Management Accounting Analysis and Reporting for GKL Group Limited

VerifiedAdded on 2020/10/22

|19

|4560

|278

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on GKL Group Limited, a civil engineering firm. It explores the essential requirements of different management accounting systems, including price optimization, inventory management, and cost accounting. The report details various reporting methods such as budget reports, performance reports, and cost managerial accounting reports, highlighting their benefits in organizational contexts. Furthermore, it delves into cost analysis techniques, specifically marginal and absorption costing, and their application in preparing income statements. The report also examines the advantages and disadvantages of budgetary control tools and compares how companies utilize management accounting to address financial challenges, ultimately contributing to organizational success. The integration of management accounting systems and reporting within the organizational process is emphasized throughout the analysis.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

PART (A)....................................................................................................................................1

Management accounting and essential requirement of different accounting method.................1

Different methods of management accounting reporting............................................................3

Benefits of management accounting systems and their application in organisational context...4

Management accounting system and reporting are integrated within the organisational process

.....................................................................................................................................................5

PART(B).....................................................................................................................................5

Calculate costs using appropriate techniques of

cost analysis to prepare an income statement using marginal and absorption costs..................5

ANNEX(A).................................................................................................................................6

ACTIVITY 2....................................................................................................................................9

PART (A)....................................................................................................................................9

Advantages and disadvantages of different planning tools of budgetary control.......................9

Different planning tools and their application for preparation of budgets................................11

PART(B)...................................................................................................................................12

Comparison of organisations to solve the financial problem with the use of management

accounting system.....................................................................................................................12

Management accounting in solving financial problems and ultimately lead to organizational

success.......................................................................................................................................13

An evaluation of how planning tools for accounting help to solve problems and support

industry with sustainable success..............................................................................................14

CONCLUSION..............................................................................................................................14

REFRENCES.................................................................................................................................15

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

PART (A)....................................................................................................................................1

Management accounting and essential requirement of different accounting method.................1

Different methods of management accounting reporting............................................................3

Benefits of management accounting systems and their application in organisational context...4

Management accounting system and reporting are integrated within the organisational process

.....................................................................................................................................................5

PART(B).....................................................................................................................................5

Calculate costs using appropriate techniques of

cost analysis to prepare an income statement using marginal and absorption costs..................5

ANNEX(A).................................................................................................................................6

ACTIVITY 2....................................................................................................................................9

PART (A)....................................................................................................................................9

Advantages and disadvantages of different planning tools of budgetary control.......................9

Different planning tools and their application for preparation of budgets................................11

PART(B)...................................................................................................................................12

Comparison of organisations to solve the financial problem with the use of management

accounting system.....................................................................................................................12

Management accounting in solving financial problems and ultimately lead to organizational

success.......................................................................................................................................13

An evaluation of how planning tools for accounting help to solve problems and support

industry with sustainable success..............................................................................................14

CONCLUSION..............................................................................................................................14

REFRENCES.................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is considered as a system of accounting that aids in to internal

management of the firms. It involves many types of information such as financial and non

financial. It examine the activities of business in summarised manner (Arroyo, 2012). Herein, it

is crucial to to understand that management accounting is not necessary part of the firms. It

based upon them they required it or not. For this report the chosen company is GKL group

limited which delivers civil engineering projects. Its headquarters is in Peterborough,

Cambridgeshire, UK. The purpose of this report is to describe the management accounting and

necessary requirements of various kinds of management accounting system as well as its

benefits. Different methods utilise for management accounting reporting. Preparation of income

statement by using marginal and absorption costing. Advantage and disadvantages of various

kinds of planning tools utilise for budgetary control. Comparison of how companies are adopting

management accounting system to responds to financial problems are also mentioned in this

report.

ACTIVITY 1

PART (A)

Management accounting and essential requirement of different accounting method

Management accounting system internal part of any organisation which can use to measure and

analysing to their process of the management. The system will provide accurate information on

time to facilitate efforts to control cost and measure productivity. With the help of the system

introducing of new product and identify all rival products after market analysis. It can consist of

different types of techniques and tools that will help to management in decision making process

and improve productivity. In the context of GKL group limited can apply these system in order

to manager all activities in effective manner and increase profitability.

Price optimization system – The particular system treated as a tool of management

accounting which can help to set price structure of their different products and services. It can

analysis the perception of customer regarding to their products and services (Baldvinsdottir,

Mitchel. and Nørreklit, 2013). After that set price which can suitable for customer and company.

It further, set prices of products to get beneficial level in an organisation. The GKL group limited

apply the system to set price of their flats as per market rate. This tool can analysis of price of

1

Management accounting is considered as a system of accounting that aids in to internal

management of the firms. It involves many types of information such as financial and non

financial. It examine the activities of business in summarised manner (Arroyo, 2012). Herein, it

is crucial to to understand that management accounting is not necessary part of the firms. It

based upon them they required it or not. For this report the chosen company is GKL group

limited which delivers civil engineering projects. Its headquarters is in Peterborough,

Cambridgeshire, UK. The purpose of this report is to describe the management accounting and

necessary requirements of various kinds of management accounting system as well as its

benefits. Different methods utilise for management accounting reporting. Preparation of income

statement by using marginal and absorption costing. Advantage and disadvantages of various

kinds of planning tools utilise for budgetary control. Comparison of how companies are adopting

management accounting system to responds to financial problems are also mentioned in this

report.

ACTIVITY 1

PART (A)

Management accounting and essential requirement of different accounting method

Management accounting system internal part of any organisation which can use to measure and

analysing to their process of the management. The system will provide accurate information on

time to facilitate efforts to control cost and measure productivity. With the help of the system

introducing of new product and identify all rival products after market analysis. It can consist of

different types of techniques and tools that will help to management in decision making process

and improve productivity. In the context of GKL group limited can apply these system in order

to manager all activities in effective manner and increase profitability.

Price optimization system – The particular system treated as a tool of management

accounting which can help to set price structure of their different products and services. It can

analysis the perception of customer regarding to their products and services (Baldvinsdottir,

Mitchel. and Nørreklit, 2013). After that set price which can suitable for customer and company.

It further, set prices of products to get beneficial level in an organisation. The GKL group limited

apply the system to set price of their flats as per market rate. This tool can analysis of price of

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

various projects which can conduct by company in present as well as in future. After set prices

they can promote their buildings and attract to more clients.

Inventory Management system – The inventory management system combination of

software and hardware. With the help of this system track movement of goods at each level of

manufacturing. The system can an organisation to know how much quantity need to to raw

material in different process and how many time take to convert into finished goods (Bodie,

2013). It can reduce wastage and proper utilise of goods in production activities. In the context of

GKL group limit, is a constructing company so for different projects need to different types of

materials. These are tracking through inventory management system and time to time provide

detailed information regarding to transfer of goods from warehouse to manufacturing. They use

it in checking the availability of various type of raw material like steel, cement etc.

Cost accounting system – The cost accounting system is a way of predict the total cost

of different products and services to determine the productivity as well as profitability. The

particular accounting system mainly followed by those companies who can work in

manufacturing sector because their rang of work on broad level. There are cost accounting

system can be divided into two parts first one is job order costing system and second one is

process costing system. In the context of GKL group limited can use both system which has been

described below - Job order costing system – It is a kind of cost accounting system which can apply in

reference to different types of products and services. In this system use the job cost sheet,

labour and material to analysis of cash flow of products and services (Burritt,

Schaltegger and Zvezdov, 2014). If any customer give order that time use this system

because it can manage in effective manner and provide all appropriate information. The

GKL group limited applied job order costing system when get many orders from different

customer and helps to proper arrange in reference to earn profit or loss.

Process costing system – This method assigns for the total cost from different units of

output. There are entering various cost regarding to different process after than calculate

sum of total cost of products and services. The system mainly used when work in process

and need to determine cost of further process. The GKL group limited can apply this

system due to predict total cost of their constructing projects at different stage.

2

they can promote their buildings and attract to more clients.

Inventory Management system – The inventory management system combination of

software and hardware. With the help of this system track movement of goods at each level of

manufacturing. The system can an organisation to know how much quantity need to to raw

material in different process and how many time take to convert into finished goods (Bodie,

2013). It can reduce wastage and proper utilise of goods in production activities. In the context of

GKL group limit, is a constructing company so for different projects need to different types of

materials. These are tracking through inventory management system and time to time provide

detailed information regarding to transfer of goods from warehouse to manufacturing. They use

it in checking the availability of various type of raw material like steel, cement etc.

Cost accounting system – The cost accounting system is a way of predict the total cost

of different products and services to determine the productivity as well as profitability. The

particular accounting system mainly followed by those companies who can work in

manufacturing sector because their rang of work on broad level. There are cost accounting

system can be divided into two parts first one is job order costing system and second one is

process costing system. In the context of GKL group limited can use both system which has been

described below - Job order costing system – It is a kind of cost accounting system which can apply in

reference to different types of products and services. In this system use the job cost sheet,

labour and material to analysis of cash flow of products and services (Burritt,

Schaltegger and Zvezdov, 2014). If any customer give order that time use this system

because it can manage in effective manner and provide all appropriate information. The

GKL group limited applied job order costing system when get many orders from different

customer and helps to proper arrange in reference to earn profit or loss.

Process costing system – This method assigns for the total cost from different units of

output. There are entering various cost regarding to different process after than calculate

sum of total cost of products and services. The system mainly used when work in process

and need to determine cost of further process. The GKL group limited can apply this

system due to predict total cost of their constructing projects at different stage.

2

Different methods of management accounting reporting

Management accounting reporting is considered as a methods of reflecting the whole then

business activities to check profit. With the usage of these reports firms can examine the

efficacious level of its various activities. It do not matter that which types of business nature,

these reports perform same for all in order to accomplish objectives. There are different types of

reports which protects enterprise from rivals (Chenhall and Smith, 2015). Moreover, as per these

accounting reports companies makes essential decisions for further plans and policies. GKL

group limited which is an engineering firm prepare various management accounting reports that

are given below:

Budget reports:

These are considered as those reports that are utilised through department of management

in order to compare actual performance with the budgeted targets. Mainly, these reports are

crucial for internal administration of firm. Reports are formulated for specific duration which

may be monthly, quarterly or annually. GKL group limited manager utilise these reports to

compare the exact outcomes with budgeted one. Moreover, this aids them in examining what

types of projects are effective and profitable as well as which are not.

Performance Report:

These are the reports which are formulated to measure the performance of something. It

is very much essential for firm as this assists them to monitor that which activities are

facilitating desired outcomes and which are not. Moreover, project reports perform as per the

comparison of particular activity actual outcomes with standard one (Contrafatto and Burns,

2013). In this respects, this is crucial to ascertain performance measurement standards as due to

the lack of accurate standard level this can be hard to evaluate the performance. GKL group

limited prepare these reports to measure its performance as well as to develop future decisions

about several projects. Within respective firm, this particular report is essential due to its work

nature as well as provided services.

Cost managerial accounting reports:

These types of reports are generally affiliated to calculating the whole cost that incurs in

providing goods and services. It is an efficacious manner to examine the total cost which can be

considered as a base of comparing costs with sold amount. This facilitates a structure to develop

comprehensive investigation of gross cost which obtain and overall revenue gained through

3

Management accounting reporting is considered as a methods of reflecting the whole then

business activities to check profit. With the usage of these reports firms can examine the

efficacious level of its various activities. It do not matter that which types of business nature,

these reports perform same for all in order to accomplish objectives. There are different types of

reports which protects enterprise from rivals (Chenhall and Smith, 2015). Moreover, as per these

accounting reports companies makes essential decisions for further plans and policies. GKL

group limited which is an engineering firm prepare various management accounting reports that

are given below:

Budget reports:

These are considered as those reports that are utilised through department of management

in order to compare actual performance with the budgeted targets. Mainly, these reports are

crucial for internal administration of firm. Reports are formulated for specific duration which

may be monthly, quarterly or annually. GKL group limited manager utilise these reports to

compare the exact outcomes with budgeted one. Moreover, this aids them in examining what

types of projects are effective and profitable as well as which are not.

Performance Report:

These are the reports which are formulated to measure the performance of something. It

is very much essential for firm as this assists them to monitor that which activities are

facilitating desired outcomes and which are not. Moreover, project reports perform as per the

comparison of particular activity actual outcomes with standard one (Contrafatto and Burns,

2013). In this respects, this is crucial to ascertain performance measurement standards as due to

the lack of accurate standard level this can be hard to evaluate the performance. GKL group

limited prepare these reports to measure its performance as well as to develop future decisions

about several projects. Within respective firm, this particular report is essential due to its work

nature as well as provided services.

Cost managerial accounting reports:

These types of reports are generally affiliated to calculating the whole cost that incurs in

providing goods and services. It is an efficacious manner to examine the total cost which can be

considered as a base of comparing costs with sold amount. This facilitates a structure to develop

comprehensive investigation of gross cost which obtain and overall revenue gained through

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

selling of whole units. Herein, in costs are higher than selling one then this would be the loss. If

cost is lesser than sold amount this would be considered as profitable for company. Thus, with

the assistance of it organisations can develop strategic decisions regarding which products or

services are required to be manufacture more in numbers and which one in less amount. Within

GKL group limited, its manager formulate these reports for computing the whole project costs

then examine about loss and profit.

Account receivable ageing report:

These are the reports that are useful in developing lists of that clients who has credit

transaction with organisation. Because of this report company can check how much transactions

are done in credit (Cullen and et. al., 2013). Moreover, this involves the date of proceedings, it

aids firm in listing that how many clients have to pay the amount and who has crossed the

payment date. GKL group limited finance department formulate these reports in order to view

the overall collection into marketplace so that it can develop futuristic plans and policies

consequently. Also, this decrease the stress of remembering credit transactions as they are

involved into enterprise construction projects where credit transactions are performed in large

numbers.

Benefits of management accounting systems and their application in organisational context

In management accounting system includes different types of system which can use by

GKL group to make effective their work. Through these system they can get many benefits there

are mentioned use of different types of system and their application in reference to GKL group

limited.

Price optimization system -

The system can use by an organisation to set price structure for their products and

services to get success for long time. Here in, GKL group determine price of their

different projects which is related to construction. Price optimization system provide a range and thoughts of customer regarding to their

product according to that the company has been set price to attract more customer (Dosch

and Wilson, 2010).

Inventory management system -

4

cost is lesser than sold amount this would be considered as profitable for company. Thus, with

the assistance of it organisations can develop strategic decisions regarding which products or

services are required to be manufacture more in numbers and which one in less amount. Within

GKL group limited, its manager formulate these reports for computing the whole project costs

then examine about loss and profit.

Account receivable ageing report:

These are the reports that are useful in developing lists of that clients who has credit

transaction with organisation. Because of this report company can check how much transactions

are done in credit (Cullen and et. al., 2013). Moreover, this involves the date of proceedings, it

aids firm in listing that how many clients have to pay the amount and who has crossed the

payment date. GKL group limited finance department formulate these reports in order to view

the overall collection into marketplace so that it can develop futuristic plans and policies

consequently. Also, this decrease the stress of remembering credit transactions as they are

involved into enterprise construction projects where credit transactions are performed in large

numbers.

Benefits of management accounting systems and their application in organisational context

In management accounting system includes different types of system which can use by

GKL group to make effective their work. Through these system they can get many benefits there

are mentioned use of different types of system and their application in reference to GKL group

limited.

Price optimization system -

The system can use by an organisation to set price structure for their products and

services to get success for long time. Here in, GKL group determine price of their

different projects which is related to construction. Price optimization system provide a range and thoughts of customer regarding to their

product according to that the company has been set price to attract more customer (Dosch

and Wilson, 2010).

Inventory management system -

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Through the inventory management system can track goods and services at each level of

manufacturing process. The GKL group limited can apply the system and know position

of the goods every time and check availability. The system can provide advantage to reduce wastage and properly utilise of all resources

at each level of constructing.

Cost Accounting System

In this system estimate cost of different projects after that control on different business

activities of GKL group limited.

Through the system company can analysis of the profitability and compare performance

through actual earned income which is incurred cost.

Management accounting system and reporting are integrated within the organisational process

Management accounting system and reports are major part of organisational process

because it can provide help in decision making process. Each accounting system provide benefits

and required information which can help to smoothly run of organisational process and these

reports help to know position of the company (Ewert and Wagenhofer, 2012). It further connect

link between accounting system and reports with organisation process because they are help to

top management to estimate future situations and get success for long time. In reference to GKL

group limited can apply system and reports in their process because in constructing company

need to different types of information and analysis future income and expenses.

PART(B)

Calculate costs using appropriate techniques of

cost analysis to prepare an income statement using marginal and absorption costs

Cost analysis is considered as the procedures of modelling costs in order to support

strategic planning, decision taking as well as cost minimisation. There are various techniques

that are utilise to formulate income statement (Faÿ, Introna and Puyou, 2012). The some

techniques that are used by GKL group limited are mentioned below:

Marginal Costing:

This is considered as a types of cost techniques where marginal cost that are variable cost

is charged to cost units at the time fixed cost for the period of time is totally written off against

5

manufacturing process. The GKL group limited can apply the system and know position

of the goods every time and check availability. The system can provide advantage to reduce wastage and properly utilise of all resources

at each level of constructing.

Cost Accounting System

In this system estimate cost of different projects after that control on different business

activities of GKL group limited.

Through the system company can analysis of the profitability and compare performance

through actual earned income which is incurred cost.

Management accounting system and reporting are integrated within the organisational process

Management accounting system and reports are major part of organisational process

because it can provide help in decision making process. Each accounting system provide benefits

and required information which can help to smoothly run of organisational process and these

reports help to know position of the company (Ewert and Wagenhofer, 2012). It further connect

link between accounting system and reports with organisation process because they are help to

top management to estimate future situations and get success for long time. In reference to GKL

group limited can apply system and reports in their process because in constructing company

need to different types of information and analysis future income and expenses.

PART(B)

Calculate costs using appropriate techniques of

cost analysis to prepare an income statement using marginal and absorption costs

Cost analysis is considered as the procedures of modelling costs in order to support

strategic planning, decision taking as well as cost minimisation. There are various techniques

that are utilise to formulate income statement (Faÿ, Introna and Puyou, 2012). The some

techniques that are used by GKL group limited are mentioned below:

Marginal Costing:

This is considered as a types of cost techniques where marginal cost that are variable cost

is charged to cost units at the time fixed cost for the period of time is totally written off against

5

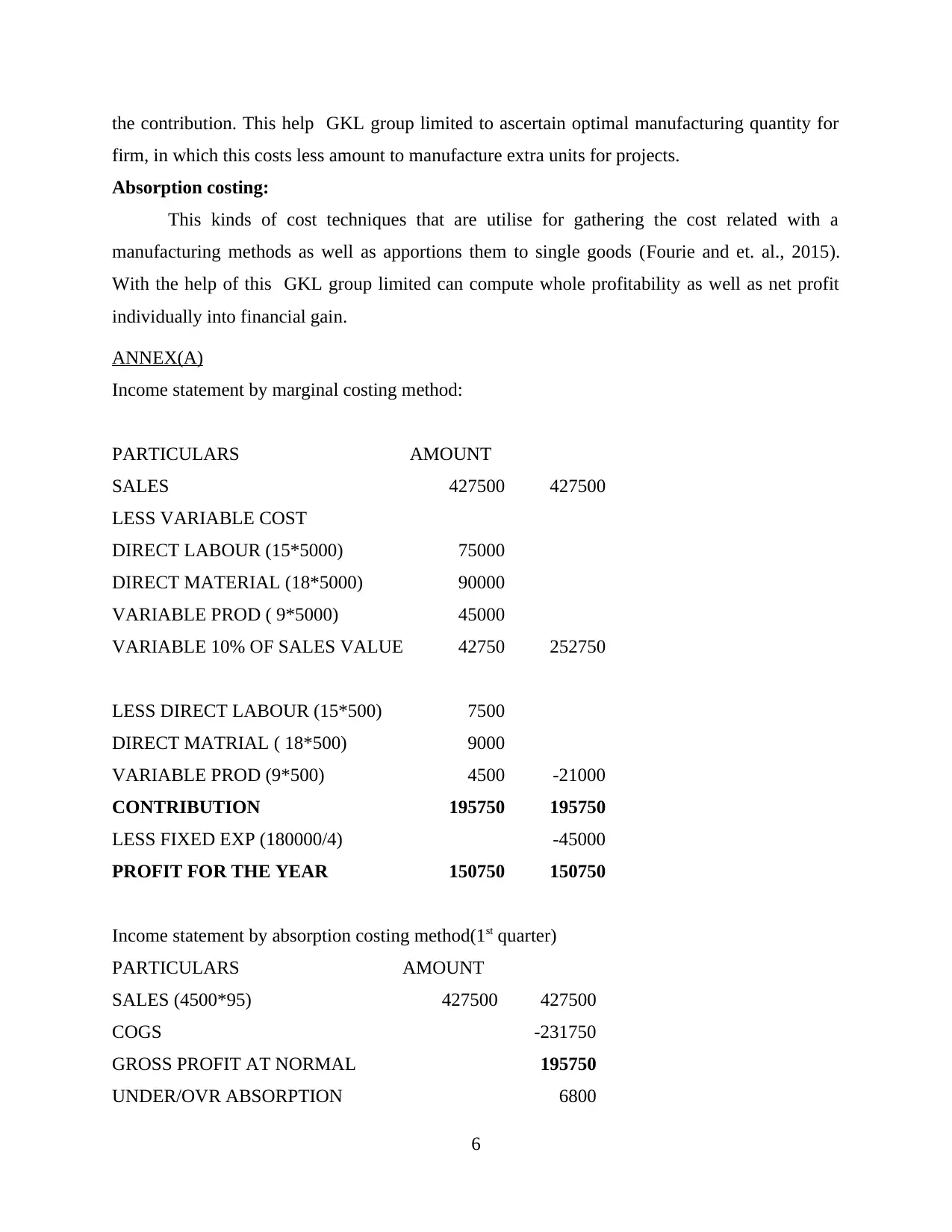

the contribution. This help GKL group limited to ascertain optimal manufacturing quantity for

firm, in which this costs less amount to manufacture extra units for projects.

Absorption costing:

This kinds of cost techniques that are utilise for gathering the cost related with a

manufacturing methods as well as apportions them to single goods (Fourie and et. al., 2015).

With the help of this GKL group limited can compute whole profitability as well as net profit

individually into financial gain.

ANNEX(A)

Income statement by marginal costing method:

PARTICULARS AMOUNT

SALES 427500 427500

LESS VARIABLE COST

DIRECT LABOUR (15*5000) 75000

DIRECT MATERIAL (18*5000) 90000

VARIABLE PROD ( 9*5000) 45000

VARIABLE 10% OF SALES VALUE 42750 252750

LESS DIRECT LABOUR (15*500) 7500

DIRECT MATRIAL ( 18*500) 9000

VARIABLE PROD (9*500) 4500 -21000

CONTRIBUTION 195750 195750

LESS FIXED EXP (180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

Income statement by absorption costing method(1st quarter)

PARTICULARS AMOUNT

SALES (4500*95) 427500 427500

COGS -231750

GROSS PROFIT AT NORMAL 195750

UNDER/OVR ABSORPTION 6800

6

firm, in which this costs less amount to manufacture extra units for projects.

Absorption costing:

This kinds of cost techniques that are utilise for gathering the cost related with a

manufacturing methods as well as apportions them to single goods (Fourie and et. al., 2015).

With the help of this GKL group limited can compute whole profitability as well as net profit

individually into financial gain.

ANNEX(A)

Income statement by marginal costing method:

PARTICULARS AMOUNT

SALES 427500 427500

LESS VARIABLE COST

DIRECT LABOUR (15*5000) 75000

DIRECT MATERIAL (18*5000) 90000

VARIABLE PROD ( 9*5000) 45000

VARIABLE 10% OF SALES VALUE 42750 252750

LESS DIRECT LABOUR (15*500) 7500

DIRECT MATRIAL ( 18*500) 9000

VARIABLE PROD (9*500) 4500 -21000

CONTRIBUTION 195750 195750

LESS FIXED EXP (180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

Income statement by absorption costing method(1st quarter)

PARTICULARS AMOUNT

SALES (4500*95) 427500 427500

COGS -231750

GROSS PROFIT AT NORMAL 195750

UNDER/OVR ABSORPTION 6800

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

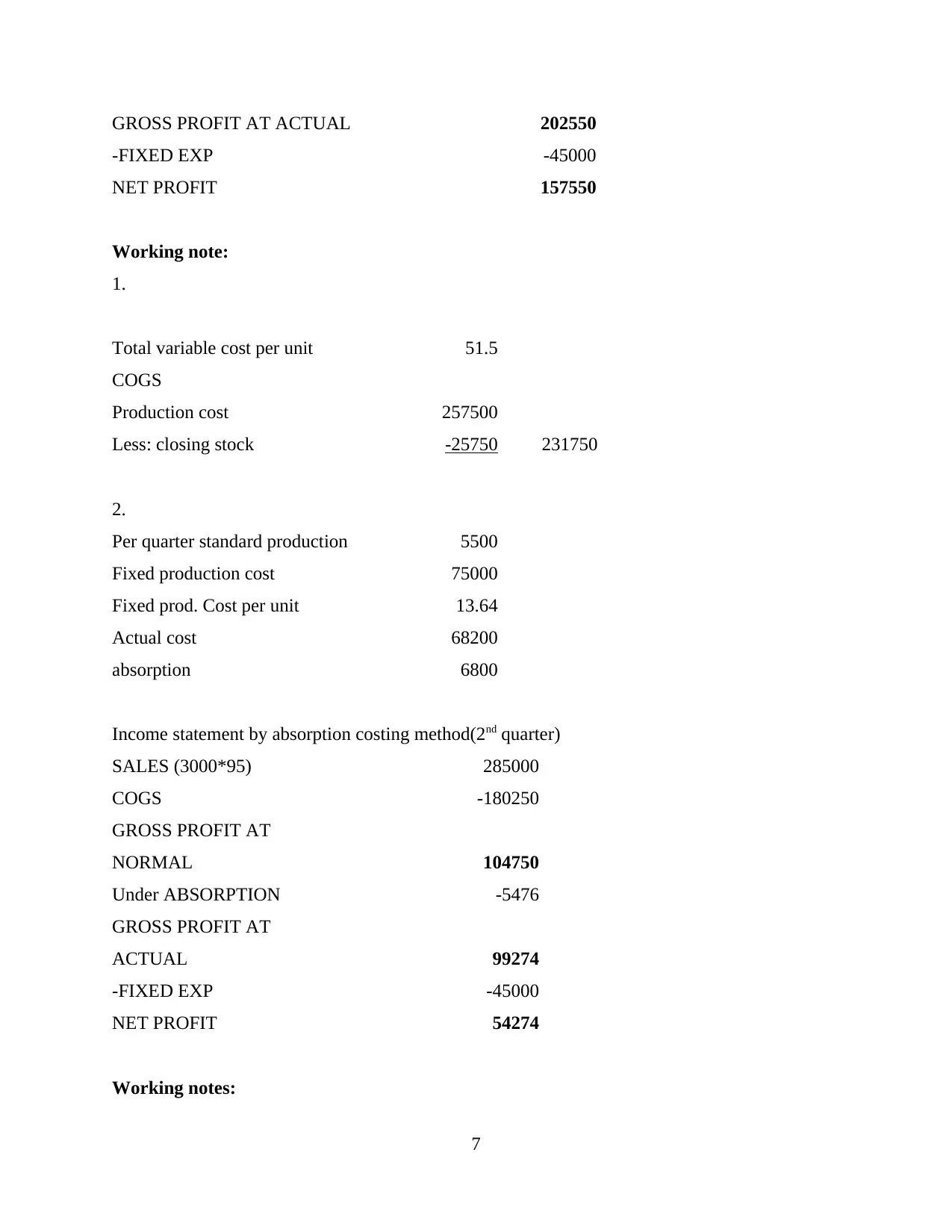

GROSS PROFIT AT ACTUAL 202550

-FIXED EXP -45000

NET PROFIT 157550

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method(2nd quarter)

SALES (3000*95) 285000

COGS -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

-FIXED EXP -45000

NET PROFIT 54274

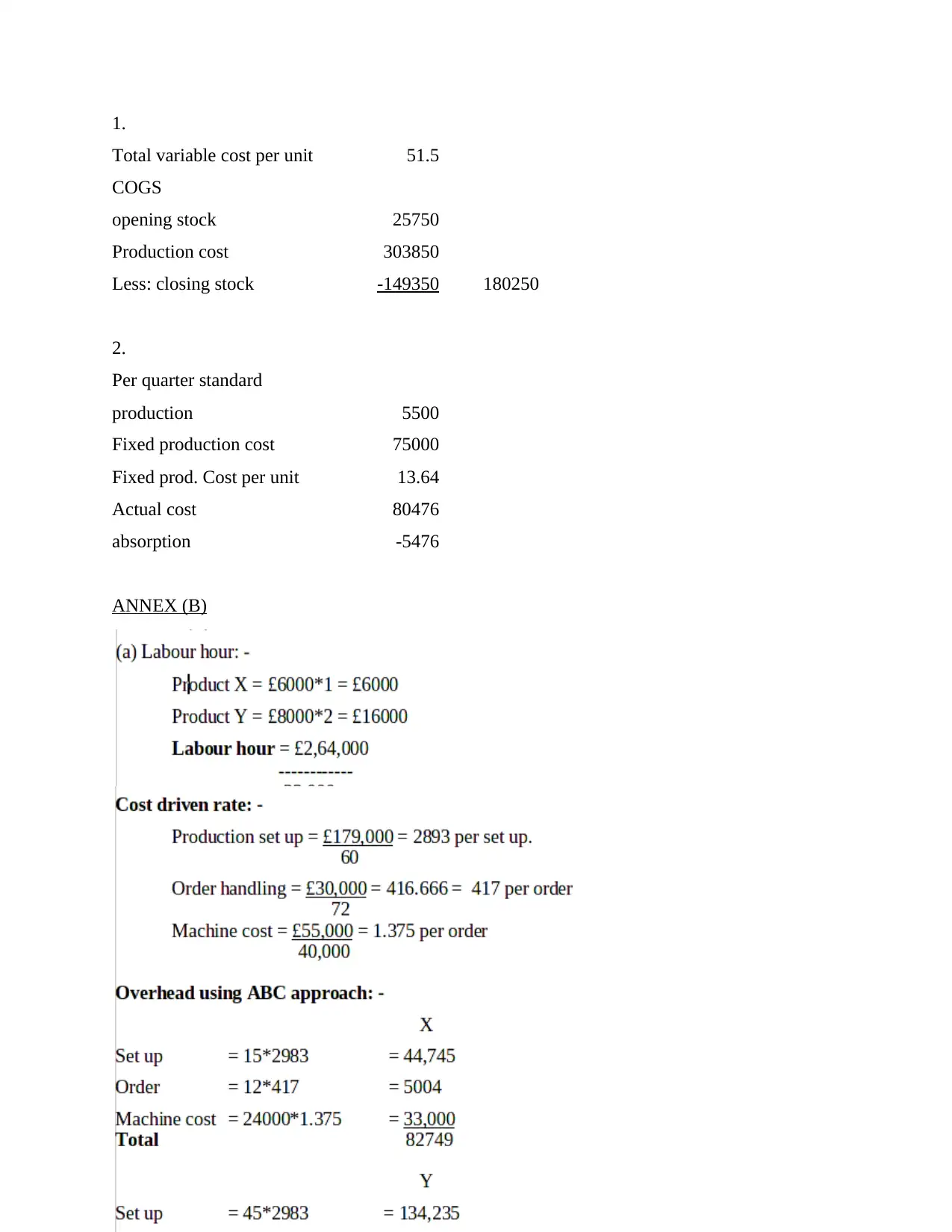

Working notes:

7

-FIXED EXP -45000

NET PROFIT 157550

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method(2nd quarter)

SALES (3000*95) 285000

COGS -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

-FIXED EXP -45000

NET PROFIT 54274

Working notes:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.

Total variable cost per unit 51.5

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

absorption -5476

ANNEX (B)

8

Total variable cost per unit 51.5

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

absorption -5476

ANNEX (B)

8

Interpretation:

On the basis of above revolved problems it have been identified that the two product

named as X and Y, whose rates of labour is £12. also, in this conventional absorption methods is

used so the total overheads into X is £72,000 as well as within y is £192,000. Furthermore, in

Activity based costing approach rates of machine hours for both products are different. As in X

products £24,000 and in y £16,000. also, overheads are also different. Y product consumer

higher expenses than X that are X( £ 82749) and Y(£181,255).

ACTIVITY 2

PART (A)

Advantages and disadvantages of different planning tools of budgetary control

Mainly budget is considered as a formal statement of estimated income and expenses

based upon futuristic objectives as well as plans. Moreover, this predicts the financial situations

and results of organisations (Gates, Nicolas and Walker, 2012). It is generally formulated

through GKL group limited in order to assign capital for various forms of procedures as well as

activities after analysing revenue, expense and last years profitability. Budgetary control is is

refers as a procedures for manager for setting performance and financial goals with budgets,

analyse actual results as well as set performance as per the needs. It is the process which is useful

to face and handle budget that is observed for practices and process. Moreover, it is performed

by monitoring the differences among desired and exact results for taking decision in order to

develop effective budget. In GKL group limited , it is utilise by manager for valuing variances in

budget as well as affiliated that variances with performance to develop efficacious strategies and

policies for minimising those variances.

GKL group limited which is a civil engineering firm have to maintain as well as control

budget figure and various procedures and activities to accomplish sustainability into growth and

also enhance net profit. Company has to build a effectual plan for controlling budget which are

needs to ensure that activities are done efficaciously (Harris and Durden, 2012). Thus, there are

9

On the basis of above revolved problems it have been identified that the two product

named as X and Y, whose rates of labour is £12. also, in this conventional absorption methods is

used so the total overheads into X is £72,000 as well as within y is £192,000. Furthermore, in

Activity based costing approach rates of machine hours for both products are different. As in X

products £24,000 and in y £16,000. also, overheads are also different. Y product consumer

higher expenses than X that are X( £ 82749) and Y(£181,255).

ACTIVITY 2

PART (A)

Advantages and disadvantages of different planning tools of budgetary control

Mainly budget is considered as a formal statement of estimated income and expenses

based upon futuristic objectives as well as plans. Moreover, this predicts the financial situations

and results of organisations (Gates, Nicolas and Walker, 2012). It is generally formulated

through GKL group limited in order to assign capital for various forms of procedures as well as

activities after analysing revenue, expense and last years profitability. Budgetary control is is

refers as a procedures for manager for setting performance and financial goals with budgets,

analyse actual results as well as set performance as per the needs. It is the process which is useful

to face and handle budget that is observed for practices and process. Moreover, it is performed

by monitoring the differences among desired and exact results for taking decision in order to

develop effective budget. In GKL group limited , it is utilise by manager for valuing variances in

budget as well as affiliated that variances with performance to develop efficacious strategies and

policies for minimising those variances.

GKL group limited which is a civil engineering firm have to maintain as well as control

budget figure and various procedures and activities to accomplish sustainability into growth and

also enhance net profit. Company has to build a effectual plan for controlling budget which are

needs to ensure that activities are done efficaciously (Harris and Durden, 2012). Thus, there are

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.