Analysis of the Global Financial Crisis: Causes and Economic Outcomes

VerifiedAdded on 2019/11/12

|12

|2512

|213

Report

AI Summary

This report provides a comprehensive analysis of the Global Financial Crisis, examining its causes and consequences. The report delves into the factors that led to the crisis, including the burst of the subprime mortgage bubble, the credit crunch, national debt and budget deficits, low interest rates, the housing market crash, devaluation of the dollar, and the collapse of Lehman Brothers. It also explores the economic business cycles and indicators. The report further discusses the consequences of the crisis on the labor market, housing market, and the overall economy. The report concludes by emphasizing the importance of understanding the crisis and its impact on demand and policy, highlighting the need for sustainable economic practices. The report is a detailed study on the great recession and provides insights into the complex events that led to the financial downturn and its lasting effects on the global economy.

Running Head: Global Financial Crisis

Name

Professor

Institution

Course

Date

Global Financial Crisis Due To US

Name

Professor

Institution

Course

Date

Global Financial Crisis Due To US

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Global Financial Crisis 2

The Global Financial Crisis which is caused due to USA

The global monetary crisis, generally denoting the US 2008 great recession was caused

by numerous factors, all taking place simultaneously and at the end led to a severe decline in the

entire global economy .Financial crisis are usually characterized by declined inflations and rising

of the rates of unemployment. These financial states follow periods of high growth in economy

also referred to as boom (Scott, 2013).

This global fiscal crisis devastated both trade and consumers’ self-assurance in several

countries. Considering its severe effects it was termed as great recession and led to high financial

meltdown spreading out at an alarming rate in every corner of the whole world. It was noted as

the most horrible case of the economic slump after the huge global depression faced following

the Second World War (Scott, 2013).

In regard to many economists, this global financial crisis mainly came up because of the

abrupt busting of house bubble in US, caused by the fast growth of flawed directives of sub -

prime mortgages. In order to understand this global financial crisis, this research has analyzed

both the consequences and causes of this great financial crisis (Scott, 2013).

Business cycle vs. Global Financial Crisis

Business cycles comprises of periodic variations in economic activities, such as

production and employment. The usual cycle entails a rise in an activity up to when it reaches its

highest point or peak, and then followed by a drop in both the output and employment till the

economy reaches its low point, referred to as a trough (Scott, 2013).

The Global Financial Crisis which is caused due to USA

The global monetary crisis, generally denoting the US 2008 great recession was caused

by numerous factors, all taking place simultaneously and at the end led to a severe decline in the

entire global economy .Financial crisis are usually characterized by declined inflations and rising

of the rates of unemployment. These financial states follow periods of high growth in economy

also referred to as boom (Scott, 2013).

This global fiscal crisis devastated both trade and consumers’ self-assurance in several

countries. Considering its severe effects it was termed as great recession and led to high financial

meltdown spreading out at an alarming rate in every corner of the whole world. It was noted as

the most horrible case of the economic slump after the huge global depression faced following

the Second World War (Scott, 2013).

In regard to many economists, this global financial crisis mainly came up because of the

abrupt busting of house bubble in US, caused by the fast growth of flawed directives of sub -

prime mortgages. In order to understand this global financial crisis, this research has analyzed

both the consequences and causes of this great financial crisis (Scott, 2013).

Business cycle vs. Global Financial Crisis

Business cycles comprises of periodic variations in economic activities, such as

production and employment. The usual cycle entails a rise in an activity up to when it reaches its

highest point or peak, and then followed by a drop in both the output and employment till the

economy reaches its low point, referred to as a trough (Scott, 2013).

Global Financial Crisis 3

In reference to the Austrian business cycle theory, economic growth is viable if it comes

as a result of increased investment funded by higher savings. Contrary to this, financial bang that

is as a result of growth in credit is unsustainable. In the cases where the creation of credit made

by the financial system surpasses the rate of saving by the society, the monetary mediators end

up giving out loans at rates of interest which are below the standards where market forces clear

in the market. Information is hence attached in marketplace prices is misleading, affecting

entrepreneurial decisions and causes improper allocation of the resources in the entire economy

(Reinhart & Rogoff, 2013).

As a result, many capital goods and inadequate consumer goods will are produced in

relation to the final consumer inclinations. As the capital goods miss out on demand, production

capacity runs dormant and the boom caused by the credit expansion bust.The 2002-2007

expansion was described by both accommodation and the residential real estate boom. This

boom ascertained to be unsustainable and closely followed by bust in both financial markets and

economy at large which led to the global financial crisis commonly referred to as the great

recession (Crotty, 2013).

Economic business sequence indicators

Business sequences are hard to foresee, but some gauges, referred to as indicators, are

able to give indications to business managers, shareholders, and the officials of the

administration officials on the state of commerce cycles. Three main categories of business cycle

indicators have been pointed out founded on timing: leading indicators, coincident indicators and

lagging indicators. These indicators are put in place mainly to foresee both the troughs and peaks

In reference to the Austrian business cycle theory, economic growth is viable if it comes

as a result of increased investment funded by higher savings. Contrary to this, financial bang that

is as a result of growth in credit is unsustainable. In the cases where the creation of credit made

by the financial system surpasses the rate of saving by the society, the monetary mediators end

up giving out loans at rates of interest which are below the standards where market forces clear

in the market. Information is hence attached in marketplace prices is misleading, affecting

entrepreneurial decisions and causes improper allocation of the resources in the entire economy

(Reinhart & Rogoff, 2013).

As a result, many capital goods and inadequate consumer goods will are produced in

relation to the final consumer inclinations. As the capital goods miss out on demand, production

capacity runs dormant and the boom caused by the credit expansion bust.The 2002-2007

expansion was described by both accommodation and the residential real estate boom. This

boom ascertained to be unsustainable and closely followed by bust in both financial markets and

economy at large which led to the global financial crisis commonly referred to as the great

recession (Crotty, 2013).

Economic business sequence indicators

Business sequences are hard to foresee, but some gauges, referred to as indicators, are

able to give indications to business managers, shareholders, and the officials of the

administration officials on the state of commerce cycles. Three main categories of business cycle

indicators have been pointed out founded on timing: leading indicators, coincident indicators and

lagging indicators. These indicators are put in place mainly to foresee both the troughs and peaks

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Global Financial Crisis 4

of trade cycles in the USA and other 10 nations around the world, including Australia, China,

Germany, France and Mexico (Scott, 201).

Leading indicators

They are measures of the financial activities whereby the shifts can foretell the start of a

business cycle. Some of the leading pointers comprise and not limited to weekly average

working time in manufacturing sector, the order of goods placed by factories and the stock

prices. A rise or turn down in these measures could send an indication on the commencement of

a business cycle. These indicators are given much concentration due to their behavior to shift in

go forward of business cycles (Scott, 2013).

Lagging indicators

Lagging indicators entails the measures varying after the market has already gone into an era of

variation. These indicators are: the standard unemployment length, the cost of labor per

manufacturing unit productivity, standard prime rate, customer price index and the profitable

loaning activities. These indicators are ignored sometimes because of their tendency to change

the direction after the economy moves into a business cycle. However, they can give valuable

insights on structural economy problems (Scott, 2013).

Coincident indicators

They usually consist of the aggregate financial activity measures that adjust with the

advancement in the trade cycle. They aid in the definition of business cycles. Examples of these

indicators are the rate of unemployment, industrial production and the levels of personal incomes

(Crotty, 2013).

of trade cycles in the USA and other 10 nations around the world, including Australia, China,

Germany, France and Mexico (Scott, 201).

Leading indicators

They are measures of the financial activities whereby the shifts can foretell the start of a

business cycle. Some of the leading pointers comprise and not limited to weekly average

working time in manufacturing sector, the order of goods placed by factories and the stock

prices. A rise or turn down in these measures could send an indication on the commencement of

a business cycle. These indicators are given much concentration due to their behavior to shift in

go forward of business cycles (Scott, 2013).

Lagging indicators

Lagging indicators entails the measures varying after the market has already gone into an era of

variation. These indicators are: the standard unemployment length, the cost of labor per

manufacturing unit productivity, standard prime rate, customer price index and the profitable

loaning activities. These indicators are ignored sometimes because of their tendency to change

the direction after the economy moves into a business cycle. However, they can give valuable

insights on structural economy problems (Scott, 2013).

Coincident indicators

They usually consist of the aggregate financial activity measures that adjust with the

advancement in the trade cycle. They aid in the definition of business cycles. Examples of these

indicators are the rate of unemployment, industrial production and the levels of personal incomes

(Crotty, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Global Financial Crisis 5

Causes of the Global financial crisis

In response to this crucial question, most of the Americans are likely to mention

something to do with subprime mortgages, bankruptcy of the Lehman brothers, or the Wall

Street greed. But these were these factors really enough to cause such a catastrophic economic

downturn? While these risky mortgages and dubious financial market activities played a very

important role in fueling the conditions which later on brought such an economic collapse, there

exist other structural problems mainly with the manner in which the US economy created the

demand growth in the decades preceding to this great recession (Scott, 2013). These underlying

factors generated conditions that made this crisis almost inevitable. They include;

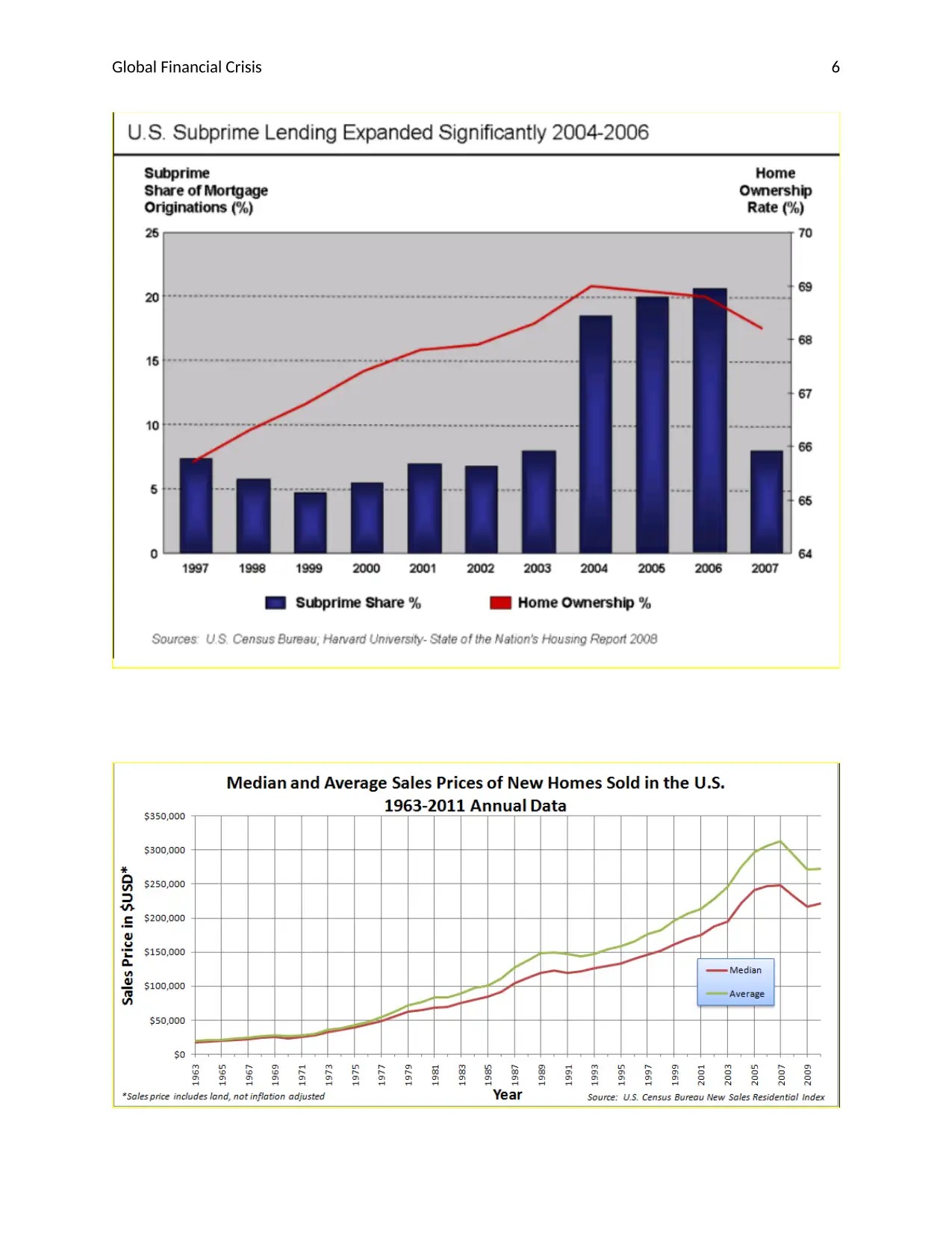

The burst of Subprime mortgages and housing bubble.

It is very clear that there were no regulations to govern the subprime mortgages and

where these mortgage companies could trade mortgages without considering whether the buyers

could pay back. On March 2007 it is predicted that the subprime mortgages in US was at $1.3

trillion and also with about 7.5 million unsettled subprime mortgages. This was due to subprime

mortgage rising to almost 21% of the entire origination of mortgage via the climax of the

housing bubble of the US. The enormous majority of subprime mortgages were as a result of

massive foreclosures hence greatly affecting the institutions and the individual mortgage brokers

who were not under Community Reinvestment Act cover. It thus indirectly led to a slow growth

and started a fall on the consumer spending and investment (Scott, 2013).

Causes of the Global financial crisis

In response to this crucial question, most of the Americans are likely to mention

something to do with subprime mortgages, bankruptcy of the Lehman brothers, or the Wall

Street greed. But these were these factors really enough to cause such a catastrophic economic

downturn? While these risky mortgages and dubious financial market activities played a very

important role in fueling the conditions which later on brought such an economic collapse, there

exist other structural problems mainly with the manner in which the US economy created the

demand growth in the decades preceding to this great recession (Scott, 2013). These underlying

factors generated conditions that made this crisis almost inevitable. They include;

The burst of Subprime mortgages and housing bubble.

It is very clear that there were no regulations to govern the subprime mortgages and

where these mortgage companies could trade mortgages without considering whether the buyers

could pay back. On March 2007 it is predicted that the subprime mortgages in US was at $1.3

trillion and also with about 7.5 million unsettled subprime mortgages. This was due to subprime

mortgage rising to almost 21% of the entire origination of mortgage via the climax of the

housing bubble of the US. The enormous majority of subprime mortgages were as a result of

massive foreclosures hence greatly affecting the institutions and the individual mortgage brokers

who were not under Community Reinvestment Act cover. It thus indirectly led to a slow growth

and started a fall on the consumer spending and investment (Scott, 2013).

Global Financial Crisis 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Global Financial Crisis 7

The Credit Crunch

The high subprime mortgages evasions had caused credit crunch which narrowed to an

abrupt shortage of money and hence resulting to decline in the available lends by the banks.

Many commercial and even investment banks went through massive losses as a result of these

mortgage loans. Banks as a result became very reluctant to give out loans to people and even

other banks leading to a decline in funds circulating in money markets (Scott, 2013).

National debt and the Budget deficit

In the year 2007 the US debt was reading 65 percent of the GDP and became even worse

after the inclusion of pension liabilities. At such a huge budget arrears the government of the

United States automatically had a small fiscal policy expansion capability since the

demographics were against the fiscal stability hence worsening the deficit. This budget deficit

led to challenges in attracting the flow of capital as the Asian investors who were aware of this

deficit reduced the capital flow to US leading to devaluation of the dollar (Scott, 2013).

The Low interest rate

The monetary authorities in US had accustomed the rates of interest to strange levels

leading to a boom in debt-finance consumption which led its way all through to boosting the

housing bubble. It is also claimed that the interest rates in US were stayed too low for a very long

time to an extent of even standing at 1 percent in 2003 and 2004. This activated the great

financial crisis. The monetary policy in US is also criticized for its failure to undertake the

overrated benefit bubble while backing up the fast expansion in subprime mortgages

(Shiller,2012).

The Credit Crunch

The high subprime mortgages evasions had caused credit crunch which narrowed to an

abrupt shortage of money and hence resulting to decline in the available lends by the banks.

Many commercial and even investment banks went through massive losses as a result of these

mortgage loans. Banks as a result became very reluctant to give out loans to people and even

other banks leading to a decline in funds circulating in money markets (Scott, 2013).

National debt and the Budget deficit

In the year 2007 the US debt was reading 65 percent of the GDP and became even worse

after the inclusion of pension liabilities. At such a huge budget arrears the government of the

United States automatically had a small fiscal policy expansion capability since the

demographics were against the fiscal stability hence worsening the deficit. This budget deficit

led to challenges in attracting the flow of capital as the Asian investors who were aware of this

deficit reduced the capital flow to US leading to devaluation of the dollar (Scott, 2013).

The Low interest rate

The monetary authorities in US had accustomed the rates of interest to strange levels

leading to a boom in debt-finance consumption which led its way all through to boosting the

housing bubble. It is also claimed that the interest rates in US were stayed too low for a very long

time to an extent of even standing at 1 percent in 2003 and 2004. This activated the great

financial crisis. The monetary policy in US is also criticized for its failure to undertake the

overrated benefit bubble while backing up the fast expansion in subprime mortgages

(Shiller,2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Global Financial Crisis 8

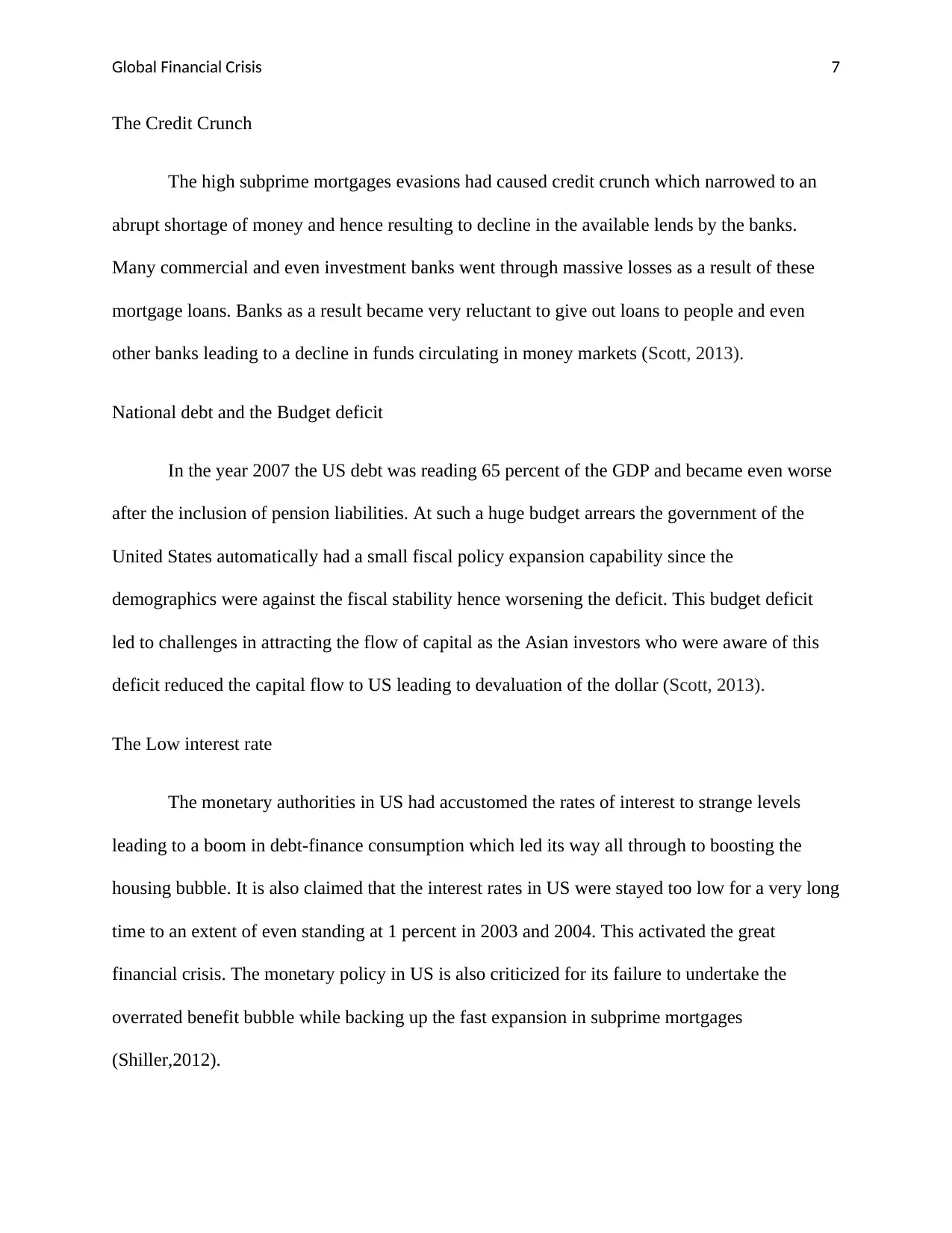

The House crash

US house markets play very important roles as bases of consumers expenditure and the

rate of economic growth. Several factors contributed to the house price increasing faster than the

consumers earning, and as a result it led to overvalued assets. It has been noted that the house

prices increased very fast until 2006 and then declined after the boom. When the prices went

down to adjust this imbalance, it had a major effects on the consumers spending where people

were not able to get extra money for spending (Scott, 2013).

Devaluation of the dollar

In reference to the economic theory, a decrease in exchange rates ultimately helps in

increasing the exports and encouraging the growth in the sector of exports. The decline in the

dollar value however led to cost-push inflation and eventually to a decline in the living standards

where goods for consumption were very expensive hence leading to reduced individual spending

power. This dollar deterioration made US less competitive as compared to its trading partners

(Frankel & Saravelos, 2014).

The Collapse of Lehman brothers

Collapse of Lehman brothers on the year 2008 marked the onset of a new page in global

crisis. All the governments around the world struggled to liberate financial institutions as the

consequences from both the stock market and housing collapse became worse. Many of these

institutions continued to face very serious liquidity problems (Gordon, 2012).

The consequences of Global financial crisis

The House crash

US house markets play very important roles as bases of consumers expenditure and the

rate of economic growth. Several factors contributed to the house price increasing faster than the

consumers earning, and as a result it led to overvalued assets. It has been noted that the house

prices increased very fast until 2006 and then declined after the boom. When the prices went

down to adjust this imbalance, it had a major effects on the consumers spending where people

were not able to get extra money for spending (Scott, 2013).

Devaluation of the dollar

In reference to the economic theory, a decrease in exchange rates ultimately helps in

increasing the exports and encouraging the growth in the sector of exports. The decline in the

dollar value however led to cost-push inflation and eventually to a decline in the living standards

where goods for consumption were very expensive hence leading to reduced individual spending

power. This dollar deterioration made US less competitive as compared to its trading partners

(Frankel & Saravelos, 2014).

The Collapse of Lehman brothers

Collapse of Lehman brothers on the year 2008 marked the onset of a new page in global

crisis. All the governments around the world struggled to liberate financial institutions as the

consequences from both the stock market and housing collapse became worse. Many of these

institutions continued to face very serious liquidity problems (Gordon, 2012).

The consequences of Global financial crisis

Global Financial Crisis 9

After anguish all the way through the greatest and deepest monetary turn down from the

years of 1930s, the U.S. is 8 years precede ting the bureaucratic end of the immense financial

crisis. GDP and the stock market have showed some improvements, the economic effects of this

great financial crisis still reverberate through the U.S. economy (Epstein, 2013).

Consequences on the Labor market

Labor market statistics indicate that about 14 million Americans are still jobless with 6.3

million not working for more than six months. 11.3 million People are not working up to their

wishes. Growth in job is positive although very slow, and at current increase rate, it possibly

will take ten years or even more than this to restore this 5% rate of unemployment (Arnold,

2014).

Consequences on the house market

A number of homes experienced financial crisis and its result has subsided somewhat, but the

housing market is not changing and home prices reach new lows in first quarter of the year 2011

(Plain & Hesse, 2014).

Consequences on the economy

The market aggravation has demonstrated vital holes between incomes and spending in

the state and furthermore the local spending plans, the stock market system misfortunes

uncovered underfunded the pension plans across the nation. The foreseen long term results of

budgetary crisis imply that every one of the states should set up some optional cuts and

enormous taxes to have the capacity to accomplish the adjusted spending plans (San, 2012).

Conclusion

After anguish all the way through the greatest and deepest monetary turn down from the

years of 1930s, the U.S. is 8 years precede ting the bureaucratic end of the immense financial

crisis. GDP and the stock market have showed some improvements, the economic effects of this

great financial crisis still reverberate through the U.S. economy (Epstein, 2013).

Consequences on the Labor market

Labor market statistics indicate that about 14 million Americans are still jobless with 6.3

million not working for more than six months. 11.3 million People are not working up to their

wishes. Growth in job is positive although very slow, and at current increase rate, it possibly

will take ten years or even more than this to restore this 5% rate of unemployment (Arnold,

2014).

Consequences on the house market

A number of homes experienced financial crisis and its result has subsided somewhat, but the

housing market is not changing and home prices reach new lows in first quarter of the year 2011

(Plain & Hesse, 2014).

Consequences on the economy

The market aggravation has demonstrated vital holes between incomes and spending in

the state and furthermore the local spending plans, the stock market system misfortunes

uncovered underfunded the pension plans across the nation. The foreseen long term results of

budgetary crisis imply that every one of the states should set up some optional cuts and

enormous taxes to have the capacity to accomplish the adjusted spending plans (San, 2012).

Conclusion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Global Financial Crisis 10

The Global financial crisis brings about a realistic emphasis much of the general message

as conveyed above. Facts of the occasions leading to this crisis are very complex, but when

considered as a whole, this relic confirms the important part played by the demand as a driving

force of recent economies over an extensive period of time. Demand is a very important thing

for the enactment of emerging economies beyond just short-run business cycles, and policy

cannot also be taken for granted since demand generation won’t be adequate to maintain full

employment, even over period-long horizons. Furthermore, in today’s historical era, the key

drivers of demand have been historic changes of income distribution joined with the dynamics of

financial uncertainty. Generally, the majority of the population is recovering from this financial

crisis and the consequences it had on personal finances and financial security. Americans feel

that credit is adequately available to them.

However, despite these assurance reasons about the economic conditions in the United

States, the findings highlight that economic challenges still remain for a significant percentage of

the population.

The Global financial crisis brings about a realistic emphasis much of the general message

as conveyed above. Facts of the occasions leading to this crisis are very complex, but when

considered as a whole, this relic confirms the important part played by the demand as a driving

force of recent economies over an extensive period of time. Demand is a very important thing

for the enactment of emerging economies beyond just short-run business cycles, and policy

cannot also be taken for granted since demand generation won’t be adequate to maintain full

employment, even over period-long horizons. Furthermore, in today’s historical era, the key

drivers of demand have been historic changes of income distribution joined with the dynamics of

financial uncertainty. Generally, the majority of the population is recovering from this financial

crisis and the consequences it had on personal finances and financial security. Americans feel

that credit is adequately available to them.

However, despite these assurance reasons about the economic conditions in the United

States, the findings highlight that economic challenges still remain for a significant percentage of

the population.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Global Financial Crisis 11

Work cited

Arnold, P. J. (2014). Worldwide money related emergency: The test to bookkeeping research.

Bookkeeping, organizations and society, 23(5), 834-845.

Crotty, J. (2013). Auxiliary reasons for the worldwide monetary emergency: a basic appraisal of

the 'new financial design'. Cambridge diary of financial aspects, 36(5), 654-674.

Epstein, G. A. (Ed.). (2013). Financialization and the world economy. Edward Elgar

Distributing.

Frankel, J., and Saravelos, G. (2014). Can driving markers survey nation powerlessness? Proof

from the 2008– 09 worldwide monetary emergency. Diary of Universal Financial

matters, 90(1), 212-214.

Gordon, R. J. (2012). It is safe to say that us is monetary development over? Wavering

advancement goes up against the six headwinds (No. w11115). National Agency of

Financial Exploration.

Plain, N., and Hesse, H. (2014). Monetary overflows to developing markets amid the worldwide

money related crisis (No. 6-89). Universal Financial Store

Reinhart, C. M., and Rogoff, K. S. (2013). Is the 2007 US sub-prime budgetary emergency so

extraordinary? An international verifiable correlation (No. w14561). National Agency of

Financial Exploration.

San, M.S., 2012. Global financial crisis. Plastic Rainbow Book Publication.

Scott, H.J., 2013. Global financial crisis. Nova Science Publishers.

Work cited

Arnold, P. J. (2014). Worldwide money related emergency: The test to bookkeeping research.

Bookkeeping, organizations and society, 23(5), 834-845.

Crotty, J. (2013). Auxiliary reasons for the worldwide monetary emergency: a basic appraisal of

the 'new financial design'. Cambridge diary of financial aspects, 36(5), 654-674.

Epstein, G. A. (Ed.). (2013). Financialization and the world economy. Edward Elgar

Distributing.

Frankel, J., and Saravelos, G. (2014). Can driving markers survey nation powerlessness? Proof

from the 2008– 09 worldwide monetary emergency. Diary of Universal Financial

matters, 90(1), 212-214.

Gordon, R. J. (2012). It is safe to say that us is monetary development over? Wavering

advancement goes up against the six headwinds (No. w11115). National Agency of

Financial Exploration.

Plain, N., and Hesse, H. (2014). Monetary overflows to developing markets amid the worldwide

money related crisis (No. 6-89). Universal Financial Store

Reinhart, C. M., and Rogoff, K. S. (2013). Is the 2007 US sub-prime budgetary emergency so

extraordinary? An international verifiable correlation (No. w14561). National Agency of

Financial Exploration.

San, M.S., 2012. Global financial crisis. Plastic Rainbow Book Publication.

Scott, H.J., 2013. Global financial crisis. Nova Science Publishers.

Global Financial Crisis 12

Shiller, R. J. (2012). The subprime arrangement: how the present worldwide monetary

emergency happened, and what to do about it. Princeton College Press.

Shiller, R. J. (2012). The subprime arrangement: how the present worldwide monetary

emergency happened, and what to do about it. Princeton College Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.