Accounting Method II: Glacier Holdings Ltd Dividend Assignment

VerifiedAdded on 2023/01/11

|10

|2401

|67

Homework Assignment

AI Summary

This assignment report analyzes the dividend of Glacier Holdings Ltd., a public company, focusing on its financial year ending June 30th. The report details the journal entries related to dividend declaration and payment, including entries for the final dividend, preference share dividend, and dividend payment to equity shareholders with the DRP option. It includes a working paper for the dividend calculation, illustrating how the 4% per share dividend was determined, and how the DRP option impacted the distribution of cash versus shares. Furthermore, the report provides a comprehensive list of ordinary shareholders, detailing the number of shares each holds after the dividend payment, considering the DRP option. The report concludes that accounting is the process of formulating different reports of business and journal entries are the basis of accounting as it is the first step which is taken to record the information of day to day transactions of the entity. The assignment also includes calculations related to the DRP option, showing how the number of shares held by shareholders changed after the dividend was issued.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Preparation of the journal’s entries..............................................................................................1

List of ordinary shareholders and the number of shares they each hold after the payment of

final dividend...............................................................................................................................3

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Preparation of the journal’s entries..............................................................................................1

List of ordinary shareholders and the number of shares they each hold after the payment of

final dividend...............................................................................................................................3

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

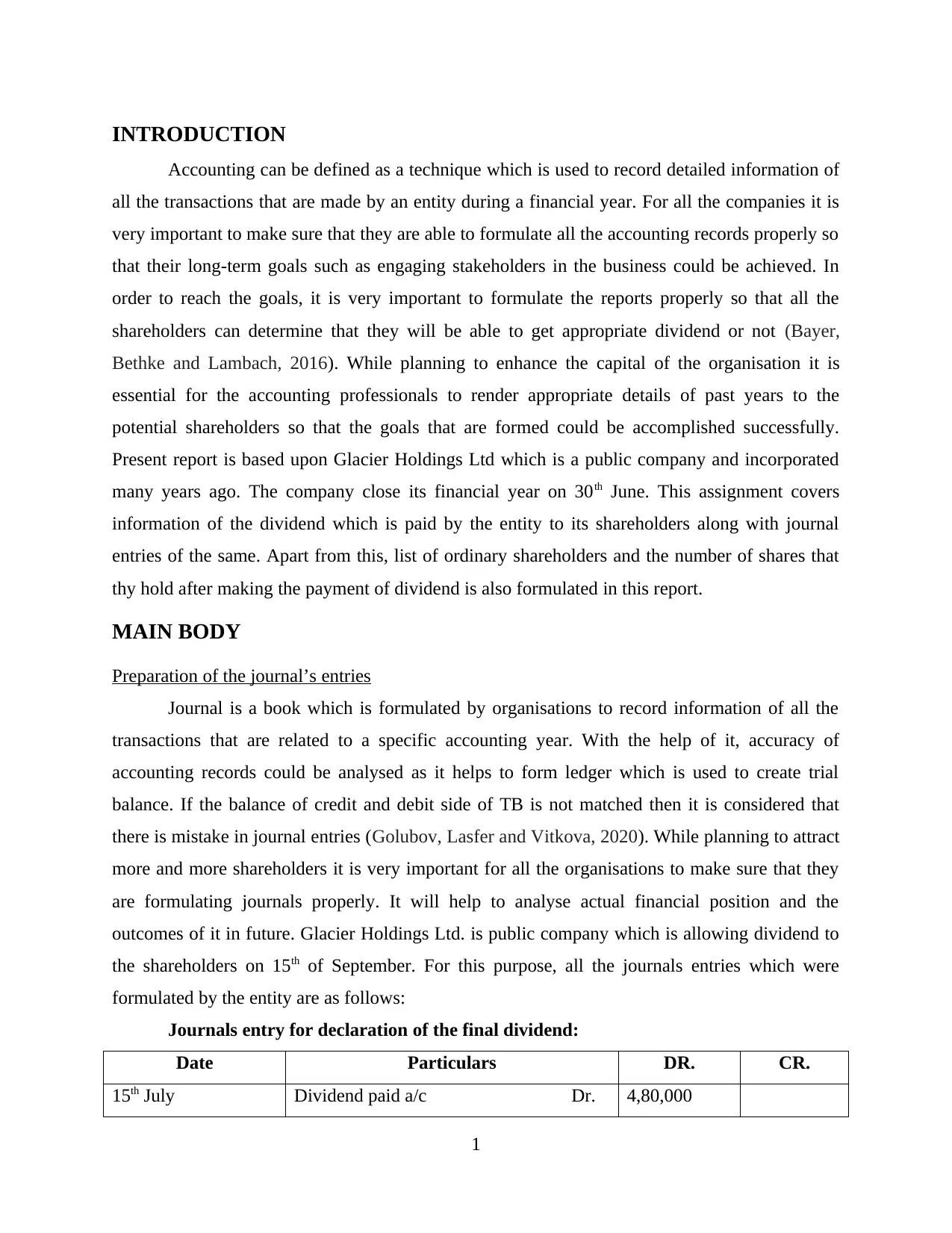

INTRODUCTION

Accounting can be defined as a technique which is used to record detailed information of

all the transactions that are made by an entity during a financial year. For all the companies it is

very important to make sure that they are able to formulate all the accounting records properly so

that their long-term goals such as engaging stakeholders in the business could be achieved. In

order to reach the goals, it is very important to formulate the reports properly so that all the

shareholders can determine that they will be able to get appropriate dividend or not (Bayer,

Bethke and Lambach, 2016). While planning to enhance the capital of the organisation it is

essential for the accounting professionals to render appropriate details of past years to the

potential shareholders so that the goals that are formed could be accomplished successfully.

Present report is based upon Glacier Holdings Ltd which is a public company and incorporated

many years ago. The company close its financial year on 30th June. This assignment covers

information of the dividend which is paid by the entity to its shareholders along with journal

entries of the same. Apart from this, list of ordinary shareholders and the number of shares that

thy hold after making the payment of dividend is also formulated in this report.

MAIN BODY

Preparation of the journal’s entries

Journal is a book which is formulated by organisations to record information of all the

transactions that are related to a specific accounting year. With the help of it, accuracy of

accounting records could be analysed as it helps to form ledger which is used to create trial

balance. If the balance of credit and debit side of TB is not matched then it is considered that

there is mistake in journal entries (Golubov, Lasfer and Vitkova, 2020). While planning to attract

more and more shareholders it is very important for all the organisations to make sure that they

are formulating journals properly. It will help to analyse actual financial position and the

outcomes of it in future. Glacier Holdings Ltd. is public company which is allowing dividend to

the shareholders on 15th of September. For this purpose, all the journals entries which were

formulated by the entity are as follows:

Journals entry for declaration of the final dividend:

Date Particulars DR. CR.

15th July Dividend paid a/c Dr. 4,80,000

1

Accounting can be defined as a technique which is used to record detailed information of

all the transactions that are made by an entity during a financial year. For all the companies it is

very important to make sure that they are able to formulate all the accounting records properly so

that their long-term goals such as engaging stakeholders in the business could be achieved. In

order to reach the goals, it is very important to formulate the reports properly so that all the

shareholders can determine that they will be able to get appropriate dividend or not (Bayer,

Bethke and Lambach, 2016). While planning to enhance the capital of the organisation it is

essential for the accounting professionals to render appropriate details of past years to the

potential shareholders so that the goals that are formed could be accomplished successfully.

Present report is based upon Glacier Holdings Ltd which is a public company and incorporated

many years ago. The company close its financial year on 30th June. This assignment covers

information of the dividend which is paid by the entity to its shareholders along with journal

entries of the same. Apart from this, list of ordinary shareholders and the number of shares that

thy hold after making the payment of dividend is also formulated in this report.

MAIN BODY

Preparation of the journal’s entries

Journal is a book which is formulated by organisations to record information of all the

transactions that are related to a specific accounting year. With the help of it, accuracy of

accounting records could be analysed as it helps to form ledger which is used to create trial

balance. If the balance of credit and debit side of TB is not matched then it is considered that

there is mistake in journal entries (Golubov, Lasfer and Vitkova, 2020). While planning to attract

more and more shareholders it is very important for all the organisations to make sure that they

are formulating journals properly. It will help to analyse actual financial position and the

outcomes of it in future. Glacier Holdings Ltd. is public company which is allowing dividend to

the shareholders on 15th of September. For this purpose, all the journals entries which were

formulated by the entity are as follows:

Journals entry for declaration of the final dividend:

Date Particulars DR. CR.

15th July Dividend paid a/c Dr. 4,80,000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

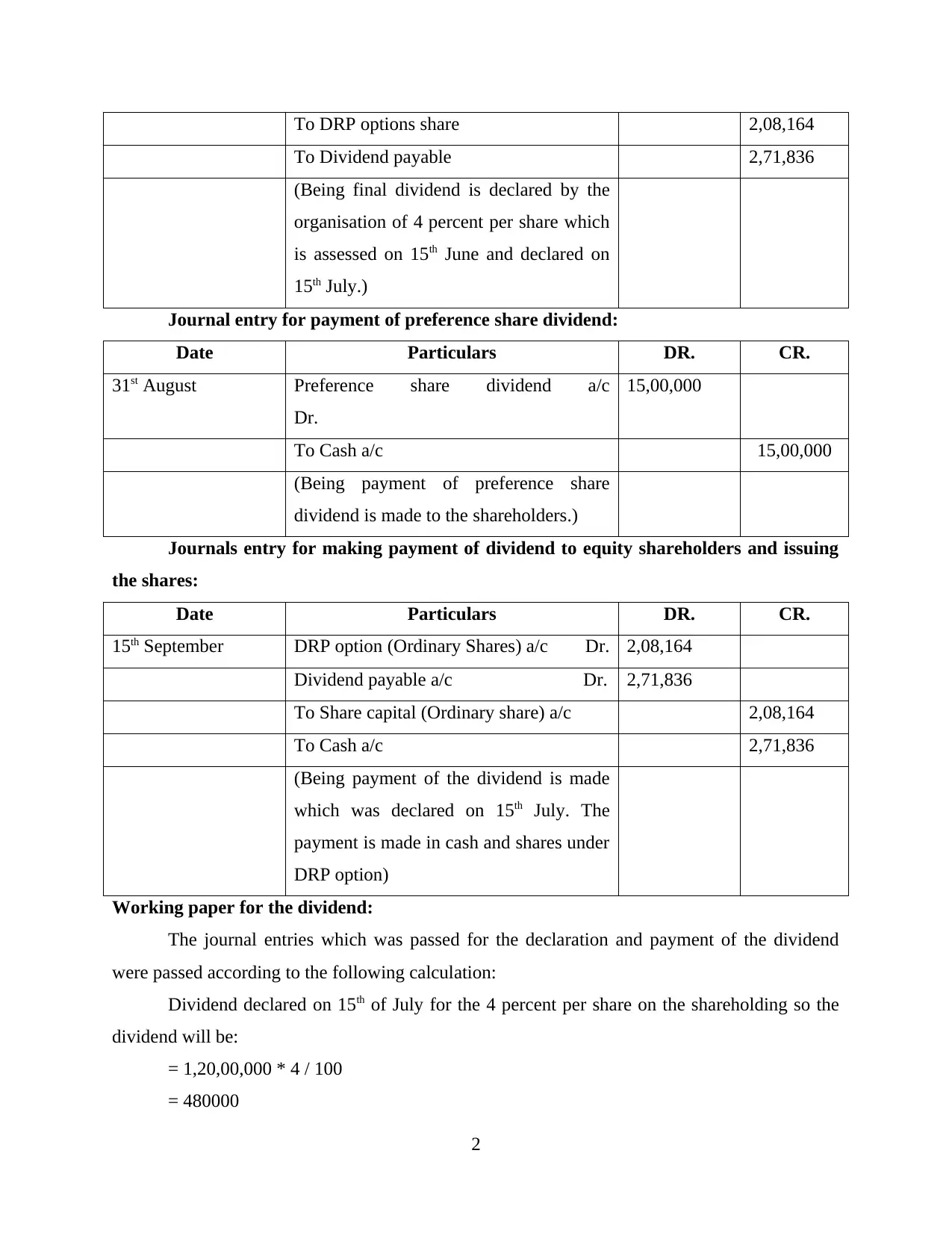

To DRP options share 2,08,164

To Dividend payable 2,71,836

(Being final dividend is declared by the

organisation of 4 percent per share which

is assessed on 15th June and declared on

15th July.)

Journal entry for payment of preference share dividend:

Date Particulars DR. CR.

31st August Preference share dividend a/c

Dr.

15,00,000

To Cash a/c 15,00,000

(Being payment of preference share

dividend is made to the shareholders.)

Journals entry for making payment of dividend to equity shareholders and issuing

the shares:

Date Particulars DR. CR.

15th September DRP option (Ordinary Shares) a/c Dr. 2,08,164

Dividend payable a/c Dr. 2,71,836

To Share capital (Ordinary share) a/c 2,08,164

To Cash a/c 2,71,836

(Being payment of the dividend is made

which was declared on 15th July. The

payment is made in cash and shares under

DRP option)

Working paper for the dividend:

The journal entries which was passed for the declaration and payment of the dividend

were passed according to the following calculation:

Dividend declared on 15th of July for the 4 percent per share on the shareholding so the

dividend will be:

= 1,20,00,000 * 4 / 100

= 480000

2

To Dividend payable 2,71,836

(Being final dividend is declared by the

organisation of 4 percent per share which

is assessed on 15th June and declared on

15th July.)

Journal entry for payment of preference share dividend:

Date Particulars DR. CR.

31st August Preference share dividend a/c

Dr.

15,00,000

To Cash a/c 15,00,000

(Being payment of preference share

dividend is made to the shareholders.)

Journals entry for making payment of dividend to equity shareholders and issuing

the shares:

Date Particulars DR. CR.

15th September DRP option (Ordinary Shares) a/c Dr. 2,08,164

Dividend payable a/c Dr. 2,71,836

To Share capital (Ordinary share) a/c 2,08,164

To Cash a/c 2,71,836

(Being payment of the dividend is made

which was declared on 15th July. The

payment is made in cash and shares under

DRP option)

Working paper for the dividend:

The journal entries which was passed for the declaration and payment of the dividend

were passed according to the following calculation:

Dividend declared on 15th of July for the 4 percent per share on the shareholding so the

dividend will be:

= 1,20,00,000 * 4 / 100

= 480000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The entity provided an option of DRP to all the shareholders and they can take shares

rather than cash as dividend. At 15th of July some of them selected this option and the shares for

the plan were 52,04,100. The dividend for the same shares which will be issues as nore shares

will be as follows:

= 52,04,100 * 4 / 100

= 2,08,164

As 52,04,100 shares were subject to the DRP option and the remaining 67,95,900 shares

were not subject to the same so the cash dividend which will be issued for the holders of these

shares will be as follows:

= 67,95,900 * 4 / 100

= 2,71,836

From the above calculations it has been determined that the cash dividend which will be

issued to the shareholders who have not adopted the DRP option will be 2,71,836 dollars. On the

other hand, all the share holders who have adopted the option of DRP will be issues dividend on

2,08,164 dollars in the form of cash (Huang and Sharif, 2017).

List of ordinary shareholders and the number of shares they each hold after the payment of final

dividend

Dividend is a type of return which is offered by the organisation to the shareholders so that

their involvement in the business could be increased. For all the business entities it is very

important to provide dividend to the shareholders because if they will not get any return on their

funds then it will leave negative impact upon their engagement. In order to keep them involved

in the business and maintain their interest. There are different types of dividends that are

provided by the enterprises (Jagannathan and Liu, 2019). It could be in the form on cash or

shares. Glacier Holding Ltd provided an option of DRP to all the shareholders in which they can

take shares rather than cash dividend.

It is very beneficial for the shareholders as by adopting this option they can increase their

capital in the entity and their power of decision making. It is totally up to the shareholders that

they want to select this option or not (Jagannathan, Liu and Zhang, 2019). The company will

only allocate shares to the shareholders who have agreed to the DRP option.

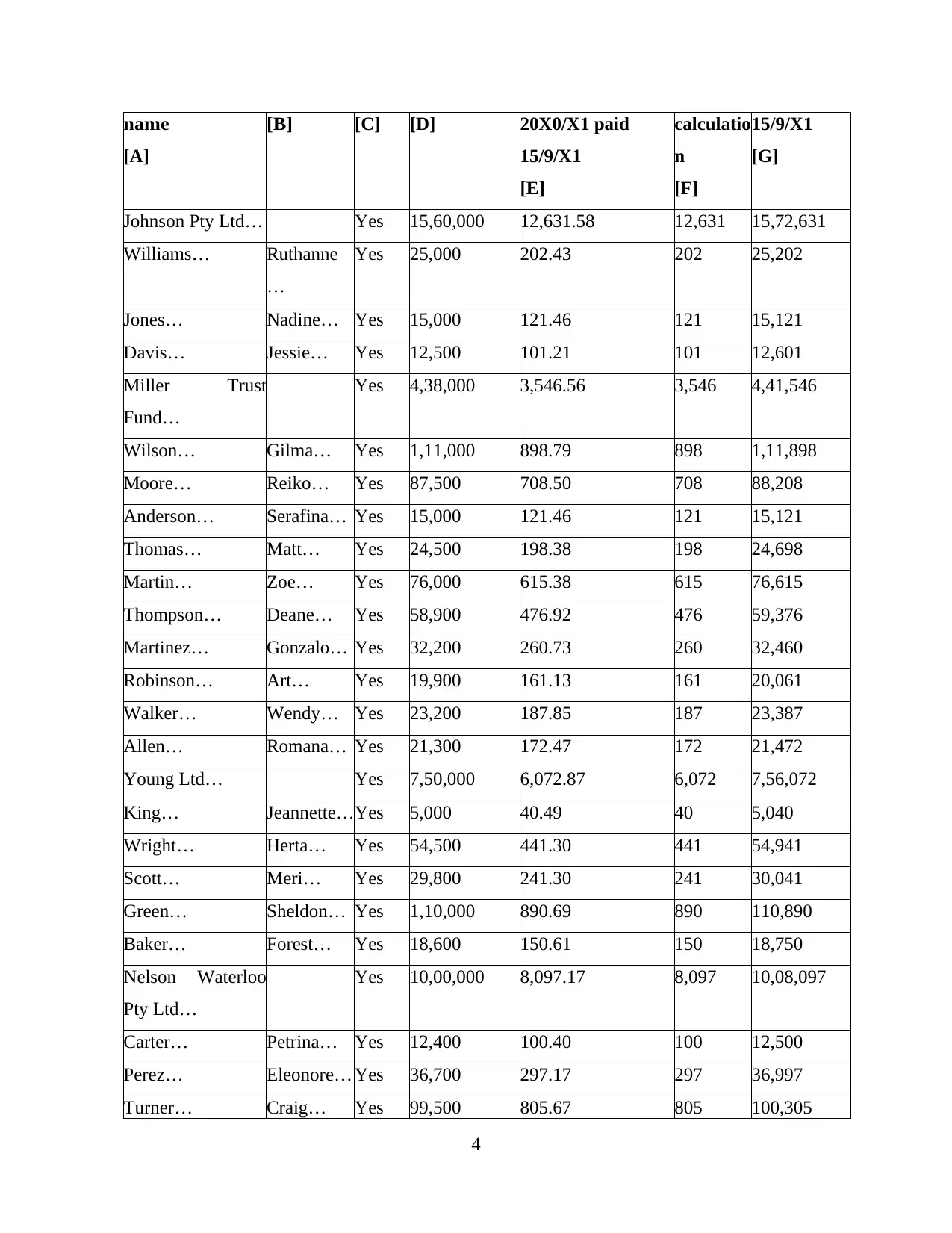

Family

name/Corporate

First

Name

DRP 1/7/20X1 DRP calculation

on final dividend

Roundin

g of

Share

balance

3

rather than cash as dividend. At 15th of July some of them selected this option and the shares for

the plan were 52,04,100. The dividend for the same shares which will be issues as nore shares

will be as follows:

= 52,04,100 * 4 / 100

= 2,08,164

As 52,04,100 shares were subject to the DRP option and the remaining 67,95,900 shares

were not subject to the same so the cash dividend which will be issued for the holders of these

shares will be as follows:

= 67,95,900 * 4 / 100

= 2,71,836

From the above calculations it has been determined that the cash dividend which will be

issued to the shareholders who have not adopted the DRP option will be 2,71,836 dollars. On the

other hand, all the share holders who have adopted the option of DRP will be issues dividend on

2,08,164 dollars in the form of cash (Huang and Sharif, 2017).

List of ordinary shareholders and the number of shares they each hold after the payment of final

dividend

Dividend is a type of return which is offered by the organisation to the shareholders so that

their involvement in the business could be increased. For all the business entities it is very

important to provide dividend to the shareholders because if they will not get any return on their

funds then it will leave negative impact upon their engagement. In order to keep them involved

in the business and maintain their interest. There are different types of dividends that are

provided by the enterprises (Jagannathan and Liu, 2019). It could be in the form on cash or

shares. Glacier Holding Ltd provided an option of DRP to all the shareholders in which they can

take shares rather than cash dividend.

It is very beneficial for the shareholders as by adopting this option they can increase their

capital in the entity and their power of decision making. It is totally up to the shareholders that

they want to select this option or not (Jagannathan, Liu and Zhang, 2019). The company will

only allocate shares to the shareholders who have agreed to the DRP option.

Family

name/Corporate

First

Name

DRP 1/7/20X1 DRP calculation

on final dividend

Roundin

g of

Share

balance

3

name

[A]

[B] [C] [D] 20X0/X1 paid

15/9/X1

[E]

calculatio

n

[F]

15/9/X1

[G]

Johnson Pty Ltd… Yes 15,60,000 12,631.58 12,631 15,72,631

Williams… Ruthanne

…

Yes 25,000 202.43 202 25,202

Jones… Nadine… Yes 15,000 121.46 121 15,121

Davis… Jessie… Yes 12,500 101.21 101 12,601

Miller Trust

Fund…

Yes 4,38,000 3,546.56 3,546 4,41,546

Wilson… Gilma… Yes 1,11,000 898.79 898 1,11,898

Moore… Reiko… Yes 87,500 708.50 708 88,208

Anderson… Serafina… Yes 15,000 121.46 121 15,121

Thomas… Matt… Yes 24,500 198.38 198 24,698

Martin… Zoe… Yes 76,000 615.38 615 76,615

Thompson… Deane… Yes 58,900 476.92 476 59,376

Martinez… Gonzalo… Yes 32,200 260.73 260 32,460

Robinson… Art… Yes 19,900 161.13 161 20,061

Walker… Wendy… Yes 23,200 187.85 187 23,387

Allen… Romana… Yes 21,300 172.47 172 21,472

Young Ltd… Yes 7,50,000 6,072.87 6,072 7,56,072

King… Jeannette…Yes 5,000 40.49 40 5,040

Wright… Herta… Yes 54,500 441.30 441 54,941

Scott… Meri… Yes 29,800 241.30 241 30,041

Green… Sheldon… Yes 1,10,000 890.69 890 110,890

Baker… Forest… Yes 18,600 150.61 150 18,750

Nelson Waterloo

Pty Ltd…

Yes 10,00,000 8,097.17 8,097 10,08,097

Carter… Petrina… Yes 12,400 100.40 100 12,500

Perez… Eleonore… Yes 36,700 297.17 297 36,997

Turner… Craig… Yes 99,500 805.67 805 100,305

4

[A]

[B] [C] [D] 20X0/X1 paid

15/9/X1

[E]

calculatio

n

[F]

15/9/X1

[G]

Johnson Pty Ltd… Yes 15,60,000 12,631.58 12,631 15,72,631

Williams… Ruthanne

…

Yes 25,000 202.43 202 25,202

Jones… Nadine… Yes 15,000 121.46 121 15,121

Davis… Jessie… Yes 12,500 101.21 101 12,601

Miller Trust

Fund…

Yes 4,38,000 3,546.56 3,546 4,41,546

Wilson… Gilma… Yes 1,11,000 898.79 898 1,11,898

Moore… Reiko… Yes 87,500 708.50 708 88,208

Anderson… Serafina… Yes 15,000 121.46 121 15,121

Thomas… Matt… Yes 24,500 198.38 198 24,698

Martin… Zoe… Yes 76,000 615.38 615 76,615

Thompson… Deane… Yes 58,900 476.92 476 59,376

Martinez… Gonzalo… Yes 32,200 260.73 260 32,460

Robinson… Art… Yes 19,900 161.13 161 20,061

Walker… Wendy… Yes 23,200 187.85 187 23,387

Allen… Romana… Yes 21,300 172.47 172 21,472

Young Ltd… Yes 7,50,000 6,072.87 6,072 7,56,072

King… Jeannette…Yes 5,000 40.49 40 5,040

Wright… Herta… Yes 54,500 441.30 441 54,941

Scott… Meri… Yes 29,800 241.30 241 30,041

Green… Sheldon… Yes 1,10,000 890.69 890 110,890

Baker… Forest… Yes 18,600 150.61 150 18,750

Nelson Waterloo

Pty Ltd…

Yes 10,00,000 8,097.17 8,097 10,08,097

Carter… Petrina… Yes 12,400 100.40 100 12,500

Perez… Eleonore… Yes 36,700 297.17 297 36,997

Turner… Craig… Yes 99,500 805.67 805 100,305

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

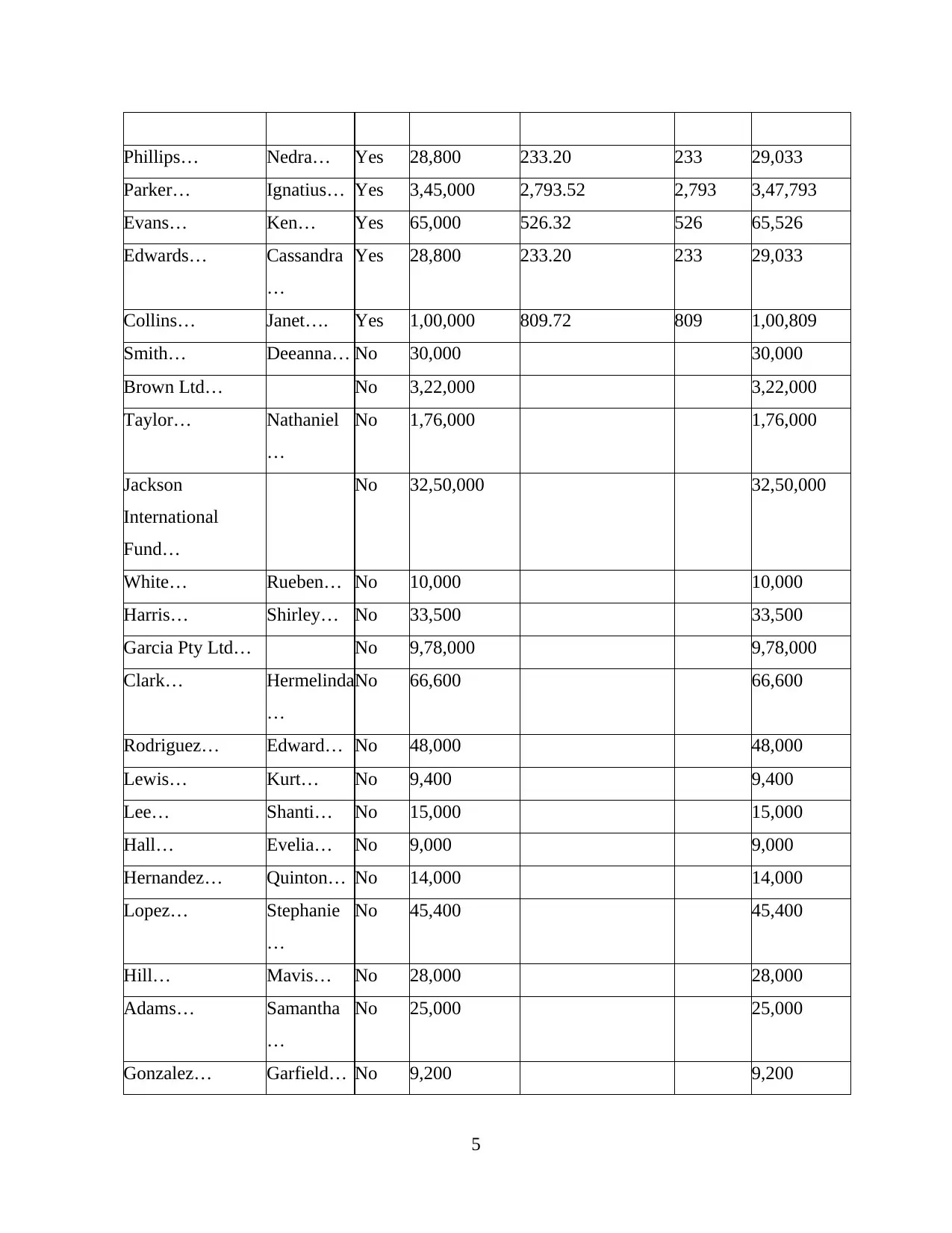

Phillips… Nedra… Yes 28,800 233.20 233 29,033

Parker… Ignatius… Yes 3,45,000 2,793.52 2,793 3,47,793

Evans… Ken… Yes 65,000 526.32 526 65,526

Edwards… Cassandra

…

Yes 28,800 233.20 233 29,033

Collins… Janet…. Yes 1,00,000 809.72 809 1,00,809

Smith… Deeanna… No 30,000 30,000

Brown Ltd… No 3,22,000 3,22,000

Taylor… Nathaniel

…

No 1,76,000 1,76,000

Jackson

International

Fund…

No 32,50,000 32,50,000

White… Rueben… No 10,000 10,000

Harris… Shirley… No 33,500 33,500

Garcia Pty Ltd… No 9,78,000 9,78,000

Clark… Hermelinda

…

No 66,600 66,600

Rodriguez… Edward… No 48,000 48,000

Lewis… Kurt… No 9,400 9,400

Lee… Shanti… No 15,000 15,000

Hall… Evelia… No 9,000 9,000

Hernandez… Quinton… No 14,000 14,000

Lopez… Stephanie

…

No 45,400 45,400

Hill… Mavis… No 28,000 28,000

Adams… Samantha

…

No 25,000 25,000

Gonzalez… Garfield… No 9,200 9,200

5

Parker… Ignatius… Yes 3,45,000 2,793.52 2,793 3,47,793

Evans… Ken… Yes 65,000 526.32 526 65,526

Edwards… Cassandra

…

Yes 28,800 233.20 233 29,033

Collins… Janet…. Yes 1,00,000 809.72 809 1,00,809

Smith… Deeanna… No 30,000 30,000

Brown Ltd… No 3,22,000 3,22,000

Taylor… Nathaniel

…

No 1,76,000 1,76,000

Jackson

International

Fund…

No 32,50,000 32,50,000

White… Rueben… No 10,000 10,000

Harris… Shirley… No 33,500 33,500

Garcia Pty Ltd… No 9,78,000 9,78,000

Clark… Hermelinda

…

No 66,600 66,600

Rodriguez… Edward… No 48,000 48,000

Lewis… Kurt… No 9,400 9,400

Lee… Shanti… No 15,000 15,000

Hall… Evelia… No 9,000 9,000

Hernandez… Quinton… No 14,000 14,000

Lopez… Stephanie

…

No 45,400 45,400

Hill… Mavis… No 28,000 28,000

Adams… Samantha

…

No 25,000 25,000

Gonzalez… Garfield… No 9,200 9,200

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

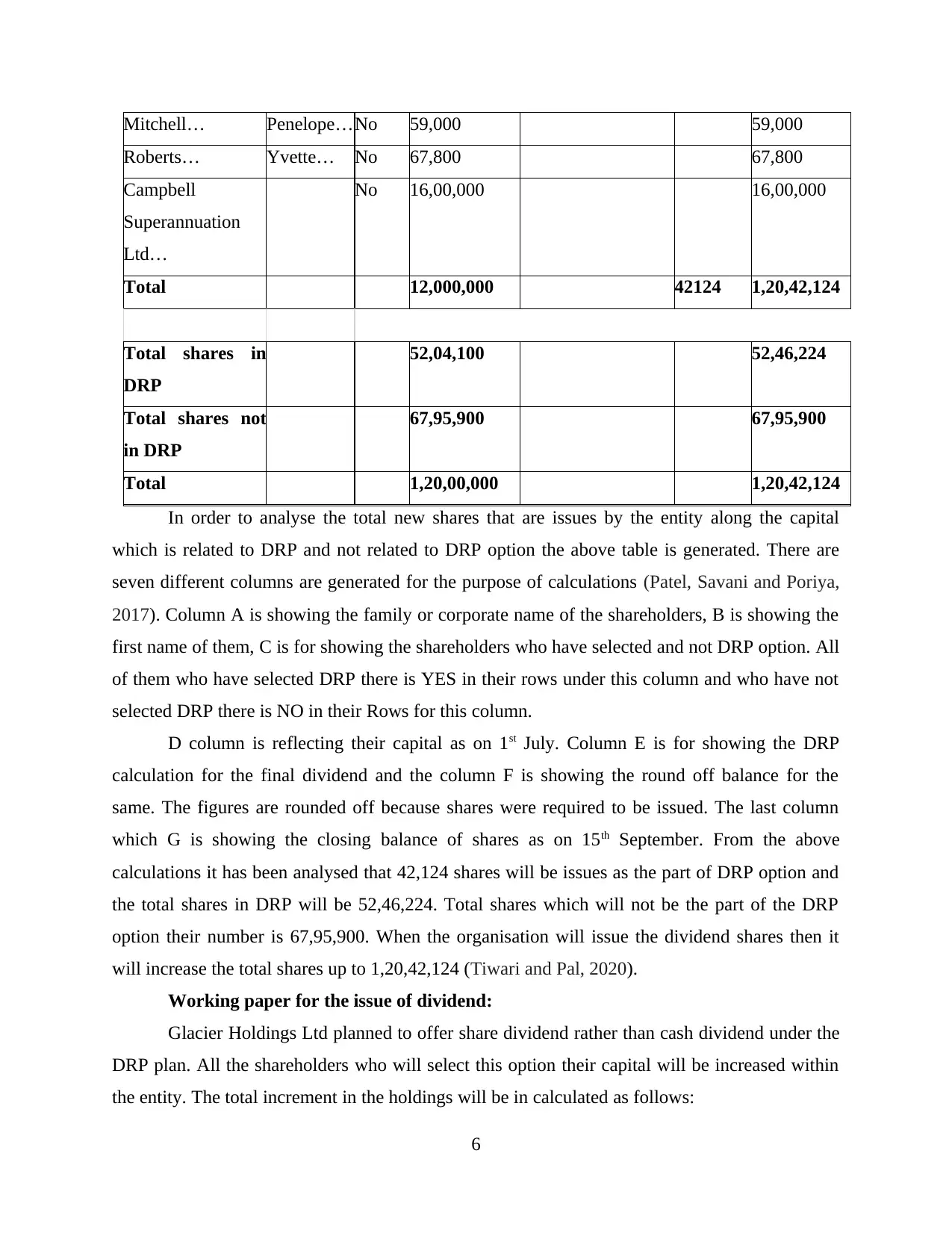

Mitchell… Penelope…No 59,000 59,000

Roberts… Yvette… No 67,800 67,800

Campbell

Superannuation

Ltd…

No 16,00,000 16,00,000

Total 12,000,000 42124 1,20,42,124

Total shares in

DRP

52,04,100 52,46,224

Total shares not

in DRP

67,95,900 67,95,900

Total 1,20,00,000 1,20,42,124

In order to analyse the total new shares that are issues by the entity along the capital

which is related to DRP and not related to DRP option the above table is generated. There are

seven different columns are generated for the purpose of calculations (Patel, Savani and Poriya,

2017). Column A is showing the family or corporate name of the shareholders, B is showing the

first name of them, C is for showing the shareholders who have selected and not DRP option. All

of them who have selected DRP there is YES in their rows under this column and who have not

selected DRP there is NO in their Rows for this column.

D column is reflecting their capital as on 1st July. Column E is for showing the DRP

calculation for the final dividend and the column F is showing the round off balance for the

same. The figures are rounded off because shares were required to be issued. The last column

which G is showing the closing balance of shares as on 15th September. From the above

calculations it has been analysed that 42,124 shares will be issues as the part of DRP option and

the total shares in DRP will be 52,46,224. Total shares which will not be the part of the DRP

option their number is 67,95,900. When the organisation will issue the dividend shares then it

will increase the total shares up to 1,20,42,124 (Tiwari and Pal, 2020).

Working paper for the issue of dividend:

Glacier Holdings Ltd planned to offer share dividend rather than cash dividend under the

DRP plan. All the shareholders who will select this option their capital will be increased within

the entity. The total increment in the holdings will be in calculated as follows:

6

Roberts… Yvette… No 67,800 67,800

Campbell

Superannuation

Ltd…

No 16,00,000 16,00,000

Total 12,000,000 42124 1,20,42,124

Total shares in

DRP

52,04,100 52,46,224

Total shares not

in DRP

67,95,900 67,95,900

Total 1,20,00,000 1,20,42,124

In order to analyse the total new shares that are issues by the entity along the capital

which is related to DRP and not related to DRP option the above table is generated. There are

seven different columns are generated for the purpose of calculations (Patel, Savani and Poriya,

2017). Column A is showing the family or corporate name of the shareholders, B is showing the

first name of them, C is for showing the shareholders who have selected and not DRP option. All

of them who have selected DRP there is YES in their rows under this column and who have not

selected DRP there is NO in their Rows for this column.

D column is reflecting their capital as on 1st July. Column E is for showing the DRP

calculation for the final dividend and the column F is showing the round off balance for the

same. The figures are rounded off because shares were required to be issued. The last column

which G is showing the closing balance of shares as on 15th September. From the above

calculations it has been analysed that 42,124 shares will be issues as the part of DRP option and

the total shares in DRP will be 52,46,224. Total shares which will not be the part of the DRP

option their number is 67,95,900. When the organisation will issue the dividend shares then it

will increase the total shares up to 1,20,42,124 (Tiwari and Pal, 2020).

Working paper for the issue of dividend:

Glacier Holdings Ltd planned to offer share dividend rather than cash dividend under the

DRP plan. All the shareholders who will select this option their capital will be increased within

the entity. The total increment in the holdings will be in calculated as follows:

6

= Shareholding * 0.04 / (5.20 * 095)

In the above formula 0.04 is the dividend rate, 5.20 is the share price as on 15th July, 0.95

is the share issues at 95% of the share price. It is calculated as follows:

= 5.20 * 0.95

= 4.94

The total increment in the holdings will be added to the existing capital of the

shareholders (Ying and Bowen, 2017). After implementation of it the aggregated capital for the

shareholders will be as follows:

Total number of shares of shareholders who have selected DRP = 52,46,224

Total number of shares of shareholders who have not selected the DRP option =

67,95,900

Total shares at 15th September = 1,20,42,124

CONCLUSION

From the above project report, it has been concluded that accounting is the process of

formulating different reports of business. Main purpose of creating them is to keep detailed

information of all the transactions which have taken place during the accounting year. Journal

entries are considered as the basis of accounting as it is the first step which is taken to record the

information of day to day transactions of the entity. All the organisations allow dividend to the

shareholders on their capital. Sometime companies provide them option of taking cash or shares

as the dividend. It is beneficial for the enterprise as well as the shareholders. With the help of it,

entity can save monetary resources to meet the future obligations apart from the holders can

increase their holding with the entity. It will help them to enhance their power of decision

making for the organisation.

7

In the above formula 0.04 is the dividend rate, 5.20 is the share price as on 15th July, 0.95

is the share issues at 95% of the share price. It is calculated as follows:

= 5.20 * 0.95

= 4.94

The total increment in the holdings will be added to the existing capital of the

shareholders (Ying and Bowen, 2017). After implementation of it the aggregated capital for the

shareholders will be as follows:

Total number of shares of shareholders who have selected DRP = 52,46,224

Total number of shares of shareholders who have not selected the DRP option =

67,95,900

Total shares at 15th September = 1,20,42,124

CONCLUSION

From the above project report, it has been concluded that accounting is the process of

formulating different reports of business. Main purpose of creating them is to keep detailed

information of all the transactions which have taken place during the accounting year. Journal

entries are considered as the basis of accounting as it is the first step which is taken to record the

information of day to day transactions of the entity. All the organisations allow dividend to the

shareholders on their capital. Sometime companies provide them option of taking cash or shares

as the dividend. It is beneficial for the enterprise as well as the shareholders. With the help of it,

entity can save monetary resources to meet the future obligations apart from the holders can

increase their holding with the entity. It will help them to enhance their power of decision

making for the organisation.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Bayer, M., Bethke, F. S. and Lambach, D., 2016. The democratic dividend of nonviolent

resistance. Journal of Peace Research. 53(6). pp.758-771.

Golubov, A., Lasfer, M. and Vitkova, V., 2020. Active catering to dividend clienteles: Evidence

from takeovers. Journal of Financial Economics.

Huang, Y. and Sharif, N., 2017. From ‘labour dividend’to ‘robot dividend’: Technological

change and workers’ power in South China. Agrarian South: Journal of Political

Economy. 6(1). pp.53-78.

Jagannathan, R. and Liu, B., 2019. Dividend dynamics, learning, and expected stock index

returns. The Journal of Finance. 74(1). pp.401-448.

Jagannathan, R., Liu, B. and Zhang, J., 2019. Corrigendum for Dividend Dynamics, Learning,

and Expected Stock Index Returns (The Journal of Finance,(2019). 74. 1,(401-448),

10.1111/jofi. 12731). Journal of Finance. 74(4). pp.2107-2116.

Patel, P., Savani, J. and Poriya, N., 2017. Semi-Strong Form of Market Efficiency for Dividend

and Bonus Announcements: An Empirical Study of India Stock Markets. ANVESHAK-

International Journal of Management. 6(1). pp.108-121.

Tiwari, S. and Pal, D., 2020. DIVIDEND POLICY DECISIONS AND SHARE PRICES

RELATIONSHIP. Finance & Accounting Research Journal. 2(2). pp.76-81.

Ying, W. and Bowen, D., 2017. The Aging Population and the Second Population Dividend:

Empirical Evidence from 18 Aging Nations. Finance & Economics. (8). p.7.

8

Books and Journals:

Bayer, M., Bethke, F. S. and Lambach, D., 2016. The democratic dividend of nonviolent

resistance. Journal of Peace Research. 53(6). pp.758-771.

Golubov, A., Lasfer, M. and Vitkova, V., 2020. Active catering to dividend clienteles: Evidence

from takeovers. Journal of Financial Economics.

Huang, Y. and Sharif, N., 2017. From ‘labour dividend’to ‘robot dividend’: Technological

change and workers’ power in South China. Agrarian South: Journal of Political

Economy. 6(1). pp.53-78.

Jagannathan, R. and Liu, B., 2019. Dividend dynamics, learning, and expected stock index

returns. The Journal of Finance. 74(1). pp.401-448.

Jagannathan, R., Liu, B. and Zhang, J., 2019. Corrigendum for Dividend Dynamics, Learning,

and Expected Stock Index Returns (The Journal of Finance,(2019). 74. 1,(401-448),

10.1111/jofi. 12731). Journal of Finance. 74(4). pp.2107-2116.

Patel, P., Savani, J. and Poriya, N., 2017. Semi-Strong Form of Market Efficiency for Dividend

and Bonus Announcements: An Empirical Study of India Stock Markets. ANVESHAK-

International Journal of Management. 6(1). pp.108-121.

Tiwari, S. and Pal, D., 2020. DIVIDEND POLICY DECISIONS AND SHARE PRICES

RELATIONSHIP. Finance & Accounting Research Journal. 2(2). pp.76-81.

Ying, W. and Bowen, D., 2017. The Aging Population and the Second Population Dividend:

Empirical Evidence from 18 Aging Nations. Finance & Economics. (8). p.7.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.