Real World Analytics Project: Analyzing GSK Share Prices with GBM

VerifiedAdded on 2023/05/31

|7

|1036

|218

Project

AI Summary

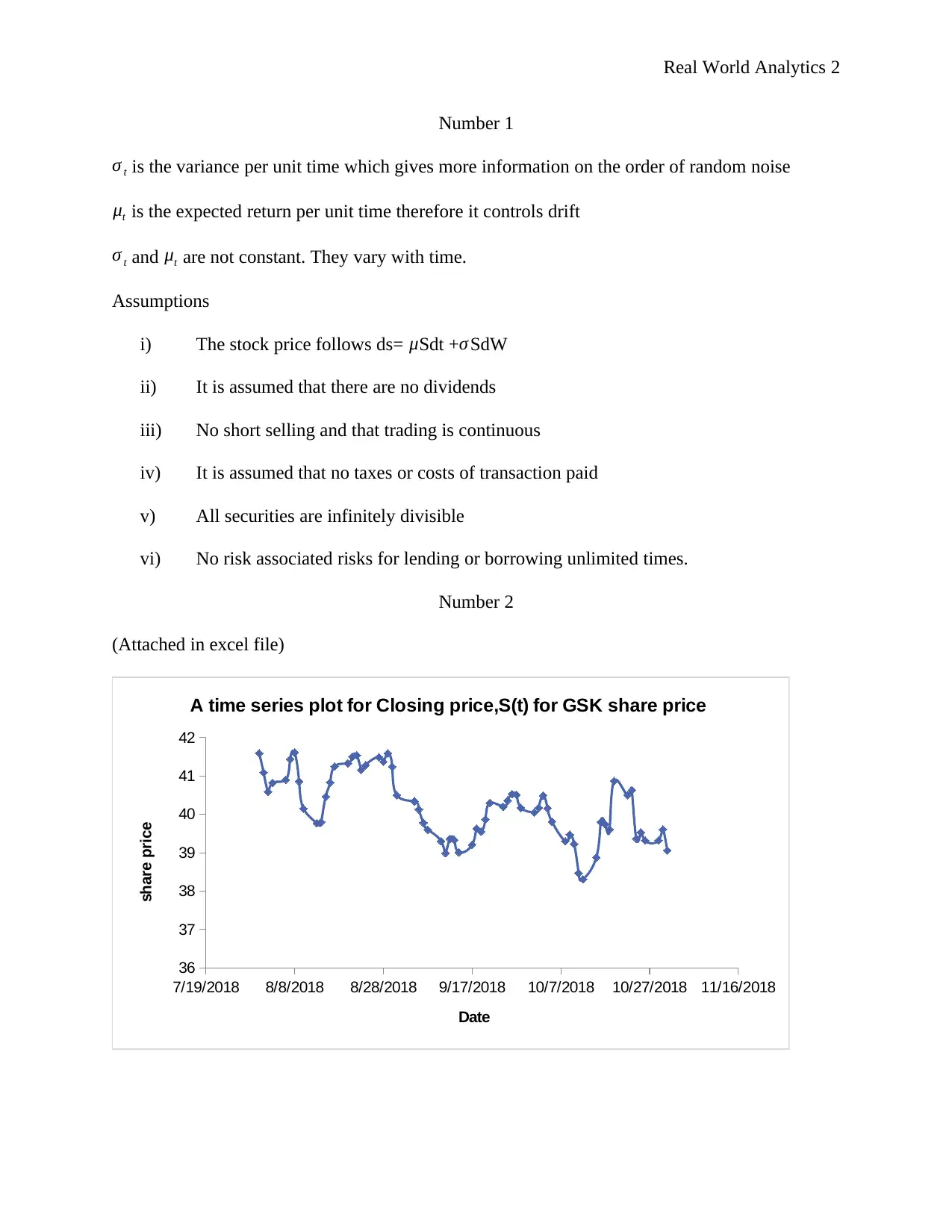

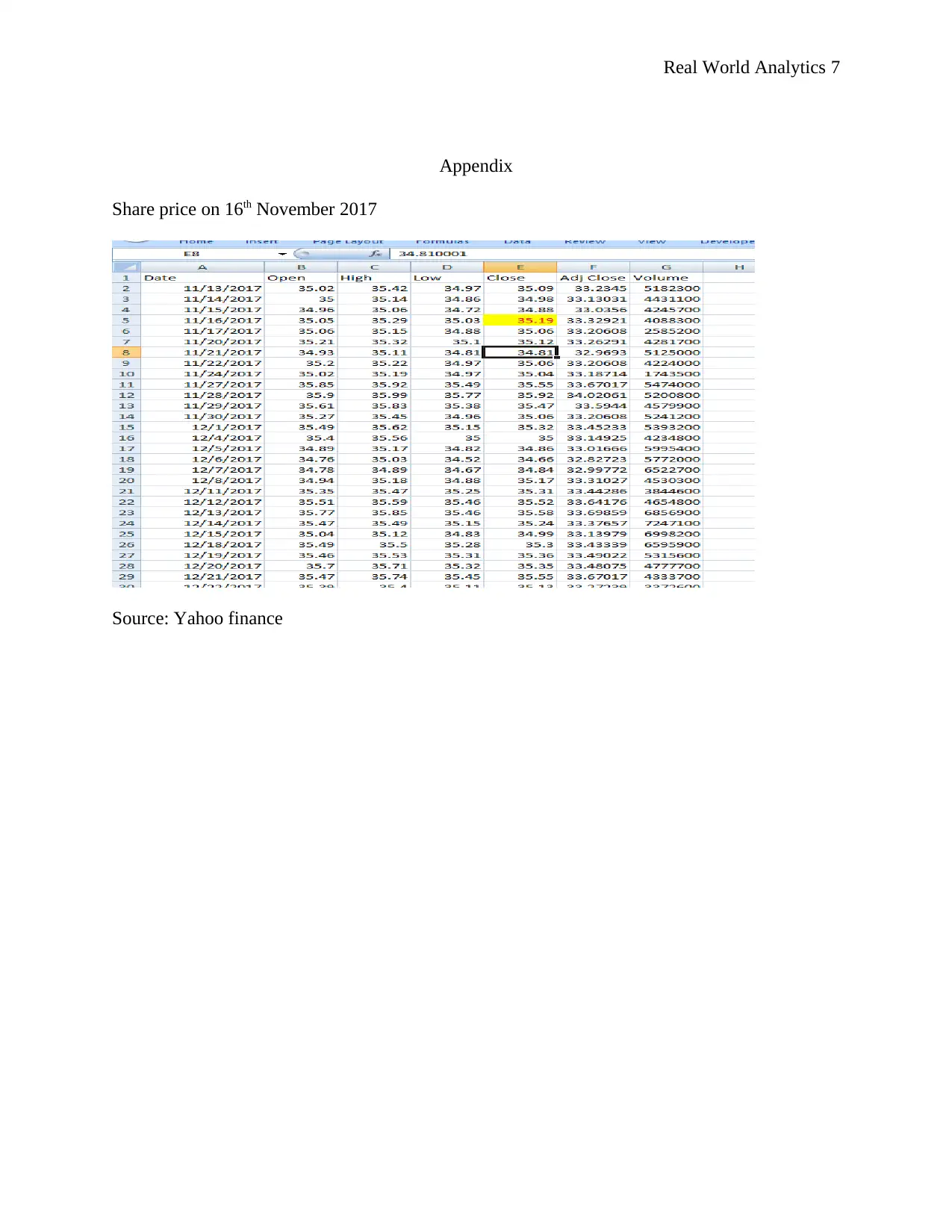

This project analyzes the share price of GlaxoSmithKline (GSK) using real-world analytics and the Geometric Brownian Motion (GBM) model. The student begins by outlining the assumptions of GBM and then presents a time series plot of GSK's closing share prices. The core of the project involves applying the GBM formula to model and predict share price movements. The student calculates the drift and annual volatility of the share prices, compares them to external data, and discusses potential discrepancies. The analysis includes a simulation to predict a specific share price, comparing the result to published data, and assessing the accuracy of the GBM model. The project concludes with a discussion of the limitations of GBM, such as the assumption of continuous stock prices and normal distribution of returns. The student used data from August 2018 to October 2018 and found a drift of -0.0001 and an annual volatility of 0.2. The project demonstrates the practical application of GBM in financial modeling and highlights the importance of understanding its limitations.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.