Comprehensive Examination of GICs, Mortgages, Debt, and Ratios

VerifiedAdded on 2022/11/13

|13

|4276

|98

Homework Assignment

AI Summary

This assignment delves into the analysis of Guaranteed Investment Certificates (GICs) and mortgages, focusing on interest rates, loan-to-value ratios, and the rationale behind the spread between GIC and mortgage rates. It explores different mortgage lenders in Canada, including TD Canada Trust and FNB Corporation, and their lending practices. The assignment also examines debt service ratios, including gross debt service (GDS) and total debt service (TDS), outlining the components and industry standards. Furthermore, it addresses amortization schedules and the reasons for discrepancies in outstanding balances, along with the circumstances under which discount rates are offered. The analysis covers various aspects of financial instruments and lending practices, offering a comprehensive overview of the Canadian financial landscape.

Answer 1

Part A

Guaranteed Investment Certificate are Canadian investment which provides a rate of return which is

fixed in nature on the amount of capital invested for a fixed period of time. The same is equivalent to

Certificate of Deposit or Term deposit. These are issued by Canadian Financial institutions such as

bank or credit union. These certificate represents the loan issued by the investor to the bank and can

be of varied period ranging from 6 months to 5 years. Different banks have different rate of interest

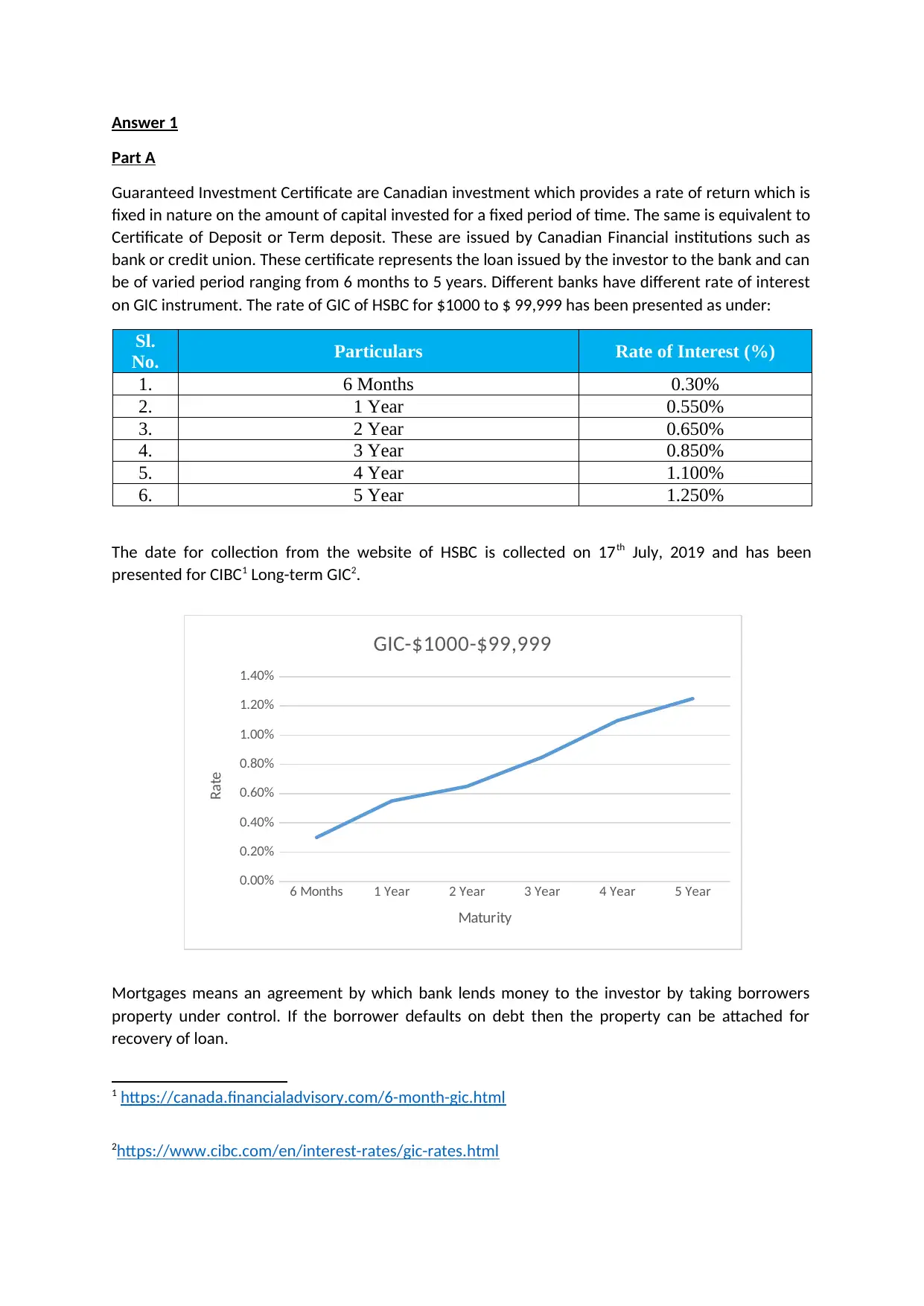

on GIC instrument. The rate of GIC of HSBC for $1000 to $ 99,999 has been presented as under:

Sl.

No. Particulars Rate of Interest (%)

1. 6 Months 0.30%

2. 1 Year 0.550%

3. 2 Year 0.650%

4. 3 Year 0.850%

5. 4 Year 1.100%

6. 5 Year 1.250%

The date for collection from the website of HSBC is collected on 17th July, 2019 and has been

presented for CIBC1 Long-term GIC2.

Mortgages means an agreement by which bank lends money to the investor by taking borrowers

property under control. If the borrower defaults on debt then the property can be attached for

recovery of loan.

1 https://canada.financialadvisory.com/6-month-gic.html

2https://www.cibc.com/en/interest-rates/gic-rates.html

6 Months 1 Year 2 Year 3 Year 4 Year 5 Year

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

GIC-$1000-$99,999

Maturity

Rate

Part A

Guaranteed Investment Certificate are Canadian investment which provides a rate of return which is

fixed in nature on the amount of capital invested for a fixed period of time. The same is equivalent to

Certificate of Deposit or Term deposit. These are issued by Canadian Financial institutions such as

bank or credit union. These certificate represents the loan issued by the investor to the bank and can

be of varied period ranging from 6 months to 5 years. Different banks have different rate of interest

on GIC instrument. The rate of GIC of HSBC for $1000 to $ 99,999 has been presented as under:

Sl.

No. Particulars Rate of Interest (%)

1. 6 Months 0.30%

2. 1 Year 0.550%

3. 2 Year 0.650%

4. 3 Year 0.850%

5. 4 Year 1.100%

6. 5 Year 1.250%

The date for collection from the website of HSBC is collected on 17th July, 2019 and has been

presented for CIBC1 Long-term GIC2.

Mortgages means an agreement by which bank lends money to the investor by taking borrowers

property under control. If the borrower defaults on debt then the property can be attached for

recovery of loan.

1 https://canada.financialadvisory.com/6-month-gic.html

2https://www.cibc.com/en/interest-rates/gic-rates.html

6 Months 1 Year 2 Year 3 Year 4 Year 5 Year

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

GIC-$1000-$99,999

Maturity

Rate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

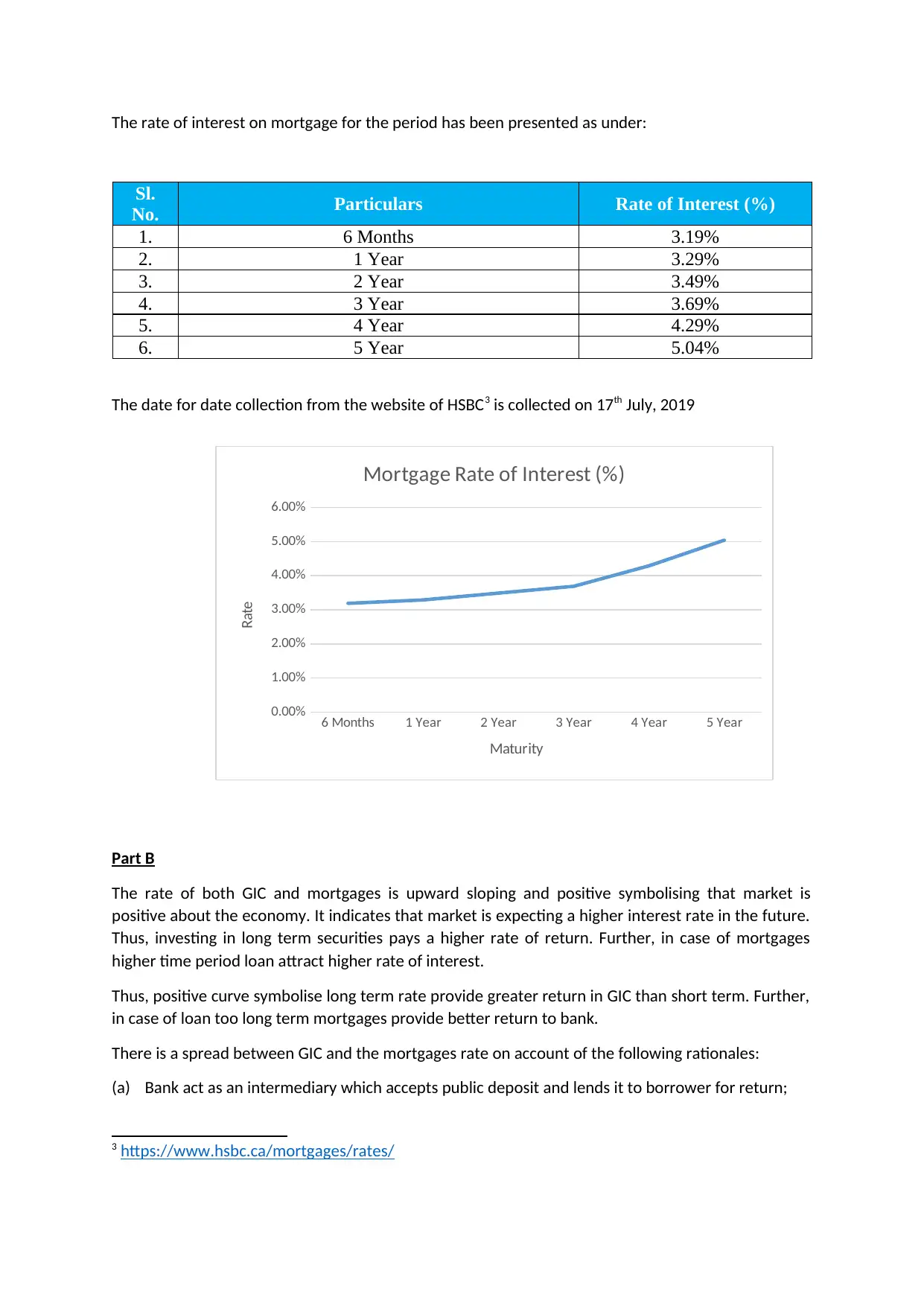

The rate of interest on mortgage for the period has been presented as under:

Sl.

No. Particulars Rate of Interest (%)

1. 6 Months 3.19%

2. 1 Year 3.29%

3. 2 Year 3.49%

4. 3 Year 3.69%

5. 4 Year 4.29%

6. 5 Year 5.04%

The date for date collection from the website of HSBC3 is collected on 17th July, 2019

Part B

The rate of both GIC and mortgages is upward sloping and positive symbolising that market is

positive about the economy. It indicates that market is expecting a higher interest rate in the future.

Thus, investing in long term securities pays a higher rate of return. Further, in case of mortgages

higher time period loan attract higher rate of interest.

Thus, positive curve symbolise long term rate provide greater return in GIC than short term. Further,

in case of loan too long term mortgages provide better return to bank.

There is a spread between GIC and the mortgages rate on account of the following rationales:

(a) Bank act as an intermediary which accepts public deposit and lends it to borrower for return;

3 https://www.hsbc.ca/mortgages/rates/

6 Months 1 Year 2 Year 3 Year 4 Year 5 Year

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Mortgage Rate of Interest (%)

Maturity

Rate

Sl.

No. Particulars Rate of Interest (%)

1. 6 Months 3.19%

2. 1 Year 3.29%

3. 2 Year 3.49%

4. 3 Year 3.69%

5. 4 Year 4.29%

6. 5 Year 5.04%

The date for date collection from the website of HSBC3 is collected on 17th July, 2019

Part B

The rate of both GIC and mortgages is upward sloping and positive symbolising that market is

positive about the economy. It indicates that market is expecting a higher interest rate in the future.

Thus, investing in long term securities pays a higher rate of return. Further, in case of mortgages

higher time period loan attract higher rate of interest.

Thus, positive curve symbolise long term rate provide greater return in GIC than short term. Further,

in case of loan too long term mortgages provide better return to bank.

There is a spread between GIC and the mortgages rate on account of the following rationales:

(a) Bank act as an intermediary which accepts public deposit and lends it to borrower for return;

3 https://www.hsbc.ca/mortgages/rates/

6 Months 1 Year 2 Year 3 Year 4 Year 5 Year

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Mortgage Rate of Interest (%)

Maturity

Rate

(b) Bank has administrative cost which is met from lending and borrowing which accounts for more

than 70% of the revenue of the business;

(c) The opportunity cost of capital also results in gap as bank has to provide interest rate to the

lender and has to meet its expenses too.

(d) Liquidity is higher in case of GIC than in case of Mortgages. Hence, GIC and Mortgages gap is

present;

(e) Risk is higher in mortgage than in GIC as bank are cash rich solid institutions;

(f) Matching of asset and liability requires bank to lend at a higher rate in order to match the asset

and liability side of balance sheet.

Answer 2

There are many mortgage lender in Canada. Some of the prominent mortgage lenders are F.N.B

Corporation, Scotia Bank, TD Canada trust etc.

Part A

I have done a google research to find the top companies in Canada providing the service and then

applied filter to contact the bank. The bank are quick in responding and provide very quick solution

to the customer once you contact them.

Under conventional model mortgage, TD Canada trust provides 80% LTV with 20% down payment

and rest funded by Bank. The said mortgage is generally for a single family dwelling as duly

highlighted in their website.

The LTV4 ratio or Loan to Value Ratio symbolise the maximum amount of loan that shall be disbursed

by the bank considering the value of the property. In the case of TDD Trust i.e. 80% of the value of

property.

Under conventional model mortgage, FNB Corporation provides 85% LTV with 15% down payment

and rest funded by Bank. The said mortgage is generally for a single family dwelling as duly

highlighted in their website5.

Yes, there are difference as the LTV ratio changes on the nature of property. The highest LTV is

provided for the residential property. Further, the LTV also varies on the basis of the credit rating of

the borrower, location of the property etc.

Part B

Yes, many times in Canada the lenders do carry an appraisal to ascertain the true value of the

property when they doubt that the value of the paper does not represent the true value of the

property. Further, the appraisal is carries out to safeguard the amount of money lent and to create a

buffer to prevent erosion of loan on account of drastic fall in the value of property. Further, the

lending value is generally near 80% of the value of property. In case the same reaches near about

90% of the value of the property, it may cause issue for the bank. Also, the crisis in 2008 emphasizes

on appraisal.

4 https://www.td.com/ca/en/personal-banking/products/mortgages/first-time-home-buyer/down-

payments/

5https://www.fnb-online.com/borrow/personal-loans/home-equity-loan

than 70% of the revenue of the business;

(c) The opportunity cost of capital also results in gap as bank has to provide interest rate to the

lender and has to meet its expenses too.

(d) Liquidity is higher in case of GIC than in case of Mortgages. Hence, GIC and Mortgages gap is

present;

(e) Risk is higher in mortgage than in GIC as bank are cash rich solid institutions;

(f) Matching of asset and liability requires bank to lend at a higher rate in order to match the asset

and liability side of balance sheet.

Answer 2

There are many mortgage lender in Canada. Some of the prominent mortgage lenders are F.N.B

Corporation, Scotia Bank, TD Canada trust etc.

Part A

I have done a google research to find the top companies in Canada providing the service and then

applied filter to contact the bank. The bank are quick in responding and provide very quick solution

to the customer once you contact them.

Under conventional model mortgage, TD Canada trust provides 80% LTV with 20% down payment

and rest funded by Bank. The said mortgage is generally for a single family dwelling as duly

highlighted in their website.

The LTV4 ratio or Loan to Value Ratio symbolise the maximum amount of loan that shall be disbursed

by the bank considering the value of the property. In the case of TDD Trust i.e. 80% of the value of

property.

Under conventional model mortgage, FNB Corporation provides 85% LTV with 15% down payment

and rest funded by Bank. The said mortgage is generally for a single family dwelling as duly

highlighted in their website5.

Yes, there are difference as the LTV ratio changes on the nature of property. The highest LTV is

provided for the residential property. Further, the LTV also varies on the basis of the credit rating of

the borrower, location of the property etc.

Part B

Yes, many times in Canada the lenders do carry an appraisal to ascertain the true value of the

property when they doubt that the value of the paper does not represent the true value of the

property. Further, the appraisal is carries out to safeguard the amount of money lent and to create a

buffer to prevent erosion of loan on account of drastic fall in the value of property. Further, the

lending value is generally near 80% of the value of property. In case the same reaches near about

90% of the value of the property, it may cause issue for the bank. Also, the crisis in 2008 emphasizes

on appraisal.

4 https://www.td.com/ca/en/personal-banking/products/mortgages/first-time-home-buyer/down-

payments/

5https://www.fnb-online.com/borrow/personal-loans/home-equity-loan

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part C

Currently, the maximum the gross debt service ratio applied is 35% of the gross family income. This

ratio defines the percentage of the gross income of the borrower which are generally used for

covering the payment of housing cost like utility bill, mortgages, taxes etc6. The present threshold is

set at 35%7.

Yes, the rate varies depending on the credit rating of the borrower and the financial strength of the

books of the borrower. The higher the strength and good the books are the higher the rate of gross

debt service ratio shall be.

Part D

The following elements are included in the Gross debt service ratio computation:

(a) Monthly Housing Costs encompassing principal, interest and heat;

(b) 50% of Condo fees;

(c) Gross monthly income.

Part E

The total debt service ratio represents the percentage of your income that will be required to cover

all the debts. The formula for computation of Total debt service is similar to the computation of the

gross debt service. Further, in the total debt service ratio all your debts taken into consideration for

analysis. The debt encompass car loan, credit car loan, alimony etc. The industry standard for the

ratio is approximately 42%.

For computing the ratio add all debt related cost and divide the same with monthly income.

The other steps that lenders take to understand the credit worthiness of the borrower encompass

the following:

(a) Total Expense Ratio;

(b) Living Standards and habits;

(c) Savings;

(d) Financial soundness;

Part F

Discount Rates are offered generally in the following circumstances:

(a) Customer Loyalty;

(b) Strong Financials;

(c) Government aided incentive programs;

(d) Attract customers and increase business;

(e) Negotiation.

6 https://www.superbrokers.ca/library/glossary/terms/gross_debt_service.php

7https://www.whichmortgage.ca/article/what-are-tds-gds-and-ltv-ratios-174913.aspx

Currently, the maximum the gross debt service ratio applied is 35% of the gross family income. This

ratio defines the percentage of the gross income of the borrower which are generally used for

covering the payment of housing cost like utility bill, mortgages, taxes etc6. The present threshold is

set at 35%7.

Yes, the rate varies depending on the credit rating of the borrower and the financial strength of the

books of the borrower. The higher the strength and good the books are the higher the rate of gross

debt service ratio shall be.

Part D

The following elements are included in the Gross debt service ratio computation:

(a) Monthly Housing Costs encompassing principal, interest and heat;

(b) 50% of Condo fees;

(c) Gross monthly income.

Part E

The total debt service ratio represents the percentage of your income that will be required to cover

all the debts. The formula for computation of Total debt service is similar to the computation of the

gross debt service. Further, in the total debt service ratio all your debts taken into consideration for

analysis. The debt encompass car loan, credit car loan, alimony etc. The industry standard for the

ratio is approximately 42%.

For computing the ratio add all debt related cost and divide the same with monthly income.

The other steps that lenders take to understand the credit worthiness of the borrower encompass

the following:

(a) Total Expense Ratio;

(b) Living Standards and habits;

(c) Savings;

(d) Financial soundness;

Part F

Discount Rates are offered generally in the following circumstances:

(a) Customer Loyalty;

(b) Strong Financials;

(c) Government aided incentive programs;

(d) Attract customers and increase business;

(e) Negotiation.

6 https://www.superbrokers.ca/library/glossary/terms/gross_debt_service.php

7https://www.whichmortgage.ca/article/what-are-tds-gds-and-ltv-ratios-174913.aspx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

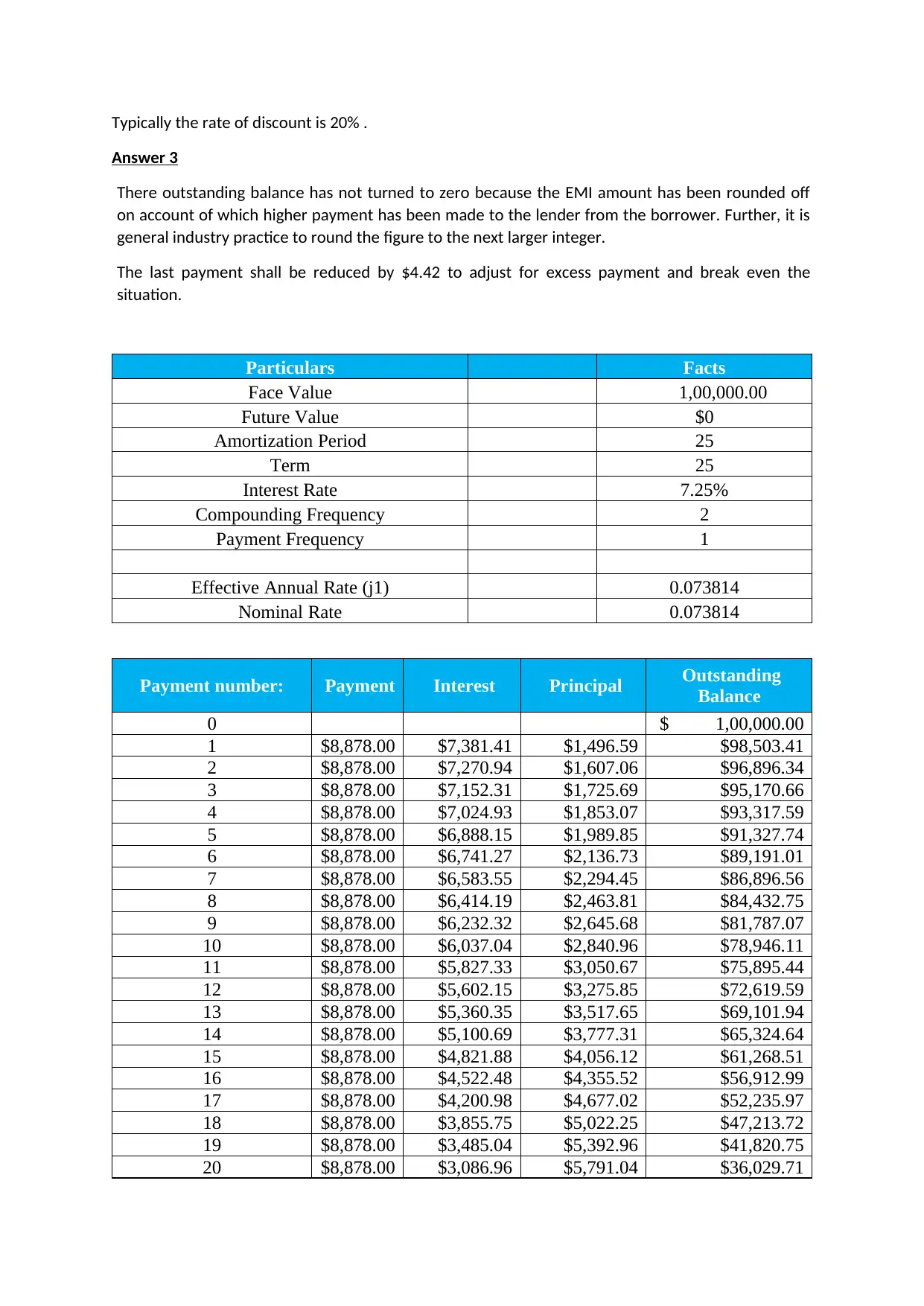

Typically the rate of discount is 20% .

Answer 3

There outstanding balance has not turned to zero because the EMI amount has been rounded off

on account of which higher payment has been made to the lender from the borrower. Further, it is

general industry practice to round the figure to the next larger integer.

The last payment shall be reduced by $4.42 to adjust for excess payment and break even the

situation.

Particulars Facts

Face Value 1,00,000.00

Future Value $0

Amortization Period 25

Term 25

Interest Rate 7.25%

Compounding Frequency 2

Payment Frequency 1

Effective Annual Rate (j1) 0.073814

Nominal Rate 0.073814

Payment number: Payment Interest Principal Outstanding

Balance

0 $ 1,00,000.00

1 $8,878.00 $7,381.41 $1,496.59 $98,503.41

2 $8,878.00 $7,270.94 $1,607.06 $96,896.34

3 $8,878.00 $7,152.31 $1,725.69 $95,170.66

4 $8,878.00 $7,024.93 $1,853.07 $93,317.59

5 $8,878.00 $6,888.15 $1,989.85 $91,327.74

6 $8,878.00 $6,741.27 $2,136.73 $89,191.01

7 $8,878.00 $6,583.55 $2,294.45 $86,896.56

8 $8,878.00 $6,414.19 $2,463.81 $84,432.75

9 $8,878.00 $6,232.32 $2,645.68 $81,787.07

10 $8,878.00 $6,037.04 $2,840.96 $78,946.11

11 $8,878.00 $5,827.33 $3,050.67 $75,895.44

12 $8,878.00 $5,602.15 $3,275.85 $72,619.59

13 $8,878.00 $5,360.35 $3,517.65 $69,101.94

14 $8,878.00 $5,100.69 $3,777.31 $65,324.64

15 $8,878.00 $4,821.88 $4,056.12 $61,268.51

16 $8,878.00 $4,522.48 $4,355.52 $56,912.99

17 $8,878.00 $4,200.98 $4,677.02 $52,235.97

18 $8,878.00 $3,855.75 $5,022.25 $47,213.72

19 $8,878.00 $3,485.04 $5,392.96 $41,820.75

20 $8,878.00 $3,086.96 $5,791.04 $36,029.71

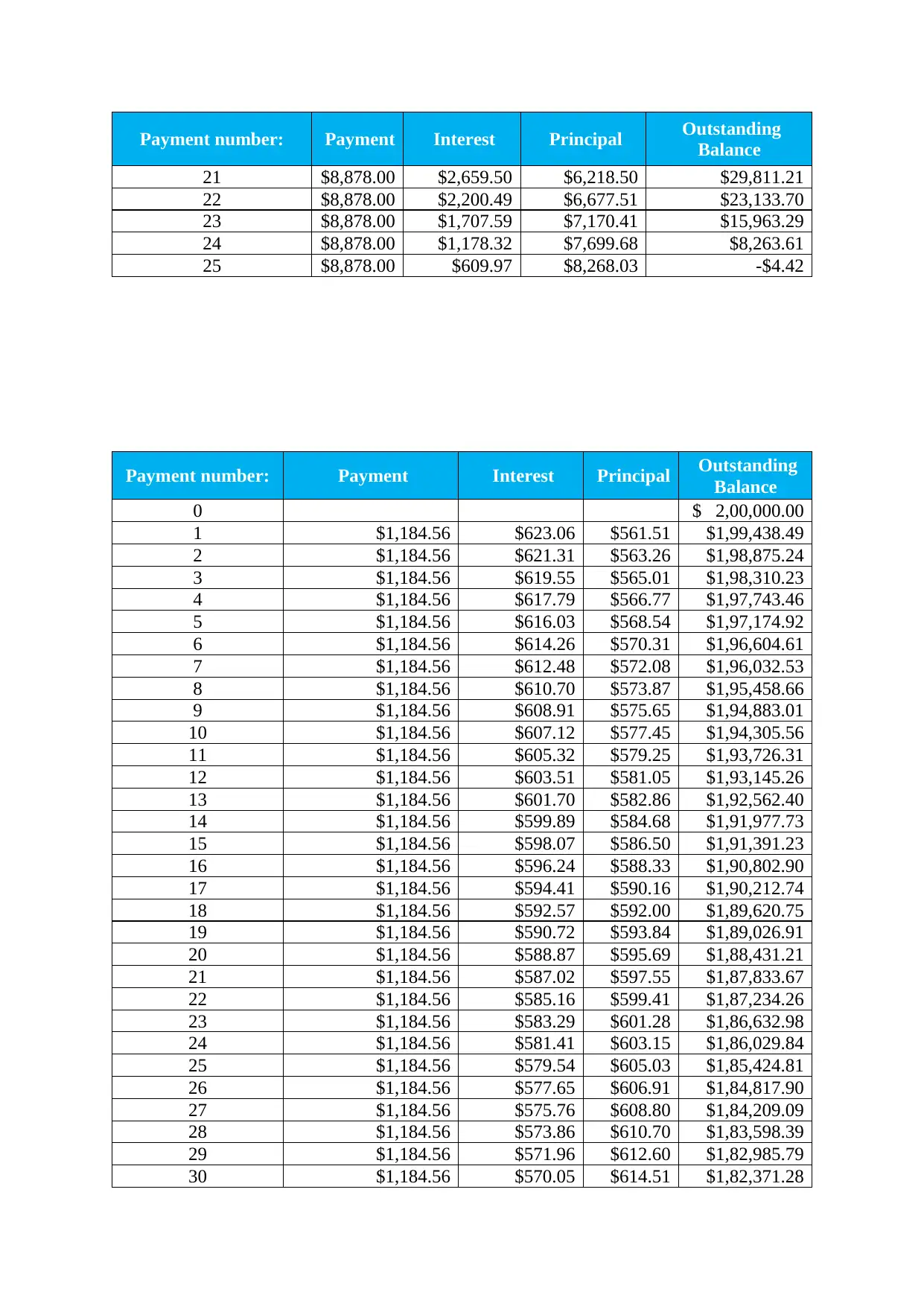

Answer 3

There outstanding balance has not turned to zero because the EMI amount has been rounded off

on account of which higher payment has been made to the lender from the borrower. Further, it is

general industry practice to round the figure to the next larger integer.

The last payment shall be reduced by $4.42 to adjust for excess payment and break even the

situation.

Particulars Facts

Face Value 1,00,000.00

Future Value $0

Amortization Period 25

Term 25

Interest Rate 7.25%

Compounding Frequency 2

Payment Frequency 1

Effective Annual Rate (j1) 0.073814

Nominal Rate 0.073814

Payment number: Payment Interest Principal Outstanding

Balance

0 $ 1,00,000.00

1 $8,878.00 $7,381.41 $1,496.59 $98,503.41

2 $8,878.00 $7,270.94 $1,607.06 $96,896.34

3 $8,878.00 $7,152.31 $1,725.69 $95,170.66

4 $8,878.00 $7,024.93 $1,853.07 $93,317.59

5 $8,878.00 $6,888.15 $1,989.85 $91,327.74

6 $8,878.00 $6,741.27 $2,136.73 $89,191.01

7 $8,878.00 $6,583.55 $2,294.45 $86,896.56

8 $8,878.00 $6,414.19 $2,463.81 $84,432.75

9 $8,878.00 $6,232.32 $2,645.68 $81,787.07

10 $8,878.00 $6,037.04 $2,840.96 $78,946.11

11 $8,878.00 $5,827.33 $3,050.67 $75,895.44

12 $8,878.00 $5,602.15 $3,275.85 $72,619.59

13 $8,878.00 $5,360.35 $3,517.65 $69,101.94

14 $8,878.00 $5,100.69 $3,777.31 $65,324.64

15 $8,878.00 $4,821.88 $4,056.12 $61,268.51

16 $8,878.00 $4,522.48 $4,355.52 $56,912.99

17 $8,878.00 $4,200.98 $4,677.02 $52,235.97

18 $8,878.00 $3,855.75 $5,022.25 $47,213.72

19 $8,878.00 $3,485.04 $5,392.96 $41,820.75

20 $8,878.00 $3,086.96 $5,791.04 $36,029.71

Payment number: Payment Interest Principal Outstanding

Balance

21 $8,878.00 $2,659.50 $6,218.50 $29,811.21

22 $8,878.00 $2,200.49 $6,677.51 $23,133.70

23 $8,878.00 $1,707.59 $7,170.41 $15,963.29

24 $8,878.00 $1,178.32 $7,699.68 $8,263.61

25 $8,878.00 $609.97 $8,268.03 -$4.42

Payment number: Payment Interest Principal Outstanding

Balance

0 $ 2,00,000.00

1 $1,184.56 $623.06 $561.51 $1,99,438.49

2 $1,184.56 $621.31 $563.26 $1,98,875.24

3 $1,184.56 $619.55 $565.01 $1,98,310.23

4 $1,184.56 $617.79 $566.77 $1,97,743.46

5 $1,184.56 $616.03 $568.54 $1,97,174.92

6 $1,184.56 $614.26 $570.31 $1,96,604.61

7 $1,184.56 $612.48 $572.08 $1,96,032.53

8 $1,184.56 $610.70 $573.87 $1,95,458.66

9 $1,184.56 $608.91 $575.65 $1,94,883.01

10 $1,184.56 $607.12 $577.45 $1,94,305.56

11 $1,184.56 $605.32 $579.25 $1,93,726.31

12 $1,184.56 $603.51 $581.05 $1,93,145.26

13 $1,184.56 $601.70 $582.86 $1,92,562.40

14 $1,184.56 $599.89 $584.68 $1,91,977.73

15 $1,184.56 $598.07 $586.50 $1,91,391.23

16 $1,184.56 $596.24 $588.33 $1,90,802.90

17 $1,184.56 $594.41 $590.16 $1,90,212.74

18 $1,184.56 $592.57 $592.00 $1,89,620.75

19 $1,184.56 $590.72 $593.84 $1,89,026.91

20 $1,184.56 $588.87 $595.69 $1,88,431.21

21 $1,184.56 $587.02 $597.55 $1,87,833.67

22 $1,184.56 $585.16 $599.41 $1,87,234.26

23 $1,184.56 $583.29 $601.28 $1,86,632.98

24 $1,184.56 $581.41 $603.15 $1,86,029.84

25 $1,184.56 $579.54 $605.03 $1,85,424.81

26 $1,184.56 $577.65 $606.91 $1,84,817.90

27 $1,184.56 $575.76 $608.80 $1,84,209.09

28 $1,184.56 $573.86 $610.70 $1,83,598.39

29 $1,184.56 $571.96 $612.60 $1,82,985.79

30 $1,184.56 $570.05 $614.51 $1,82,371.28

Balance

21 $8,878.00 $2,659.50 $6,218.50 $29,811.21

22 $8,878.00 $2,200.49 $6,677.51 $23,133.70

23 $8,878.00 $1,707.59 $7,170.41 $15,963.29

24 $8,878.00 $1,178.32 $7,699.68 $8,263.61

25 $8,878.00 $609.97 $8,268.03 -$4.42

Payment number: Payment Interest Principal Outstanding

Balance

0 $ 2,00,000.00

1 $1,184.56 $623.06 $561.51 $1,99,438.49

2 $1,184.56 $621.31 $563.26 $1,98,875.24

3 $1,184.56 $619.55 $565.01 $1,98,310.23

4 $1,184.56 $617.79 $566.77 $1,97,743.46

5 $1,184.56 $616.03 $568.54 $1,97,174.92

6 $1,184.56 $614.26 $570.31 $1,96,604.61

7 $1,184.56 $612.48 $572.08 $1,96,032.53

8 $1,184.56 $610.70 $573.87 $1,95,458.66

9 $1,184.56 $608.91 $575.65 $1,94,883.01

10 $1,184.56 $607.12 $577.45 $1,94,305.56

11 $1,184.56 $605.32 $579.25 $1,93,726.31

12 $1,184.56 $603.51 $581.05 $1,93,145.26

13 $1,184.56 $601.70 $582.86 $1,92,562.40

14 $1,184.56 $599.89 $584.68 $1,91,977.73

15 $1,184.56 $598.07 $586.50 $1,91,391.23

16 $1,184.56 $596.24 $588.33 $1,90,802.90

17 $1,184.56 $594.41 $590.16 $1,90,212.74

18 $1,184.56 $592.57 $592.00 $1,89,620.75

19 $1,184.56 $590.72 $593.84 $1,89,026.91

20 $1,184.56 $588.87 $595.69 $1,88,431.21

21 $1,184.56 $587.02 $597.55 $1,87,833.67

22 $1,184.56 $585.16 $599.41 $1,87,234.26

23 $1,184.56 $583.29 $601.28 $1,86,632.98

24 $1,184.56 $581.41 $603.15 $1,86,029.84

25 $1,184.56 $579.54 $605.03 $1,85,424.81

26 $1,184.56 $577.65 $606.91 $1,84,817.90

27 $1,184.56 $575.76 $608.80 $1,84,209.09

28 $1,184.56 $573.86 $610.70 $1,83,598.39

29 $1,184.56 $571.96 $612.60 $1,82,985.79

30 $1,184.56 $570.05 $614.51 $1,82,371.28

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

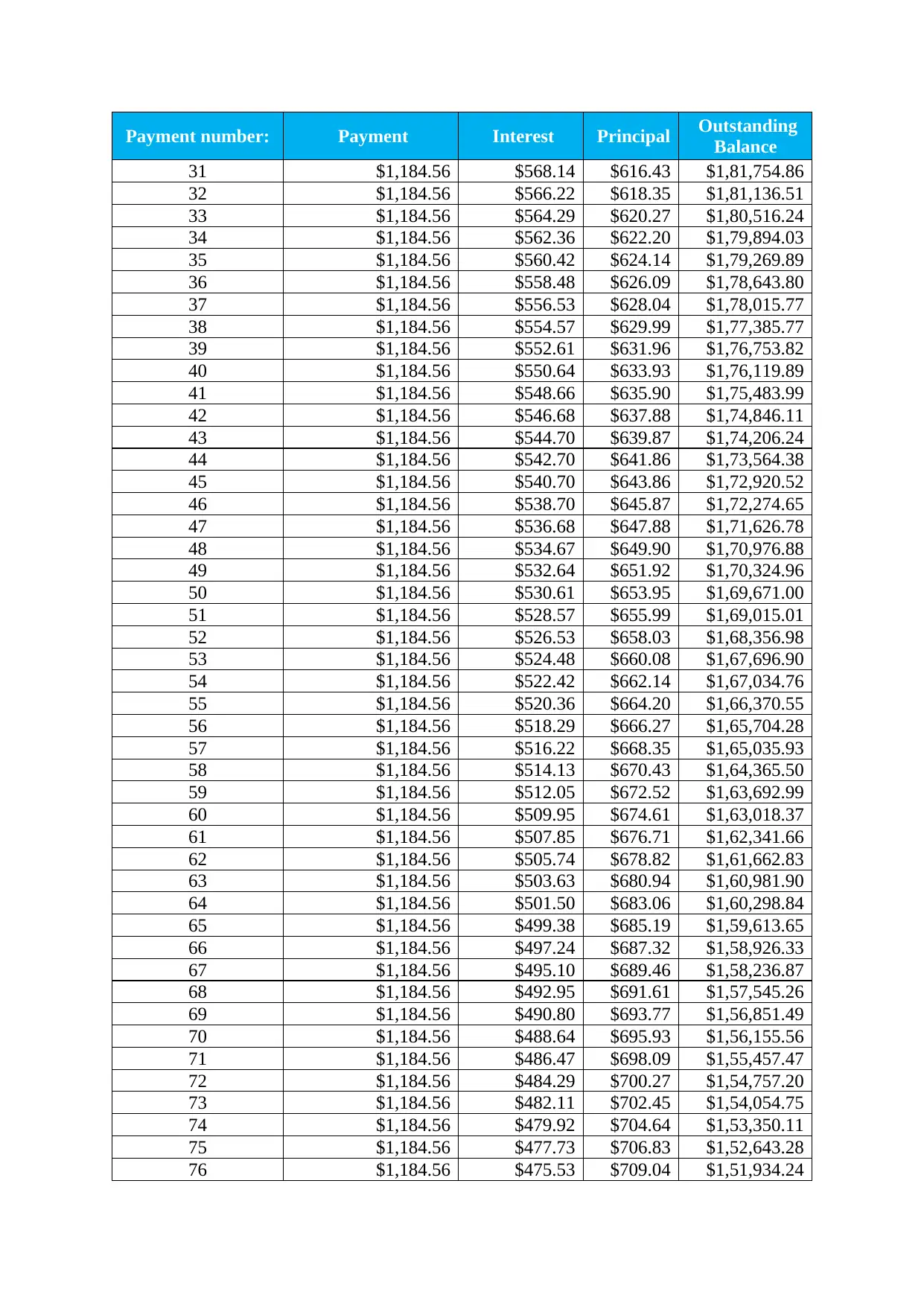

Payment number: Payment Interest Principal Outstanding

Balance

31 $1,184.56 $568.14 $616.43 $1,81,754.86

32 $1,184.56 $566.22 $618.35 $1,81,136.51

33 $1,184.56 $564.29 $620.27 $1,80,516.24

34 $1,184.56 $562.36 $622.20 $1,79,894.03

35 $1,184.56 $560.42 $624.14 $1,79,269.89

36 $1,184.56 $558.48 $626.09 $1,78,643.80

37 $1,184.56 $556.53 $628.04 $1,78,015.77

38 $1,184.56 $554.57 $629.99 $1,77,385.77

39 $1,184.56 $552.61 $631.96 $1,76,753.82

40 $1,184.56 $550.64 $633.93 $1,76,119.89

41 $1,184.56 $548.66 $635.90 $1,75,483.99

42 $1,184.56 $546.68 $637.88 $1,74,846.11

43 $1,184.56 $544.70 $639.87 $1,74,206.24

44 $1,184.56 $542.70 $641.86 $1,73,564.38

45 $1,184.56 $540.70 $643.86 $1,72,920.52

46 $1,184.56 $538.70 $645.87 $1,72,274.65

47 $1,184.56 $536.68 $647.88 $1,71,626.78

48 $1,184.56 $534.67 $649.90 $1,70,976.88

49 $1,184.56 $532.64 $651.92 $1,70,324.96

50 $1,184.56 $530.61 $653.95 $1,69,671.00

51 $1,184.56 $528.57 $655.99 $1,69,015.01

52 $1,184.56 $526.53 $658.03 $1,68,356.98

53 $1,184.56 $524.48 $660.08 $1,67,696.90

54 $1,184.56 $522.42 $662.14 $1,67,034.76

55 $1,184.56 $520.36 $664.20 $1,66,370.55

56 $1,184.56 $518.29 $666.27 $1,65,704.28

57 $1,184.56 $516.22 $668.35 $1,65,035.93

58 $1,184.56 $514.13 $670.43 $1,64,365.50

59 $1,184.56 $512.05 $672.52 $1,63,692.99

60 $1,184.56 $509.95 $674.61 $1,63,018.37

61 $1,184.56 $507.85 $676.71 $1,62,341.66

62 $1,184.56 $505.74 $678.82 $1,61,662.83

63 $1,184.56 $503.63 $680.94 $1,60,981.90

64 $1,184.56 $501.50 $683.06 $1,60,298.84

65 $1,184.56 $499.38 $685.19 $1,59,613.65

66 $1,184.56 $497.24 $687.32 $1,58,926.33

67 $1,184.56 $495.10 $689.46 $1,58,236.87

68 $1,184.56 $492.95 $691.61 $1,57,545.26

69 $1,184.56 $490.80 $693.77 $1,56,851.49

70 $1,184.56 $488.64 $695.93 $1,56,155.56

71 $1,184.56 $486.47 $698.09 $1,55,457.47

72 $1,184.56 $484.29 $700.27 $1,54,757.20

73 $1,184.56 $482.11 $702.45 $1,54,054.75

74 $1,184.56 $479.92 $704.64 $1,53,350.11

75 $1,184.56 $477.73 $706.83 $1,52,643.28

76 $1,184.56 $475.53 $709.04 $1,51,934.24

Balance

31 $1,184.56 $568.14 $616.43 $1,81,754.86

32 $1,184.56 $566.22 $618.35 $1,81,136.51

33 $1,184.56 $564.29 $620.27 $1,80,516.24

34 $1,184.56 $562.36 $622.20 $1,79,894.03

35 $1,184.56 $560.42 $624.14 $1,79,269.89

36 $1,184.56 $558.48 $626.09 $1,78,643.80

37 $1,184.56 $556.53 $628.04 $1,78,015.77

38 $1,184.56 $554.57 $629.99 $1,77,385.77

39 $1,184.56 $552.61 $631.96 $1,76,753.82

40 $1,184.56 $550.64 $633.93 $1,76,119.89

41 $1,184.56 $548.66 $635.90 $1,75,483.99

42 $1,184.56 $546.68 $637.88 $1,74,846.11

43 $1,184.56 $544.70 $639.87 $1,74,206.24

44 $1,184.56 $542.70 $641.86 $1,73,564.38

45 $1,184.56 $540.70 $643.86 $1,72,920.52

46 $1,184.56 $538.70 $645.87 $1,72,274.65

47 $1,184.56 $536.68 $647.88 $1,71,626.78

48 $1,184.56 $534.67 $649.90 $1,70,976.88

49 $1,184.56 $532.64 $651.92 $1,70,324.96

50 $1,184.56 $530.61 $653.95 $1,69,671.00

51 $1,184.56 $528.57 $655.99 $1,69,015.01

52 $1,184.56 $526.53 $658.03 $1,68,356.98

53 $1,184.56 $524.48 $660.08 $1,67,696.90

54 $1,184.56 $522.42 $662.14 $1,67,034.76

55 $1,184.56 $520.36 $664.20 $1,66,370.55

56 $1,184.56 $518.29 $666.27 $1,65,704.28

57 $1,184.56 $516.22 $668.35 $1,65,035.93

58 $1,184.56 $514.13 $670.43 $1,64,365.50

59 $1,184.56 $512.05 $672.52 $1,63,692.99

60 $1,184.56 $509.95 $674.61 $1,63,018.37

61 $1,184.56 $507.85 $676.71 $1,62,341.66

62 $1,184.56 $505.74 $678.82 $1,61,662.83

63 $1,184.56 $503.63 $680.94 $1,60,981.90

64 $1,184.56 $501.50 $683.06 $1,60,298.84

65 $1,184.56 $499.38 $685.19 $1,59,613.65

66 $1,184.56 $497.24 $687.32 $1,58,926.33

67 $1,184.56 $495.10 $689.46 $1,58,236.87

68 $1,184.56 $492.95 $691.61 $1,57,545.26

69 $1,184.56 $490.80 $693.77 $1,56,851.49

70 $1,184.56 $488.64 $695.93 $1,56,155.56

71 $1,184.56 $486.47 $698.09 $1,55,457.47

72 $1,184.56 $484.29 $700.27 $1,54,757.20

73 $1,184.56 $482.11 $702.45 $1,54,054.75

74 $1,184.56 $479.92 $704.64 $1,53,350.11

75 $1,184.56 $477.73 $706.83 $1,52,643.28

76 $1,184.56 $475.53 $709.04 $1,51,934.24

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

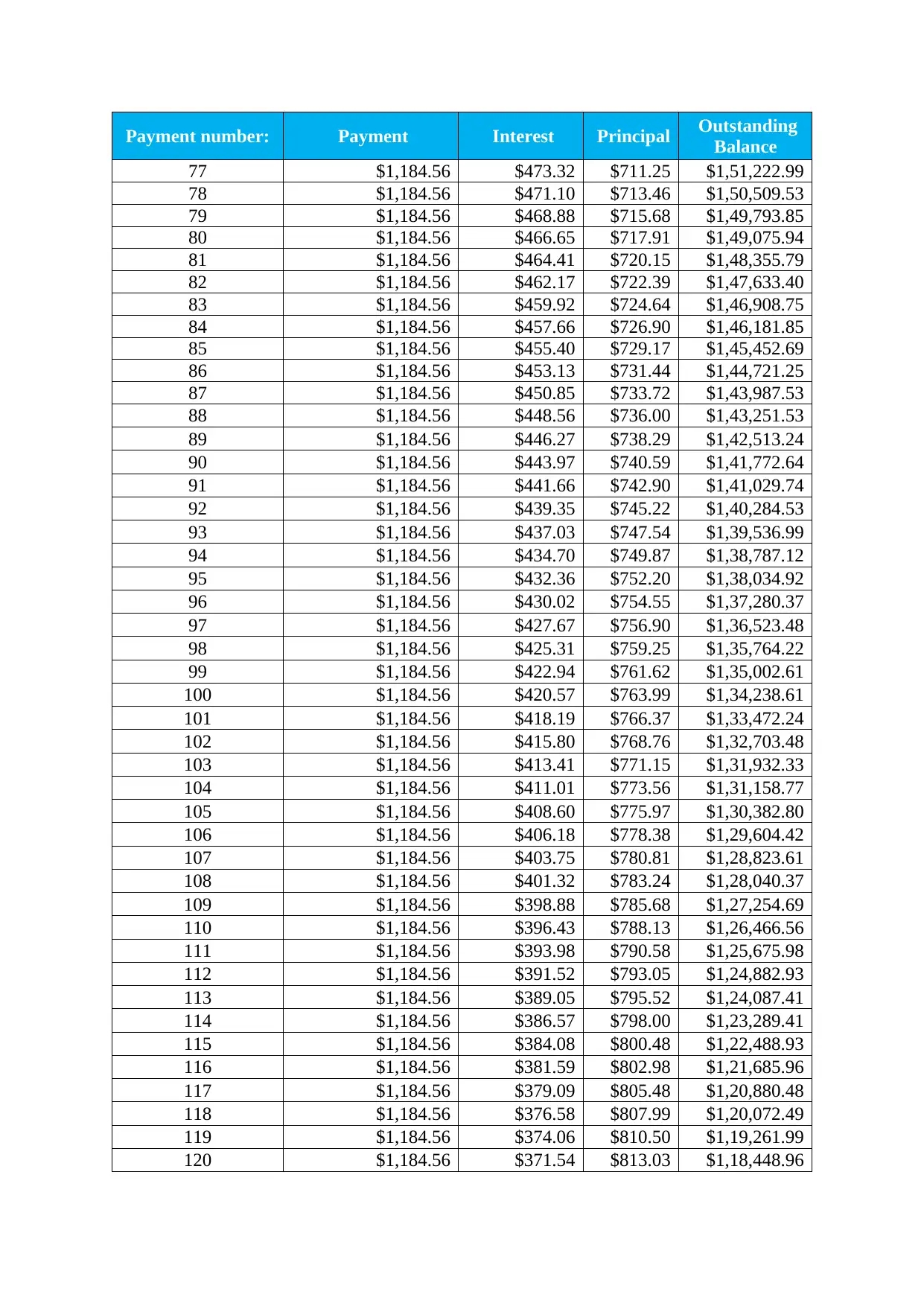

Payment number: Payment Interest Principal Outstanding

Balance

77 $1,184.56 $473.32 $711.25 $1,51,222.99

78 $1,184.56 $471.10 $713.46 $1,50,509.53

79 $1,184.56 $468.88 $715.68 $1,49,793.85

80 $1,184.56 $466.65 $717.91 $1,49,075.94

81 $1,184.56 $464.41 $720.15 $1,48,355.79

82 $1,184.56 $462.17 $722.39 $1,47,633.40

83 $1,184.56 $459.92 $724.64 $1,46,908.75

84 $1,184.56 $457.66 $726.90 $1,46,181.85

85 $1,184.56 $455.40 $729.17 $1,45,452.69

86 $1,184.56 $453.13 $731.44 $1,44,721.25

87 $1,184.56 $450.85 $733.72 $1,43,987.53

88 $1,184.56 $448.56 $736.00 $1,43,251.53

89 $1,184.56 $446.27 $738.29 $1,42,513.24

90 $1,184.56 $443.97 $740.59 $1,41,772.64

91 $1,184.56 $441.66 $742.90 $1,41,029.74

92 $1,184.56 $439.35 $745.22 $1,40,284.53

93 $1,184.56 $437.03 $747.54 $1,39,536.99

94 $1,184.56 $434.70 $749.87 $1,38,787.12

95 $1,184.56 $432.36 $752.20 $1,38,034.92

96 $1,184.56 $430.02 $754.55 $1,37,280.37

97 $1,184.56 $427.67 $756.90 $1,36,523.48

98 $1,184.56 $425.31 $759.25 $1,35,764.22

99 $1,184.56 $422.94 $761.62 $1,35,002.61

100 $1,184.56 $420.57 $763.99 $1,34,238.61

101 $1,184.56 $418.19 $766.37 $1,33,472.24

102 $1,184.56 $415.80 $768.76 $1,32,703.48

103 $1,184.56 $413.41 $771.15 $1,31,932.33

104 $1,184.56 $411.01 $773.56 $1,31,158.77

105 $1,184.56 $408.60 $775.97 $1,30,382.80

106 $1,184.56 $406.18 $778.38 $1,29,604.42

107 $1,184.56 $403.75 $780.81 $1,28,823.61

108 $1,184.56 $401.32 $783.24 $1,28,040.37

109 $1,184.56 $398.88 $785.68 $1,27,254.69

110 $1,184.56 $396.43 $788.13 $1,26,466.56

111 $1,184.56 $393.98 $790.58 $1,25,675.98

112 $1,184.56 $391.52 $793.05 $1,24,882.93

113 $1,184.56 $389.05 $795.52 $1,24,087.41

114 $1,184.56 $386.57 $798.00 $1,23,289.41

115 $1,184.56 $384.08 $800.48 $1,22,488.93

116 $1,184.56 $381.59 $802.98 $1,21,685.96

117 $1,184.56 $379.09 $805.48 $1,20,880.48

118 $1,184.56 $376.58 $807.99 $1,20,072.49

119 $1,184.56 $374.06 $810.50 $1,19,261.99

120 $1,184.56 $371.54 $813.03 $1,18,448.96

Balance

77 $1,184.56 $473.32 $711.25 $1,51,222.99

78 $1,184.56 $471.10 $713.46 $1,50,509.53

79 $1,184.56 $468.88 $715.68 $1,49,793.85

80 $1,184.56 $466.65 $717.91 $1,49,075.94

81 $1,184.56 $464.41 $720.15 $1,48,355.79

82 $1,184.56 $462.17 $722.39 $1,47,633.40

83 $1,184.56 $459.92 $724.64 $1,46,908.75

84 $1,184.56 $457.66 $726.90 $1,46,181.85

85 $1,184.56 $455.40 $729.17 $1,45,452.69

86 $1,184.56 $453.13 $731.44 $1,44,721.25

87 $1,184.56 $450.85 $733.72 $1,43,987.53

88 $1,184.56 $448.56 $736.00 $1,43,251.53

89 $1,184.56 $446.27 $738.29 $1,42,513.24

90 $1,184.56 $443.97 $740.59 $1,41,772.64

91 $1,184.56 $441.66 $742.90 $1,41,029.74

92 $1,184.56 $439.35 $745.22 $1,40,284.53

93 $1,184.56 $437.03 $747.54 $1,39,536.99

94 $1,184.56 $434.70 $749.87 $1,38,787.12

95 $1,184.56 $432.36 $752.20 $1,38,034.92

96 $1,184.56 $430.02 $754.55 $1,37,280.37

97 $1,184.56 $427.67 $756.90 $1,36,523.48

98 $1,184.56 $425.31 $759.25 $1,35,764.22

99 $1,184.56 $422.94 $761.62 $1,35,002.61

100 $1,184.56 $420.57 $763.99 $1,34,238.61

101 $1,184.56 $418.19 $766.37 $1,33,472.24

102 $1,184.56 $415.80 $768.76 $1,32,703.48

103 $1,184.56 $413.41 $771.15 $1,31,932.33

104 $1,184.56 $411.01 $773.56 $1,31,158.77

105 $1,184.56 $408.60 $775.97 $1,30,382.80

106 $1,184.56 $406.18 $778.38 $1,29,604.42

107 $1,184.56 $403.75 $780.81 $1,28,823.61

108 $1,184.56 $401.32 $783.24 $1,28,040.37

109 $1,184.56 $398.88 $785.68 $1,27,254.69

110 $1,184.56 $396.43 $788.13 $1,26,466.56

111 $1,184.56 $393.98 $790.58 $1,25,675.98

112 $1,184.56 $391.52 $793.05 $1,24,882.93

113 $1,184.56 $389.05 $795.52 $1,24,087.41

114 $1,184.56 $386.57 $798.00 $1,23,289.41

115 $1,184.56 $384.08 $800.48 $1,22,488.93

116 $1,184.56 $381.59 $802.98 $1,21,685.96

117 $1,184.56 $379.09 $805.48 $1,20,880.48

118 $1,184.56 $376.58 $807.99 $1,20,072.49

119 $1,184.56 $374.06 $810.50 $1,19,261.99

120 $1,184.56 $371.54 $813.03 $1,18,448.96

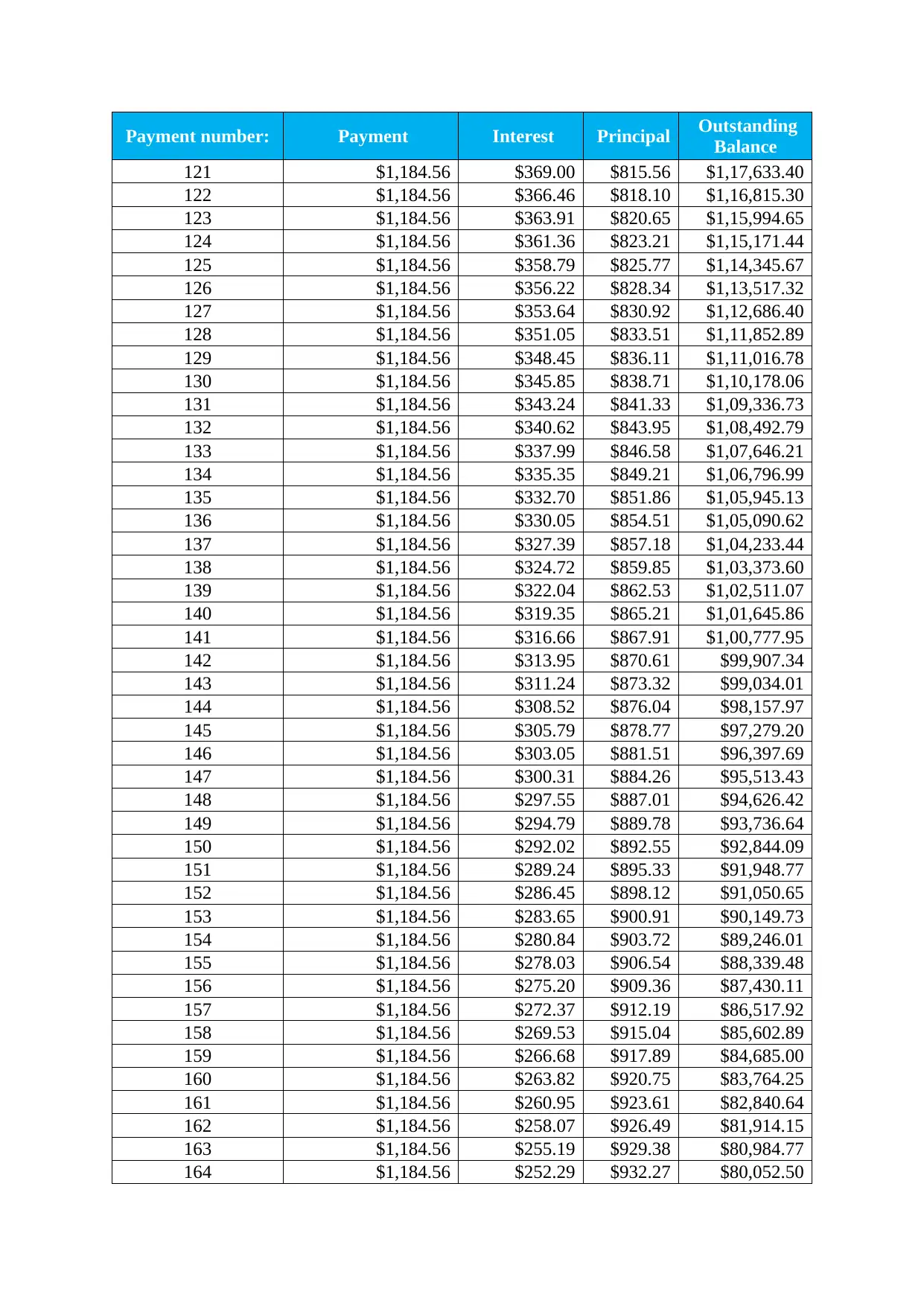

Payment number: Payment Interest Principal Outstanding

Balance

121 $1,184.56 $369.00 $815.56 $1,17,633.40

122 $1,184.56 $366.46 $818.10 $1,16,815.30

123 $1,184.56 $363.91 $820.65 $1,15,994.65

124 $1,184.56 $361.36 $823.21 $1,15,171.44

125 $1,184.56 $358.79 $825.77 $1,14,345.67

126 $1,184.56 $356.22 $828.34 $1,13,517.32

127 $1,184.56 $353.64 $830.92 $1,12,686.40

128 $1,184.56 $351.05 $833.51 $1,11,852.89

129 $1,184.56 $348.45 $836.11 $1,11,016.78

130 $1,184.56 $345.85 $838.71 $1,10,178.06

131 $1,184.56 $343.24 $841.33 $1,09,336.73

132 $1,184.56 $340.62 $843.95 $1,08,492.79

133 $1,184.56 $337.99 $846.58 $1,07,646.21

134 $1,184.56 $335.35 $849.21 $1,06,796.99

135 $1,184.56 $332.70 $851.86 $1,05,945.13

136 $1,184.56 $330.05 $854.51 $1,05,090.62

137 $1,184.56 $327.39 $857.18 $1,04,233.44

138 $1,184.56 $324.72 $859.85 $1,03,373.60

139 $1,184.56 $322.04 $862.53 $1,02,511.07

140 $1,184.56 $319.35 $865.21 $1,01,645.86

141 $1,184.56 $316.66 $867.91 $1,00,777.95

142 $1,184.56 $313.95 $870.61 $99,907.34

143 $1,184.56 $311.24 $873.32 $99,034.01

144 $1,184.56 $308.52 $876.04 $98,157.97

145 $1,184.56 $305.79 $878.77 $97,279.20

146 $1,184.56 $303.05 $881.51 $96,397.69

147 $1,184.56 $300.31 $884.26 $95,513.43

148 $1,184.56 $297.55 $887.01 $94,626.42

149 $1,184.56 $294.79 $889.78 $93,736.64

150 $1,184.56 $292.02 $892.55 $92,844.09

151 $1,184.56 $289.24 $895.33 $91,948.77

152 $1,184.56 $286.45 $898.12 $91,050.65

153 $1,184.56 $283.65 $900.91 $90,149.73

154 $1,184.56 $280.84 $903.72 $89,246.01

155 $1,184.56 $278.03 $906.54 $88,339.48

156 $1,184.56 $275.20 $909.36 $87,430.11

157 $1,184.56 $272.37 $912.19 $86,517.92

158 $1,184.56 $269.53 $915.04 $85,602.89

159 $1,184.56 $266.68 $917.89 $84,685.00

160 $1,184.56 $263.82 $920.75 $83,764.25

161 $1,184.56 $260.95 $923.61 $82,840.64

162 $1,184.56 $258.07 $926.49 $81,914.15

163 $1,184.56 $255.19 $929.38 $80,984.77

164 $1,184.56 $252.29 $932.27 $80,052.50

Balance

121 $1,184.56 $369.00 $815.56 $1,17,633.40

122 $1,184.56 $366.46 $818.10 $1,16,815.30

123 $1,184.56 $363.91 $820.65 $1,15,994.65

124 $1,184.56 $361.36 $823.21 $1,15,171.44

125 $1,184.56 $358.79 $825.77 $1,14,345.67

126 $1,184.56 $356.22 $828.34 $1,13,517.32

127 $1,184.56 $353.64 $830.92 $1,12,686.40

128 $1,184.56 $351.05 $833.51 $1,11,852.89

129 $1,184.56 $348.45 $836.11 $1,11,016.78

130 $1,184.56 $345.85 $838.71 $1,10,178.06

131 $1,184.56 $343.24 $841.33 $1,09,336.73

132 $1,184.56 $340.62 $843.95 $1,08,492.79

133 $1,184.56 $337.99 $846.58 $1,07,646.21

134 $1,184.56 $335.35 $849.21 $1,06,796.99

135 $1,184.56 $332.70 $851.86 $1,05,945.13

136 $1,184.56 $330.05 $854.51 $1,05,090.62

137 $1,184.56 $327.39 $857.18 $1,04,233.44

138 $1,184.56 $324.72 $859.85 $1,03,373.60

139 $1,184.56 $322.04 $862.53 $1,02,511.07

140 $1,184.56 $319.35 $865.21 $1,01,645.86

141 $1,184.56 $316.66 $867.91 $1,00,777.95

142 $1,184.56 $313.95 $870.61 $99,907.34

143 $1,184.56 $311.24 $873.32 $99,034.01

144 $1,184.56 $308.52 $876.04 $98,157.97

145 $1,184.56 $305.79 $878.77 $97,279.20

146 $1,184.56 $303.05 $881.51 $96,397.69

147 $1,184.56 $300.31 $884.26 $95,513.43

148 $1,184.56 $297.55 $887.01 $94,626.42

149 $1,184.56 $294.79 $889.78 $93,736.64

150 $1,184.56 $292.02 $892.55 $92,844.09

151 $1,184.56 $289.24 $895.33 $91,948.77

152 $1,184.56 $286.45 $898.12 $91,050.65

153 $1,184.56 $283.65 $900.91 $90,149.73

154 $1,184.56 $280.84 $903.72 $89,246.01

155 $1,184.56 $278.03 $906.54 $88,339.48

156 $1,184.56 $275.20 $909.36 $87,430.11

157 $1,184.56 $272.37 $912.19 $86,517.92

158 $1,184.56 $269.53 $915.04 $85,602.89

159 $1,184.56 $266.68 $917.89 $84,685.00

160 $1,184.56 $263.82 $920.75 $83,764.25

161 $1,184.56 $260.95 $923.61 $82,840.64

162 $1,184.56 $258.07 $926.49 $81,914.15

163 $1,184.56 $255.19 $929.38 $80,984.77

164 $1,184.56 $252.29 $932.27 $80,052.50

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

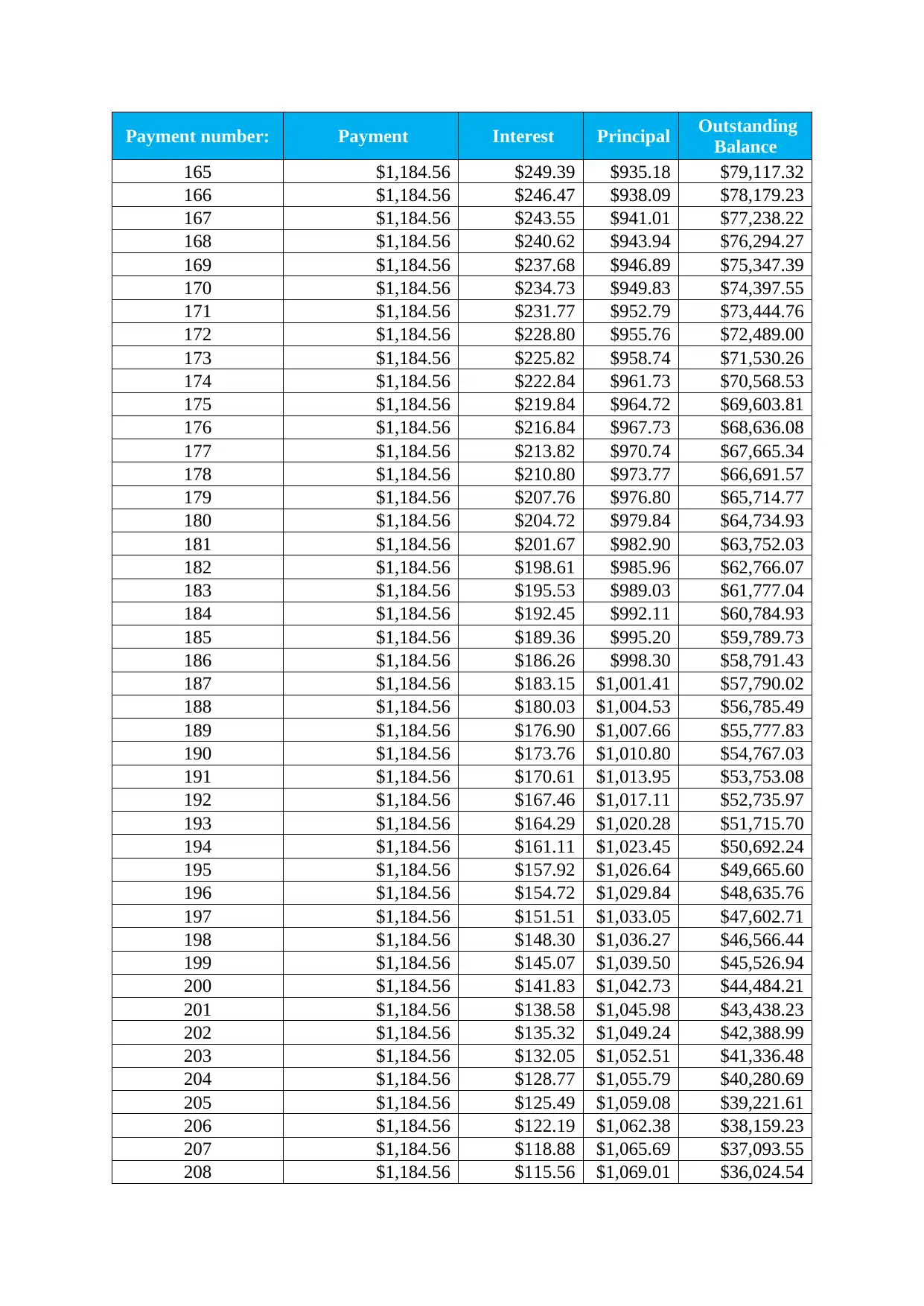

Payment number: Payment Interest Principal Outstanding

Balance

165 $1,184.56 $249.39 $935.18 $79,117.32

166 $1,184.56 $246.47 $938.09 $78,179.23

167 $1,184.56 $243.55 $941.01 $77,238.22

168 $1,184.56 $240.62 $943.94 $76,294.27

169 $1,184.56 $237.68 $946.89 $75,347.39

170 $1,184.56 $234.73 $949.83 $74,397.55

171 $1,184.56 $231.77 $952.79 $73,444.76

172 $1,184.56 $228.80 $955.76 $72,489.00

173 $1,184.56 $225.82 $958.74 $71,530.26

174 $1,184.56 $222.84 $961.73 $70,568.53

175 $1,184.56 $219.84 $964.72 $69,603.81

176 $1,184.56 $216.84 $967.73 $68,636.08

177 $1,184.56 $213.82 $970.74 $67,665.34

178 $1,184.56 $210.80 $973.77 $66,691.57

179 $1,184.56 $207.76 $976.80 $65,714.77

180 $1,184.56 $204.72 $979.84 $64,734.93

181 $1,184.56 $201.67 $982.90 $63,752.03

182 $1,184.56 $198.61 $985.96 $62,766.07

183 $1,184.56 $195.53 $989.03 $61,777.04

184 $1,184.56 $192.45 $992.11 $60,784.93

185 $1,184.56 $189.36 $995.20 $59,789.73

186 $1,184.56 $186.26 $998.30 $58,791.43

187 $1,184.56 $183.15 $1,001.41 $57,790.02

188 $1,184.56 $180.03 $1,004.53 $56,785.49

189 $1,184.56 $176.90 $1,007.66 $55,777.83

190 $1,184.56 $173.76 $1,010.80 $54,767.03

191 $1,184.56 $170.61 $1,013.95 $53,753.08

192 $1,184.56 $167.46 $1,017.11 $52,735.97

193 $1,184.56 $164.29 $1,020.28 $51,715.70

194 $1,184.56 $161.11 $1,023.45 $50,692.24

195 $1,184.56 $157.92 $1,026.64 $49,665.60

196 $1,184.56 $154.72 $1,029.84 $48,635.76

197 $1,184.56 $151.51 $1,033.05 $47,602.71

198 $1,184.56 $148.30 $1,036.27 $46,566.44

199 $1,184.56 $145.07 $1,039.50 $45,526.94

200 $1,184.56 $141.83 $1,042.73 $44,484.21

201 $1,184.56 $138.58 $1,045.98 $43,438.23

202 $1,184.56 $135.32 $1,049.24 $42,388.99

203 $1,184.56 $132.05 $1,052.51 $41,336.48

204 $1,184.56 $128.77 $1,055.79 $40,280.69

205 $1,184.56 $125.49 $1,059.08 $39,221.61

206 $1,184.56 $122.19 $1,062.38 $38,159.23

207 $1,184.56 $118.88 $1,065.69 $37,093.55

208 $1,184.56 $115.56 $1,069.01 $36,024.54

Balance

165 $1,184.56 $249.39 $935.18 $79,117.32

166 $1,184.56 $246.47 $938.09 $78,179.23

167 $1,184.56 $243.55 $941.01 $77,238.22

168 $1,184.56 $240.62 $943.94 $76,294.27

169 $1,184.56 $237.68 $946.89 $75,347.39

170 $1,184.56 $234.73 $949.83 $74,397.55

171 $1,184.56 $231.77 $952.79 $73,444.76

172 $1,184.56 $228.80 $955.76 $72,489.00

173 $1,184.56 $225.82 $958.74 $71,530.26

174 $1,184.56 $222.84 $961.73 $70,568.53

175 $1,184.56 $219.84 $964.72 $69,603.81

176 $1,184.56 $216.84 $967.73 $68,636.08

177 $1,184.56 $213.82 $970.74 $67,665.34

178 $1,184.56 $210.80 $973.77 $66,691.57

179 $1,184.56 $207.76 $976.80 $65,714.77

180 $1,184.56 $204.72 $979.84 $64,734.93

181 $1,184.56 $201.67 $982.90 $63,752.03

182 $1,184.56 $198.61 $985.96 $62,766.07

183 $1,184.56 $195.53 $989.03 $61,777.04

184 $1,184.56 $192.45 $992.11 $60,784.93

185 $1,184.56 $189.36 $995.20 $59,789.73

186 $1,184.56 $186.26 $998.30 $58,791.43

187 $1,184.56 $183.15 $1,001.41 $57,790.02

188 $1,184.56 $180.03 $1,004.53 $56,785.49

189 $1,184.56 $176.90 $1,007.66 $55,777.83

190 $1,184.56 $173.76 $1,010.80 $54,767.03

191 $1,184.56 $170.61 $1,013.95 $53,753.08

192 $1,184.56 $167.46 $1,017.11 $52,735.97

193 $1,184.56 $164.29 $1,020.28 $51,715.70

194 $1,184.56 $161.11 $1,023.45 $50,692.24

195 $1,184.56 $157.92 $1,026.64 $49,665.60

196 $1,184.56 $154.72 $1,029.84 $48,635.76

197 $1,184.56 $151.51 $1,033.05 $47,602.71

198 $1,184.56 $148.30 $1,036.27 $46,566.44

199 $1,184.56 $145.07 $1,039.50 $45,526.94

200 $1,184.56 $141.83 $1,042.73 $44,484.21

201 $1,184.56 $138.58 $1,045.98 $43,438.23

202 $1,184.56 $135.32 $1,049.24 $42,388.99

203 $1,184.56 $132.05 $1,052.51 $41,336.48

204 $1,184.56 $128.77 $1,055.79 $40,280.69

205 $1,184.56 $125.49 $1,059.08 $39,221.61

206 $1,184.56 $122.19 $1,062.38 $38,159.23

207 $1,184.56 $118.88 $1,065.69 $37,093.55

208 $1,184.56 $115.56 $1,069.01 $36,024.54

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

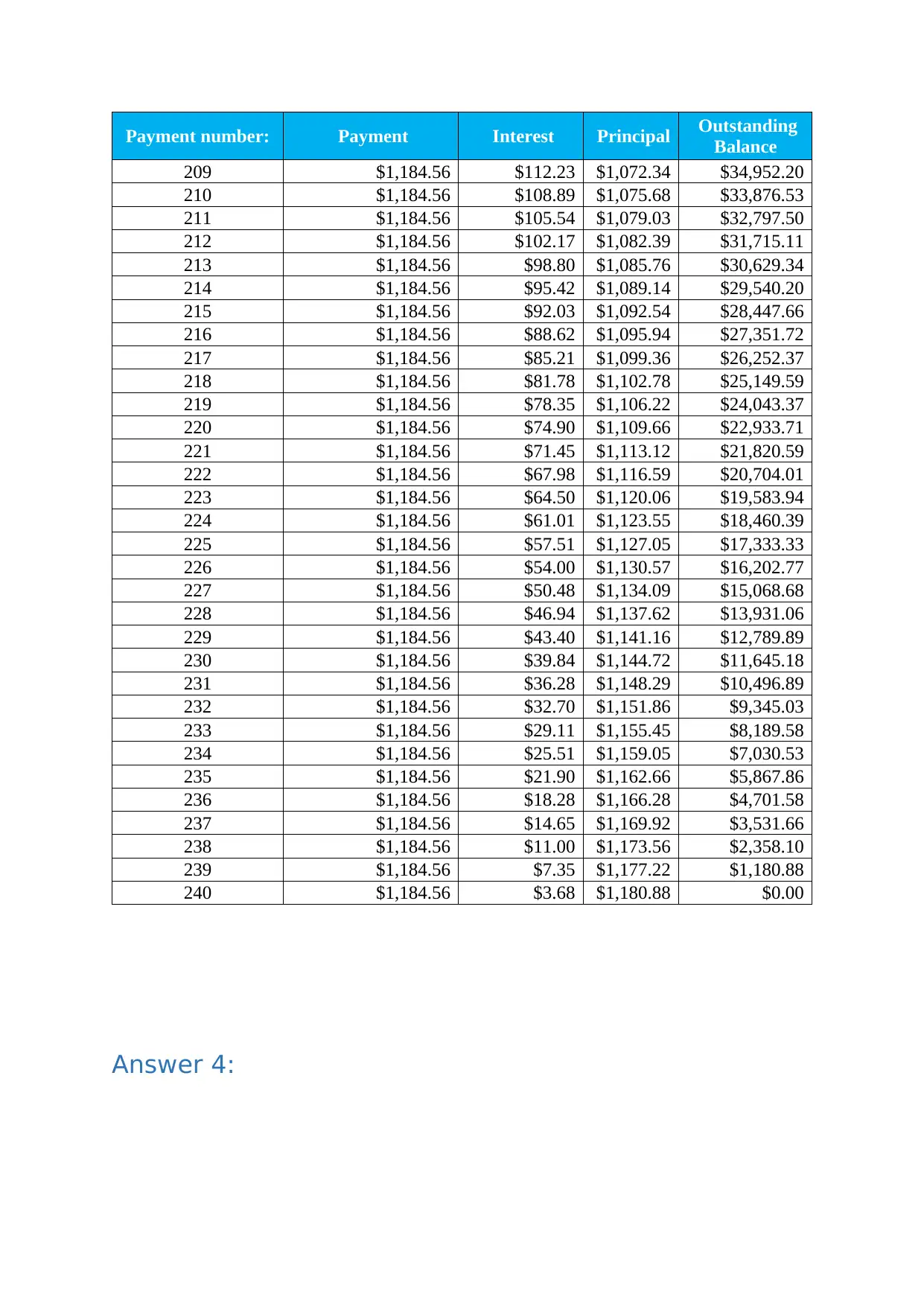

Payment number: Payment Interest Principal Outstanding

Balance

209 $1,184.56 $112.23 $1,072.34 $34,952.20

210 $1,184.56 $108.89 $1,075.68 $33,876.53

211 $1,184.56 $105.54 $1,079.03 $32,797.50

212 $1,184.56 $102.17 $1,082.39 $31,715.11

213 $1,184.56 $98.80 $1,085.76 $30,629.34

214 $1,184.56 $95.42 $1,089.14 $29,540.20

215 $1,184.56 $92.03 $1,092.54 $28,447.66

216 $1,184.56 $88.62 $1,095.94 $27,351.72

217 $1,184.56 $85.21 $1,099.36 $26,252.37

218 $1,184.56 $81.78 $1,102.78 $25,149.59

219 $1,184.56 $78.35 $1,106.22 $24,043.37

220 $1,184.56 $74.90 $1,109.66 $22,933.71

221 $1,184.56 $71.45 $1,113.12 $21,820.59

222 $1,184.56 $67.98 $1,116.59 $20,704.01

223 $1,184.56 $64.50 $1,120.06 $19,583.94

224 $1,184.56 $61.01 $1,123.55 $18,460.39

225 $1,184.56 $57.51 $1,127.05 $17,333.33

226 $1,184.56 $54.00 $1,130.57 $16,202.77

227 $1,184.56 $50.48 $1,134.09 $15,068.68

228 $1,184.56 $46.94 $1,137.62 $13,931.06

229 $1,184.56 $43.40 $1,141.16 $12,789.89

230 $1,184.56 $39.84 $1,144.72 $11,645.18

231 $1,184.56 $36.28 $1,148.29 $10,496.89

232 $1,184.56 $32.70 $1,151.86 $9,345.03

233 $1,184.56 $29.11 $1,155.45 $8,189.58

234 $1,184.56 $25.51 $1,159.05 $7,030.53

235 $1,184.56 $21.90 $1,162.66 $5,867.86

236 $1,184.56 $18.28 $1,166.28 $4,701.58

237 $1,184.56 $14.65 $1,169.92 $3,531.66

238 $1,184.56 $11.00 $1,173.56 $2,358.10

239 $1,184.56 $7.35 $1,177.22 $1,180.88

240 $1,184.56 $3.68 $1,180.88 $0.00

Answer 4:

Balance

209 $1,184.56 $112.23 $1,072.34 $34,952.20

210 $1,184.56 $108.89 $1,075.68 $33,876.53

211 $1,184.56 $105.54 $1,079.03 $32,797.50

212 $1,184.56 $102.17 $1,082.39 $31,715.11

213 $1,184.56 $98.80 $1,085.76 $30,629.34

214 $1,184.56 $95.42 $1,089.14 $29,540.20

215 $1,184.56 $92.03 $1,092.54 $28,447.66

216 $1,184.56 $88.62 $1,095.94 $27,351.72

217 $1,184.56 $85.21 $1,099.36 $26,252.37

218 $1,184.56 $81.78 $1,102.78 $25,149.59

219 $1,184.56 $78.35 $1,106.22 $24,043.37

220 $1,184.56 $74.90 $1,109.66 $22,933.71

221 $1,184.56 $71.45 $1,113.12 $21,820.59

222 $1,184.56 $67.98 $1,116.59 $20,704.01

223 $1,184.56 $64.50 $1,120.06 $19,583.94

224 $1,184.56 $61.01 $1,123.55 $18,460.39

225 $1,184.56 $57.51 $1,127.05 $17,333.33

226 $1,184.56 $54.00 $1,130.57 $16,202.77

227 $1,184.56 $50.48 $1,134.09 $15,068.68

228 $1,184.56 $46.94 $1,137.62 $13,931.06

229 $1,184.56 $43.40 $1,141.16 $12,789.89

230 $1,184.56 $39.84 $1,144.72 $11,645.18

231 $1,184.56 $36.28 $1,148.29 $10,496.89

232 $1,184.56 $32.70 $1,151.86 $9,345.03

233 $1,184.56 $29.11 $1,155.45 $8,189.58

234 $1,184.56 $25.51 $1,159.05 $7,030.53

235 $1,184.56 $21.90 $1,162.66 $5,867.86

236 $1,184.56 $18.28 $1,166.28 $4,701.58

237 $1,184.56 $14.65 $1,169.92 $3,531.66

238 $1,184.56 $11.00 $1,173.56 $2,358.10

239 $1,184.56 $7.35 $1,177.22 $1,180.88

240 $1,184.56 $3.68 $1,180.88 $0.00

Answer 4:

INTRODUCTION

Mortgage market is divided into two parts as primary mortgage market and secondary

mortgage market. Primary mortgage market refers to a market which provides loans to the

normal public and the company who buys property from the market. The secondary

mortgage market is discovered by the financial institutions.

Many people have a vision that the mortgage market is very much complicated but in fact

the reality is different. The mortgage market is very simple to understand and implement.

By understanding properly one can get a proper information about the lenders available in

the market. The first and most important part is to understand who is actually the person

who will lend the money to you. Two types of lender are available in the market institutional

lenders and private lenders. Generally, the institutional lenders are the commercial banks,

Savings and Loan, credit unions, pension funds and insurance companies. The institutional

lenders provide loan to the borrower on the basis of the credit worthiness of the borrower.

The loans are provided on the basis of the rules and guidelines prescribed. On the other

hand, private lenders are generally individuals, companies and they are not regulated by the

government. As the private lenders are not regulated through any government therefore,

they have a very flexible policy.

Depends on the types of loans

Accordingly, on the basis of above information one now knows who is the lender in the

market and how it works. In a market two types of conventional loans prevailed conforming

loans and non-conforming loans. Conforming type of loans is strictly based on Freddie Mac

policy and offer the very attractive rate of interest to the buyer. Non-conforming loans are

the guidelines and policy which are set by the individual lenders.8

Conforming types of loans see the following types of requirements to be meet:

The borrower must have very low debt and equity ratio

The borrower must have good credit ratio.

The requirement of money in order to close the loan amount. This is inclusive of

down payment and the cash reserves required for a particular period.

Non -conforming loan are the types of loan who are not required to follow any specific

guidelines. They have not any rigid guidelines to be followed while lending money.

Primary and secondary mortgage market

8 http://www.eandhrealty.com/faqs/The-mortgage-market-and-how-it-works

Mortgage market is divided into two parts as primary mortgage market and secondary

mortgage market. Primary mortgage market refers to a market which provides loans to the

normal public and the company who buys property from the market. The secondary

mortgage market is discovered by the financial institutions.

Many people have a vision that the mortgage market is very much complicated but in fact

the reality is different. The mortgage market is very simple to understand and implement.

By understanding properly one can get a proper information about the lenders available in

the market. The first and most important part is to understand who is actually the person

who will lend the money to you. Two types of lender are available in the market institutional

lenders and private lenders. Generally, the institutional lenders are the commercial banks,

Savings and Loan, credit unions, pension funds and insurance companies. The institutional

lenders provide loan to the borrower on the basis of the credit worthiness of the borrower.

The loans are provided on the basis of the rules and guidelines prescribed. On the other

hand, private lenders are generally individuals, companies and they are not regulated by the

government. As the private lenders are not regulated through any government therefore,

they have a very flexible policy.

Depends on the types of loans

Accordingly, on the basis of above information one now knows who is the lender in the

market and how it works. In a market two types of conventional loans prevailed conforming

loans and non-conforming loans. Conforming type of loans is strictly based on Freddie Mac

policy and offer the very attractive rate of interest to the buyer. Non-conforming loans are

the guidelines and policy which are set by the individual lenders.8

Conforming types of loans see the following types of requirements to be meet:

The borrower must have very low debt and equity ratio

The borrower must have good credit ratio.

The requirement of money in order to close the loan amount. This is inclusive of

down payment and the cash reserves required for a particular period.

Non -conforming loan are the types of loan who are not required to follow any specific

guidelines. They have not any rigid guidelines to be followed while lending money.

Primary and secondary mortgage market

8 http://www.eandhrealty.com/faqs/The-mortgage-market-and-how-it-works

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.