Corporate Finance Case Study: GlaxoSmithKline Analysis

VerifiedAdded on 2019/12/18

|18

|4384

|155

Case Study

AI Summary

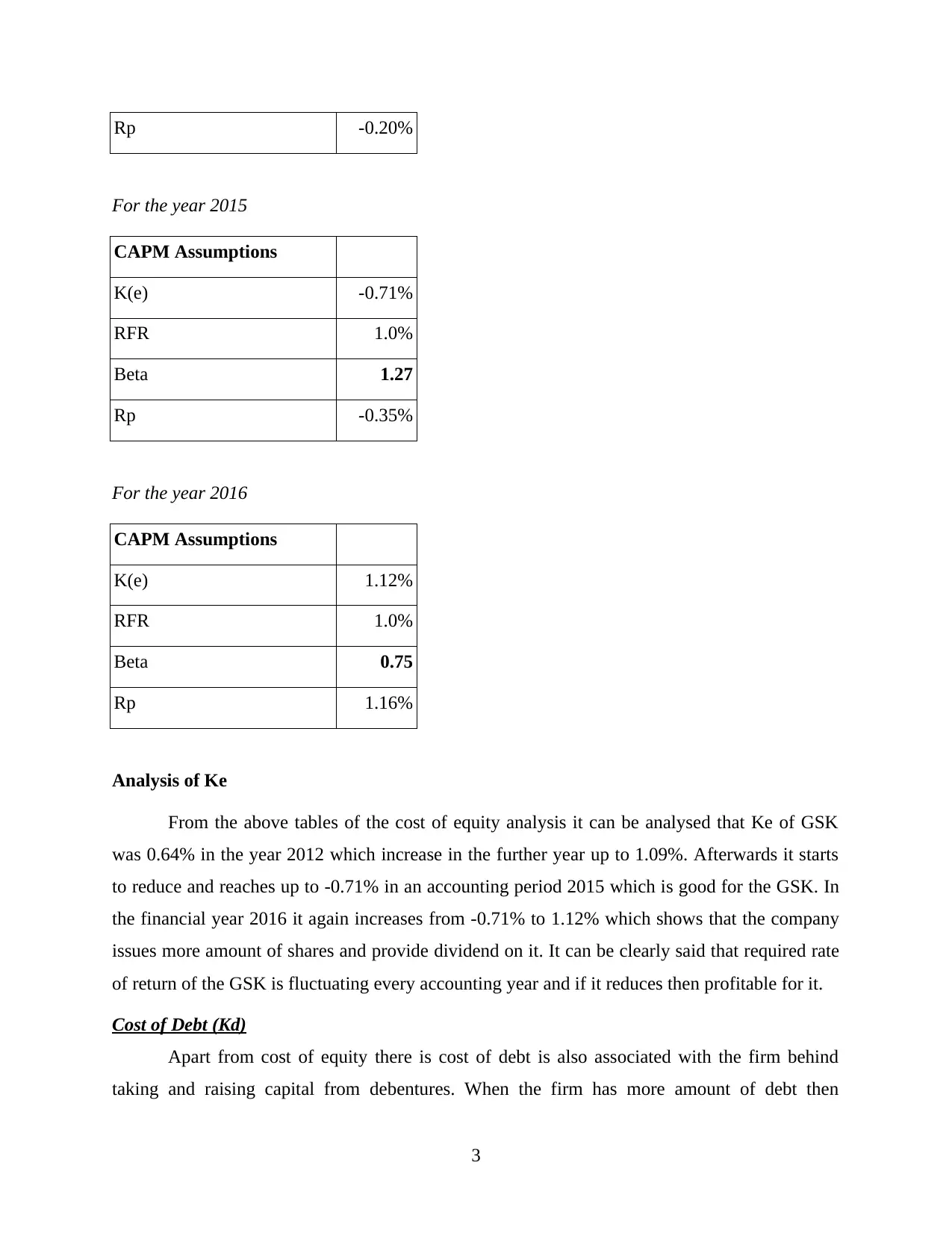

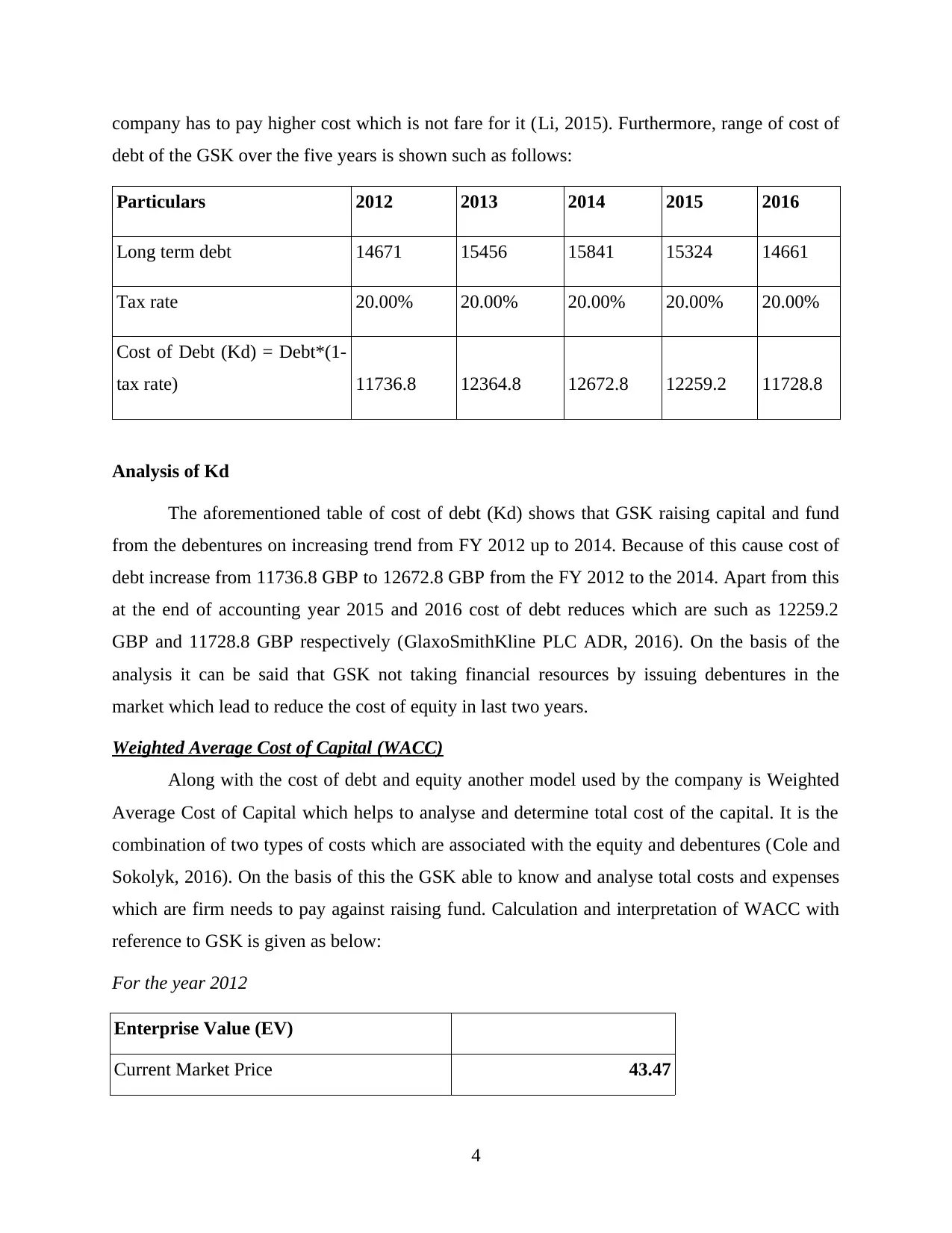

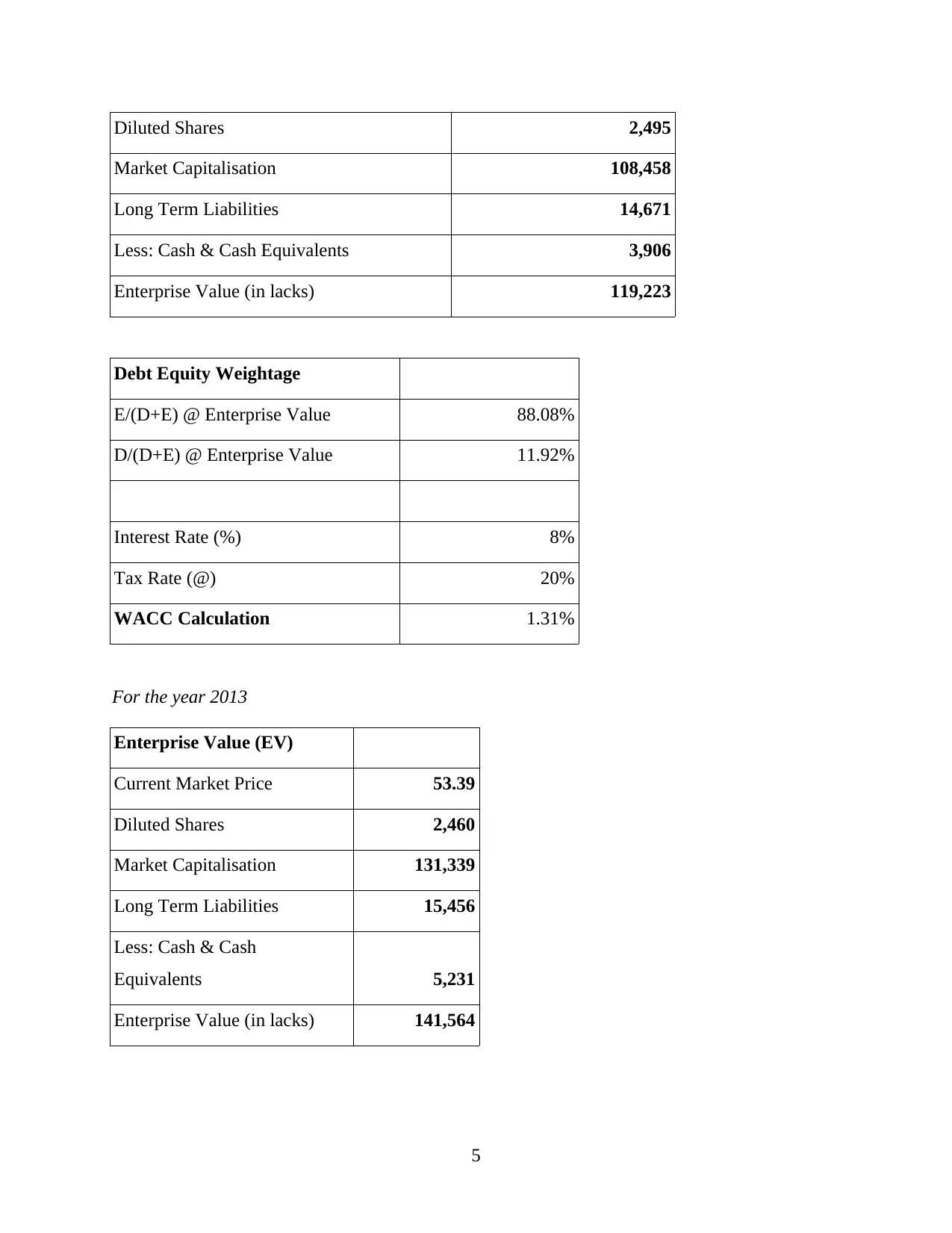

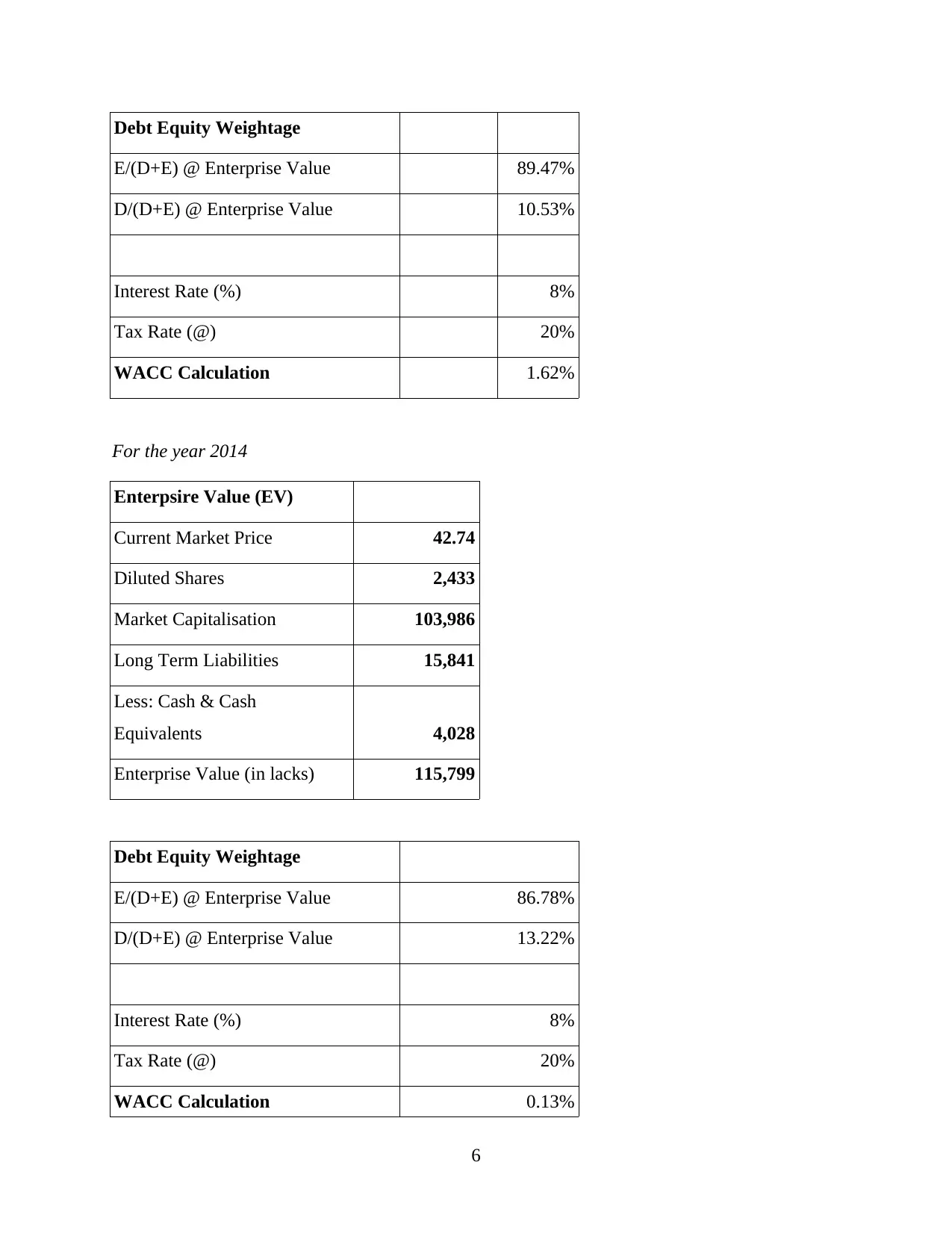

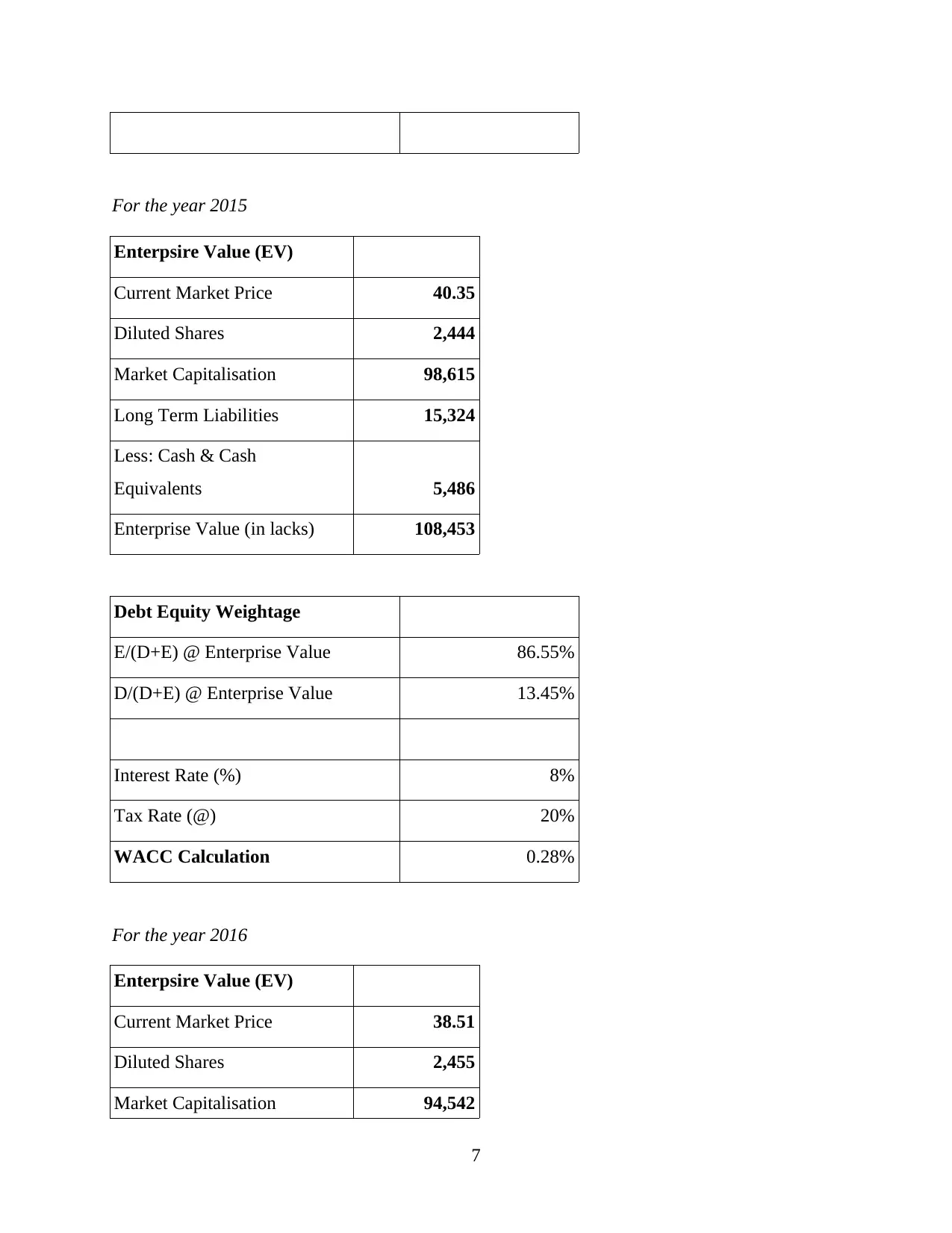

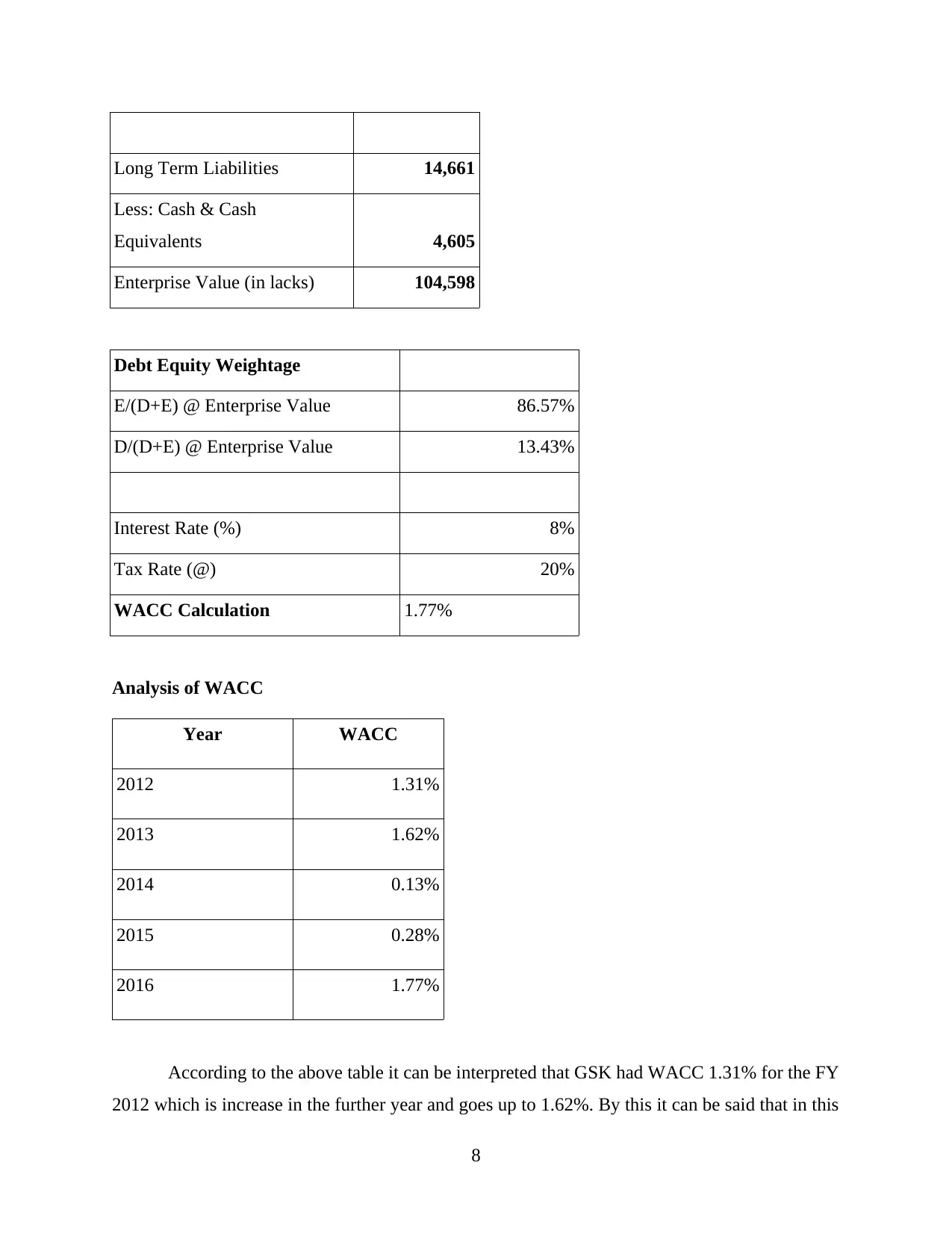

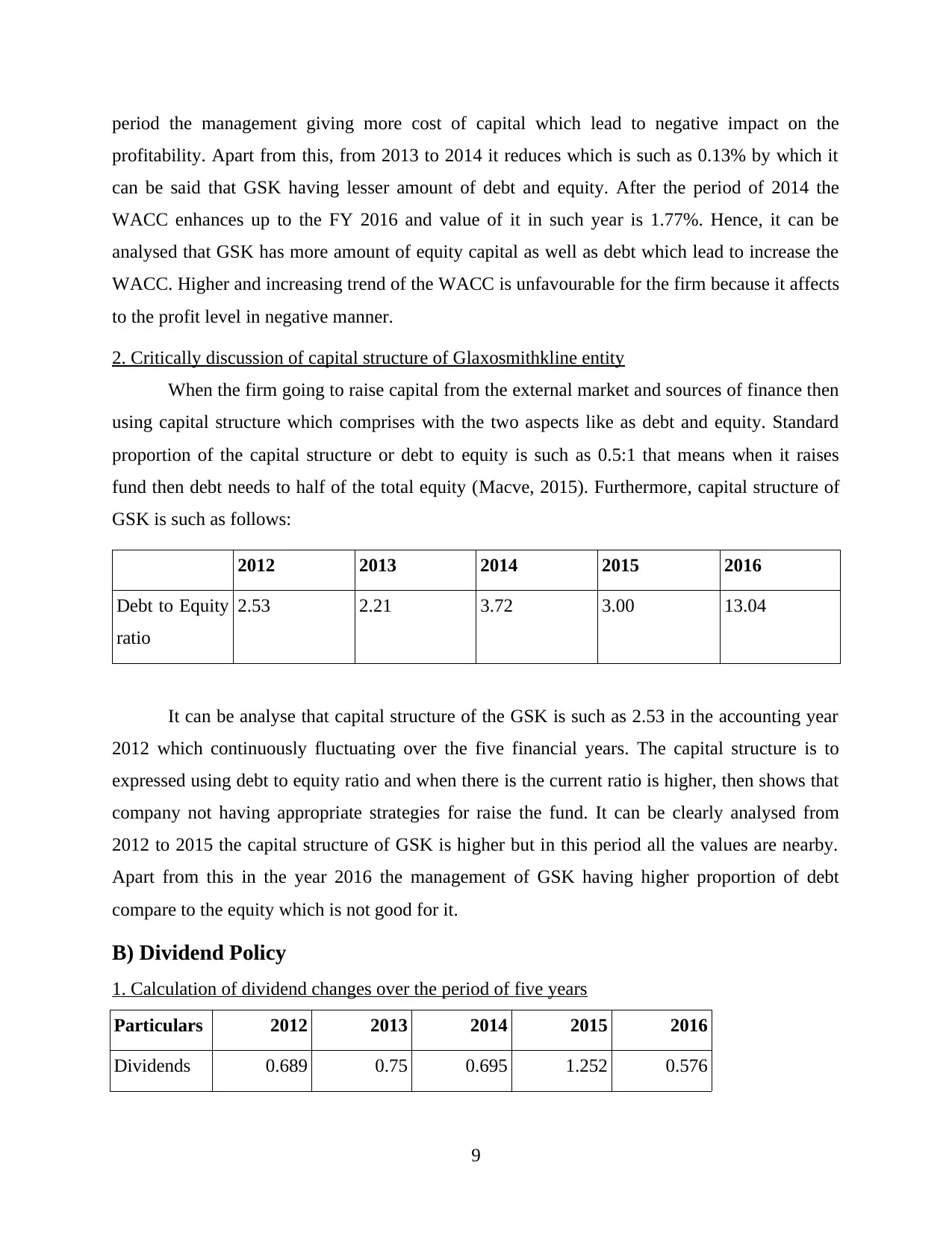

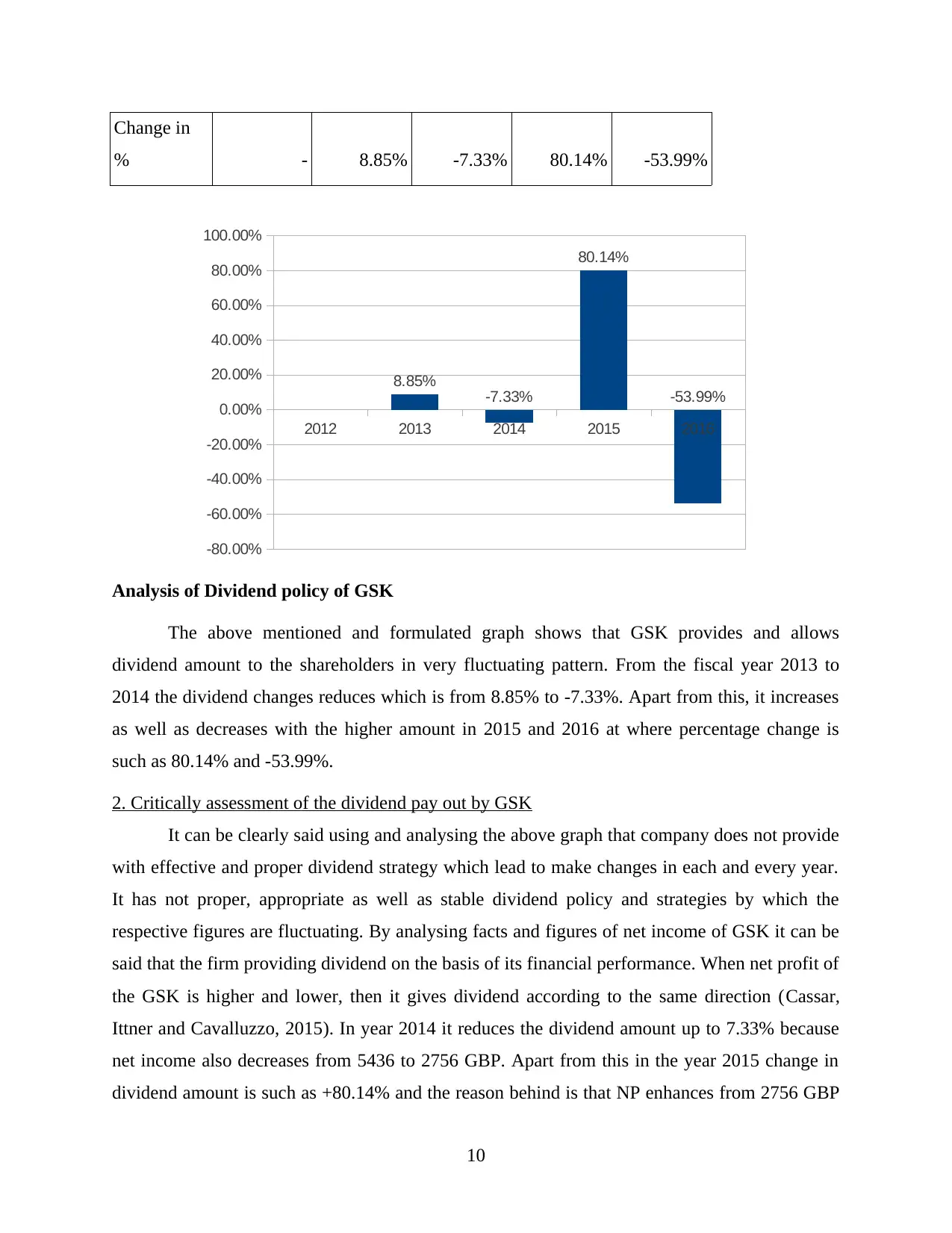

This case study examines the corporate financial strategy of GlaxoSmithKline (GSK), focusing on its discount rates, dividend policy, and capital structure. The analysis includes calculations of the cost of equity, cost of debt, and Weighted Average Cost of Capital (WACC) for GSK from 2012 to 2016, along with a critical discussion of its capital structure using debt-to-equity ratios. The study also assesses GSK's dividend policy, analyzing dividend changes over a five-year period and evaluating its dividend payout strategy. The report compares GSK's shareholder value performance with AstraZeneca (AZN) and utilizes various financial models and ratios to evaluate stock valuation and dividend strategies, providing insights into GSK's corporate life cycle and financial decision-making processes.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.