of capital.

Discounted cash flow techniques of capital budgeting focuses on discounting the expected

cash flows of the project at an appropriate rate and thereafter determine the current value of cash

flows. NPV exhibits the excess of present value of cash inflows over beginning outlay, and positive

as well as high value of NPV is always considered best for the SIG Plc (Chauhan and Vaish, 2012).

However, uncertainty regarding inflation and interest that gives rises to the cost of capital is the

main risk associated with NPV. With regards to the stated project, NPV has been computed here at

10% discounting rate in Appendix 2.

NPV @ 10% (000) = £718.28

NPV @20% (000) = -£1029.64

Calculation of IRR

IRR quantify the discounting rate which equates the PV of cash inflow and outflow at zero

NPV, computed here as follows:

IRR = Lower discount rate + NPV at lower rate/NPV at lower rate – NPV at discount rate*(High

rate-lower rate)

= 10% + (£718.27)/( £718.27 - -£1029.64)*(20%-10%)

= 10% + (£718.27 / £1747.92)*10%

= 10% + 4%

= 14%

Finding the result of the capital budgeting, it can be suggested to the board members to

invest money in the project. It is because, as per the selection criteria of NPV, the project indicates

favourable return worth £718.28, thus, it will drive positive return to the company. Moreover,

5

From: Financial controller

Date: 7th March 2016

Subject: Investment appraisal and challenges in merger and acquisition

Project evaluation

SIG Plc is a leading supplier of special building products in Europe and in the current

market, there are two investment opportunities is considering by the firm for the investment in SIG

interior and acquisition purpose. The projected life time of the project is expected to 5 year at an

initial investment of £7,000,000. Investment appraisal techniques are the best way that suggest

investor whether to invest money or not to get an enough or adequate amount of return over the cost

of capital.

Discounted cash flow techniques of capital budgeting focuses on discounting the expected

cash flows of the project at an appropriate rate and thereafter determine the current value of cash

flows. NPV exhibits the excess of present value of cash inflows over beginning outlay, and positive

as well as high value of NPV is always considered best for the SIG Plc (Chauhan and Vaish, 2012).

However, uncertainty regarding inflation and interest that gives rises to the cost of capital is the

main risk associated with NPV. With regards to the stated project, NPV has been computed here at

10% discounting rate in Appendix 2.

NPV @ 10% (000) = £718.28

NPV @20% (000) = -£1029.64

Calculation of IRR

IRR quantify the discounting rate which equates the PV of cash inflow and outflow at zero

NPV, computed here as follows:

IRR = Lower discount rate + NPV at lower rate/NPV at lower rate – NPV at discount rate*(High

rate-lower rate)

= 10% + (£718.27)/( £718.27 - -£1029.64)*(20%-10%)

= 10% + (£718.27 / £1747.92)*10%

= 10% + 4%

= 14%

Finding the result of the capital budgeting, it can be suggested to the board members to

invest money in the project. It is because, as per the selection criteria of NPV, the project indicates

favourable return worth £718.28, thus, it will drive positive return to the company. Moreover,

5

project’s IRR is also greater from cost of capital of 10% to 14%, therefore, it recommend business

to put their money in the existing investment opportunity for SIG interior to earn return.

Appraising the financing section

There are various sources through which SIG Plc can gather required amount of capital for

the investment purpose such as fixed source of capital and fluctuating source of capital, under the

first, SIG’s directors has to bear fixed financial burden whilst under the fluctuating, cost of capital

do not remain fixed. For instance, if company take long-term borrowings from the bank, then it will

have to pay fixed amount of interest as a financial cost to the lender (Cabral, Grilo and Cruz-

Machado, 2012). Moreover, it can also issue preferences shares for the monetary collection and

have to pay a fixed rate of dividend to the shareholders. However, if it issue more equity (ordinary)

shares then, it will not be necessary for the SIG Plc to pay fixed dividend to the proprietors as it is a

kind of fluctuating capital and on this, dividend decisions are taken by the firm considering the

business profitability.

Critically analysing the challenges in M&A

SIG’s BOD are considering to acquire Bristol company at a transaction value of £20m, but

the directors are concerning about its financing and potential risk & challenges. Acquisition refers to

the process of getting ownership rights in another organization. In the given scenario, it is clearly

stated that SIG Plc’s managers are looking to acquire Bristol company. Although, M&A corporate

strategy helps firm to expand their operations, generate larger revenue and high market share, still,

there are number of difficulties faced by entrepreneurs in M&A. For instance, if both the acquiring

and acquisition companies are located in two different countries, then it gives rises to the cultural

challenges in M&A procedure. Moreover, employee retention is also a challenge exists at the time

of M&A. Inherently, at the time of acquisition, companies often face threatening situation to retain

their workforce in the organization because Bristol’s employees have negative perception and belief

towards organization’s stability and as a result, they can decide to leave the job. It also arise

challenges for the SIG. For instance, if Bristol employees require easy access to upper level

managers, flexible working practices and others and new management removes it, then workers will

be adversely affected results in shrinking productivity to a great extent (Jemison and Sitkin 2013).

In merger, company can pay larger focus to the integration and cost-cutting and avoid daily

functioning results in loss of revenue. With this, M&A strategy may fail to create significant value

for the shareholder.

Further, in the current age of globalization, the introduction of advanced and new

technologies leads to increase market uncertainty and create obstacles in M&A procedure. In

6

to put their money in the existing investment opportunity for SIG interior to earn return.

Appraising the financing section

There are various sources through which SIG Plc can gather required amount of capital for

the investment purpose such as fixed source of capital and fluctuating source of capital, under the

first, SIG’s directors has to bear fixed financial burden whilst under the fluctuating, cost of capital

do not remain fixed. For instance, if company take long-term borrowings from the bank, then it will

have to pay fixed amount of interest as a financial cost to the lender (Cabral, Grilo and Cruz-

Machado, 2012). Moreover, it can also issue preferences shares for the monetary collection and

have to pay a fixed rate of dividend to the shareholders. However, if it issue more equity (ordinary)

shares then, it will not be necessary for the SIG Plc to pay fixed dividend to the proprietors as it is a

kind of fluctuating capital and on this, dividend decisions are taken by the firm considering the

business profitability.

Critically analysing the challenges in M&A

SIG’s BOD are considering to acquire Bristol company at a transaction value of £20m, but

the directors are concerning about its financing and potential risk & challenges. Acquisition refers to

the process of getting ownership rights in another organization. In the given scenario, it is clearly

stated that SIG Plc’s managers are looking to acquire Bristol company. Although, M&A corporate

strategy helps firm to expand their operations, generate larger revenue and high market share, still,

there are number of difficulties faced by entrepreneurs in M&A. For instance, if both the acquiring

and acquisition companies are located in two different countries, then it gives rises to the cultural

challenges in M&A procedure. Moreover, employee retention is also a challenge exists at the time

of M&A. Inherently, at the time of acquisition, companies often face threatening situation to retain

their workforce in the organization because Bristol’s employees have negative perception and belief

towards organization’s stability and as a result, they can decide to leave the job. It also arise

challenges for the SIG. For instance, if Bristol employees require easy access to upper level

managers, flexible working practices and others and new management removes it, then workers will

be adversely affected results in shrinking productivity to a great extent (Jemison and Sitkin 2013).

In merger, company can pay larger focus to the integration and cost-cutting and avoid daily

functioning results in loss of revenue. With this, M&A strategy may fail to create significant value

for the shareholder.

Further, in the current age of globalization, the introduction of advanced and new

technologies leads to increase market uncertainty and create obstacles in M&A procedure. In

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

addition to this, in order to cope up with the M&A, SIG’s directors and managers requires too much

time, as a result, there is a risk that they can neglect their core business functioning. Although, there

are number of challenges, still, it provides benefits of size and global reach to the SIG through the

acquisition of Bristol. It helps to strengthen the competitive position through squeezing greater

efficiency; as a result, it can defeat rival firms.

CONCLUSION

Above project report concluded that GEC’s profitability performance and liquidity position

is strong indicates that it is generating good return on their total sales and capable to pay suppliers

on right time. Lastly, report founded that at 10% discounting rate, SIG Plc’s proposed project will

bring positive return and its IRR is also higher to 14% hence, it is a viable investment opportunity.

7

time, as a result, there is a risk that they can neglect their core business functioning. Although, there

are number of challenges, still, it provides benefits of size and global reach to the SIG through the

acquisition of Bristol. It helps to strengthen the competitive position through squeezing greater

efficiency; as a result, it can defeat rival firms.

CONCLUSION

Above project report concluded that GEC’s profitability performance and liquidity position

is strong indicates that it is generating good return on their total sales and capable to pay suppliers

on right time. Lastly, report founded that at 10% discounting rate, SIG Plc’s proposed project will

bring positive return and its IRR is also higher to 14% hence, it is a viable investment opportunity.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Cabral, I., Grilo, A. and Cruz-Machado, V., 2012. A decision-making model for lean, agile, resilient

and green supply chain management. International Journal of Production Research. 50(17).

pp. 4830-4845.

Chauhan, A. and Vaish, R., 2012. Magnetic material selection using multiple attribute decision

making approach. Materials & Design. 36. pp. 1-5.

Hwang, C. L. and Yoon, K., 2012. Multiple attribute decision making: methods and applications a

state-of-the-art survey. Springer Science & Business Media.

Newell, B. R., Lagnado, D. A. and Shanks, D. R., 2015. Straight choices: The psychology of

decision making. Psychology Press.

Provost, F. and Fawcett, T., 2013. Data science and its relationship to big data and data-driven

decision making. Big Data. 1(1). pp. 51-59.

Online

Financial ratio of General Electronic Company. 2013. [Online]. Available through: <

http://financials.morningstar.com/balance-sheet/bs.html?t=GE®ion=usa&culture=en-

US>. [Accessed on 7th March 2016].

Jemison, D. and Sitkin, B. S., 2013. Acquisition: The Process Can be a problem. [Online]. Available

through: https://hbr.org/1986/03/acquisitions-the-process-can-be-a-problem. [Accessed on

7th March 2016].

8

Books and Journals

Cabral, I., Grilo, A. and Cruz-Machado, V., 2012. A decision-making model for lean, agile, resilient

and green supply chain management. International Journal of Production Research. 50(17).

pp. 4830-4845.

Chauhan, A. and Vaish, R., 2012. Magnetic material selection using multiple attribute decision

making approach. Materials & Design. 36. pp. 1-5.

Hwang, C. L. and Yoon, K., 2012. Multiple attribute decision making: methods and applications a

state-of-the-art survey. Springer Science & Business Media.

Newell, B. R., Lagnado, D. A. and Shanks, D. R., 2015. Straight choices: The psychology of

decision making. Psychology Press.

Provost, F. and Fawcett, T., 2013. Data science and its relationship to big data and data-driven

decision making. Big Data. 1(1). pp. 51-59.

Online

Financial ratio of General Electronic Company. 2013. [Online]. Available through: <

http://financials.morningstar.com/balance-sheet/bs.html?t=GE®ion=usa&culture=en-

US>. [Accessed on 7th March 2016].

Jemison, D. and Sitkin, B. S., 2013. Acquisition: The Process Can be a problem. [Online]. Available

through: https://hbr.org/1986/03/acquisitions-the-process-can-be-a-problem. [Accessed on

7th March 2016].

8

APPENDIX

Appendix 1 Calculation of profitability and liquidity ratios

Amount (In USD million)

Profitability ratios Formula 2012 2013 2014 2015 2016

Total sales 147359 146045 148589 117386 123693

Gross profit (GP) 73049 68904 67278 34693 36210

Net profit (NP) 13641 13057 15233 -6144 8175

Gross profit ratio GP/Total sales*100 49.57% 47.18% 45.28% 29.55% 29.27%

Net profit ratio NP/Total sales*100 9.26% 8.94% 10.25% -5.23% 6.61%

Liquidity ratios

Current assets 428729 422303 412952 170827 157058

Current liabilities 183084 167220 163096 106030 81580

Inventory 15374 17325 17689 22515 22353

Current ratio Current assets/current liabilities 2.34 2.53 2.53 1.61 1.93

Quick/Acid test ratio

(Current assets-stock)/Current

liabilities 2.26 2.42 2.42 1.40 1.65

Appendix 2 Calculation of net present value

Year Cash flows

Discounting

factor @

10%

Discounting

factor @ 20%

Discounted cash

flows @ 10% DCF @ 20%

1 1600 0.9091 0.8333 1454.55 1333.33

2 1800 0.8264 0.6944 1487.60 1250.00

3 2200 0.7513 0.5787 1652.89 1273.15

4 2300 0.6830 0.4823 1570.93 1109.18

5 2500 0.6209 0.4019 1552.30 1004.69

Present value of cash inflows 7718.28 5970.36

Less: Initial investment 7000 7000

Net present value 718.28 -1029.64

9

Appendix 1 Calculation of profitability and liquidity ratios

Amount (In USD million)

Profitability ratios Formula 2012 2013 2014 2015 2016

Total sales 147359 146045 148589 117386 123693

Gross profit (GP) 73049 68904 67278 34693 36210

Net profit (NP) 13641 13057 15233 -6144 8175

Gross profit ratio GP/Total sales*100 49.57% 47.18% 45.28% 29.55% 29.27%

Net profit ratio NP/Total sales*100 9.26% 8.94% 10.25% -5.23% 6.61%

Liquidity ratios

Current assets 428729 422303 412952 170827 157058

Current liabilities 183084 167220 163096 106030 81580

Inventory 15374 17325 17689 22515 22353

Current ratio Current assets/current liabilities 2.34 2.53 2.53 1.61 1.93

Quick/Acid test ratio

(Current assets-stock)/Current

liabilities 2.26 2.42 2.42 1.40 1.65

Appendix 2 Calculation of net present value

Year Cash flows

Discounting

factor @

10%

Discounting

factor @ 20%

Discounted cash

flows @ 10% DCF @ 20%

1 1600 0.9091 0.8333 1454.55 1333.33

2 1800 0.8264 0.6944 1487.60 1250.00

3 2200 0.7513 0.5787 1652.89 1273.15

4 2300 0.6830 0.4823 1570.93 1109.18

5 2500 0.6209 0.4019 1552.30 1004.69

Present value of cash inflows 7718.28 5970.36

Less: Initial investment 7000 7000

Net present value 718.28 -1029.64

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.