SIT718: Real World Analytics Assessment Task 2 - Problem Solving

VerifiedAdded on 2023/01/13

|12

|1047

|35

Project

AI Summary

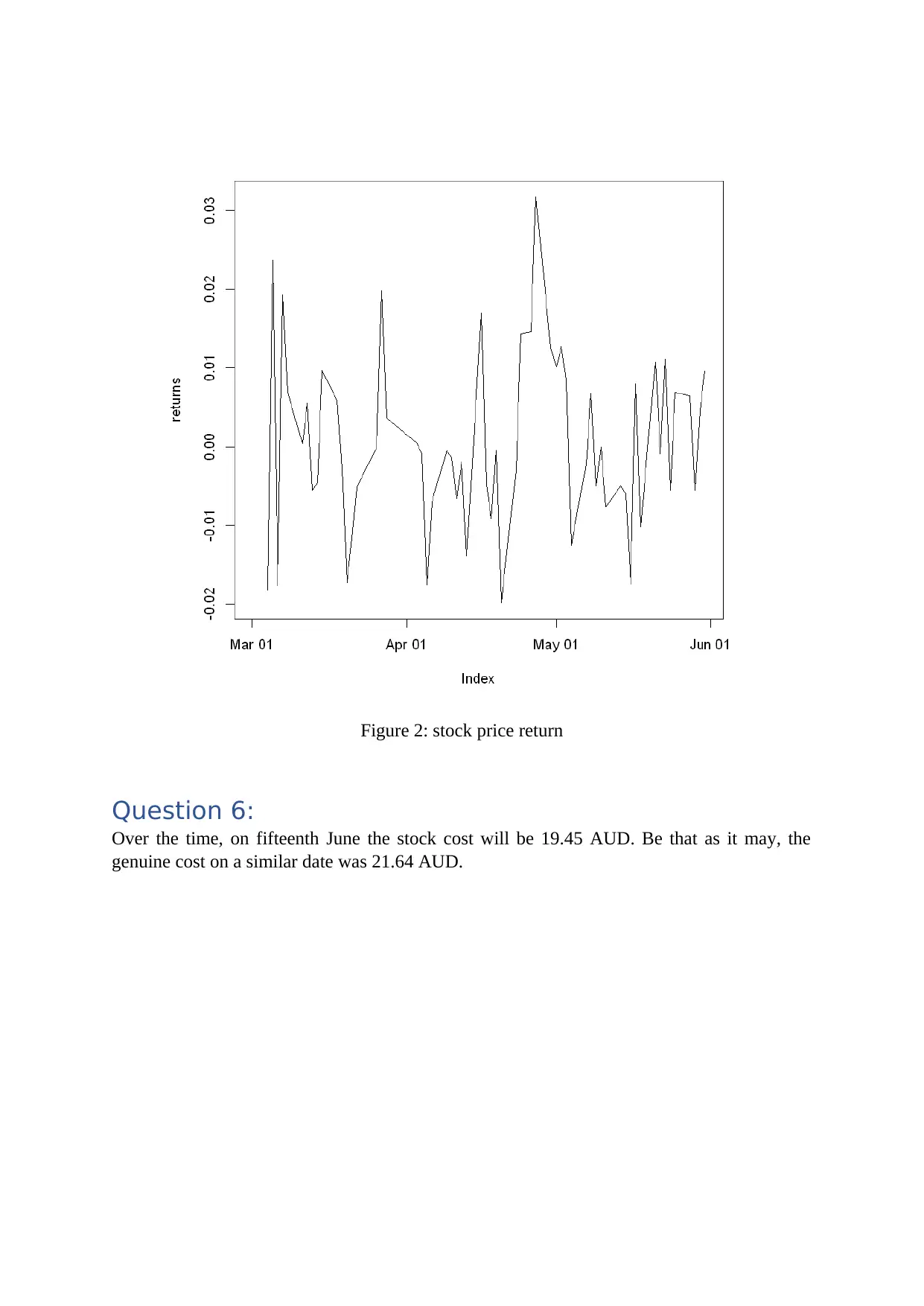

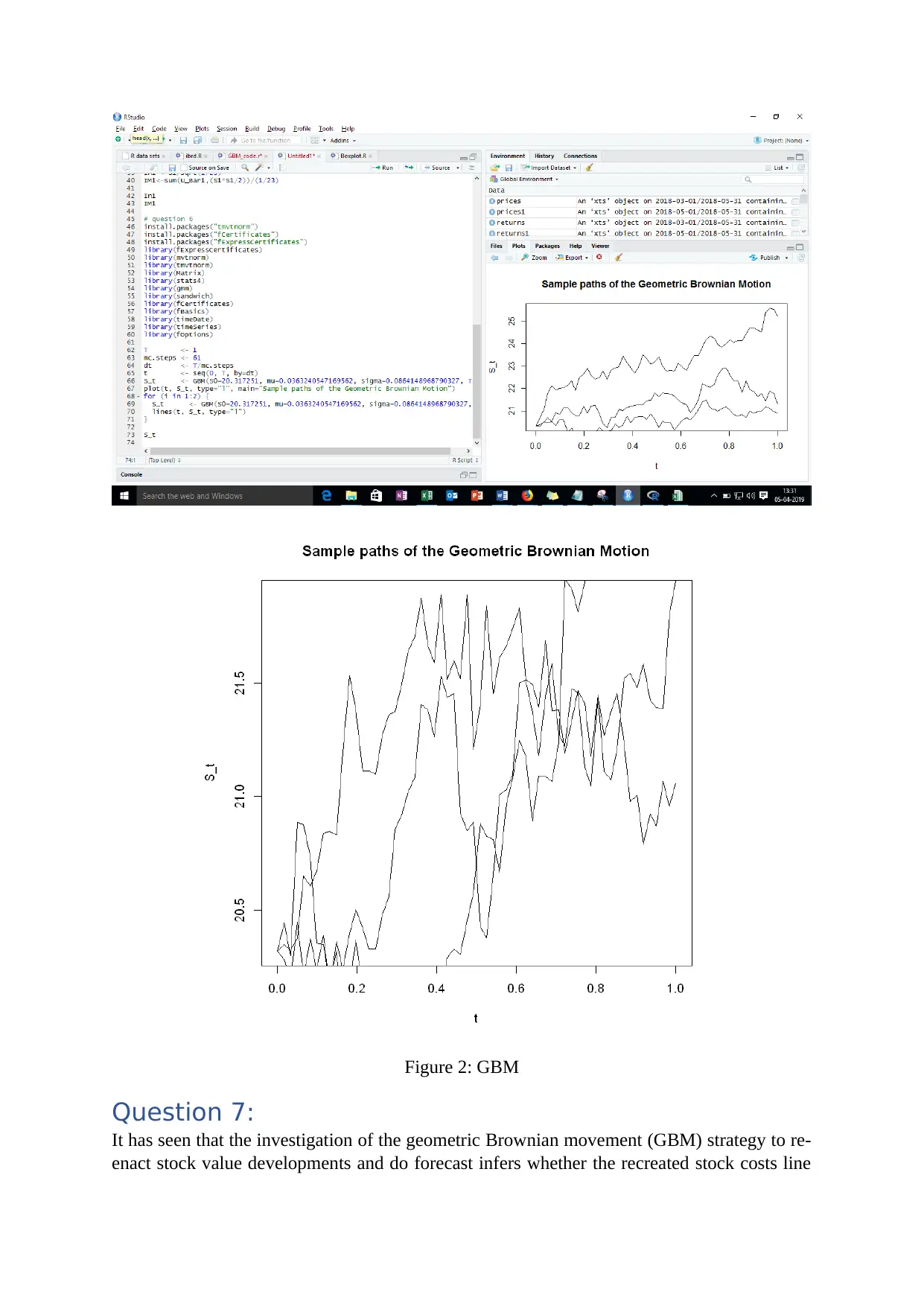

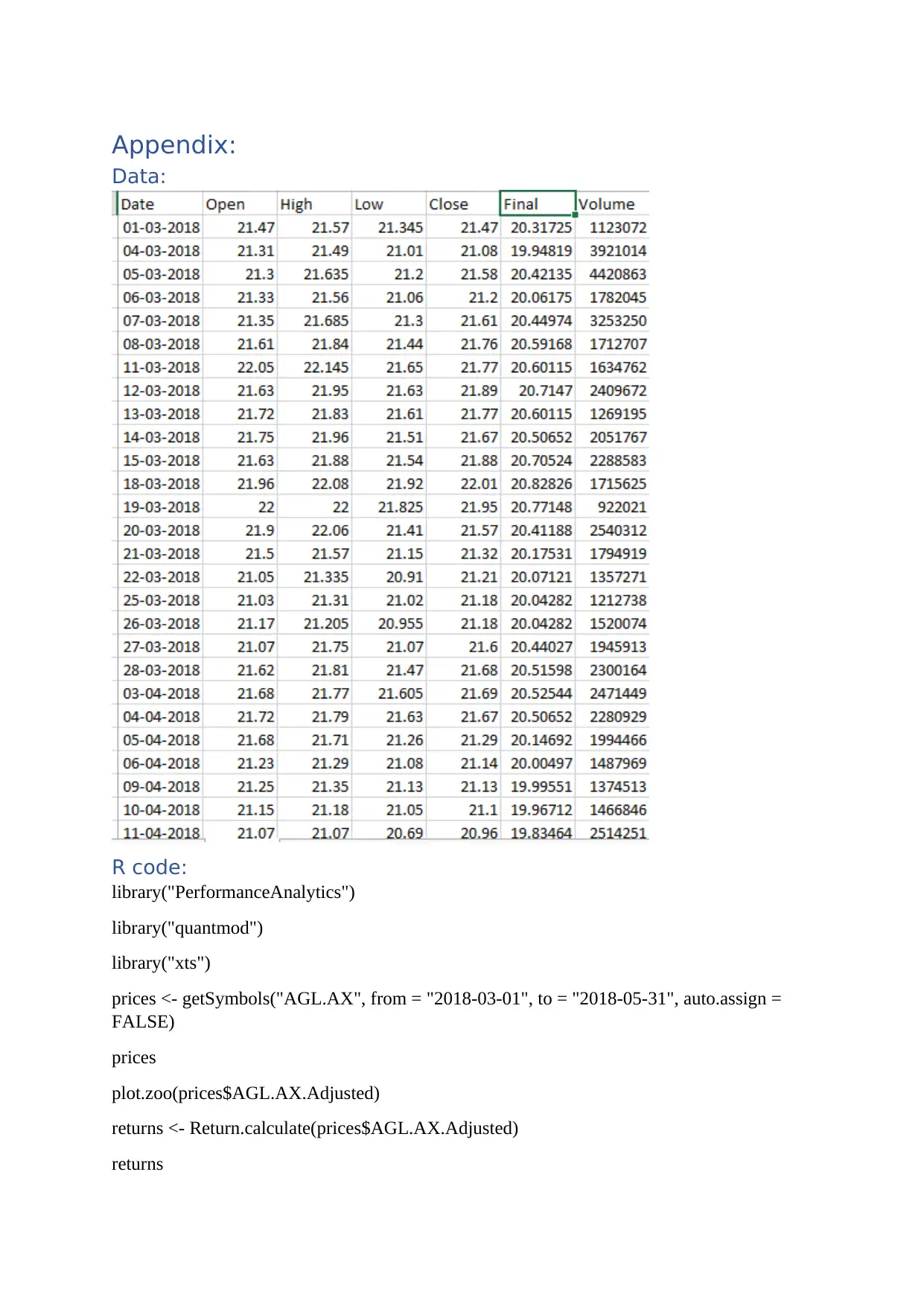

This assignment analyzes the behavior and performance of AGL.AX, an Australian publicly listed company, using historical stock data from March to May 2018. The analysis focuses on applying the Geometric Brownian Motion (GBM) model to simulate stock price movements and forecast future values. The student calculates drift and volatility, examines the distribution of stock returns, and compares predicted stock prices with actual values. The project includes R code for data manipulation, visualization, and GBM implementation. The student finds that the GBM model's parameters are not consistent over different time periods, and the predicted stock price on June 15th differs from the actual price. The assignment highlights the challenges and limitations of using GBM for stock price prediction. The solution also contains references and an appendix with data and R code.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.