Accounting Standards Worldwide: A Comprehensive Comparative Analysis

VerifiedAdded on 2019/10/08

|9

|2739

|162

Report

AI Summary

This report delves into the diverse landscape of accounting standards across the globe, highlighting the increasing importance of standardized financial reporting in an era of globalization. It explores the ongoing efforts to establish a universally accepted set of accounting standards, while acknowledging the challenges posed by differing national perspectives and regulations. The report provides a comparative analysis of key accounting frameworks, including IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles), examining their respective roles, applications, and implications for multinational corporations. It discusses the historical development of accounting standards, the roles of standard-setting bodies like IASB and FASB, and the core principles of recognition, measurement, presentation, and disclosure. Furthermore, the report outlines the various types of accounting standards, including disclosure, presentation, and content standards, offering a comprehensive overview of the subject matter.

BLOG: ACCOUNTING STANDARDS

WHAT ARE DIFFERENT ACCOUNTING

STANDARDS AROUND THE WORLD?

WHAT ARE DIFFERENT ACCOUNTING

STANDARDS AROUND THE WORLD?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING STANDARDS

8th August 2019

The need to have a specific set of accounting standards is increased by globalisation. The users

of financial statements around the world are working in order to establish a common set of

accounting standards that could be applied by companies operating globally. Till date the efforts

to formulate a set of globally applicable accounting standards yet not become fruitful. The

procedure of developing a universal set of accounting standards receive conflicting views and

opinions from different nations that have restricted the path of developing a set of accounting

standards that could be applied by all companies across the world. Some nations support the step

of implementing a single and worldwide applicable set of accounting standards, and as a result of

this, the maximum number of nations that support the development of a worldwide accepted set

of accounting standards have started embracing IFRS (International Financial Reporting

Standards) issued by IASB (International Accounting Standards Board).

Some nations are still using their national GAAP (Generally Accepted Accounting Principles)

standards because they believe that adopting another accounting standard might cause various

complexities and complications as well as undermine the nation's sovereignty. Due to this

reason, some countries still support to keep a different set of accounting standards at the national

level that are formulated by considering the countries' laws, regulation related to trade which is

distinct from other countries. The act of implementing a single set of accounting standards leads

to simplification. There are a number of companies that operates through different business lines

and many subsidiaries. These companies tend to consolidate their financial reports for providing

a comprehensive financial report on their overall corporate performance. Here, if a business

organisation is needed to apply and abide by a different set of accounting standards, then it

becomes very challenging to consolidate its business reports.

The elements that are represented in a different manner in various financial statements make it

tough to merge the financial report. In addition to this, the use of different currencies like

pounds, dollars, and yens make it very difficult to consolidate financial reports. A set of global

accounting standards needs to be formulated to simplify the accounting process as well as to

8th August 2019

The need to have a specific set of accounting standards is increased by globalisation. The users

of financial statements around the world are working in order to establish a common set of

accounting standards that could be applied by companies operating globally. Till date the efforts

to formulate a set of globally applicable accounting standards yet not become fruitful. The

procedure of developing a universal set of accounting standards receive conflicting views and

opinions from different nations that have restricted the path of developing a set of accounting

standards that could be applied by all companies across the world. Some nations support the step

of implementing a single and worldwide applicable set of accounting standards, and as a result of

this, the maximum number of nations that support the development of a worldwide accepted set

of accounting standards have started embracing IFRS (International Financial Reporting

Standards) issued by IASB (International Accounting Standards Board).

Some nations are still using their national GAAP (Generally Accepted Accounting Principles)

standards because they believe that adopting another accounting standard might cause various

complexities and complications as well as undermine the nation's sovereignty. Due to this

reason, some countries still support to keep a different set of accounting standards at the national

level that are formulated by considering the countries' laws, regulation related to trade which is

distinct from other countries. The act of implementing a single set of accounting standards leads

to simplification. There are a number of companies that operates through different business lines

and many subsidiaries. These companies tend to consolidate their financial reports for providing

a comprehensive financial report on their overall corporate performance. Here, if a business

organisation is needed to apply and abide by a different set of accounting standards, then it

becomes very challenging to consolidate its business reports.

The elements that are represented in a different manner in various financial statements make it

tough to merge the financial report. In addition to this, the use of different currencies like

pounds, dollars, and yens make it very difficult to consolidate financial reports. A set of global

accounting standards needs to be formulated to simplify the accounting process as well as to

enable multinational companies to merge their annual financial statements with ease. However,

the current situation is different because global accounting standards are yet not been prepared

and some nations still following their own set of accounting standards due to which there are two

different sets of accounting standards are prevailing.

Definition and Discussion on Accounting Standard

Accounting standard refers to a set of procedures, principles, and standards that are common and

defined on the basis of practices and policies in relation to financial accounting. Accounting

standards are developed with the aim of improving the transparency and consistency of financial

reporting of companies operating from all the different countries across the world. Accounting

standards use to relate to every aspect of a company's finances which include assets, liabilities,

expenses, revenue, and shareholders' equity. Some of the specific examples of accounting

standards include asset classification, revenue recognition, allowable or accepted methods for

amortisation, depreciation, what is treated depreciable, measurement of outstanding shares, and

lease classifications. These standards use to apply to the full breadth of a company's financial

picture. Banks, regulatory agencies, and investors count on the accounting standards for ensuring

the accuracy and relevancy of a company's financial information and data.

Accounting standards means some written policy documents that are issued by expert accounting

bodies or by a country's government or by any other regulatory body in order to cover the aspects

associated with recognition, treatment, measurement, presentation, as well as disclosure of

financial transactions in different financial statements. The companies operating internationally

use to follow IFRS (International Financial Reporting Standards) that are formulated by the

IASB. These standards provide a guideline for the companies that follow Non-U.S. GAAP for

reporting their annual financial statements. In the US, GAAP (Generally Accepted Accounting

Principles) is stands as the set of accounting standards which is widely accepted by the US based

companies while preparing their periodic financial statements. GAAP encompasses the details,

legalities, and complexities of corporate and business accounting. GAAP is used by FASB as the

base for its comprehensive set of approved accounting practices and methods.

the current situation is different because global accounting standards are yet not been prepared

and some nations still following their own set of accounting standards due to which there are two

different sets of accounting standards are prevailing.

Definition and Discussion on Accounting Standard

Accounting standard refers to a set of procedures, principles, and standards that are common and

defined on the basis of practices and policies in relation to financial accounting. Accounting

standards are developed with the aim of improving the transparency and consistency of financial

reporting of companies operating from all the different countries across the world. Accounting

standards use to relate to every aspect of a company's finances which include assets, liabilities,

expenses, revenue, and shareholders' equity. Some of the specific examples of accounting

standards include asset classification, revenue recognition, allowable or accepted methods for

amortisation, depreciation, what is treated depreciable, measurement of outstanding shares, and

lease classifications. These standards use to apply to the full breadth of a company's financial

picture. Banks, regulatory agencies, and investors count on the accounting standards for ensuring

the accuracy and relevancy of a company's financial information and data.

Accounting standards means some written policy documents that are issued by expert accounting

bodies or by a country's government or by any other regulatory body in order to cover the aspects

associated with recognition, treatment, measurement, presentation, as well as disclosure of

financial transactions in different financial statements. The companies operating internationally

use to follow IFRS (International Financial Reporting Standards) that are formulated by the

IASB. These standards provide a guideline for the companies that follow Non-U.S. GAAP for

reporting their annual financial statements. In the US, GAAP (Generally Accepted Accounting

Principles) is stands as the set of accounting standards which is widely accepted by the US based

companies while preparing their periodic financial statements. GAAP encompasses the details,

legalities, and complexities of corporate and business accounting. GAAP is used by FASB as the

base for its comprehensive set of approved accounting practices and methods.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

While the US based public companies are currently needed to follow the GAAP standards at the

time of filing their periodic financial statements, the private companies of the country are still

allowed to choose the standards system they prefer. This might change soon depending on the

upcoming decisions from the Securities Exchange Commission (SEC) that has been discussing

whether to step-out with recommending the global standards of accounting, either completely or

partially. According to the Bloomberg BNA, James Schnurr, the Chief Accountant of SEC, the

IFRS are supplemental-reporting approach and this would be treated as a simple alternative to

the complete adoption of accounting standards that are issued by IASB. Till date, IFRS standards

are not widely accepted in the US. Still, the IASB and FASB are working together to agree on as

well as to set accounting standards that could be applied both nationally and internationally. At

present, there are two sets of accounting standards one is GAAP (followed by the public

companies of the US) formulated by FASB, and the other one is IFRS (a set of worldwide

accepted accounting standards) formulated by IASB.

Accounting standards are developed by IASB and FASB with to assist companies in dealing with

the four major accounting issues, namely

The recognition of corporate level financial events

Measurement of the business transactions that are financial in nature

Presentation of periodic financial statements in a true and fair manner

Disclosure requirements of companies for ensuring their stakeholders that they are

properly informed.

History of Accounting Standards and their Purpose

In 1930, the American Institute of Accountants, currently popular as the American Institute of

Certified Public Accountants, in collaboration with the NSCE (New York Stock Exchange)

attempted to represent the accounting standards first. Following such attempt of AICPA and

NSCE, in 1933, the Securities Act and in 1934, the Securities Exchange Act was developed by

the SEC (Securities and Exchange Commission). At that time, accounting standards were also

established by the Accounting Standards Board of the US Government for setting accounting

time of filing their periodic financial statements, the private companies of the country are still

allowed to choose the standards system they prefer. This might change soon depending on the

upcoming decisions from the Securities Exchange Commission (SEC) that has been discussing

whether to step-out with recommending the global standards of accounting, either completely or

partially. According to the Bloomberg BNA, James Schnurr, the Chief Accountant of SEC, the

IFRS are supplemental-reporting approach and this would be treated as a simple alternative to

the complete adoption of accounting standards that are issued by IASB. Till date, IFRS standards

are not widely accepted in the US. Still, the IASB and FASB are working together to agree on as

well as to set accounting standards that could be applied both nationally and internationally. At

present, there are two sets of accounting standards one is GAAP (followed by the public

companies of the US) formulated by FASB, and the other one is IFRS (a set of worldwide

accepted accounting standards) formulated by IASB.

Accounting standards are developed by IASB and FASB with to assist companies in dealing with

the four major accounting issues, namely

The recognition of corporate level financial events

Measurement of the business transactions that are financial in nature

Presentation of periodic financial statements in a true and fair manner

Disclosure requirements of companies for ensuring their stakeholders that they are

properly informed.

History of Accounting Standards and their Purpose

In 1930, the American Institute of Accountants, currently popular as the American Institute of

Certified Public Accountants, in collaboration with the NSCE (New York Stock Exchange)

attempted to represent the accounting standards first. Following such attempt of AICPA and

NSCE, in 1933, the Securities Act and in 1934, the Securities Exchange Act was developed by

the SEC (Securities and Exchange Commission). At that time, accounting standards were also

established by the Accounting Standards Board of the US Government for setting accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

principles and standards for every state as well as local governments. Accounting standards use

to specify the time and the way all the events that economic in nature are required to be

recognised, measured, and then displayed.

Entities like banks, regulatory agencies, and investors rely on the accounting standards for

ensuring relevance and accuracy of the information provides by entities about their financial

performance. These types of technical pronouncements in the US have ensured the transparency

in financial reporting along with having set the limits or boundaries for the measures required to

be used by entities in their practices related to financial reporting. In 1973, on the basis of the

recommendation made by the AICPA, the Financial Accounting Standard Board was established

as independently operated accounting standards setting board. It was formed to take over the

determinations as well as the updates of GAAP. FASB, till date, is entirely responsible for the

Accounting Standards Codification which is a centralised resource where the US based

accountants use to find every current GAAP.

U.S. GAAP - Accounting Standards

The first set of accounting standards was developed, managed as well as by AICPA. In 1973, all

the responsibilities of AICPA were transferred to the newly formed FASB. An independent non-

profit organisation, FASB has the power to establish as well as interpret GAAP in the US for

publicly and privately operated companies along with non-profit organisations. GAAP refers to a

set of accounting standards representing how both profit and non-profits making companies, and

governments need to prepare and then present their individual financial statements. The SEC

requires every listed (listed on the US securities exchange) companies operating in the US to

adhere to the accounting standards titled U.S. GAAP while preparing their periodic financial

statements. Accounting standards use to ensure comparability of periodic financial statements of

multiple companies. The comparability between the financial statements of multiple companies

was ensured because ensured all companies follow the same set of rules, guidelines, and

accounting standards while preparing their financial statements which made these statements

credible. Such comparability of financial statements also allows more effective economic

decisions on the basis of consistent and accurate information of companies regarding their

to specify the time and the way all the events that economic in nature are required to be

recognised, measured, and then displayed.

Entities like banks, regulatory agencies, and investors rely on the accounting standards for

ensuring relevance and accuracy of the information provides by entities about their financial

performance. These types of technical pronouncements in the US have ensured the transparency

in financial reporting along with having set the limits or boundaries for the measures required to

be used by entities in their practices related to financial reporting. In 1973, on the basis of the

recommendation made by the AICPA, the Financial Accounting Standard Board was established

as independently operated accounting standards setting board. It was formed to take over the

determinations as well as the updates of GAAP. FASB, till date, is entirely responsible for the

Accounting Standards Codification which is a centralised resource where the US based

accountants use to find every current GAAP.

U.S. GAAP - Accounting Standards

The first set of accounting standards was developed, managed as well as by AICPA. In 1973, all

the responsibilities of AICPA were transferred to the newly formed FASB. An independent non-

profit organisation, FASB has the power to establish as well as interpret GAAP in the US for

publicly and privately operated companies along with non-profit organisations. GAAP refers to a

set of accounting standards representing how both profit and non-profits making companies, and

governments need to prepare and then present their individual financial statements. The SEC

requires every listed (listed on the US securities exchange) companies operating in the US to

adhere to the accounting standards titled U.S. GAAP while preparing their periodic financial

statements. Accounting standards use to ensure comparability of periodic financial statements of

multiple companies. The comparability between the financial statements of multiple companies

was ensured because ensured all companies follow the same set of rules, guidelines, and

accounting standards while preparing their financial statements which made these statements

credible. Such comparability of financial statements also allows more effective economic

decisions on the basis of consistent and accurate information of companies regarding their

financial performance and position. This is how the concept of accounting standard evoked and

came into existence.

IFRSs (International Financial Reporting Standards) by IASB

GAAP are heavily accepted and applied among private and public companies in the US whereas

IFRS is used primarily by the rest companies in the world. Multinational companies are needed

to use IFRS standards as these standards are designed by keeping the global companies in mind

to provide them a common set of accounting standards that help them to compare their financial

statements with others. In 2001, the IASB (International Accounting Standards Board) was

founded for replacing an older standards organisation. It was established in London and held

responsible for IFRS that are currently used in a number of nations across the world. At present,

FASB is working with IASB by undertaking the initiative to improve the system of financial

reporting along with the comparability and consistency of multinational companies' financial

reports to harmonise the accounting and financial reporting system across the world.

Types of Accounting Standards around the World

There are two key accounting standard-setting bodies naming International Accounting

Standards Board (IASB), and Financial Accounting Standards Board (FASB). Both these two

accounting standard setters use to set and reset accounting standards to improve accounting

system and financial reporting system transparent, reliable and understandable. These standard-

setting bodies stand as private sector organisations and consist of experienced auditors,

accountants, and academicians those who are highly capable as well as responsible to set

standards for financial reporting. The accounting standards formulated by these two standard-

setting bodies are to some extent similar in terms of the subject line. The set of accounting

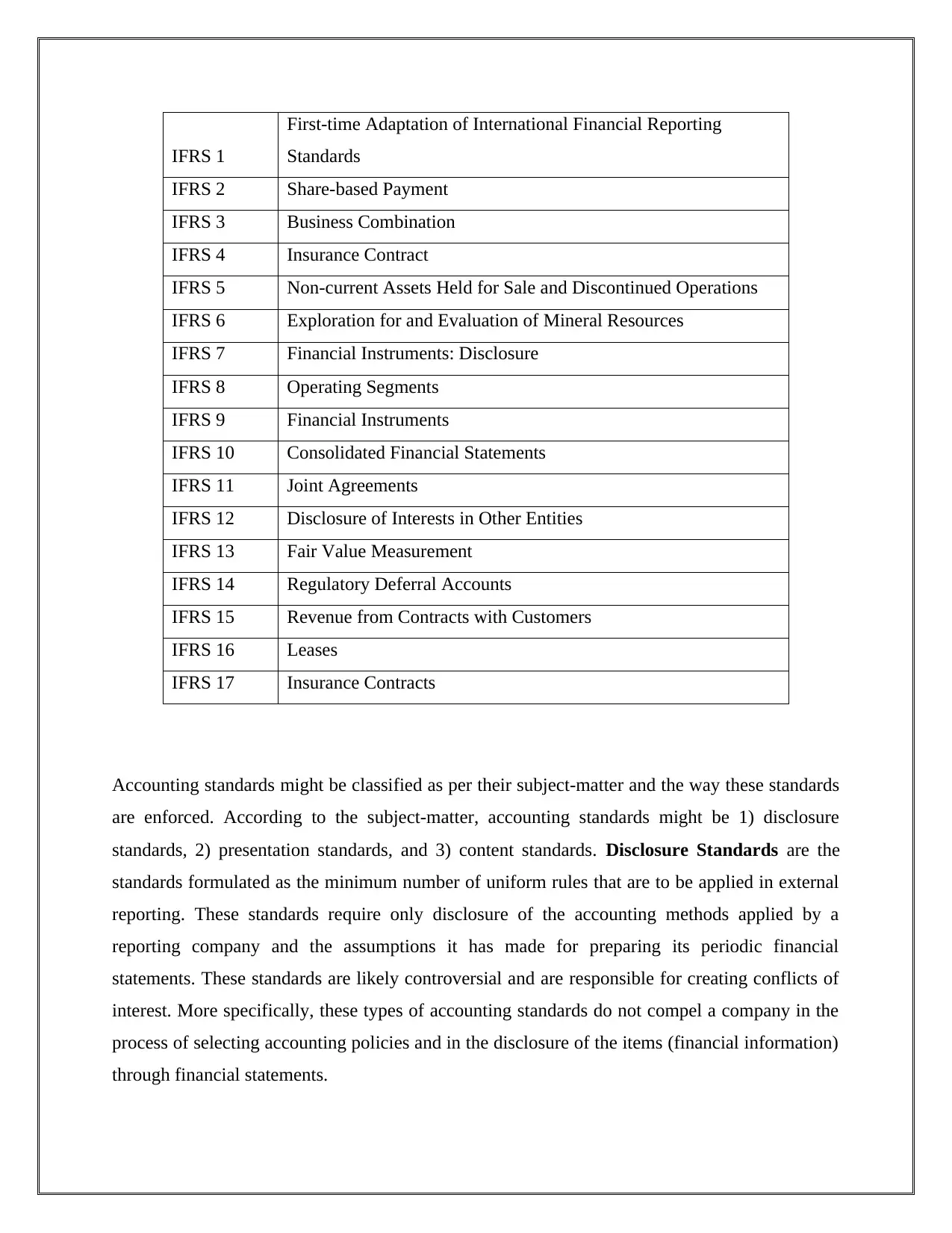

standards IASB has developed includes accounting standards from IFRS 1 to IFRS 17 along with

IAS 1 – Presentation of Financial Statements to IAS 41 - Agriculture, in total 57 accounting

standards. On the other side, the accounting standards developed by FASB are GAAP. Some of

the accounting standards accepted and used internationally and are developed by IASB as IFRSs

are provided below in a tabular form.

came into existence.

IFRSs (International Financial Reporting Standards) by IASB

GAAP are heavily accepted and applied among private and public companies in the US whereas

IFRS is used primarily by the rest companies in the world. Multinational companies are needed

to use IFRS standards as these standards are designed by keeping the global companies in mind

to provide them a common set of accounting standards that help them to compare their financial

statements with others. In 2001, the IASB (International Accounting Standards Board) was

founded for replacing an older standards organisation. It was established in London and held

responsible for IFRS that are currently used in a number of nations across the world. At present,

FASB is working with IASB by undertaking the initiative to improve the system of financial

reporting along with the comparability and consistency of multinational companies' financial

reports to harmonise the accounting and financial reporting system across the world.

Types of Accounting Standards around the World

There are two key accounting standard-setting bodies naming International Accounting

Standards Board (IASB), and Financial Accounting Standards Board (FASB). Both these two

accounting standard setters use to set and reset accounting standards to improve accounting

system and financial reporting system transparent, reliable and understandable. These standard-

setting bodies stand as private sector organisations and consist of experienced auditors,

accountants, and academicians those who are highly capable as well as responsible to set

standards for financial reporting. The accounting standards formulated by these two standard-

setting bodies are to some extent similar in terms of the subject line. The set of accounting

standards IASB has developed includes accounting standards from IFRS 1 to IFRS 17 along with

IAS 1 – Presentation of Financial Statements to IAS 41 - Agriculture, in total 57 accounting

standards. On the other side, the accounting standards developed by FASB are GAAP. Some of

the accounting standards accepted and used internationally and are developed by IASB as IFRSs

are provided below in a tabular form.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

IFRS 1

First-time Adaptation of International Financial Reporting

Standards

IFRS 2 Share-based Payment

IFRS 3 Business Combination

IFRS 4 Insurance Contract

IFRS 5 Non-current Assets Held for Sale and Discontinued Operations

IFRS 6 Exploration for and Evaluation of Mineral Resources

IFRS 7 Financial Instruments: Disclosure

IFRS 8 Operating Segments

IFRS 9 Financial Instruments

IFRS 10 Consolidated Financial Statements

IFRS 11 Joint Agreements

IFRS 12 Disclosure of Interests in Other Entities

IFRS 13 Fair Value Measurement

IFRS 14 Regulatory Deferral Accounts

IFRS 15 Revenue from Contracts with Customers

IFRS 16 Leases

IFRS 17 Insurance Contracts

Accounting standards might be classified as per their subject-matter and the way these standards

are enforced. According to the subject-matter, accounting standards might be 1) disclosure

standards, 2) presentation standards, and 3) content standards. Disclosure Standards are the

standards formulated as the minimum number of uniform rules that are to be applied in external

reporting. These standards require only disclosure of the accounting methods applied by a

reporting company and the assumptions it has made for preparing its periodic financial

statements. These standards are likely controversial and are responsible for creating conflicts of

interest. More specifically, these types of accounting standards do not compel a company in the

process of selecting accounting policies and in the disclosure of the items (financial information)

through financial statements.

First-time Adaptation of International Financial Reporting

Standards

IFRS 2 Share-based Payment

IFRS 3 Business Combination

IFRS 4 Insurance Contract

IFRS 5 Non-current Assets Held for Sale and Discontinued Operations

IFRS 6 Exploration for and Evaluation of Mineral Resources

IFRS 7 Financial Instruments: Disclosure

IFRS 8 Operating Segments

IFRS 9 Financial Instruments

IFRS 10 Consolidated Financial Statements

IFRS 11 Joint Agreements

IFRS 12 Disclosure of Interests in Other Entities

IFRS 13 Fair Value Measurement

IFRS 14 Regulatory Deferral Accounts

IFRS 15 Revenue from Contracts with Customers

IFRS 16 Leases

IFRS 17 Insurance Contracts

Accounting standards might be classified as per their subject-matter and the way these standards

are enforced. According to the subject-matter, accounting standards might be 1) disclosure

standards, 2) presentation standards, and 3) content standards. Disclosure Standards are the

standards formulated as the minimum number of uniform rules that are to be applied in external

reporting. These standards require only disclosure of the accounting methods applied by a

reporting company and the assumptions it has made for preparing its periodic financial

statements. These standards are likely controversial and are responsible for creating conflicts of

interest. More specifically, these types of accounting standards do not compel a company in the

process of selecting accounting policies and in the disclosure of the items (financial information)

through financial statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Presentation Standards use to specify the types and form of accounting information required to

be showcased or presented. These standards might specify that some financial statements (like a

company's funds-flow statement) be presented and the order to be used for presenting such

financial statement in the annual report. These types of standards place a little constraint on the

selection of accounting procedures and policies than the disclosure standards. Moreover, these

types of accounting standards target to reduce the users' expenditure while utilizing a company's

financial statements. Content Standards use to specify a company's accounting information that

is required to be presented publicly at the end of a particular financial period.

Benefits and Limitations of Accounting Standards

Benefits of Accounting Standards are -

Improve the reliability and credibility of a company's financial statements: A

company's financial statements are used in making appropriate economic decisions by a

number of internal and external users like existing as well as potential shareholders and

suppliers, trade creditors, employees, customers, taxation authorities, along with few

more interested parties. Due to this, the financial statements of companies must be

reliable, accurate, and credible that could help the stakeholders to make sound financial

decisions in relation to the reporting entity. The main aim of developing accounting

standards by IASB and FASB is to ensure the reliability and credibility of the reporting

entities' financial statements to assist their stakeholders in decision making.

Beneficial for accountants as well as auditors: A set of accounting standards act as

guiding rules to a company's auditors and accountants. The use of accounting standards

helps accountants to ensure correctness, integrity, and reliability of accounts and financial

reports. It helps auditors to measure whether the reporting entity has followed the

standards while preparing financial statements or not. These standards help auditors to

monitor a company's financial performance.

Facilitates in comparison and resolving conflict: Accounting standards assist

companies in comparing their own financial status with other companies which

ultimately lead the companies in developing more effective business decisions to enhance

be showcased or presented. These standards might specify that some financial statements (like a

company's funds-flow statement) be presented and the order to be used for presenting such

financial statement in the annual report. These types of standards place a little constraint on the

selection of accounting procedures and policies than the disclosure standards. Moreover, these

types of accounting standards target to reduce the users' expenditure while utilizing a company's

financial statements. Content Standards use to specify a company's accounting information that

is required to be presented publicly at the end of a particular financial period.

Benefits and Limitations of Accounting Standards

Benefits of Accounting Standards are -

Improve the reliability and credibility of a company's financial statements: A

company's financial statements are used in making appropriate economic decisions by a

number of internal and external users like existing as well as potential shareholders and

suppliers, trade creditors, employees, customers, taxation authorities, along with few

more interested parties. Due to this, the financial statements of companies must be

reliable, accurate, and credible that could help the stakeholders to make sound financial

decisions in relation to the reporting entity. The main aim of developing accounting

standards by IASB and FASB is to ensure the reliability and credibility of the reporting

entities' financial statements to assist their stakeholders in decision making.

Beneficial for accountants as well as auditors: A set of accounting standards act as

guiding rules to a company's auditors and accountants. The use of accounting standards

helps accountants to ensure correctness, integrity, and reliability of accounts and financial

reports. It helps auditors to measure whether the reporting entity has followed the

standards while preparing financial statements or not. These standards help auditors to

monitor a company's financial performance.

Facilitates in comparison and resolving conflict: Accounting standards assist

companies in comparing their own financial status with other companies which

ultimately lead the companies in developing more effective business decisions to enhance

their corporate financial performance. It helps in resolving conflicts arise in measuring,

recognition and other accounting procedures while preparing annual accounts and

financial statements. Moreover, to some extent, it allows companies to reduce confusing

variations in accounting treatments that are used in preparing financial statements.

Helps in compliance with regulatory authorities: Accounting standards help

companies to act in compliance with the pre-fixed accounting rules and regulations in

relation to financial statements and disclosure. Proper application of accounting standards

assists a company to restrict or eliminate the chances of arising legal issues, and

accounting fraud.

Limitations of Accounting Standards are –

Restricts companies to make their own choice: Every alternative solution in

accounting to some accounting issues has its benefits and by erasing the power to choose

between the alternatives solutions brings rigidity. Rigidity is not good as it uses to take

away the flexibility in adopting as well as applying accounting policies and principles.

Inability to override statue: Accounting standards are not capable of overriding statue.

In this because they are needed to be formulated within the scope of the prevailing statue.

recognition and other accounting procedures while preparing annual accounts and

financial statements. Moreover, to some extent, it allows companies to reduce confusing

variations in accounting treatments that are used in preparing financial statements.

Helps in compliance with regulatory authorities: Accounting standards help

companies to act in compliance with the pre-fixed accounting rules and regulations in

relation to financial statements and disclosure. Proper application of accounting standards

assists a company to restrict or eliminate the chances of arising legal issues, and

accounting fraud.

Limitations of Accounting Standards are –

Restricts companies to make their own choice: Every alternative solution in

accounting to some accounting issues has its benefits and by erasing the power to choose

between the alternatives solutions brings rigidity. Rigidity is not good as it uses to take

away the flexibility in adopting as well as applying accounting policies and principles.

Inability to override statue: Accounting standards are not capable of overriding statue.

In this because they are needed to be formulated within the scope of the prevailing statue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.