Global Corporate, Financial Accounting, and Owners’ Equity Analysis

VerifiedAdded on 2023/06/04

|15

|3060

|329

Report

AI Summary

This report provides a comprehensive overview of corporate regulation, accounting standard setting, and owners’ equity from a global perspective. It highlights the necessity of regulating financial accounting and reporting to prevent manipulation and fraud, emphasizing the role of organizations like IASB in developing standardized accounting practices. The report also discusses the Australian Accounting Standards Board's (AASB) participation in the global standard-setting process and the reasons why IFRS is not mandatory for all member nations. Finally, it includes an analysis of the owners’ equity and debt-to-equity positions of four public listed firms in the Australian Securities Exchange (ASX): BHP Billiton, Rio Tinto, Orica Limited, and Fortescue Metals Group, evaluating their financial leverage and capital structures.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate and Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary:

The primary aim of this report is to provide a brief overview of the corporate regulation,

accounting standard setting and owners’ equity from the global perspective. It has been found

that the managers might not be willing to disclose the internal financial information to all users

of the financial statements. Hence, regulation in financial accounting and reporting is necessary.

It has been further evaluated that all nations have their own accounting standards; however, for

bringing comparability and standardisation, the organisations like IASB have made attempts to

develop a single standard acceptable for maximum countries. Finally, it is found out that Orica

Limited is placed in a better position in the Australian mining sector in terms of debt and equity

compared to BHP Billiton, Rio Tinto and Fortescue Metals Group.

Executive Summary:

The primary aim of this report is to provide a brief overview of the corporate regulation,

accounting standard setting and owners’ equity from the global perspective. It has been found

that the managers might not be willing to disclose the internal financial information to all users

of the financial statements. Hence, regulation in financial accounting and reporting is necessary.

It has been further evaluated that all nations have their own accounting standards; however, for

bringing comparability and standardisation, the organisations like IASB have made attempts to

develop a single standard acceptable for maximum countries. Finally, it is found out that Orica

Limited is placed in a better position in the Australian mining sector in terms of debt and equity

compared to BHP Billiton, Rio Tinto and Fortescue Metals Group.

2CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction:....................................................................................................................................3

Corporate Regulation:......................................................................................................................3

Answer to Question (i):...............................................................................................................3

Accounting Standard Setting:..........................................................................................................5

Answer to Question (ii):..............................................................................................................5

Owners’ Equity:...............................................................................................................................6

Answer to Question (iii):.............................................................................................................6

Answer to Question (iv):.............................................................................................................8

Conclusion:....................................................................................................................................10

References:....................................................................................................................................12

Table of Contents

Introduction:....................................................................................................................................3

Corporate Regulation:......................................................................................................................3

Answer to Question (i):...............................................................................................................3

Accounting Standard Setting:..........................................................................................................5

Answer to Question (ii):..............................................................................................................5

Owners’ Equity:...............................................................................................................................6

Answer to Question (iii):.............................................................................................................6

Answer to Question (iv):.............................................................................................................8

Conclusion:....................................................................................................................................10

References:....................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE AND FINANCIAL ACCOUNTING

Introduction:

The report is prepared with the intent of providing a brief overview of the corporate

regulation, accounting standard setting and owners’ equity from the global perspective. The first

section would provide a brief overview of the necessity of regulating financial accounting and

reporting along with providing power to the manager in voluntary disclosure of financial

accounting information. The second section would emphasise on the role of the “Australian

Accounting Standards Board (AASB)” in setting the international standard setting process,

which is identified as IFRS. Moreover, it would discuss the reasons that IFRS is not mandatory

for the member nations of IASB. Finally, the report would shed light on selecting four public

listed firms in ASX and evaluation would be made in relation their owners’ equity position as

well as debt-equity position.

Corporate Regulation:

Answer to Question (i):

Favourable points for regulation of financial accounting and reporting:

There is need to regulate financial accounting and reporting due to a variety of reasons.

Firstly, if it is not regulated, the information published by the business organisations might be

selective and it could be manipulated by the individuals accountable to send the same into the

market (Henderson et al. 2015).Therefore, the organisations are need to fulfil various criteria for

aligning with the public interest of the current as well as potential investors. The regulating

authorities formulated the criteria for assuring information quality at minimal or no cost for

shielding the public from misleading, fraudulent and hidden disclosures. Secondly, the demand

Introduction:

The report is prepared with the intent of providing a brief overview of the corporate

regulation, accounting standard setting and owners’ equity from the global perspective. The first

section would provide a brief overview of the necessity of regulating financial accounting and

reporting along with providing power to the manager in voluntary disclosure of financial

accounting information. The second section would emphasise on the role of the “Australian

Accounting Standards Board (AASB)” in setting the international standard setting process,

which is identified as IFRS. Moreover, it would discuss the reasons that IFRS is not mandatory

for the member nations of IASB. Finally, the report would shed light on selecting four public

listed firms in ASX and evaluation would be made in relation their owners’ equity position as

well as debt-equity position.

Corporate Regulation:

Answer to Question (i):

Favourable points for regulation of financial accounting and reporting:

There is need to regulate financial accounting and reporting due to a variety of reasons.

Firstly, if it is not regulated, the information published by the business organisations might be

selective and it could be manipulated by the individuals accountable to send the same into the

market (Henderson et al. 2015).Therefore, the organisations are need to fulfil various criteria for

aligning with the public interest of the current as well as potential investors. The regulating

authorities formulated the criteria for assuring information quality at minimal or no cost for

shielding the public from misleading, fraudulent and hidden disclosures. Secondly, the demand

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE AND FINANCIAL ACCOUNTING

for actual and true accounting information is on the increasing scale from the prospective

investors. When investments are made in the business entities, it is necessary for the regulating

authorities to intervene into the matter for ensuring that the formats of accounting and reporting

fulfil the investors’ needs by answering to their questions.

When an organisation finds its shares listed in the stock market, it would be proper when

such information is published in standardised formats. This would help in comparing the same

with the financial performance of the peers for ensuring that both shareholders and insiders have

equal knowledge of information (Beatty and Liao 2014). Therefore, it could be said that the

necessity of regulation is important for increasing the standard of the profession.

Favourable points for voluntary disclosure of financial accounting and reporting:

When managers are provided with the opportunity of disclosing voluntary financial

information, they would conduct the work in a fair and responsible manner as suitable agents of

their owners or shareholders. Since the managers have knowledge about internal activities of the

organisations, they have more knowledge about the actual financial conditions. This would assist

them in to provide certain non-standardised financial information to the market (Jehu and

Ibrahim 2017). This could be considered as signalling theory, in which the concerned

organisations have the unique benefit of transferring significant information like likely dividend

in the form a signal to the market regarding their growth tendencies. When such information is

disclosed by the managers of the business organisations, the share price would increase

significantly and the business outsiders would be ensured about the financial conditions.

However, the managers might not be willing to disclose the internal financial information

to all users of the financial statements. Instead, they might distort such information to the

for actual and true accounting information is on the increasing scale from the prospective

investors. When investments are made in the business entities, it is necessary for the regulating

authorities to intervene into the matter for ensuring that the formats of accounting and reporting

fulfil the investors’ needs by answering to their questions.

When an organisation finds its shares listed in the stock market, it would be proper when

such information is published in standardised formats. This would help in comparing the same

with the financial performance of the peers for ensuring that both shareholders and insiders have

equal knowledge of information (Beatty and Liao 2014). Therefore, it could be said that the

necessity of regulation is important for increasing the standard of the profession.

Favourable points for voluntary disclosure of financial accounting and reporting:

When managers are provided with the opportunity of disclosing voluntary financial

information, they would conduct the work in a fair and responsible manner as suitable agents of

their owners or shareholders. Since the managers have knowledge about internal activities of the

organisations, they have more knowledge about the actual financial conditions. This would assist

them in to provide certain non-standardised financial information to the market (Jehu and

Ibrahim 2017). This could be considered as signalling theory, in which the concerned

organisations have the unique benefit of transferring significant information like likely dividend

in the form a signal to the market regarding their growth tendencies. When such information is

disclosed by the managers of the business organisations, the share price would increase

significantly and the business outsiders would be ensured about the financial conditions.

However, the managers might not be willing to disclose the internal financial information

to all users of the financial statements. Instead, they might distort such information to the

5CORPORATE AND FINANCIAL ACCOUNTING

investors for gaining more funds due to the fear of losing their jobs. Moreover, all information

should not be made public, as per the demand of the regulations (Page 2014). Hence, regulation

on financial accounting and reporting is preferred over voluntary disclosure of financial

information in order to avoid manipulation and frauds in the financial reports of the business

organisations.

Accounting Standard Setting:

Answer to Question (ii):

Process through which AASB participates in the global standard setting process:

AASB has the vision of enhancing its reputation in the form of a leading national standard

setter for gaining recognition in the international centre of excellence. This would be ensured by

formulating and maintaining greater quality standards of financial reporting for all the Australian

economic sectors by contributing through talent and leadership in order to develop international

standards of financial reporting (Bamber and McMeeking 2016). AASB takes part in the global

standard setting process in the following ways:

The accounting standards as well as standard amendments made by IASB are in line with

the legislative drafting protocols of Australia and the requirements of “Federal Register

of Legislative Instruments”.

The accounting compilations or standards are filed on the “Federal Register of

Legislative Instruments” and they are disclosed on the website of AASB within three

days after they are finalised (Erb and Pelger 2015).

The responses are made to all the important drafts of IPSASB and IASB.

investors for gaining more funds due to the fear of losing their jobs. Moreover, all information

should not be made public, as per the demand of the regulations (Page 2014). Hence, regulation

on financial accounting and reporting is preferred over voluntary disclosure of financial

information in order to avoid manipulation and frauds in the financial reports of the business

organisations.

Accounting Standard Setting:

Answer to Question (ii):

Process through which AASB participates in the global standard setting process:

AASB has the vision of enhancing its reputation in the form of a leading national standard

setter for gaining recognition in the international centre of excellence. This would be ensured by

formulating and maintaining greater quality standards of financial reporting for all the Australian

economic sectors by contributing through talent and leadership in order to develop international

standards of financial reporting (Bamber and McMeeking 2016). AASB takes part in the global

standard setting process in the following ways:

The accounting standards as well as standard amendments made by IASB are in line with

the legislative drafting protocols of Australia and the requirements of “Federal Register

of Legislative Instruments”.

The accounting compilations or standards are filed on the “Federal Register of

Legislative Instruments” and they are disclosed on the website of AASB within three

days after they are finalised (Erb and Pelger 2015).

The responses are made to all the important drafts of IPSASB and IASB.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE AND FINANCIAL ACCOUNTING

Reason that IFRS is not compulsory for the member countries of IASB:

The IASB is a private and independent group, which formulates and approves IFRS. It

functions under the oversight of the foundation of IFRS. The IFRS Foundation is involved in

overseeing the operations conducted by IASB. The formulation of IASB dates back to 1901 for

replacing the ‘International Accounting Standards Committee (IASC)”. At present, IASB has 14

member nations and in accordance with the Constitution of the IFRS Foundation, IASB has full

accountability for all technical aspects of the foundation. These include complete discretion to

form and pursue its technical goal, which is subject to consulting needs with the public and the

trustees (Erb and Pelger 2015). Moreover, it takes into account the formulation and issuance of

IFRS as well as exposure drafts following the due procedure mentioned in the constitution.

Finally, it considers the issuance and approval of interpretations developed from the end of the

Committee of IFRS interpretations.

All nations have their own accounting standards; however, for bringing comparability

and standardisation, the organisations like IASB have made attempts to develop a single standard

acceptable for maximum countries. Despite such attempts, it is not mandatory for the member

nations to converge into IFRS, since they have their own groups of accounting standards. Hence,

the IFRS convergence is not occurring in phases (Pelger 2016).

Owners’ Equity:

The four organisations that are selected for this section include BHP Billiton, Rio Tinto,

Orica Limited and Fortescue Metals Group.

Reason that IFRS is not compulsory for the member countries of IASB:

The IASB is a private and independent group, which formulates and approves IFRS. It

functions under the oversight of the foundation of IFRS. The IFRS Foundation is involved in

overseeing the operations conducted by IASB. The formulation of IASB dates back to 1901 for

replacing the ‘International Accounting Standards Committee (IASC)”. At present, IASB has 14

member nations and in accordance with the Constitution of the IFRS Foundation, IASB has full

accountability for all technical aspects of the foundation. These include complete discretion to

form and pursue its technical goal, which is subject to consulting needs with the public and the

trustees (Erb and Pelger 2015). Moreover, it takes into account the formulation and issuance of

IFRS as well as exposure drafts following the due procedure mentioned in the constitution.

Finally, it considers the issuance and approval of interpretations developed from the end of the

Committee of IFRS interpretations.

All nations have their own accounting standards; however, for bringing comparability

and standardisation, the organisations like IASB have made attempts to develop a single standard

acceptable for maximum countries. Despite such attempts, it is not mandatory for the member

nations to converge into IFRS, since they have their own groups of accounting standards. Hence,

the IFRS convergence is not occurring in phases (Pelger 2016).

Owners’ Equity:

The four organisations that are selected for this section include BHP Billiton, Rio Tinto,

Orica Limited and Fortescue Metals Group.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AND FINANCIAL ACCOUNTING

Answer to Question (iii):

In the statement of financial position of an entity, three significant items are apparent, out

of which is equity is one of them. As per this statement, the main items of equity include share

capital, reserves, treasury shares and retained earnings. Issued capital is considered as equity of

the business organisations (Benson et al. 2015). From the annual report of BHP Billiton, the

issued capital of BHP Billiton has fallen from $2,052 million in 2014 to $2,043 million in 2015,

which has remained constant in both the years 2016 and 2017. The issued capital of Rio Tinto

has fallen from $224 million in 2014 to $220 million in 2016, which has increased again to $224

million in 2016 and further to $230 million in 2017. For Orica Limited, the issued capital has

fallen from $1,975 million in 2014 to $1,954.4 million in 2015; however, it has increased to

$2,025.3 million in 2016 and $2,068.5 million in 2027. In case of Fortescue Metals Group, the

issued capital has risen from $1,289 million in 2014 to $1,294 million in 2015, which has

increased to $1,301 million in 2016 with further decline to $1,289 million in 2017. The variation

in issued capital is the outcome of the motive of maintaining an optimal capital structure for all

the business organisations.

The next item of equity for all the four organisations includes reserves. For BHP Billiton,

Rio Tinto and Fortescue Metals Group, the trend is fluctuating; however, the reserves of Orica

Limited seem to carry a negative amount. In the words of Marshall (2016), reserve is considered

as a part of equity obtained in excess of basic share capital. The main reason that Orica Limited

has negative reserves is due to the fact that it has accumulated business losses.

The final item of equity is considered as retained earnings. It signifies the earnings and

losses of an organisation from its establishment after paying out dividends to its shareholders

(Hoskin, Fizzell and Cherry 2014). The retained earnings for Orica Limited, BHP Billiton and

Answer to Question (iii):

In the statement of financial position of an entity, three significant items are apparent, out

of which is equity is one of them. As per this statement, the main items of equity include share

capital, reserves, treasury shares and retained earnings. Issued capital is considered as equity of

the business organisations (Benson et al. 2015). From the annual report of BHP Billiton, the

issued capital of BHP Billiton has fallen from $2,052 million in 2014 to $2,043 million in 2015,

which has remained constant in both the years 2016 and 2017. The issued capital of Rio Tinto

has fallen from $224 million in 2014 to $220 million in 2016, which has increased again to $224

million in 2016 and further to $230 million in 2017. For Orica Limited, the issued capital has

fallen from $1,975 million in 2014 to $1,954.4 million in 2015; however, it has increased to

$2,025.3 million in 2016 and $2,068.5 million in 2027. In case of Fortescue Metals Group, the

issued capital has risen from $1,289 million in 2014 to $1,294 million in 2015, which has

increased to $1,301 million in 2016 with further decline to $1,289 million in 2017. The variation

in issued capital is the outcome of the motive of maintaining an optimal capital structure for all

the business organisations.

The next item of equity for all the four organisations includes reserves. For BHP Billiton,

Rio Tinto and Fortescue Metals Group, the trend is fluctuating; however, the reserves of Orica

Limited seem to carry a negative amount. In the words of Marshall (2016), reserve is considered

as a part of equity obtained in excess of basic share capital. The main reason that Orica Limited

has negative reserves is due to the fact that it has accumulated business losses.

The final item of equity is considered as retained earnings. It signifies the earnings and

losses of an organisation from its establishment after paying out dividends to its shareholders

(Hoskin, Fizzell and Cherry 2014). The retained earnings for Orica Limited, BHP Billiton and

8CORPORATE AND FINANCIAL ACCOUNTING

Rio Tinto have declined over the years and the only exception could be observed in case of

Fortescue Metals Group where an increase could be witnessed over the years.

Therefore, it could be said that BHP Billiton accumulates more funds through equity

followed by Rio Tinto, Fortescue Metals Group and Orica Limited, since its asset base is the

largest among the four organisations operating in the mining industry of Australia.

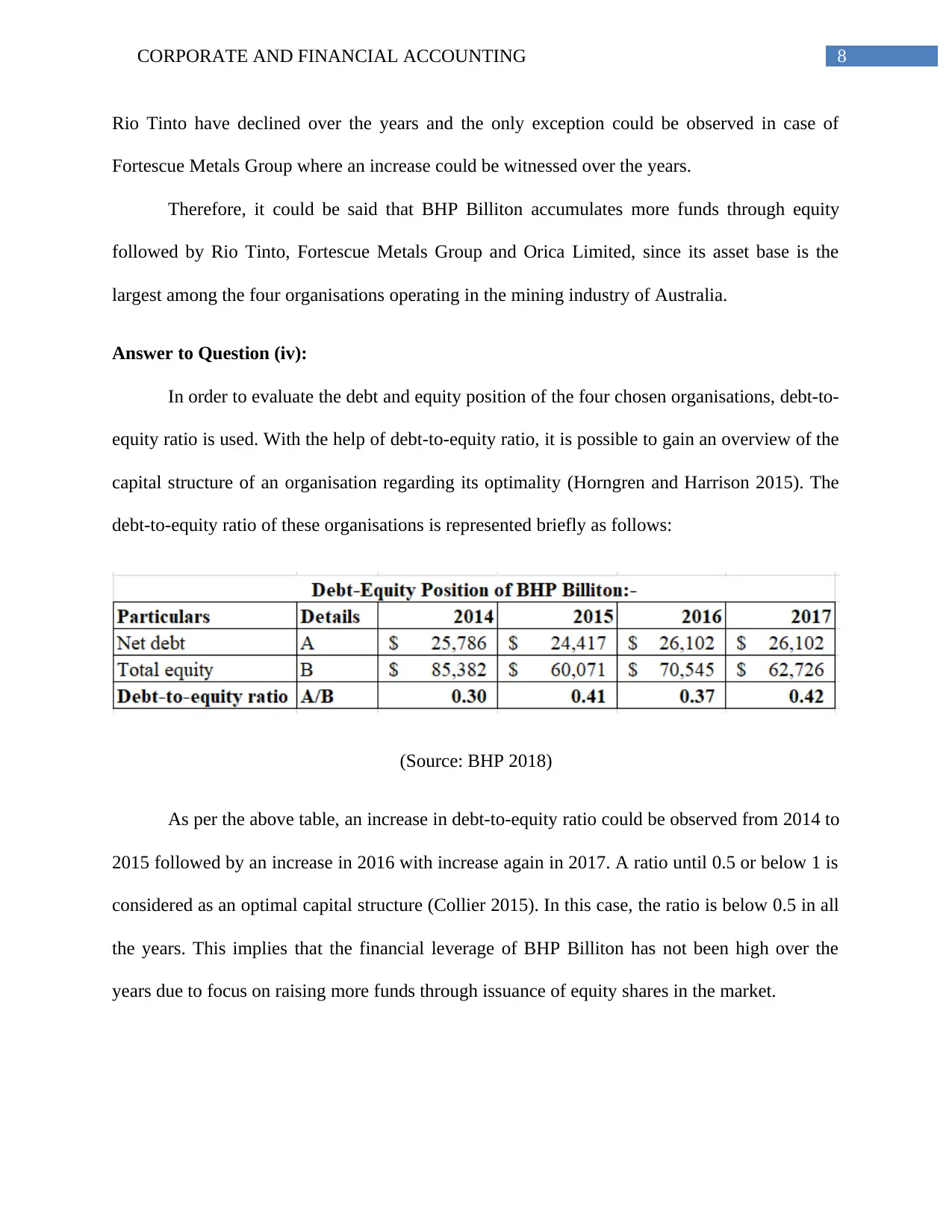

Answer to Question (iv):

In order to evaluate the debt and equity position of the four chosen organisations, debt-to-

equity ratio is used. With the help of debt-to-equity ratio, it is possible to gain an overview of the

capital structure of an organisation regarding its optimality (Horngren and Harrison 2015). The

debt-to-equity ratio of these organisations is represented briefly as follows:

(Source: BHP 2018)

As per the above table, an increase in debt-to-equity ratio could be observed from 2014 to

2015 followed by an increase in 2016 with increase again in 2017. A ratio until 0.5 or below 1 is

considered as an optimal capital structure (Collier 2015). In this case, the ratio is below 0.5 in all

the years. This implies that the financial leverage of BHP Billiton has not been high over the

years due to focus on raising more funds through issuance of equity shares in the market.

Rio Tinto have declined over the years and the only exception could be observed in case of

Fortescue Metals Group where an increase could be witnessed over the years.

Therefore, it could be said that BHP Billiton accumulates more funds through equity

followed by Rio Tinto, Fortescue Metals Group and Orica Limited, since its asset base is the

largest among the four organisations operating in the mining industry of Australia.

Answer to Question (iv):

In order to evaluate the debt and equity position of the four chosen organisations, debt-to-

equity ratio is used. With the help of debt-to-equity ratio, it is possible to gain an overview of the

capital structure of an organisation regarding its optimality (Horngren and Harrison 2015). The

debt-to-equity ratio of these organisations is represented briefly as follows:

(Source: BHP 2018)

As per the above table, an increase in debt-to-equity ratio could be observed from 2014 to

2015 followed by an increase in 2016 with increase again in 2017. A ratio until 0.5 or below 1 is

considered as an optimal capital structure (Collier 2015). In this case, the ratio is below 0.5 in all

the years. This implies that the financial leverage of BHP Billiton has not been high over the

years due to focus on raising more funds through issuance of equity shares in the market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE AND FINANCIAL ACCOUNTING

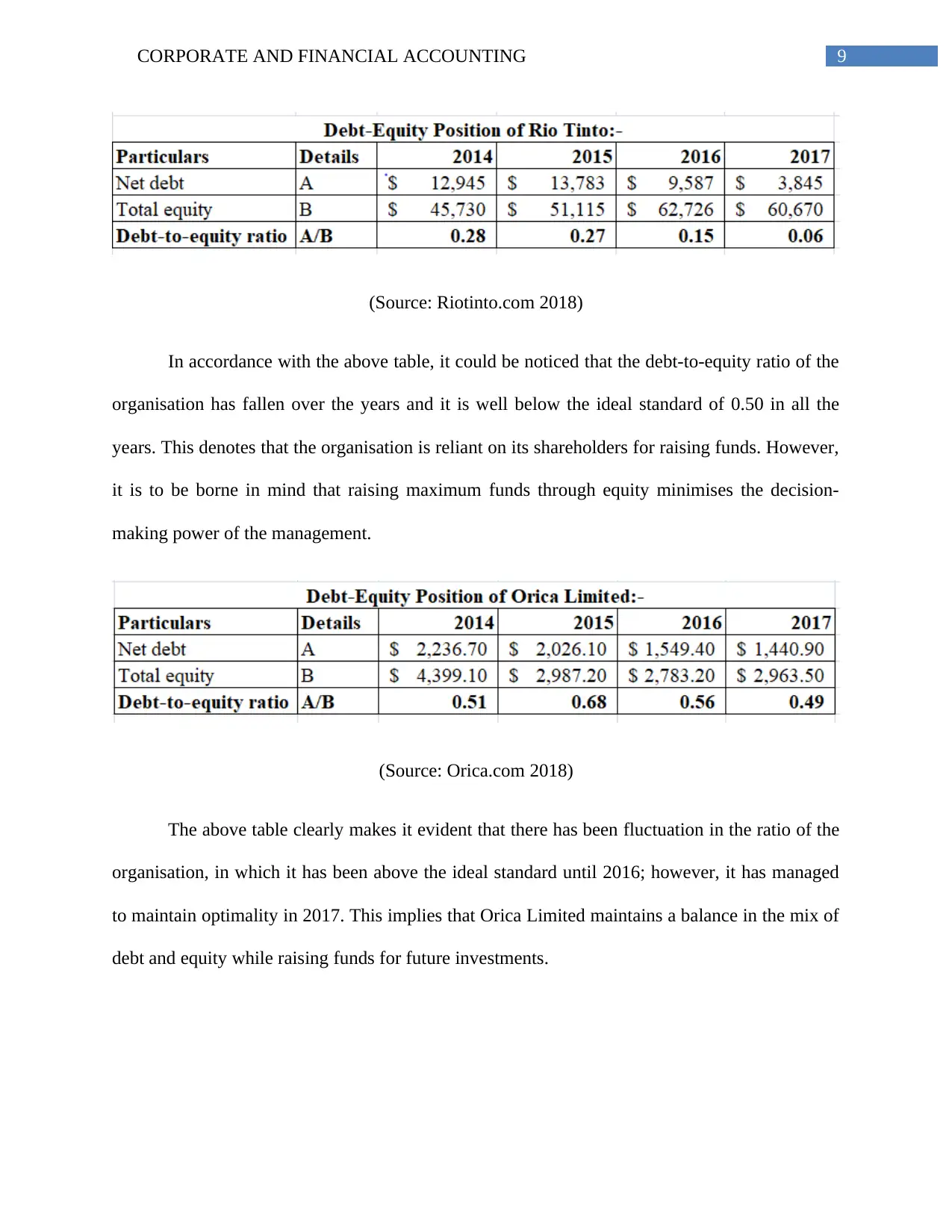

(Source: Riotinto.com 2018)

In accordance with the above table, it could be noticed that the debt-to-equity ratio of the

organisation has fallen over the years and it is well below the ideal standard of 0.50 in all the

years. This denotes that the organisation is reliant on its shareholders for raising funds. However,

it is to be borne in mind that raising maximum funds through equity minimises the decision-

making power of the management.

(Source: Orica.com 2018)

The above table clearly makes it evident that there has been fluctuation in the ratio of the

organisation, in which it has been above the ideal standard until 2016; however, it has managed

to maintain optimality in 2017. This implies that Orica Limited maintains a balance in the mix of

debt and equity while raising funds for future investments.

(Source: Riotinto.com 2018)

In accordance with the above table, it could be noticed that the debt-to-equity ratio of the

organisation has fallen over the years and it is well below the ideal standard of 0.50 in all the

years. This denotes that the organisation is reliant on its shareholders for raising funds. However,

it is to be borne in mind that raising maximum funds through equity minimises the decision-

making power of the management.

(Source: Orica.com 2018)

The above table clearly makes it evident that there has been fluctuation in the ratio of the

organisation, in which it has been above the ideal standard until 2016; however, it has managed

to maintain optimality in 2017. This implies that Orica Limited maintains a balance in the mix of

debt and equity while raising funds for future investments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE AND FINANCIAL ACCOUNTING

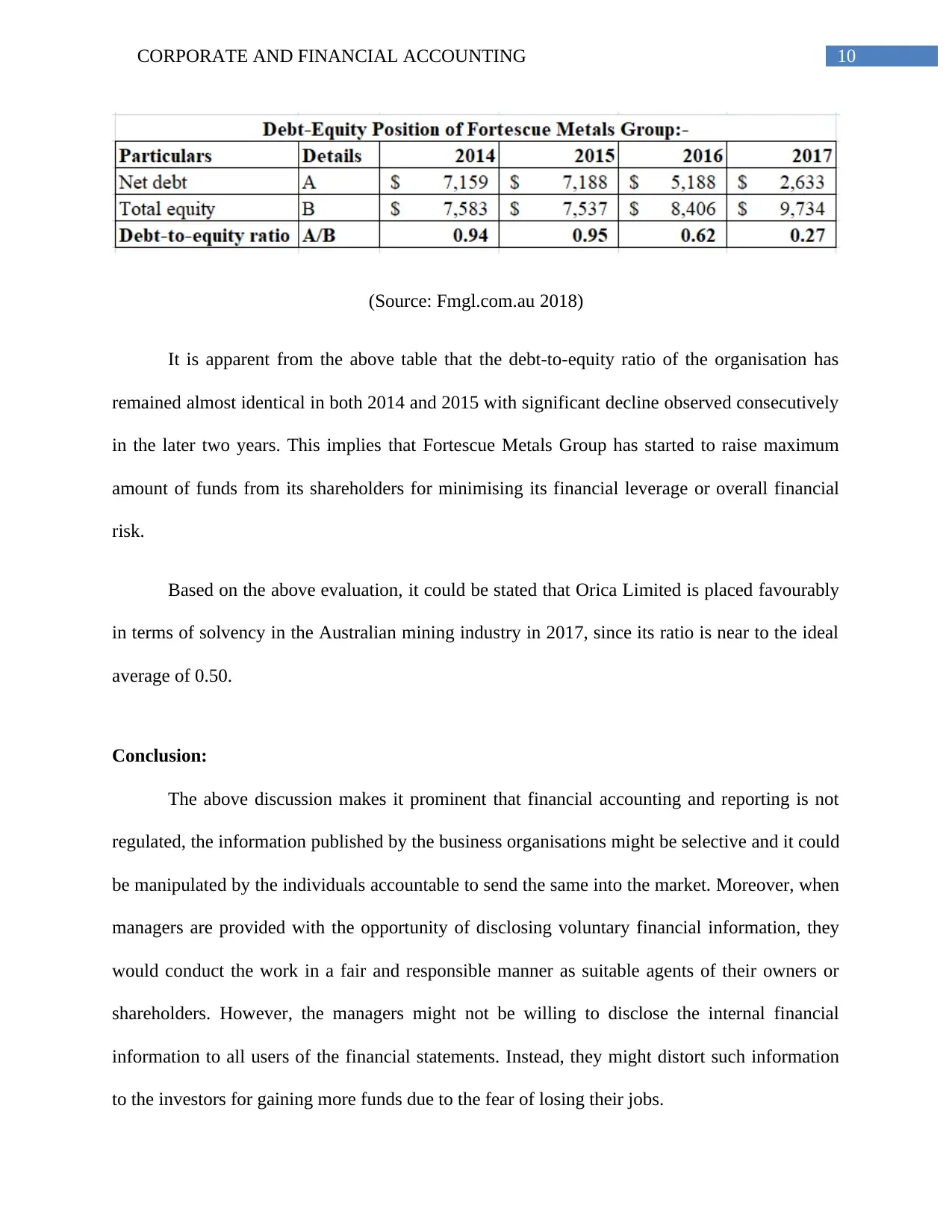

(Source: Fmgl.com.au 2018)

It is apparent from the above table that the debt-to-equity ratio of the organisation has

remained almost identical in both 2014 and 2015 with significant decline observed consecutively

in the later two years. This implies that Fortescue Metals Group has started to raise maximum

amount of funds from its shareholders for minimising its financial leverage or overall financial

risk.

Based on the above evaluation, it could be stated that Orica Limited is placed favourably

in terms of solvency in the Australian mining industry in 2017, since its ratio is near to the ideal

average of 0.50.

Conclusion:

The above discussion makes it prominent that financial accounting and reporting is not

regulated, the information published by the business organisations might be selective and it could

be manipulated by the individuals accountable to send the same into the market. Moreover, when

managers are provided with the opportunity of disclosing voluntary financial information, they

would conduct the work in a fair and responsible manner as suitable agents of their owners or

shareholders. However, the managers might not be willing to disclose the internal financial

information to all users of the financial statements. Instead, they might distort such information

to the investors for gaining more funds due to the fear of losing their jobs.

(Source: Fmgl.com.au 2018)

It is apparent from the above table that the debt-to-equity ratio of the organisation has

remained almost identical in both 2014 and 2015 with significant decline observed consecutively

in the later two years. This implies that Fortescue Metals Group has started to raise maximum

amount of funds from its shareholders for minimising its financial leverage or overall financial

risk.

Based on the above evaluation, it could be stated that Orica Limited is placed favourably

in terms of solvency in the Australian mining industry in 2017, since its ratio is near to the ideal

average of 0.50.

Conclusion:

The above discussion makes it prominent that financial accounting and reporting is not

regulated, the information published by the business organisations might be selective and it could

be manipulated by the individuals accountable to send the same into the market. Moreover, when

managers are provided with the opportunity of disclosing voluntary financial information, they

would conduct the work in a fair and responsible manner as suitable agents of their owners or

shareholders. However, the managers might not be willing to disclose the internal financial

information to all users of the financial statements. Instead, they might distort such information

to the investors for gaining more funds due to the fear of losing their jobs.

11CORPORATE AND FINANCIAL ACCOUNTING

It has been further evaluated that all nations have their own accounting standards;

however, for bringing comparability and standardisation, the organisations like IASB have made

attempts to develop a single standard acceptable for maximum countries. Despite such attempts,

it is not mandatory for the member nations to converge into IFRS, since they have their own

groups of accounting standards. Finally, it is found out that Orica Limited is placed in a better

position in the Australian mining sector in terms of debt and equity.

It has been further evaluated that all nations have their own accounting standards;

however, for bringing comparability and standardisation, the organisations like IASB have made

attempts to develop a single standard acceptable for maximum countries. Despite such attempts,

it is not mandatory for the member nations to converge into IFRS, since they have their own

groups of accounting standards. Finally, it is found out that Orica Limited is placed in a better

position in the Australian mining sector in terms of debt and equity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.