Management Accounting Case Study: Gibson Fabricators Corporation

VerifiedAdded on 2022/09/24

|7

|376

|16

Case Study

AI Summary

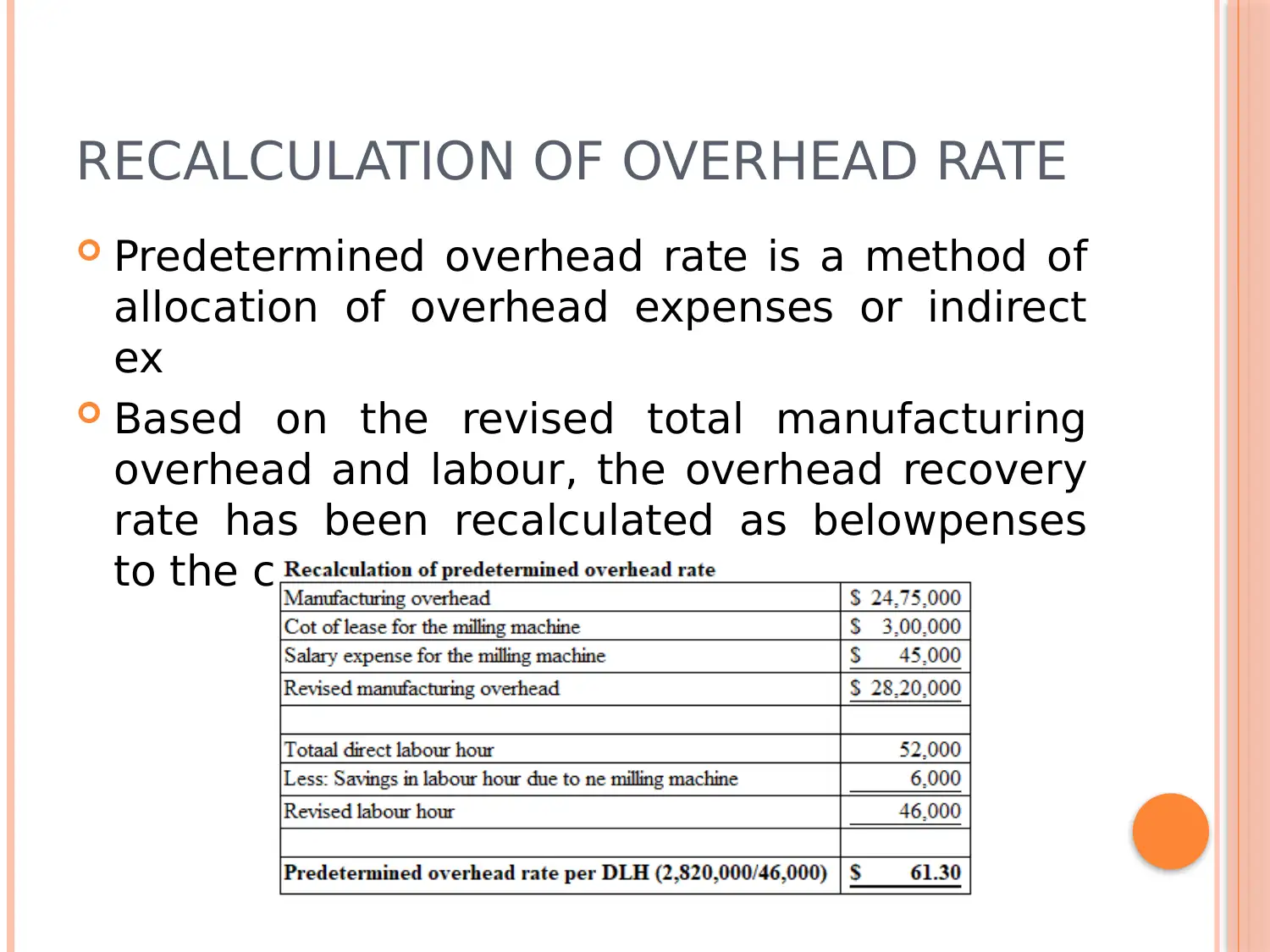

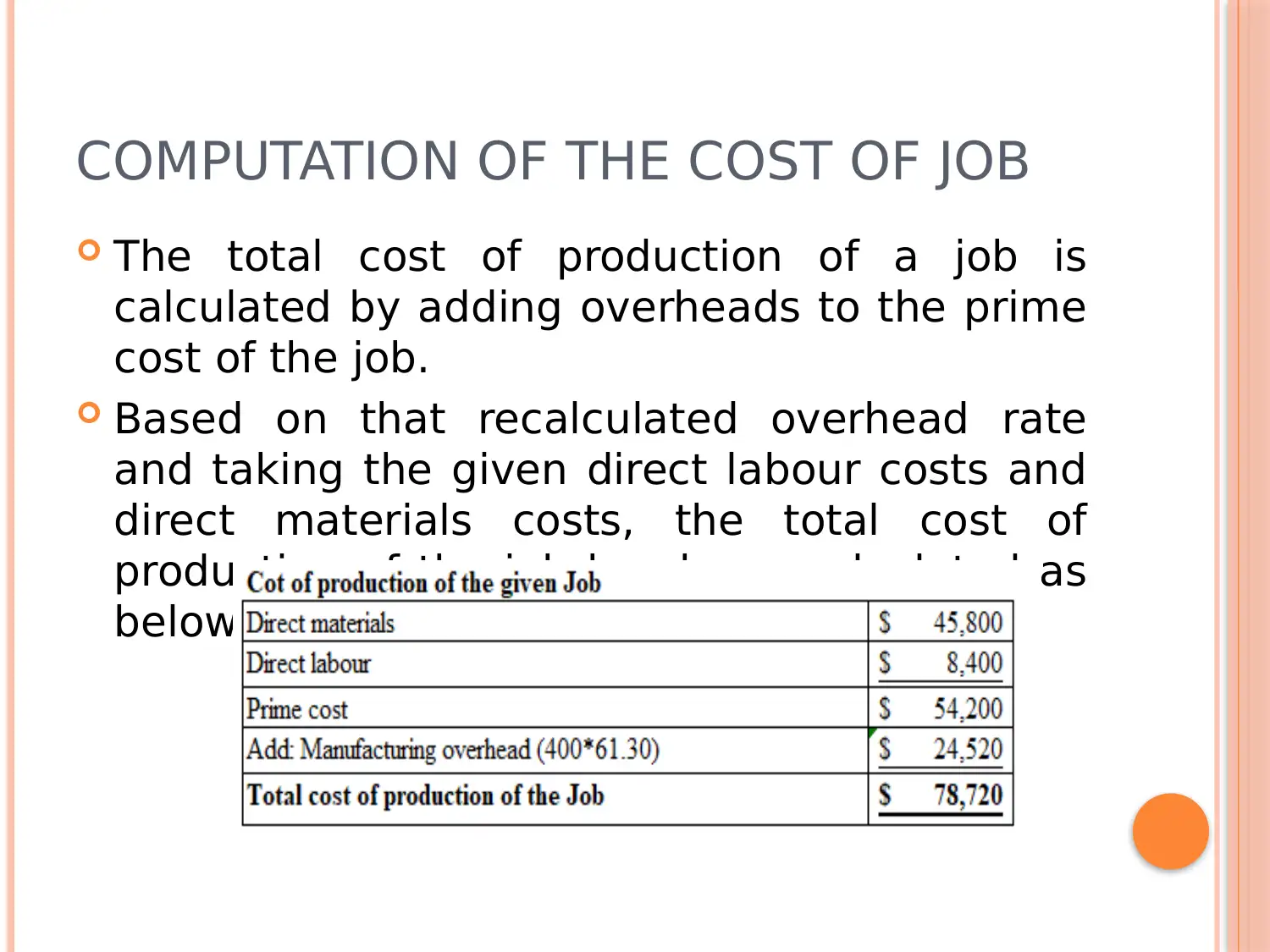

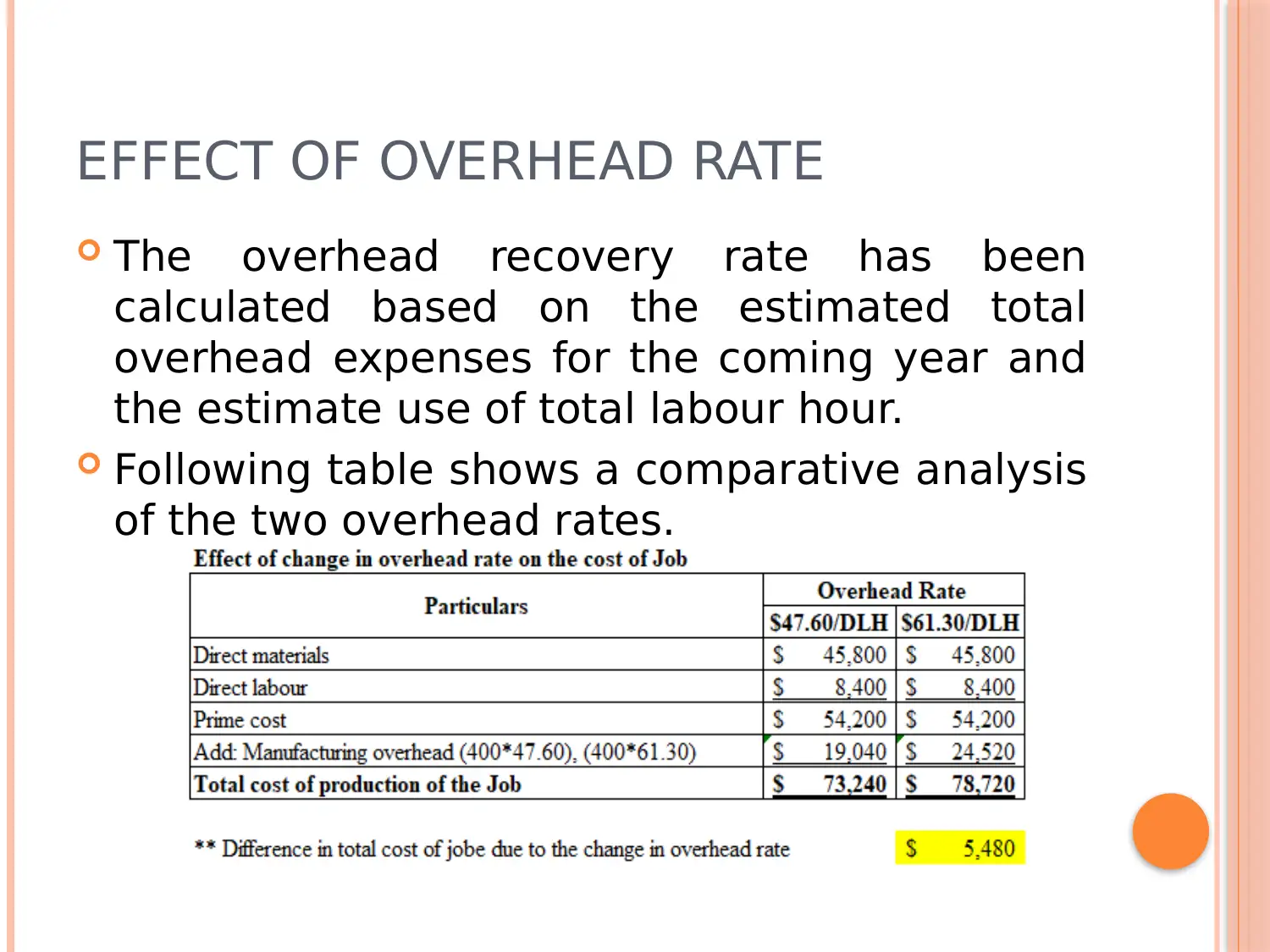

This case study analyzes the accounting practices of Gibson Fabricators Corporation, focusing on the calculation and application of predetermined overhead rates. The solution addresses the computation of overhead recovery rates, the impact of these rates on job costing, and the importance of overhead costs in overall cost management. The analysis includes a comparison of different overhead rates and their effects. Furthermore, the case study evaluates the decision-making process regarding the installation of a new machine, considering the potential cost savings from reduced direct labor hours and the associated expenses. The solution emphasizes the significance of careful management of indirect costs to minimize overall costs. The case study solution submitted on Desklib offers insights into accounting principles and practical application of overhead costs.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.