Analyzing the Global Financial Crisis: Causes, Impacts, and Solutions

VerifiedAdded on 2023/01/11

|10

|2588

|31

Essay

AI Summary

This essay provides an in-depth analysis of the Global Financial Crisis (GFC), exploring its origins in financial deregulation and the subprime mortgage market. It examines the role of institutions like Lehman Brothers and the impact on the global economy, including the significance of the inverted yield curve. The essay discusses the causes of the crisis, such as the housing bubble and the Federal Reserve's actions. It also covers the effects on consumer purchasing power, economic sentiment, and major economies like China and India. Furthermore, it highlights the responses of central banks, government policies, and the challenges in preventing future economic collapses. The essay concludes by emphasizing the importance of effective interventions, understanding the crisis's impact on different nations, and considering long-term consequences for monetary policy and financial support frameworks.

Essay response and analytical

response

response

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

MAIN BODY..................................................................................................................................1

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION

Analytical response also referred as a positive approach for reader, and it depending on

the context and how it tell the thoughts on any subject or concept based on any form of written

research, question or analysis. This essay is based on the Global Financial Crises (GFC) which

affects the overall word economy. It cover the several aspects such as cause of global financial

crises overall global economy, importance as well as impact of inverted yield curve in relation to

this crises. In addition, it includes the other several impacts which are related with the topic and

how government can resolve it through making effective policies.

MAIN BODY

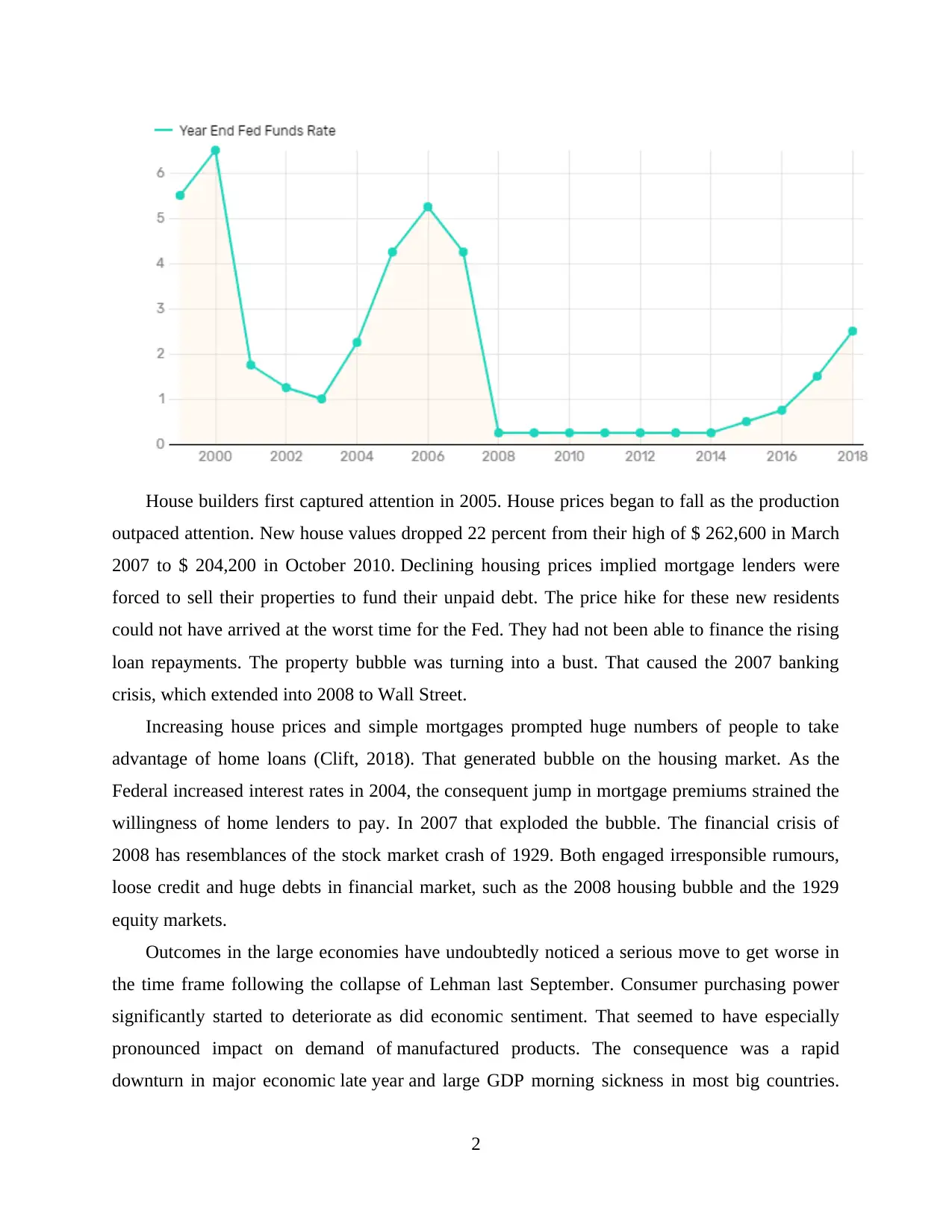

Global financial crisis was triggered largely by financial-sector deregulation. That allowed

people to offer in hedge fund financial derivatives. Financial institutions then requested more

mortgage loans to back these derivatives' profitable sales. They generated interest-only loans

which were accessible to lenders who were subprime. In 2004, even as the house prices on these

residential loans adjusted, the Federal Reserve increased the fed funds limit. Housing rates began

to decline in 2007, when demand outstripped supply. That stuck landowners who had not been

able to finance the payments but still couldn't sell their property. When the securities' prices

crumbled, lenders halted each other's borrowing.

Global financial crisis increased frequency after bankruptcy in September 2008, Lehman

Brothers made financial and economic situations very complicated for the international economy

such as for the global banking system and for central banks. For centralized banks and financial

regulatory structures, the collapse from the latest global financial crisis may be an era shifting

one. Therefore, it is absolutely critical that they correctly define the causes of the current

economic crisis so that together they can consider (Alqahtani and Mayes, 2018). First, effective

interventions and processes for urgent crisis resolution and second, recognize the gaps between

nations about how they are being affected. Finally, consider the longer-term consequences for

monetary policy and financial support frameworks.

1

Analytical response also referred as a positive approach for reader, and it depending on

the context and how it tell the thoughts on any subject or concept based on any form of written

research, question or analysis. This essay is based on the Global Financial Crises (GFC) which

affects the overall word economy. It cover the several aspects such as cause of global financial

crises overall global economy, importance as well as impact of inverted yield curve in relation to

this crises. In addition, it includes the other several impacts which are related with the topic and

how government can resolve it through making effective policies.

MAIN BODY

Global financial crisis was triggered largely by financial-sector deregulation. That allowed

people to offer in hedge fund financial derivatives. Financial institutions then requested more

mortgage loans to back these derivatives' profitable sales. They generated interest-only loans

which were accessible to lenders who were subprime. In 2004, even as the house prices on these

residential loans adjusted, the Federal Reserve increased the fed funds limit. Housing rates began

to decline in 2007, when demand outstripped supply. That stuck landowners who had not been

able to finance the payments but still couldn't sell their property. When the securities' prices

crumbled, lenders halted each other's borrowing.

Global financial crisis increased frequency after bankruptcy in September 2008, Lehman

Brothers made financial and economic situations very complicated for the international economy

such as for the global banking system and for central banks. For centralized banks and financial

regulatory structures, the collapse from the latest global financial crisis may be an era shifting

one. Therefore, it is absolutely critical that they correctly define the causes of the current

economic crisis so that together they can consider (Alqahtani and Mayes, 2018). First, effective

interventions and processes for urgent crisis resolution and second, recognize the gaps between

nations about how they are being affected. Finally, consider the longer-term consequences for

monetary policy and financial support frameworks.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

House builders first captured attention in 2005. House prices began to fall as the production

outpaced attention. New house values dropped 22 percent from their high of $ 262,600 in March

2007 to $ 204,200 in October 2010. Declining housing prices implied mortgage lenders were

forced to sell their properties to fund their unpaid debt. The price hike for these new residents

could not have arrived at the worst time for the Fed. They had not been able to finance the rising

loan repayments. The property bubble was turning into a bust. That caused the 2007 banking

crisis, which extended into 2008 to Wall Street.

Increasing house prices and simple mortgages prompted huge numbers of people to take

advantage of home loans (Clift, 2018). That generated bubble on the housing market. As the

Federal increased interest rates in 2004, the consequent jump in mortgage premiums strained the

willingness of home lenders to pay. In 2007 that exploded the bubble. The financial crisis of

2008 has resemblances of the stock market crash of 1929. Both engaged irresponsible rumours,

loose credit and huge debts in financial market, such as the 2008 housing bubble and the 1929

equity markets.

Outcomes in the large economies have undoubtedly noticed a serious move to get worse in

the time frame following the collapse of Lehman last September. Consumer purchasing power

significantly started to deteriorate as did economic sentiment. That seemed to have especially

pronounced impact on demand of manufactured products. The consequence was a rapid

downturn in major economic late year and large GDP morning sickness in most big countries.

2

outpaced attention. New house values dropped 22 percent from their high of $ 262,600 in March

2007 to $ 204,200 in October 2010. Declining housing prices implied mortgage lenders were

forced to sell their properties to fund their unpaid debt. The price hike for these new residents

could not have arrived at the worst time for the Fed. They had not been able to finance the rising

loan repayments. The property bubble was turning into a bust. That caused the 2007 banking

crisis, which extended into 2008 to Wall Street.

Increasing house prices and simple mortgages prompted huge numbers of people to take

advantage of home loans (Clift, 2018). That generated bubble on the housing market. As the

Federal increased interest rates in 2004, the consequent jump in mortgage premiums strained the

willingness of home lenders to pay. In 2007 that exploded the bubble. The financial crisis of

2008 has resemblances of the stock market crash of 1929. Both engaged irresponsible rumours,

loose credit and huge debts in financial market, such as the 2008 housing bubble and the 1929

equity markets.

Outcomes in the large economies have undoubtedly noticed a serious move to get worse in

the time frame following the collapse of Lehman last September. Consumer purchasing power

significantly started to deteriorate as did economic sentiment. That seemed to have especially

pronounced impact on demand of manufactured products. The consequence was a rapid

downturn in major economic late year and large GDP morning sickness in most big countries.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The markets of China and India started to expand but at lower levels. The signs are in the early

part of 2009 economic environment appeared very poor.

A variety of analysts have indicated that if the financial crisis extends, this might be a

sustained depression or bad. The continued growth of the recession sparked concerns of a major

economic crash. The financial crisis is expected to yield the largest selloff of banks since the

collapse of savings and loans. On October 6th, investment company UBS reported that 2008 will

see a strong global recession and its restoration impossible for at minimum two years.

UBS analysts declared that the "beginning of the peak" of the recession had ended, with the

economy starting to take the required steps to address the problem: policy infusion of capital;

financial intervention; exchange rate cuts to benefit lenders. The UK has introduced financial

inflation and central banks around the world also were slashing interest rates. UBS also

highlighted the need for the United States to introduce systematic injection. UBS also stressed

that this just addresses the banking crisis adding that "the worst has yet to come" in economic

terms. On October UBS quantified their predicted recession.

The European Union last two quarters, the US would last three quarters, and the UK can last

four-quarters (Chen, Matousek and Wanke, 2018). Iceland's economic downturn has affected all

two of the big banks in the world. Compared to the rest of its economy, the financial institution

collapse in Iceland is the biggest that any nation has survived in economic history.

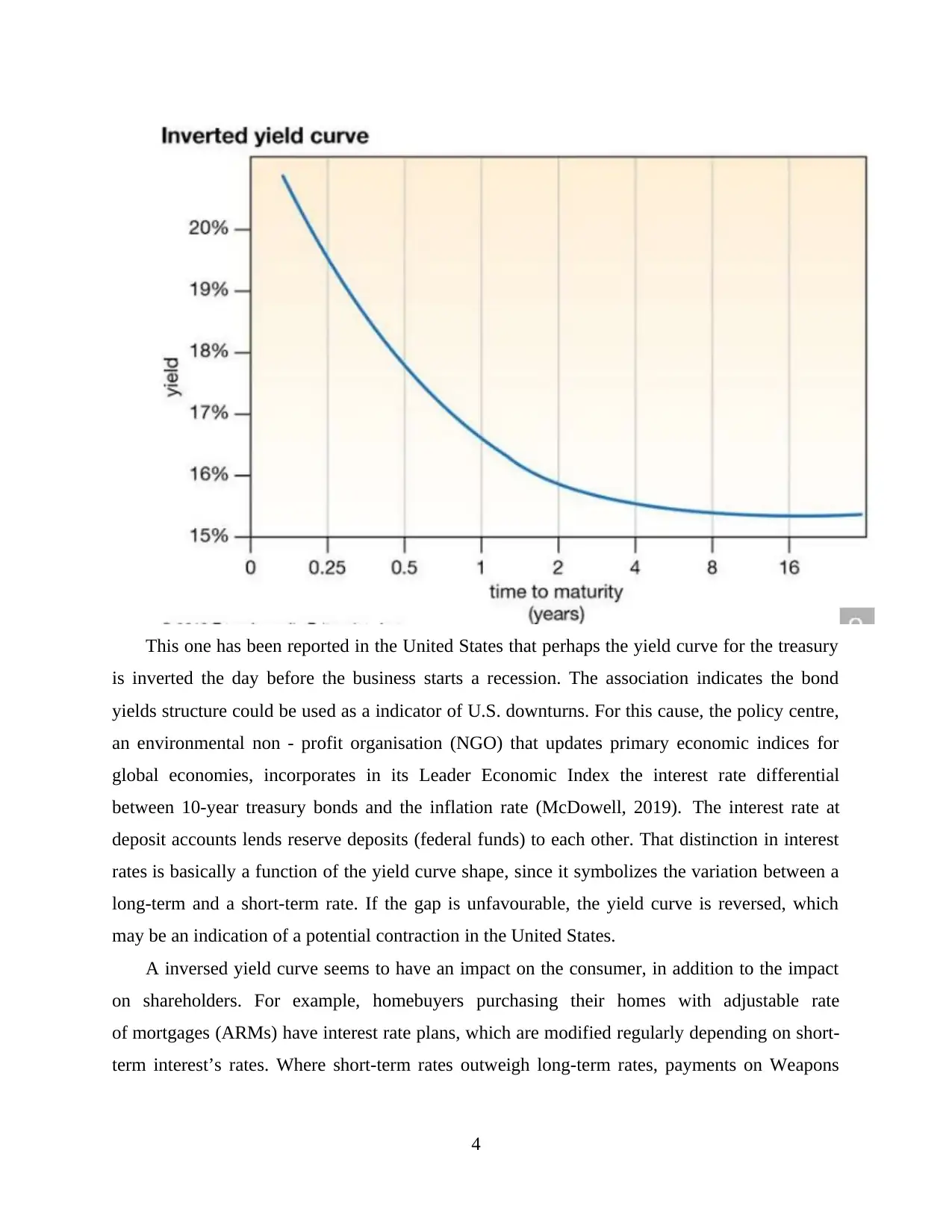

In economics and business, yield curve is a graph that demonstrates the rate of interest for a

specific debt securities related with various agreement lengths such as treasury bill. It describes

the connection between the borrowing term and the rate of inflation (yield) correlated with the

term. Because once long-term interest rates drop below short-term interest rates, there is an

inverted yield curve that also slopes downwards. Long-term creditors are ready to resolve for

lower returns in that rare scenario; likely since they think the financial outlook is grim.

3

part of 2009 economic environment appeared very poor.

A variety of analysts have indicated that if the financial crisis extends, this might be a

sustained depression or bad. The continued growth of the recession sparked concerns of a major

economic crash. The financial crisis is expected to yield the largest selloff of banks since the

collapse of savings and loans. On October 6th, investment company UBS reported that 2008 will

see a strong global recession and its restoration impossible for at minimum two years.

UBS analysts declared that the "beginning of the peak" of the recession had ended, with the

economy starting to take the required steps to address the problem: policy infusion of capital;

financial intervention; exchange rate cuts to benefit lenders. The UK has introduced financial

inflation and central banks around the world also were slashing interest rates. UBS also

highlighted the need for the United States to introduce systematic injection. UBS also stressed

that this just addresses the banking crisis adding that "the worst has yet to come" in economic

terms. On October UBS quantified their predicted recession.

The European Union last two quarters, the US would last three quarters, and the UK can last

four-quarters (Chen, Matousek and Wanke, 2018). Iceland's economic downturn has affected all

two of the big banks in the world. Compared to the rest of its economy, the financial institution

collapse in Iceland is the biggest that any nation has survived in economic history.

In economics and business, yield curve is a graph that demonstrates the rate of interest for a

specific debt securities related with various agreement lengths such as treasury bill. It describes

the connection between the borrowing term and the rate of inflation (yield) correlated with the

term. Because once long-term interest rates drop below short-term interest rates, there is an

inverted yield curve that also slopes downwards. Long-term creditors are ready to resolve for

lower returns in that rare scenario; likely since they think the financial outlook is grim.

3

This one has been reported in the United States that perhaps the yield curve for the treasury

is inverted the day before the business starts a recession. The association indicates the bond

yields structure could be used as a indicator of U.S. downturns. For this cause, the policy centre,

an environmental non - profit organisation (NGO) that updates primary economic indices for

global economies, incorporates in its Leader Economic Index the interest rate differential

between 10-year treasury bonds and the inflation rate (McDowell, 2019). The interest rate at

deposit accounts lends reserve deposits (federal funds) to each other. That distinction in interest

rates is basically a function of the yield curve shape, since it symbolizes the variation between a

long-term and a short-term rate. If the gap is unfavourable, the yield curve is reversed, which

may be an indication of a potential contraction in the United States.

A inversed yield curve seems to have an impact on the consumer, in addition to the impact

on shareholders. For example, homebuyers purchasing their homes with adjustable rate

of mortgages (ARMs) have interest rate plans, which are modified regularly depending on short-

term interest’s rates. Where short-term rates outweigh long-term rates, payments on Weapons

4

is inverted the day before the business starts a recession. The association indicates the bond

yields structure could be used as a indicator of U.S. downturns. For this cause, the policy centre,

an environmental non - profit organisation (NGO) that updates primary economic indices for

global economies, incorporates in its Leader Economic Index the interest rate differential

between 10-year treasury bonds and the inflation rate (McDowell, 2019). The interest rate at

deposit accounts lends reserve deposits (federal funds) to each other. That distinction in interest

rates is basically a function of the yield curve shape, since it symbolizes the variation between a

long-term and a short-term rate. If the gap is unfavourable, the yield curve is reversed, which

may be an indication of a potential contraction in the United States.

A inversed yield curve seems to have an impact on the consumer, in addition to the impact

on shareholders. For example, homebuyers purchasing their homes with adjustable rate

of mortgages (ARMs) have interest rate plans, which are modified regularly depending on short-

term interest’s rates. Where short-term rates outweigh long-term rates, payments on Weapons

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

continue to rise. Fixed rate mortgages can be more appealing as that happens than adjustable-rate

loans.

Credit lines are also affected. In both cases, consumers have to devote a greater proportion

of income to refurbishing existing debt (Cassis and Wójcik, 2018). This decreases dispensable

resources and has a detrimental effect on the entire economy.

Inverted yield curve is important for at least two major reasons. Firstly, it provides insight

into what those shareholders see in the economic system as a whole. If you think free

convergence speed, then the cumulative viewpoint of all market players is the best proof of what

was really heading on. This principle is analogous to our judicial system’s belief that twelve

judges are much more willing to sift through facts than either one or two and decide a rational

conclusion of a trial. The argument is that if the company is not expecting growth prospects in

the future, they pay more consideration.

Second reason is why inverted yield curve is important in relation to financial crises. The

yield curve does have a major effect on the economic supply of money. A further way of putting

it down would be that the yield curve impacts people and companies' ability to get regular bank

loans. Banks take funds, either through the Federal Reserve Discount Window or from its

borrowers at short term rates. Also it goes around rather than borrows money at low rates for

people like you and me. If, due to concerns about economic growth, the economy doesn't need

higher yields (yield premium), instead banks are pressured to invest money at lower yields. As a

result, the financial institutions cannot make quite enough profits and its earnings are squeezed.

In a really true sense, low motivation influences the banks and its need to lend money, the

flatterer the curve. Loan payments are a risk to a financial institution and if it can't make any

money to take the risk, bankers will stop taking the risk and discontinue making loans. The

economy will suffer as banks avoid issuing loans, or render the terms of the contract so stringent

that customers and firms cannot borrow. People are not allowed to buy homes and cars. Business

owners cannot spend, so they can not expand (Höllerer, Jancsary and Grafström, 2018). The

country is at a standstill. The yield curve thus has become a curved prophecy which fulfils itself

in many ways.

Securitisation was a risk-management attempt. Amount of tries were made to mitigate that

risk, or to underwrite against issues. Although these are valid things to do, the mechanisms that

enable this to occur have also helped bring on the existing problems.

5

loans.

Credit lines are also affected. In both cases, consumers have to devote a greater proportion

of income to refurbishing existing debt (Cassis and Wójcik, 2018). This decreases dispensable

resources and has a detrimental effect on the entire economy.

Inverted yield curve is important for at least two major reasons. Firstly, it provides insight

into what those shareholders see in the economic system as a whole. If you think free

convergence speed, then the cumulative viewpoint of all market players is the best proof of what

was really heading on. This principle is analogous to our judicial system’s belief that twelve

judges are much more willing to sift through facts than either one or two and decide a rational

conclusion of a trial. The argument is that if the company is not expecting growth prospects in

the future, they pay more consideration.

Second reason is why inverted yield curve is important in relation to financial crises. The

yield curve does have a major effect on the economic supply of money. A further way of putting

it down would be that the yield curve impacts people and companies' ability to get regular bank

loans. Banks take funds, either through the Federal Reserve Discount Window or from its

borrowers at short term rates. Also it goes around rather than borrows money at low rates for

people like you and me. If, due to concerns about economic growth, the economy doesn't need

higher yields (yield premium), instead banks are pressured to invest money at lower yields. As a

result, the financial institutions cannot make quite enough profits and its earnings are squeezed.

In a really true sense, low motivation influences the banks and its need to lend money, the

flatterer the curve. Loan payments are a risk to a financial institution and if it can't make any

money to take the risk, bankers will stop taking the risk and discontinue making loans. The

economy will suffer as banks avoid issuing loans, or render the terms of the contract so stringent

that customers and firms cannot borrow. People are not allowed to buy homes and cars. Business

owners cannot spend, so they can not expand (Höllerer, Jancsary and Grafström, 2018). The

country is at a standstill. The yield curve thus has become a curved prophecy which fulfils itself

in many ways.

Securitisation was a risk-management attempt. Amount of tries were made to mitigate that

risk, or to underwrite against issues. Although these are valid things to do, the mechanisms that

enable this to occur have also helped bring on the existing problems.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Essentially, what must have occurred was that financial institutions, hedge funds and many

others have become overly confident because they all assumed they would have figured out

where to take risks and make funds more efficiently. When they eventually made a lot more

money undertaking more risks, they strengthened their own belief that they would have worked

it out (Shahzad and et.al, 2018). They assumed they had efficiently stretched all of their dangers

and yet when this really goes awry, it all went horribly wrong. For eg, the demand for

collateralized debt obligations (an investment option on whether a company defaults) was

massive, approaching the total $ 50 trillion world economic production by summer 2008. It had

also been badly managed. At the moment, AIG alone, the nation's biggest insurance and

reinsurance firm, had collateralized debt obligations of around $ 400 billion that is much exposed

and little legislation. In addition, many of AIG's collateralized debt obligations were all on

mortgages, which naturally started going downhill. The commerce in such swaps developed an

amazing web of interconnected frameworks; a joint only as powerful as the weak point. Any

problem, like risk or actual substantial loss, could rapidly spread. The US government

subsequently rescue the (now about $150bn) AIG to keep them from collapsing.

Defensive players provide financial flexibility, crisis-fighting strategies and governmental

regulations, all brought in motion following the global financial crisis. However, as things now

stand, there is also no assurance that they can manage to prevent a contraction of the "garden

variety" from being another full-blown economic collapse. There is significant controversy on

monetary policy as to how central banks can react to a profound or sustained downturn. For

example, past US downturns have encountered with 500 percentage points or so of Federal

Reserve loosening and the central banks are using their balance sheet heavily in the global

financial crisis (Taranova and et.al, 2018). However, for policy levels in so many places still too

small and measurement session normalization still ongoing, the same policy solution could not

be possible. A next layer of defence is fiscal policy, where several researchers insist that

throughout the developed economies the bed for manoeuvre has narrowed.

CONCLUSION

From the above discussion it has been observed that, global financial crises occur due to

depreciation in the U.S. subprime mortgage industry and the failure of Investment Company

such as Lehman Brothers on September 15, 2008 and it turned into a global financial crisis. It

causes the several economics in different ways which become hard to recover, where

6

others have become overly confident because they all assumed they would have figured out

where to take risks and make funds more efficiently. When they eventually made a lot more

money undertaking more risks, they strengthened their own belief that they would have worked

it out (Shahzad and et.al, 2018). They assumed they had efficiently stretched all of their dangers

and yet when this really goes awry, it all went horribly wrong. For eg, the demand for

collateralized debt obligations (an investment option on whether a company defaults) was

massive, approaching the total $ 50 trillion world economic production by summer 2008. It had

also been badly managed. At the moment, AIG alone, the nation's biggest insurance and

reinsurance firm, had collateralized debt obligations of around $ 400 billion that is much exposed

and little legislation. In addition, many of AIG's collateralized debt obligations were all on

mortgages, which naturally started going downhill. The commerce in such swaps developed an

amazing web of interconnected frameworks; a joint only as powerful as the weak point. Any

problem, like risk or actual substantial loss, could rapidly spread. The US government

subsequently rescue the (now about $150bn) AIG to keep them from collapsing.

Defensive players provide financial flexibility, crisis-fighting strategies and governmental

regulations, all brought in motion following the global financial crisis. However, as things now

stand, there is also no assurance that they can manage to prevent a contraction of the "garden

variety" from being another full-blown economic collapse. There is significant controversy on

monetary policy as to how central banks can react to a profound or sustained downturn. For

example, past US downturns have encountered with 500 percentage points or so of Federal

Reserve loosening and the central banks are using their balance sheet heavily in the global

financial crisis (Taranova and et.al, 2018). However, for policy levels in so many places still too

small and measurement session normalization still ongoing, the same policy solution could not

be possible. A next layer of defence is fiscal policy, where several researchers insist that

throughout the developed economies the bed for manoeuvre has narrowed.

CONCLUSION

From the above discussion it has been observed that, global financial crises occur due to

depreciation in the U.S. subprime mortgage industry and the failure of Investment Company

such as Lehman Brothers on September 15, 2008 and it turned into a global financial crisis. It

causes the several economics in different ways which become hard to recover, where

6

government introduce suitable monetary or financial policies to mitigate the risk or future

collapse.

7

collapse.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books & Journals

Alqahtani, F. and Mayes, D.G., 2018. Financial stability of Islamic banking and the global

financial crisis: Evidence from the Gulf Cooperation Council. Economic Systems, 42(2),

pp.346-360.

Clift, B., 2018. The IMF and the Politics of Austerity in the Wake of the Global Financial Crisis.

Oxford University Press.

Chen, Z., Matousek, R. and Wanke, P., 2018. Chinese bank efficiency during the global financial

crisis: A combined approach using satisficing DEA and Support Vector Machines☆. The

North American Journal of Economics and Finance, 43, pp.71-86.

McDowell, D., 2019. Emergent international liquidity agreements: central bank cooperation after

the global financial crisis. Journal of International Relations and Development, 22(2),

pp.441-467.

Cassis, Y. and Wójcik, D. eds., 2018. International financial centres after the global financial

crisis and Brexit. Oxford University Press.

Höllerer, M.A., Jancsary, D. and Grafström, M., 2018. ‘A picture is worth a thousand words’:

Multimodal sensemaking of the global financial crisis. Organization Studies, 39(5-6),

pp.617-644.

Shahzad, K., and et.al, 2018. Audit quality during the global financial crisis: The investors’

perspective. Research in International Business and Finance, 45, pp.94-105.

Taranova, I.V., and et.al, 2018. Global financial and economic crisis in Russia: trends and

prospects. Research Journal of Pharmaceutical, Biological and Chemical Sciences, 9(6),

pp.769-775.

8

Books & Journals

Alqahtani, F. and Mayes, D.G., 2018. Financial stability of Islamic banking and the global

financial crisis: Evidence from the Gulf Cooperation Council. Economic Systems, 42(2),

pp.346-360.

Clift, B., 2018. The IMF and the Politics of Austerity in the Wake of the Global Financial Crisis.

Oxford University Press.

Chen, Z., Matousek, R. and Wanke, P., 2018. Chinese bank efficiency during the global financial

crisis: A combined approach using satisficing DEA and Support Vector Machines☆. The

North American Journal of Economics and Finance, 43, pp.71-86.

McDowell, D., 2019. Emergent international liquidity agreements: central bank cooperation after

the global financial crisis. Journal of International Relations and Development, 22(2),

pp.441-467.

Cassis, Y. and Wójcik, D. eds., 2018. International financial centres after the global financial

crisis and Brexit. Oxford University Press.

Höllerer, M.A., Jancsary, D. and Grafström, M., 2018. ‘A picture is worth a thousand words’:

Multimodal sensemaking of the global financial crisis. Organization Studies, 39(5-6),

pp.617-644.

Shahzad, K., and et.al, 2018. Audit quality during the global financial crisis: The investors’

perspective. Research in International Business and Finance, 45, pp.94-105.

Taranova, I.V., and et.al, 2018. Global financial and economic crisis in Russia: trends and

prospects. Research Journal of Pharmaceutical, Biological and Chemical Sciences, 9(6),

pp.769-775.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.