University Economics for Managers: Financial Crisis Analysis Report

VerifiedAdded on 2022/10/19

|13

|2542

|284

Report

AI Summary

This report, prepared for an Economics for Managers course, examines the causes of the global financial crisis of 2006-2009. It investigates the debate surrounding whether the crisis was primarily caused by financial innovations aimed at creating safe debt instruments or the collapse of the housing bubble. The report analyzes the impact of debt contracts, applying the Coase theorem to mitigate negative externalities, and discusses the role of shared responsibility mortgages in mitigating risks. It explores the effects of securitization on the mortgage market, the impact of macroeconomic environments, and the role of government policies, such as interest rate adjustments and the distribution of stimulus checks. The analysis also covers the role of global imbalances, including the United States' account deficits and the development of safe assets, as well as the securitization of lower-quality assets. The report concludes with recommendations for future macroeconomic policies, emphasizing the importance of maintaining equilibrium interest rates to avoid distortions in the demand for financial products. The report references various academic sources to support its findings.

Economics for Manager 1

<University>

Economics for Manager

By

<Your Name>

<Date>

<Lecturer’s Name and Course Number>

<University>

Economics for Manager

By

<Your Name>

<Date>

<Lecturer’s Name and Course Number>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Economics for Manager 2

Executive Summary

Financial crisis greatly impacted the global economy in the period between 2006 and 2009 as

financial systems were negatively impacted by the eventual fall in demand for financial products

and services. The financial crisis mainly occurred due to financial innovations by developed

economies to create more safe debt instruments without prior consideration of global imbalances.

As such, policies that were formulated to address the global imbalances exposed the economies

to the eventual financial crisis. Reversing of capital inflows as a macroeconomic policy,

securitization of low quality assets and creation of more safe assets were some of the policies

that greatly contributed to occurrence of the global financial crisis.

Executive Summary

Financial crisis greatly impacted the global economy in the period between 2006 and 2009 as

financial systems were negatively impacted by the eventual fall in demand for financial products

and services. The financial crisis mainly occurred due to financial innovations by developed

economies to create more safe debt instruments without prior consideration of global imbalances.

As such, policies that were formulated to address the global imbalances exposed the economies

to the eventual financial crisis. Reversing of capital inflows as a macroeconomic policy,

securitization of low quality assets and creation of more safe assets were some of the policies

that greatly contributed to occurrence of the global financial crisis.

Economics for Manager 3

Introduction

Global economy was hit with a financial crisis in the period between 2006 and 2009 that caused

total collapse threats to the financial systems across the globe. The above occurred when a

number of governments across the world started to bailout uninsured financial entities which

further led to stock price reductions. As such, investments and consumer lending significantly

reduced as banks did not offer short and long term credit facilities due to the financial crisis

(Caballero 2010 p.15). Therefore, the report will mainly focus on finding out whether the global

financial crisis was caused by the financial innovations or collapse of housing bubble.

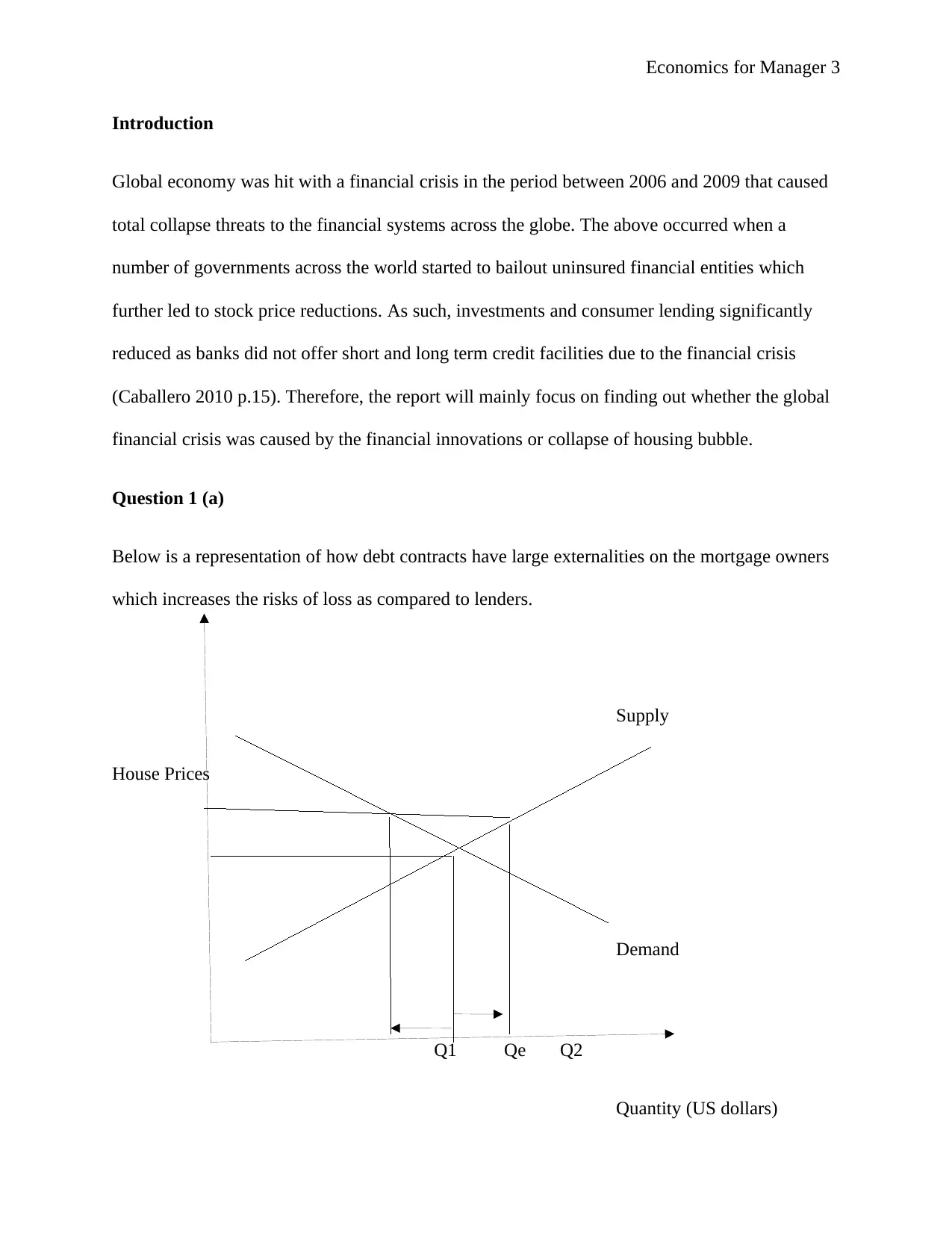

Question 1 (a)

Below is a representation of how debt contracts have large externalities on the mortgage owners

which increases the risks of loss as compared to lenders.

Supply

House Prices

Demand

Q1 Qe Q2

Quantity (US dollars)

Introduction

Global economy was hit with a financial crisis in the period between 2006 and 2009 that caused

total collapse threats to the financial systems across the globe. The above occurred when a

number of governments across the world started to bailout uninsured financial entities which

further led to stock price reductions. As such, investments and consumer lending significantly

reduced as banks did not offer short and long term credit facilities due to the financial crisis

(Caballero 2010 p.15). Therefore, the report will mainly focus on finding out whether the global

financial crisis was caused by the financial innovations or collapse of housing bubble.

Question 1 (a)

Below is a representation of how debt contracts have large externalities on the mortgage owners

which increases the risks of loss as compared to lenders.

Supply

House Prices

Demand

Q1 Qe Q2

Quantity (US dollars)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Economics for Manager 4

From the above illustration, debt contract increases possibilities of loss to the home owners

particularly in times when prices of houses reduce due to economic downturns. In such a case, a

house owner may not be in position to meet specified mortgage payments when house prices fall

and mortgage balance remains unchanged. When house prices fall, their demand significantly

declines from Qe to Q1 which is an indicator of a loss to house owners. On the other hand,

economic downturns can lead to increases in supply of mortgage houses implying that as house

prices increase, their supply will also increase from Qe to Q2. As a result, debt contracts inflict

loss unto home owners before the lenders can incur any loss when house price fall as showed on

the above illustration (Alistair 2009 p.25).

Question 1 (b)

Coase theorem emphasizes that all parties that are affected by a given externality should engage

in bargaining so as to arrive at an efficient outcomes of the trade. In application to standard debt

mortgage contract, Coase theorem can help to mitigate negative externality by creating a

bargaining atmosphere for the lenders and borrowers without prior consideration of initial

property rights (Courses.lumenlearning.com 2019).

Question 2

Shared responsibility mortgages are mainly focused on ensuring that mortgages are securitized in

home mortgage marketplaces by housing finance of United States. Shared responsibility

mortgages mitigate negative externality associated with standard debt mortgages by encouraging

the government to introduce equity related mortgages. In such a case, house owners are protected

from unexpected downturns in mortgage markets implying that unexpected fall in house prices

does not affect their capability to make mortgage payments (International Monetary Fund 2009).

From the above illustration, debt contract increases possibilities of loss to the home owners

particularly in times when prices of houses reduce due to economic downturns. In such a case, a

house owner may not be in position to meet specified mortgage payments when house prices fall

and mortgage balance remains unchanged. When house prices fall, their demand significantly

declines from Qe to Q1 which is an indicator of a loss to house owners. On the other hand,

economic downturns can lead to increases in supply of mortgage houses implying that as house

prices increase, their supply will also increase from Qe to Q2. As a result, debt contracts inflict

loss unto home owners before the lenders can incur any loss when house price fall as showed on

the above illustration (Alistair 2009 p.25).

Question 1 (b)

Coase theorem emphasizes that all parties that are affected by a given externality should engage

in bargaining so as to arrive at an efficient outcomes of the trade. In application to standard debt

mortgage contract, Coase theorem can help to mitigate negative externality by creating a

bargaining atmosphere for the lenders and borrowers without prior consideration of initial

property rights (Courses.lumenlearning.com 2019).

Question 2

Shared responsibility mortgages are mainly focused on ensuring that mortgages are securitized in

home mortgage marketplaces by housing finance of United States. Shared responsibility

mortgages mitigate negative externality associated with standard debt mortgages by encouraging

the government to introduce equity related mortgages. In such a case, house owners are protected

from unexpected downturns in mortgage markets implying that unexpected fall in house prices

does not affect their capability to make mortgage payments (International Monetary Fund 2009).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Economics for Manager 5

As a result, house owners are able to gain relief from prospects on losing out on their mortgages

through utilization of equity based mortgages that mitigate negative externality associated with

standard debt mortgages.

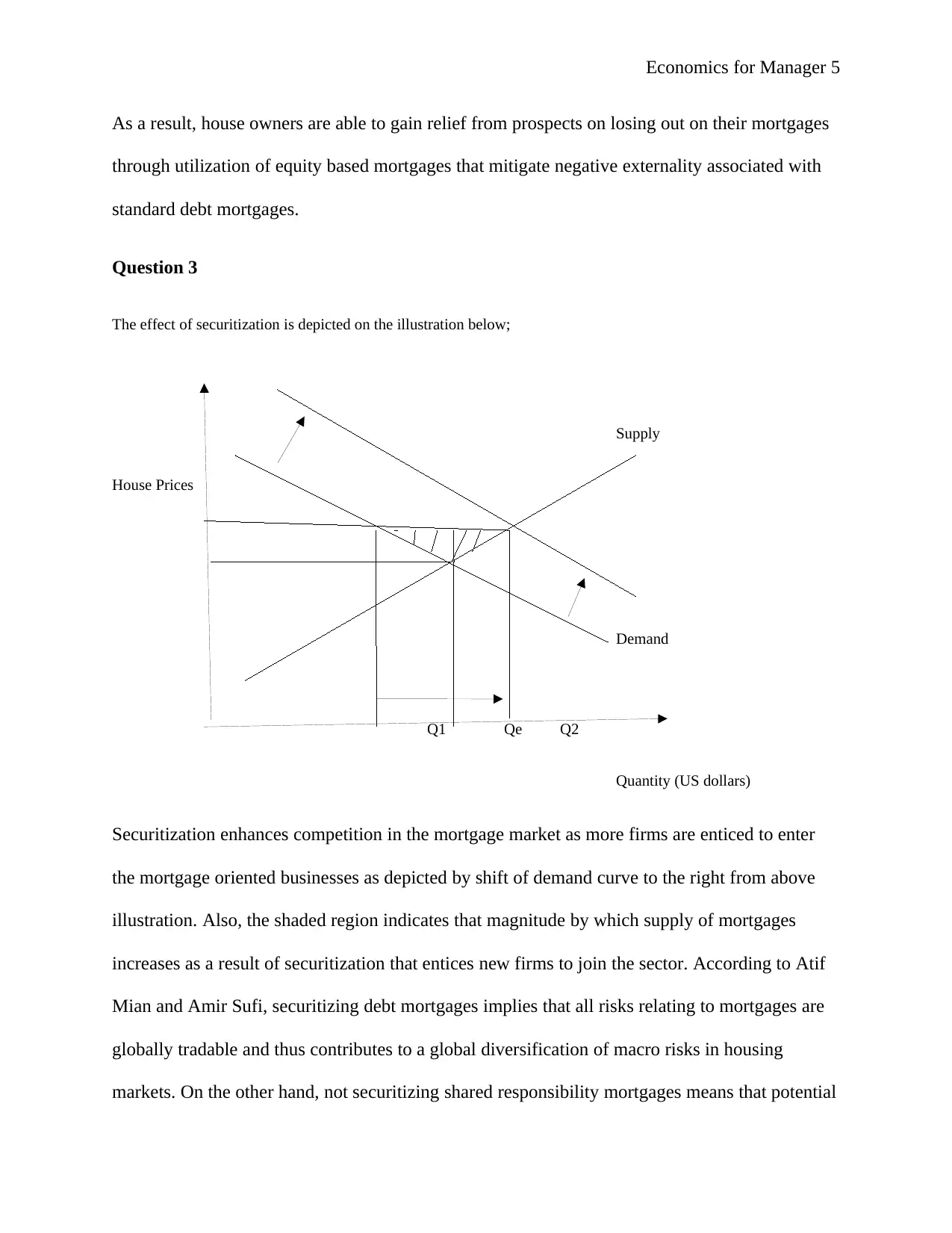

Question 3

The effect of securitization is depicted on the illustration below;

Supply

House Prices

Demand

Q1 Qe Q2

Quantity (US dollars)

Securitization enhances competition in the mortgage market as more firms are enticed to enter

the mortgage oriented businesses as depicted by shift of demand curve to the right from above

illustration. Also, the shaded region indicates that magnitude by which supply of mortgages

increases as a result of securitization that entices new firms to join the sector. According to Atif

Mian and Amir Sufi, securitizing debt mortgages implies that all risks relating to mortgages are

globally tradable and thus contributes to a global diversification of macro risks in housing

markets. On the other hand, not securitizing shared responsibility mortgages means that potential

As a result, house owners are able to gain relief from prospects on losing out on their mortgages

through utilization of equity based mortgages that mitigate negative externality associated with

standard debt mortgages.

Question 3

The effect of securitization is depicted on the illustration below;

Supply

House Prices

Demand

Q1 Qe Q2

Quantity (US dollars)

Securitization enhances competition in the mortgage market as more firms are enticed to enter

the mortgage oriented businesses as depicted by shift of demand curve to the right from above

illustration. Also, the shaded region indicates that magnitude by which supply of mortgages

increases as a result of securitization that entices new firms to join the sector. According to Atif

Mian and Amir Sufi, securitizing debt mortgages implies that all risks relating to mortgages are

globally tradable and thus contributes to a global diversification of macro risks in housing

markets. On the other hand, not securitizing shared responsibility mortgages means that potential

Economics for Manager 6

loss risks are to be incurred by individuals rather than agencies or entities (Gillian 2009). Such a

process enables government to favor debt mortgages at the expense of shared responsibility

mortgages because they do not greatly affect the aggregate demand for mortgages

Question 4

According to Amir Sufi and Atif Mian, financial crisis arose due to failure by standard mortgage

contracts to change to shifts in macroeconomic environment. In such a case, any declines in

house pricing meant that owners of houses were found to realizing negative equity a factor that is

undesirable for business oriented persons (Song & Thakor 2012 p.495). As a result, house

owners would ultimately spend less due to declines in family wealth. In an economic

perspective, the above discussed situation would lead to a decline in aggregate demand and thus

delivering the economy into a recess (Roger & Vitek 2012). Shared responsibility mortgage

would prevent occurrence of such a crisis in future by providing relief to house owners'

payments for mortgage when they actually need it the most (Santos 2011 p.1917). The above

tool links the interest payments and mortgage balance to the domestic home price index which

acts as a standard for measuring the mean value of homes in their zip codes.

Question 5 Excess supply

loss risks are to be incurred by individuals rather than agencies or entities (Gillian 2009). Such a

process enables government to favor debt mortgages at the expense of shared responsibility

mortgages because they do not greatly affect the aggregate demand for mortgages

Question 4

According to Amir Sufi and Atif Mian, financial crisis arose due to failure by standard mortgage

contracts to change to shifts in macroeconomic environment. In such a case, any declines in

house pricing meant that owners of houses were found to realizing negative equity a factor that is

undesirable for business oriented persons (Song & Thakor 2012 p.495). As a result, house

owners would ultimately spend less due to declines in family wealth. In an economic

perspective, the above discussed situation would lead to a decline in aggregate demand and thus

delivering the economy into a recess (Roger & Vitek 2012). Shared responsibility mortgage

would prevent occurrence of such a crisis in future by providing relief to house owners'

payments for mortgage when they actually need it the most (Santos 2011 p.1917). The above

tool links the interest payments and mortgage balance to the domestic home price index which

acts as a standard for measuring the mean value of homes in their zip codes.

Question 5 Excess supply

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

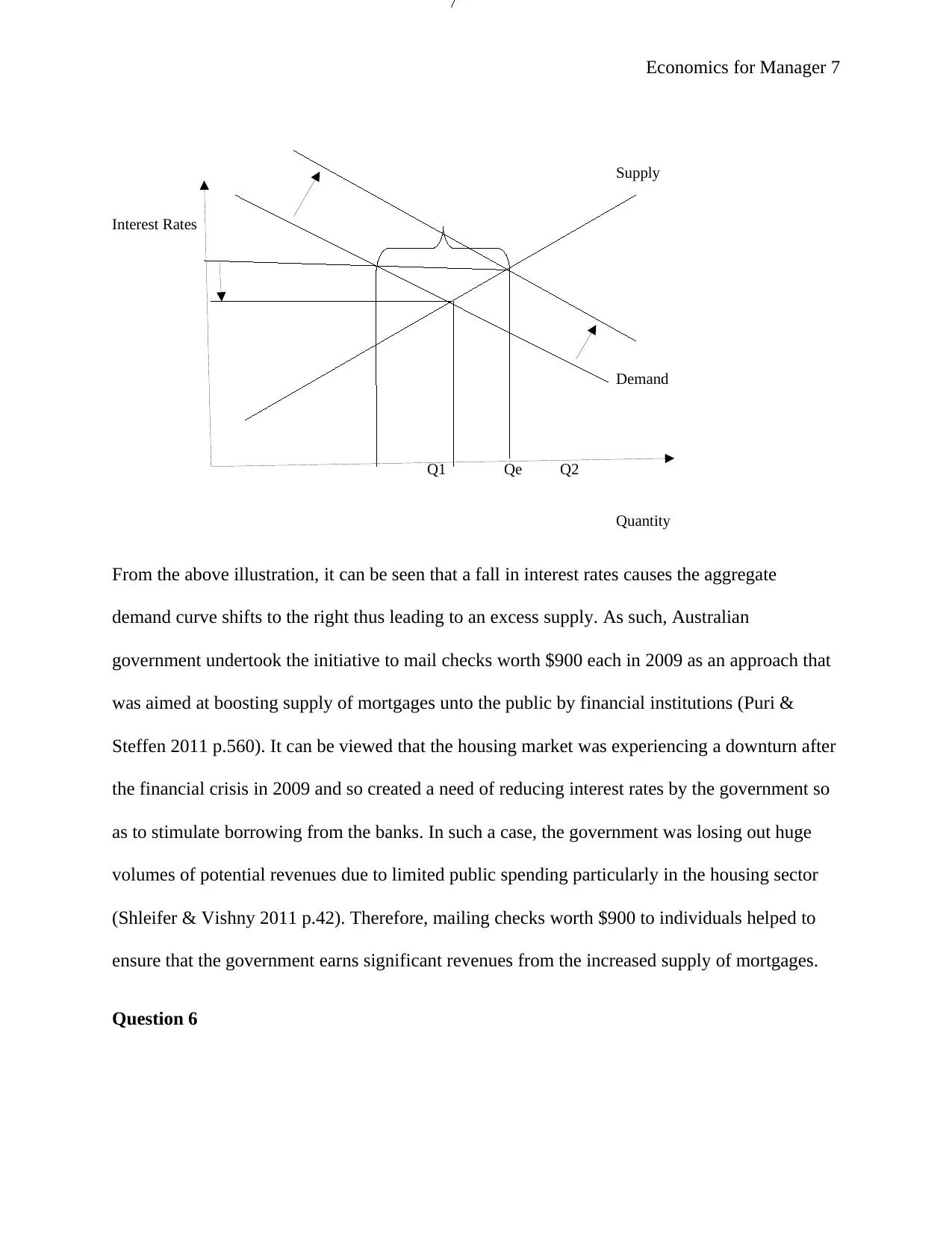

Economics for Manager 7

Supply

Interest Rates

Demand

Q1 Qe Q2

Quantity

From the above illustration, it can be seen that a fall in interest rates causes the aggregate

demand curve shifts to the right thus leading to an excess supply. As such, Australian

government undertook the initiative to mail checks worth $900 each in 2009 as an approach that

was aimed at boosting supply of mortgages unto the public by financial institutions (Puri &

Steffen 2011 p.560). It can be viewed that the housing market was experiencing a downturn after

the financial crisis in 2009 and so created a need of reducing interest rates by the government so

as to stimulate borrowing from the banks. In such a case, the government was losing out huge

volumes of potential revenues due to limited public spending particularly in the housing sector

(Shleifer & Vishny 2011 p.42). Therefore, mailing checks worth $900 to individuals helped to

ensure that the government earns significant revenues from the increased supply of mortgages.

Question 6

Supply

Interest Rates

Demand

Q1 Qe Q2

Quantity

From the above illustration, it can be seen that a fall in interest rates causes the aggregate

demand curve shifts to the right thus leading to an excess supply. As such, Australian

government undertook the initiative to mail checks worth $900 each in 2009 as an approach that

was aimed at boosting supply of mortgages unto the public by financial institutions (Puri &

Steffen 2011 p.560). It can be viewed that the housing market was experiencing a downturn after

the financial crisis in 2009 and so created a need of reducing interest rates by the government so

as to stimulate borrowing from the banks. In such a case, the government was losing out huge

volumes of potential revenues due to limited public spending particularly in the housing sector

(Shleifer & Vishny 2011 p.42). Therefore, mailing checks worth $900 to individuals helped to

ensure that the government earns significant revenues from the increased supply of mortgages.

Question 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Economics for Manager 8

Adoption of shared responsibility mortgages will help to ensure that equity related mortgages are

introduced by the government as a form of relieving house owners from potential losses when

aggregate demand for mortgages fall. When a number of individuals adopt shared responsibility

mortgages, house owners' equity will be maintained high in spite of distortions in aggregated

demand of mortgages (Pfleiderer 2012). As such, any prospects of financial crisis may not take

place given that individuals will be able to make their mortgage payments. Most significantly,

securitizing shared responsibility mortgages will help to create new modes of mortgages

particularly equity based mortgages that may hold a significantly higher future value for

investors (Nguyen 2014). From this point of view, it can be seen that wide adoption and

securitization of shared responsibility mortgages will help to ensure that future value of financial

products like equity based mortgages is boosted. The above discussed approach will likely

prevent a future financial crisis.

Question 7

As the world's largest economy, United States was faced with a challenge of global

imbalances that greatly affected its financial systems and policies that were aimed at addressing

such deficits. Evidentially, United States was experiencing huge volumes of account deficits

which created the need by International Monetary Fund to identify financial policies to addresses

the challenge of present account deficits. More so, account deficits were greatly leading to

financial losses as majority of the individuals and firms were struggling to service their loans. As

such, it always became risky for individuals and firms to undertake investment in financial

products and services such as mortgages since they had lost value due to account deficits (Lo

2012 p.157). Another important factor to note is that present account deficits had also

significantly reduced demand for financial products and services by the firms and individuals. As

Adoption of shared responsibility mortgages will help to ensure that equity related mortgages are

introduced by the government as a form of relieving house owners from potential losses when

aggregate demand for mortgages fall. When a number of individuals adopt shared responsibility

mortgages, house owners' equity will be maintained high in spite of distortions in aggregated

demand of mortgages (Pfleiderer 2012). As such, any prospects of financial crisis may not take

place given that individuals will be able to make their mortgage payments. Most significantly,

securitizing shared responsibility mortgages will help to create new modes of mortgages

particularly equity based mortgages that may hold a significantly higher future value for

investors (Nguyen 2014). From this point of view, it can be seen that wide adoption and

securitization of shared responsibility mortgages will help to ensure that future value of financial

products like equity based mortgages is boosted. The above discussed approach will likely

prevent a future financial crisis.

Question 7

As the world's largest economy, United States was faced with a challenge of global

imbalances that greatly affected its financial systems and policies that were aimed at addressing

such deficits. Evidentially, United States was experiencing huge volumes of account deficits

which created the need by International Monetary Fund to identify financial policies to addresses

the challenge of present account deficits. More so, account deficits were greatly leading to

financial losses as majority of the individuals and firms were struggling to service their loans. As

such, it always became risky for individuals and firms to undertake investment in financial

products and services such as mortgages since they had lost value due to account deficits (Lo

2012 p.157). Another important factor to note is that present account deficits had also

significantly reduced demand for financial products and services by the firms and individuals. As

Economics for Manager 9

such, the financial sector was losing out a significant volume of revenues that would be attained

from its financial products and services as potential investors were unwilling to devote their

limited resources into the sector (Lawrence 2014). In addition, emerging economies were

continuously running present account deficits that increased prospects of devastating financial

crises worldwide. As part of the efforts to addressing the risky financial practices of emerging

economies, United States government opted to undertake a macroeconomic adjustment. The

above policy involved reversing net capital inflows which had been previously backed by

economic growth and present account deficits. The above policy resulted into significantly high

demand for safe debt instruments by central banks of emerging economies than those that were

available at the market (Taillard 2019). The above situation led to the eventual financial crisis in

the period between 2006 and 2009 as the demand for safe debt instruments surpassed the

available quantity of these financial instruments.

Furthermore, United States undertook the initiative to develop safe assets that were aimed

at meeting their ever and highly increasing demand from central banks of emerging economies.

Real estate property, treasury mutual funds, cash, money finances as well as treasury bills are

some of the safe assets that the United States government decided to develop ((Thakor 2012

p.24). More so, creation of the above safe assets meant that the equilibrium interest rates were to

be increased to greater heights due to excess demand from emerging economies. As such,

potential borrowers are always discouraged to inject their resources in financial markets when

the interest rates are extremely high because they directly reduce on their profit margins. In this

regard, the policy to develop safe assets by the United States government discouraged borrowing

and thus the global economy was constrained as far as overall output and investments are

concerned (Bailey 2017). Additionally, the United States government also decided to securitize

such, the financial sector was losing out a significant volume of revenues that would be attained

from its financial products and services as potential investors were unwilling to devote their

limited resources into the sector (Lawrence 2014). In addition, emerging economies were

continuously running present account deficits that increased prospects of devastating financial

crises worldwide. As part of the efforts to addressing the risky financial practices of emerging

economies, United States government opted to undertake a macroeconomic adjustment. The

above policy involved reversing net capital inflows which had been previously backed by

economic growth and present account deficits. The above policy resulted into significantly high

demand for safe debt instruments by central banks of emerging economies than those that were

available at the market (Taillard 2019). The above situation led to the eventual financial crisis in

the period between 2006 and 2009 as the demand for safe debt instruments surpassed the

available quantity of these financial instruments.

Furthermore, United States undertook the initiative to develop safe assets that were aimed

at meeting their ever and highly increasing demand from central banks of emerging economies.

Real estate property, treasury mutual funds, cash, money finances as well as treasury bills are

some of the safe assets that the United States government decided to develop ((Thakor 2012

p.24). More so, creation of the above safe assets meant that the equilibrium interest rates were to

be increased to greater heights due to excess demand from emerging economies. As such,

potential borrowers are always discouraged to inject their resources in financial markets when

the interest rates are extremely high because they directly reduce on their profit margins. In this

regard, the policy to develop safe assets by the United States government discouraged borrowing

and thus the global economy was constrained as far as overall output and investments are

concerned (Bailey 2017). Additionally, the United States government also decided to securitize

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Economics for Manager 10

lower quality assets which created panic within the global economy. Such a policy was meant to

create a higher future value for low quality assets and yet it distorted the aggregate demand of

other current and highly valued financial assets. The above is attributed to the fact that

individuals opted to devote their resources into the securitized but low quality assets that held a

future value. In such a case, demand for the highly valued assets significantly declined which

meant that the financial systems across the globe were exposed to the eventual financial crisis

(Sufi & Mian 2016). From the above discussion, it can be concluded that financial crisis

occurred due to financial innovations that were aimed at creating safe debts.

Conclusion and Recommendations

Global economy was hit with a financial crisis in the period between 2006 and 2009 due to

global imbalances in the financial systems of various countries. As such, policies that were

formulated to address the global imbalances exposed the economies to the eventual financial

crisis. Reversing of capital inflows as a macroeconomic policy, securitization of low quality

assets and creation of more safe assets were some of the policies that greatly contributed to

occurrence of the global financial crisis. As part of the recommendations, United States

government should devise its macroeconomic policies towards maintenance of equilibrium

interest rates so as to avoid distortion of aggregate demand for financial products.

lower quality assets which created panic within the global economy. Such a policy was meant to

create a higher future value for low quality assets and yet it distorted the aggregate demand of

other current and highly valued financial assets. The above is attributed to the fact that

individuals opted to devote their resources into the securitized but low quality assets that held a

future value. In such a case, demand for the highly valued assets significantly declined which

meant that the financial systems across the globe were exposed to the eventual financial crisis

(Sufi & Mian 2016). From the above discussion, it can be concluded that financial crisis

occurred due to financial innovations that were aimed at creating safe debts.

Conclusion and Recommendations

Global economy was hit with a financial crisis in the period between 2006 and 2009 due to

global imbalances in the financial systems of various countries. As such, policies that were

formulated to address the global imbalances exposed the economies to the eventual financial

crisis. Reversing of capital inflows as a macroeconomic policy, securitization of low quality

assets and creation of more safe assets were some of the policies that greatly contributed to

occurrence of the global financial crisis. As part of the recommendations, United States

government should devise its macroeconomic policies towards maintenance of equilibrium

interest rates so as to avoid distortion of aggregate demand for financial products.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Economics for Manager 11

References

Alistair, M., 2009. The Fall of the House of Credit. Cambridge University Press, p.12-64

Bailey, T., 2017. Shared mortgages ensure the house always wins: Retrieved:

https://www.worldfinance.com/infrastructure-investment/shared-mortgages-ensure-the-house-

always-wins

Caballero, R.J., 2010. The "Other" Imbalance and The Financial Crisis: Nber Working Paper

Series, p.1-43

Courses.lumenlearning.com., 2019.How does Coase Theorem seek to solve negative

externalities?: Retrieved from:

https://courses.lumenlearning.com/boundless-economics/chapter/private-solutions/

Gillian, T., 2009. Fool's Gold: How Unrestrained Greed Corrupted a Dream, Shattered Global

Markets and Unleashed a Catastrophe. Little, Brow.

International Monetary Fund., 2009. Global Financial Stability Report: Navigating the Financial

Challenges Ahead, October.

Lawrence, D., 2014. The slumps that shaped modern finance: The Economist, Available at:

www.economist.com/news/essays/21600451-finance-not-merely-prone-crises-it-shaped-them-

five-historical-crisesshow-how-aspects-today-s-fina.

Lo, A., 2012. Reading about the financial crisis: A twenty-one book review. Journal of

Economic Literature; 50:151–78.

References

Alistair, M., 2009. The Fall of the House of Credit. Cambridge University Press, p.12-64

Bailey, T., 2017. Shared mortgages ensure the house always wins: Retrieved:

https://www.worldfinance.com/infrastructure-investment/shared-mortgages-ensure-the-house-

always-wins

Caballero, R.J., 2010. The "Other" Imbalance and The Financial Crisis: Nber Working Paper

Series, p.1-43

Courses.lumenlearning.com., 2019.How does Coase Theorem seek to solve negative

externalities?: Retrieved from:

https://courses.lumenlearning.com/boundless-economics/chapter/private-solutions/

Gillian, T., 2009. Fool's Gold: How Unrestrained Greed Corrupted a Dream, Shattered Global

Markets and Unleashed a Catastrophe. Little, Brow.

International Monetary Fund., 2009. Global Financial Stability Report: Navigating the Financial

Challenges Ahead, October.

Lawrence, D., 2014. The slumps that shaped modern finance: The Economist, Available at:

www.economist.com/news/essays/21600451-finance-not-merely-prone-crises-it-shaped-them-

five-historical-crisesshow-how-aspects-today-s-fina.

Lo, A., 2012. Reading about the financial crisis: A twenty-one book review. Journal of

Economic Literature; 50:151–78.

Economics for Manager 12

Nguyen, T., 2014. Bank capital requirements: A quantitative analysis, Working Paper: The Ohio

State University.

Pfleiderer, P., 2012. Reducing the fragility of the financial sector: The importance of equity and

why it is not expensive: Presented at the Norges Bank Macro-prudential Workshop

Puri, M & Steffen, S., 2011. Global retail lending in the aftermath of the U.S. financial crisis,

distinguishing between supply and demand effects: Journal of Financial Economics; 100:556–

78.

Roger, S & Vitek F., 2012. The global macroeconomic costs of raising bank capital adequacy

requirements; IMF Working Paper WP/12/44, International Monetary Fund

Santos, J., 2011. Bank corporate loan pricing following the subprime crisis: Review of Financial

Studies, 24:1916–43.

Shleifer, A., & Vishny, R., 2011. Fire sales in finance and macroeconomics: Journal of

Economic Perspectives; 25:29–48.

Song, F., & Thakor, A., 2012. Financial system development and political intervention: World

Bank Economic Review: 27:491–513.

Sufi, A & Mian, A., 2016. Shared responsibility mortgages: Retrieved from:

https://equitablegrowth.org/shared-responsibility-mortgages/

Taillard., M. 2019. How to Make Securities Out of Just about Anything: Retrieved from:

https://www.dummies.com/business/accounting/auditing/how-to-make-securities-out-of-just-

about-anything/

Nguyen, T., 2014. Bank capital requirements: A quantitative analysis, Working Paper: The Ohio

State University.

Pfleiderer, P., 2012. Reducing the fragility of the financial sector: The importance of equity and

why it is not expensive: Presented at the Norges Bank Macro-prudential Workshop

Puri, M & Steffen, S., 2011. Global retail lending in the aftermath of the U.S. financial crisis,

distinguishing between supply and demand effects: Journal of Financial Economics; 100:556–

78.

Roger, S & Vitek F., 2012. The global macroeconomic costs of raising bank capital adequacy

requirements; IMF Working Paper WP/12/44, International Monetary Fund

Santos, J., 2011. Bank corporate loan pricing following the subprime crisis: Review of Financial

Studies, 24:1916–43.

Shleifer, A., & Vishny, R., 2011. Fire sales in finance and macroeconomics: Journal of

Economic Perspectives; 25:29–48.

Song, F., & Thakor, A., 2012. Financial system development and political intervention: World

Bank Economic Review: 27:491–513.

Sufi, A & Mian, A., 2016. Shared responsibility mortgages: Retrieved from:

https://equitablegrowth.org/shared-responsibility-mortgages/

Taillard., M. 2019. How to Make Securities Out of Just about Anything: Retrieved from:

https://www.dummies.com/business/accounting/auditing/how-to-make-securities-out-of-just-

about-anything/

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.