Accounting and Finance Report: Cash Flow Analysis of Corporations

VerifiedAdded on 2020/05/28

|7

|844

|154

Report

AI Summary

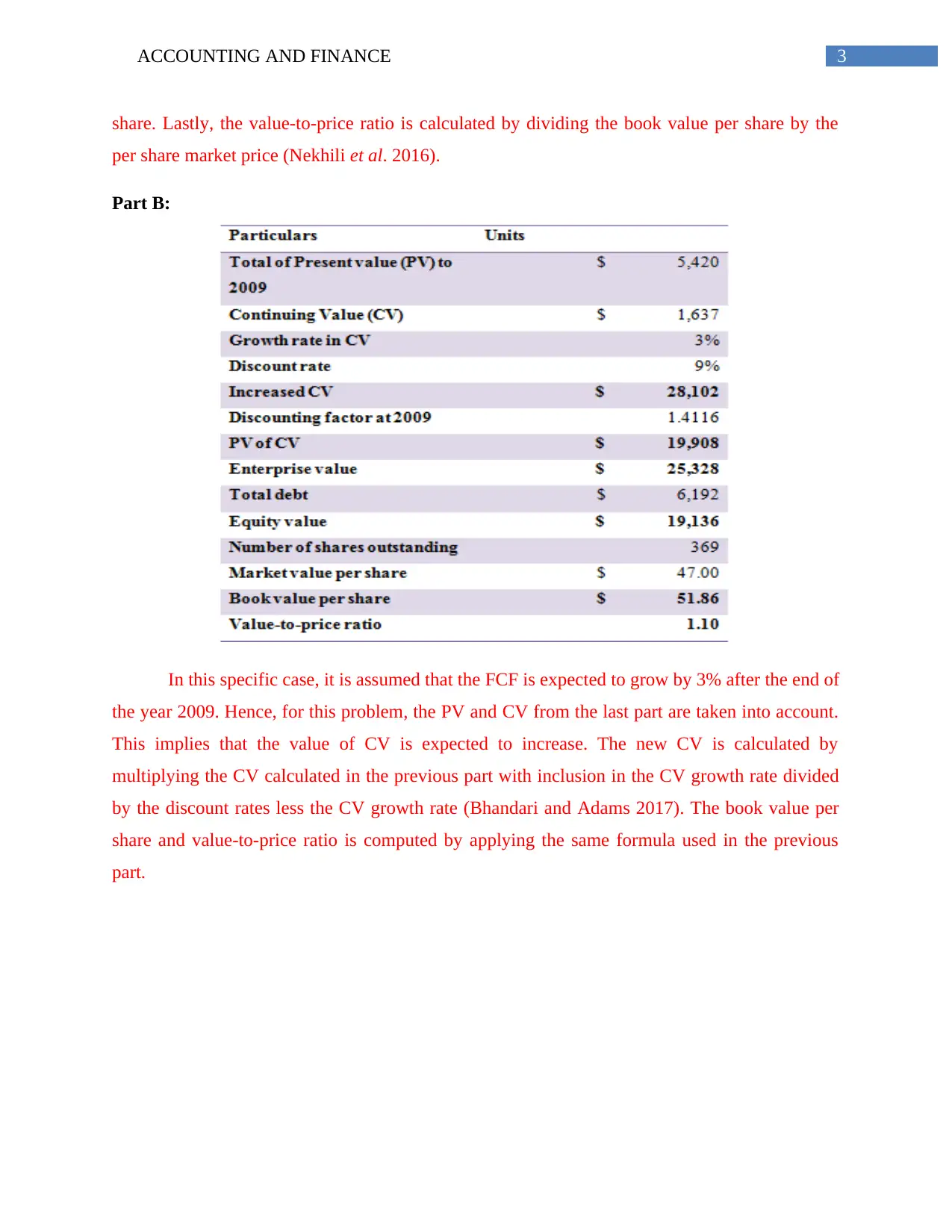

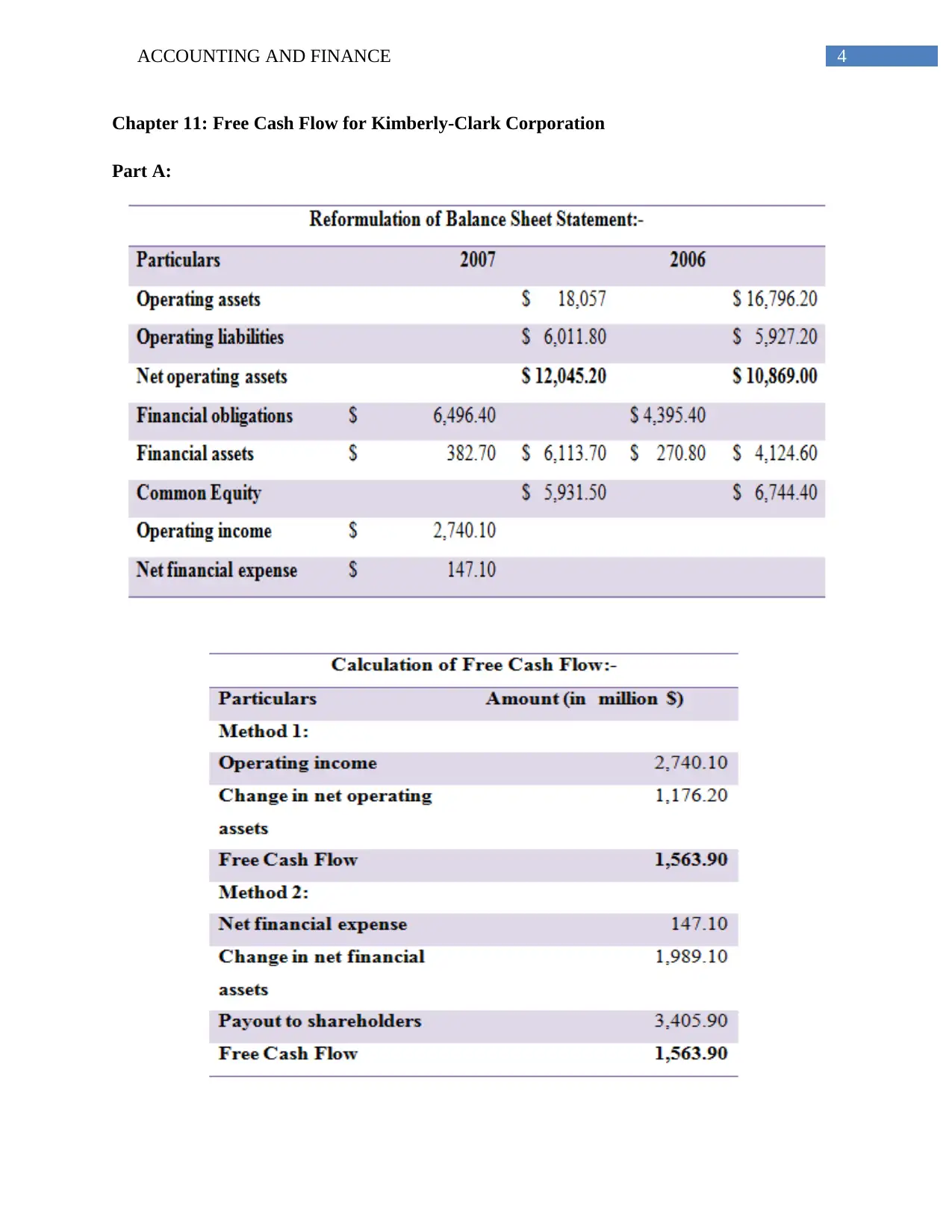

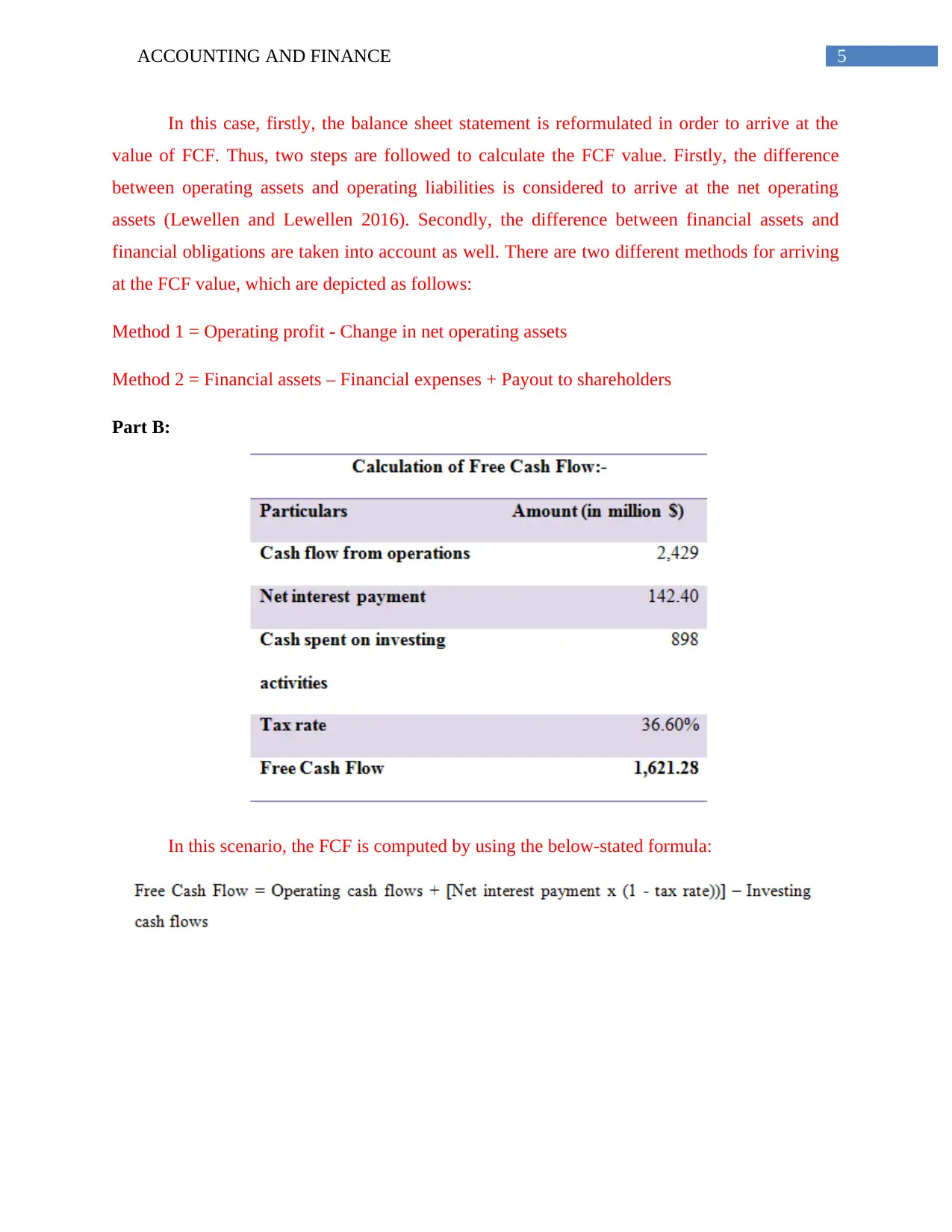

This report provides a detailed analysis of cash flow valuation, focusing on discounted cash flow (DCF) and free cash flow (FCF) methods. It examines two case studies: General Mills, Inc., and Kimberly-Clark Corporation. The report calculates FCF, present value (PV), continuing value (CV), and enterprise value (EV) under different growth rate assumptions. It also covers the calculation of book value per share and value-to-price ratios. For Kimberly-Clark, the report reformulates the balance sheet to determine FCF using two methods: operating profit adjustments and financial asset/obligation differences. The report includes references to relevant academic literature on cash flow analysis and valuation techniques. This report is designed to aid students in understanding and applying financial modeling concepts.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.