Genworth Mortgage Financial Reporting: A Contemporary Issues Analysis

VerifiedAdded on 2023/01/20

|17

|2469

|37

Report

AI Summary

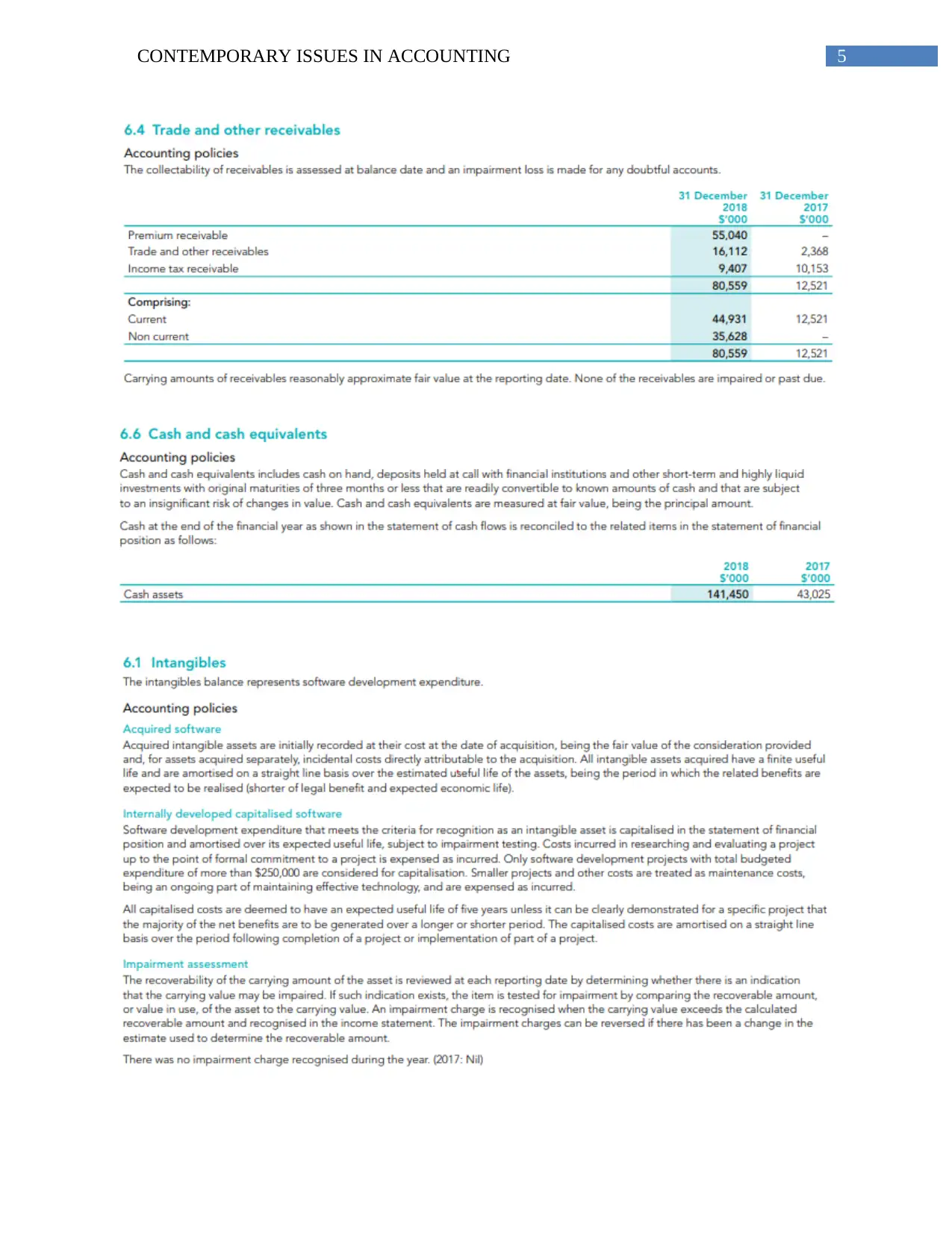

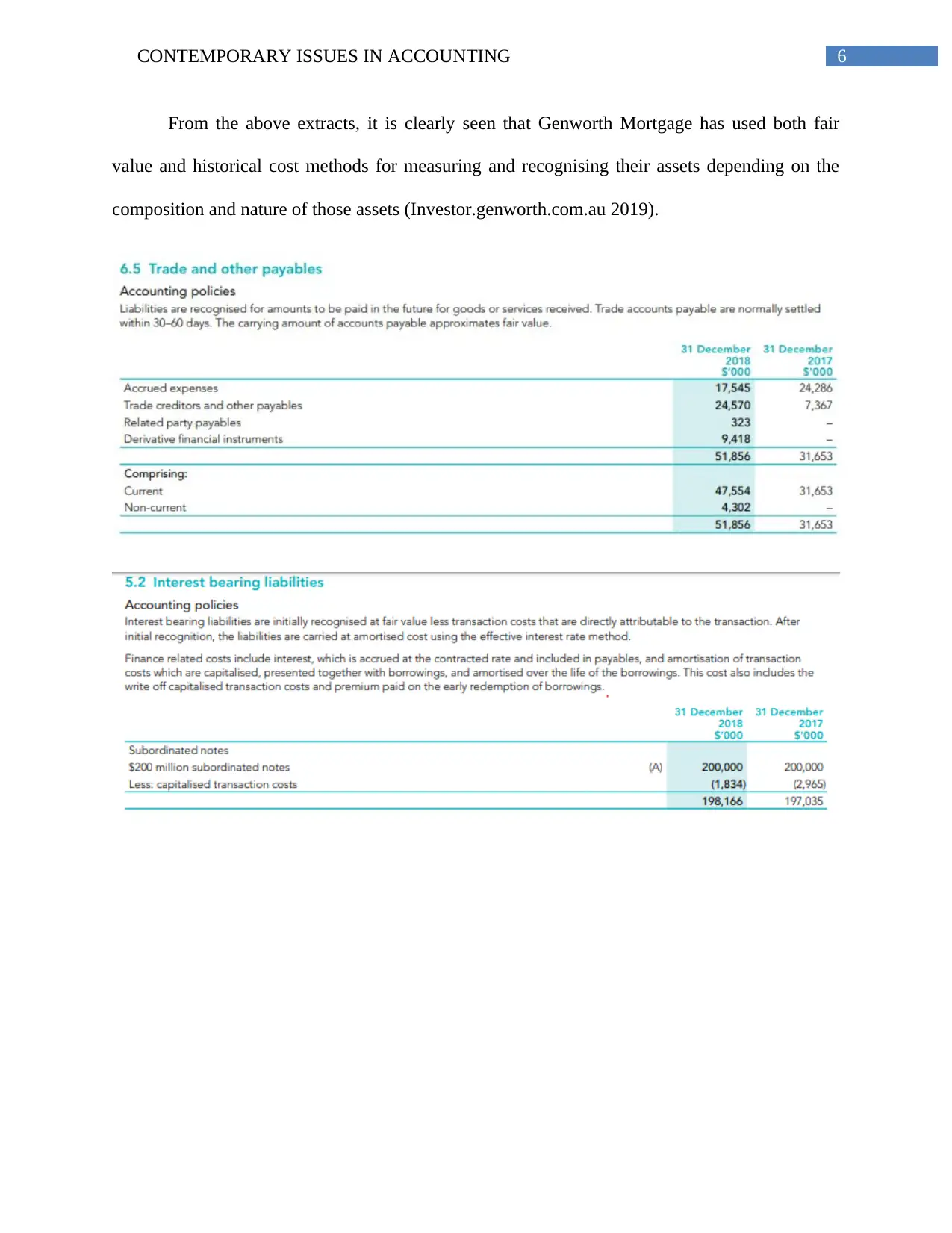

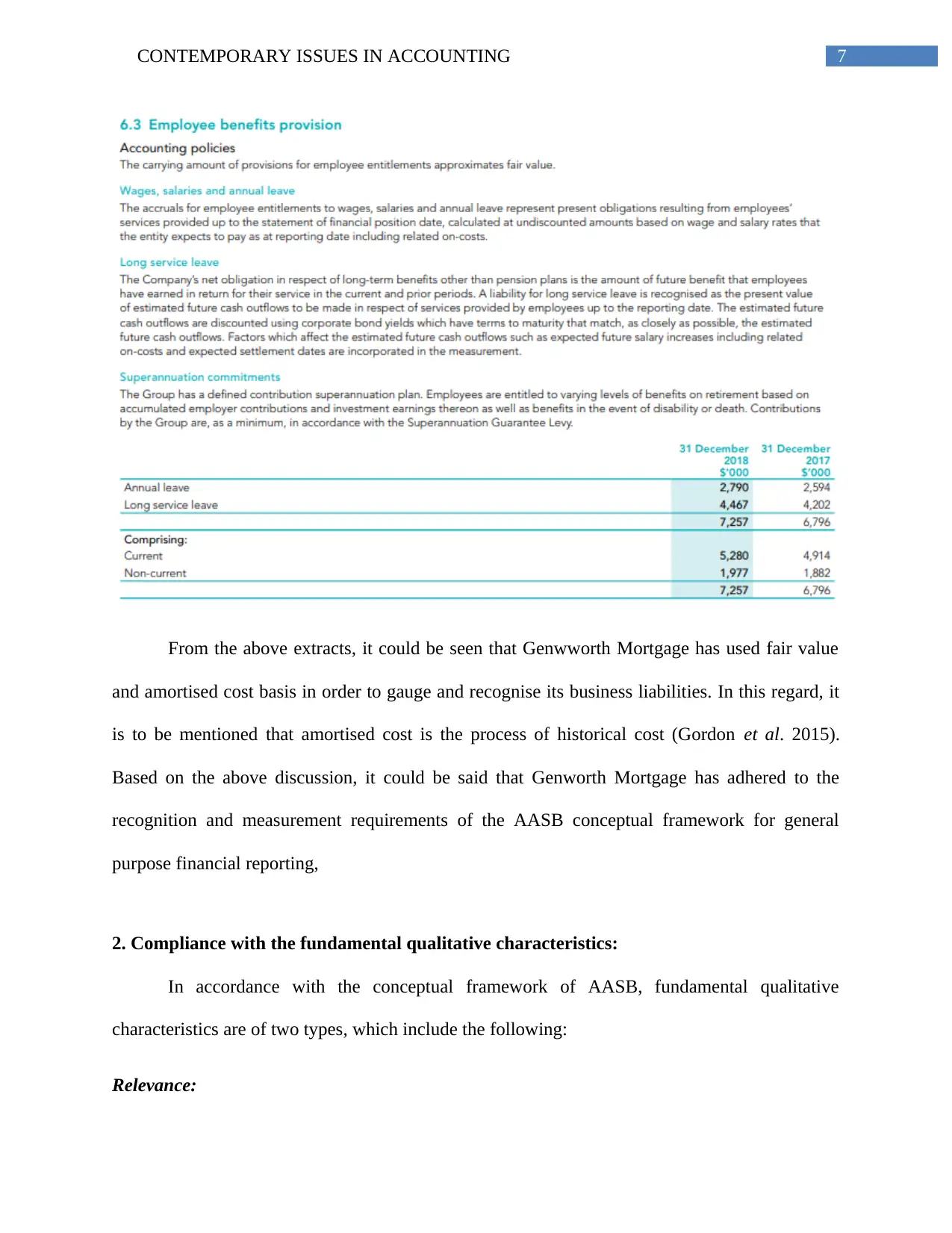

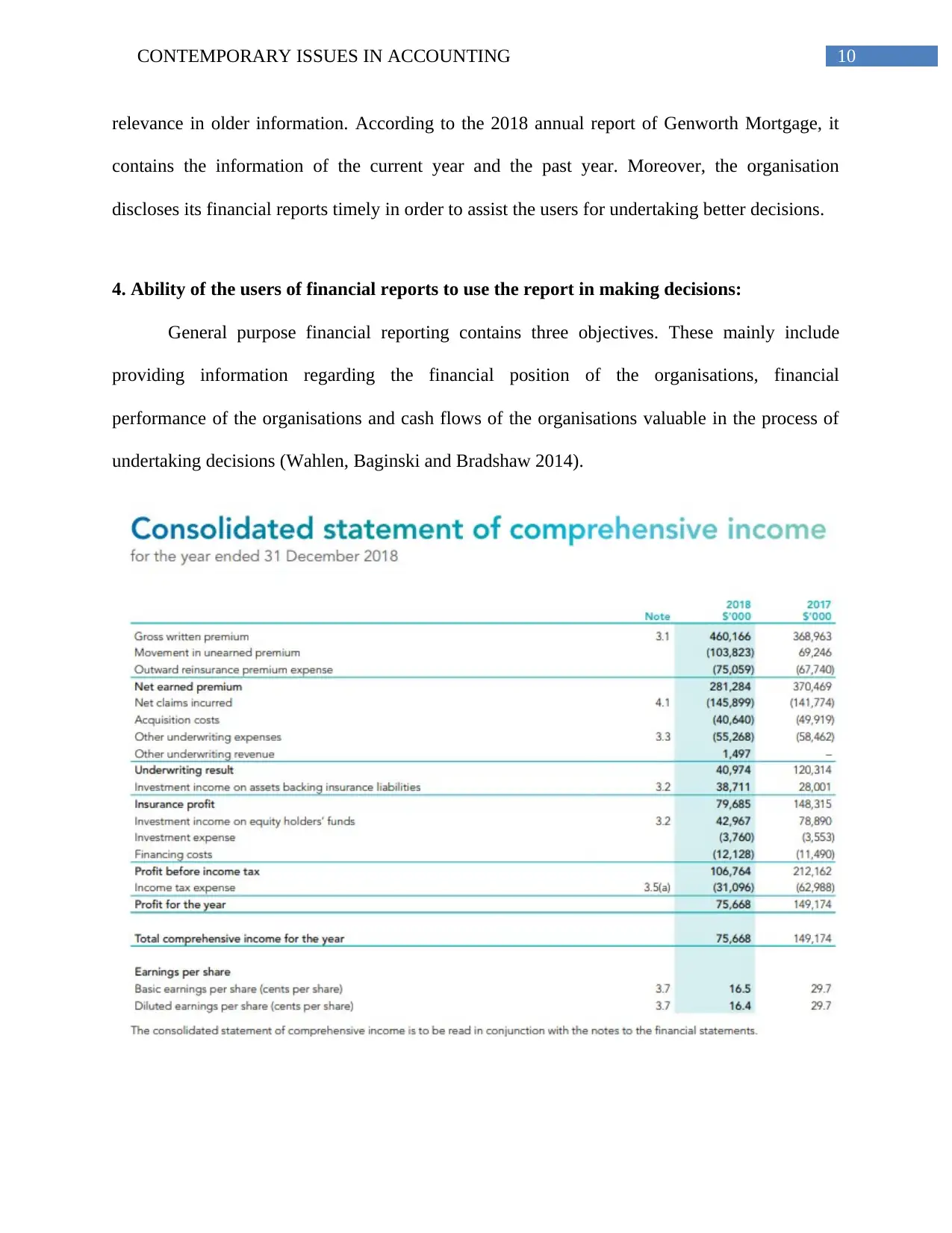

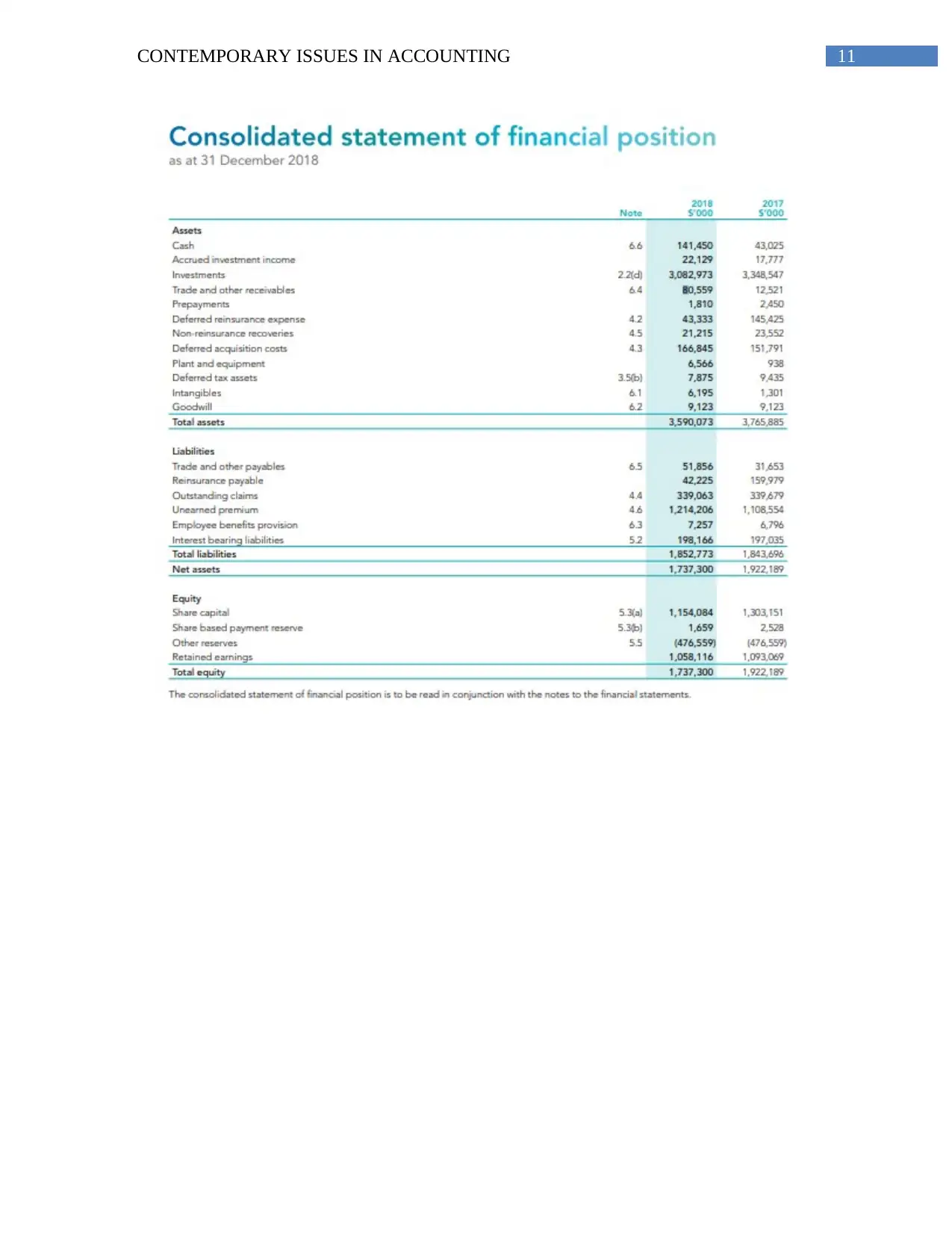

This report provides a comprehensive analysis of Genworth Mortgage's general-purpose financial reporting practices. It examines the company's adherence to the measurement requirements of the conceptual framework, fundamental and enhancing qualitative characteristics, and the ability of financial report users to make informed decisions. The analysis utilizes the 2018 annual report and relevant accounting literature to assess compliance with IFRS, AASB, IASB, and the Corporations Act 2001. The report investigates how Genworth Mortgage applies fair value and historical cost measurements, discloses relevant information, and presents financial statements in a clear and understandable manner. It also considers the required accounting knowledge for analyzing the company's reports and concludes on whether Genworth Mortgage meets the requirements for general-purpose financial reporting, providing valuable insights into the company's financial reporting quality and its usefulness to stakeholders. The report highlights how the company uses its financial statements to provide information on financial performance, financial position and cash flows to assist users in making decisions.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.