Economic Report: The Global Financial Meltdown of 2008-09 Analysis

VerifiedAdded on 2023/06/15

|11

|3081

|305

Report

AI Summary

This report provides an analysis of the global financial meltdown of 2008-09, comparing it to the Great Depression of the 1930s. It examines the causes and conditions that led to the American housing bubble, including Lehman Brothers' bankruptcy, and discusses the direct and indirect implications of these events on the US economy. The report highlights the lessons learned from the crisis, public responses, and criticisms faced, and suggests potential policy changes. It covers the role of financial institutions, the impact on unemployment and industrial production, and the governmental responses aimed at stabilizing the economy. The document emphasizes the importance of regulatory reforms and new policies to prevent future crises and promote sustainable economic growth. Desklib offers this and many more solved assignments and past papers for students.

Global Financial

Meltdown of 2008-09

Meltdown of 2008-09

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Causes and conditions that led to American housing bubble 2008 including laymen brother’s

bankruptcy...................................................................................................................................3

Similarities and differences with other events that fall under the same category are as under:. .4

Direct and indirect implication of the above events:...................................................................5

The lessons that are drawn from the outcome of the crisis of 2008-09.......................................6

Responses that came from the public and the criticism faced.....................................................8

Suggestions that can be needed regarding the change in policy..................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Causes and conditions that led to American housing bubble 2008 including laymen brother’s

bankruptcy...................................................................................................................................3

Similarities and differences with other events that fall under the same category are as under:. .4

Direct and indirect implication of the above events:...................................................................5

The lessons that are drawn from the outcome of the crisis of 2008-09.......................................6

Responses that came from the public and the criticism faced.....................................................8

Suggestions that can be needed regarding the change in policy..................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

The financial crises of 2007- 2008 and great depression of 1930s was one of the worst

economic and financial disaster that affects almost all industries, business giants and financial

corporations working across the globe in their era respectively (Diniz-Maganini, Rasheed and

Sheng, 2021). These crises lead to great recession and depression in an economy in such a way

that unemployment increases, poverty ratio rises, industrial production declines and so on.

Similarly, in financial crises, residential and commercial housing project price declines

drastically and home loans are granted by banks more than their mortgage property value. Their

impact is so long that still unemployment rate is above 9% in US market. This report indicates

effects and conditions for such disasters and it lays down the differences and similarities between

two crises. It also specifies direct and indirect impact in US economy. Further it lays down the

role plays by laymen brothers in financial crises of 2008. Further this report also mentions,

lessons and responses that could be drawn from the above event. At the end there are some

suggestions & solution and policy changes that may be required.

MAIN BODY

Causes and conditions that led to American housing bubble 2008 including laymen brother’s

bankruptcy

The bubble starts at beginning of 2006, where price of residential homes starts falling in us

market for the first time. At the beginning of such downfall, it was look like there is a slowdown

in real estate sector, which is heavily priced in market. But in such a situation, certain factors are

ignored by market players such as interest rate on home loans becomes cheaper, credit

worthiness of the home loan applicants is not properly analysed by the banking institutions. Even

mortgage loans are granted more than the value of residential property which is collateral as

security against loans (Antoniades and Antonarakis, 2022).

Further these mortgage properties are backed by guarantee of certain financial institutions

providing assurance to banks regarding their funds. This whole process involves various

intermediaries such as commercial banks, mortgage lenders, insurance companies and so on that

lead to such major crises that not only affect US market but also influence, international financial

system.

The financial crises of 2007- 2008 and great depression of 1930s was one of the worst

economic and financial disaster that affects almost all industries, business giants and financial

corporations working across the globe in their era respectively (Diniz-Maganini, Rasheed and

Sheng, 2021). These crises lead to great recession and depression in an economy in such a way

that unemployment increases, poverty ratio rises, industrial production declines and so on.

Similarly, in financial crises, residential and commercial housing project price declines

drastically and home loans are granted by banks more than their mortgage property value. Their

impact is so long that still unemployment rate is above 9% in US market. This report indicates

effects and conditions for such disasters and it lays down the differences and similarities between

two crises. It also specifies direct and indirect impact in US economy. Further it lays down the

role plays by laymen brothers in financial crises of 2008. Further this report also mentions,

lessons and responses that could be drawn from the above event. At the end there are some

suggestions & solution and policy changes that may be required.

MAIN BODY

Causes and conditions that led to American housing bubble 2008 including laymen brother’s

bankruptcy

The bubble starts at beginning of 2006, where price of residential homes starts falling in us

market for the first time. At the beginning of such downfall, it was look like there is a slowdown

in real estate sector, which is heavily priced in market. But in such a situation, certain factors are

ignored by market players such as interest rate on home loans becomes cheaper, credit

worthiness of the home loan applicants is not properly analysed by the banking institutions. Even

mortgage loans are granted more than the value of residential property which is collateral as

security against loans (Antoniades and Antonarakis, 2022).

Further these mortgage properties are backed by guarantee of certain financial institutions

providing assurance to banks regarding their funds. This whole process involves various

intermediaries such as commercial banks, mortgage lenders, insurance companies and so on that

lead to such major crises that not only affect US market but also influence, international financial

system.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The laymen brothers are one of the prestigious US firm engaged in financial services plays

an important role in such crises. They become bankrupt in 2008 after filling petition for

bankruptcy to court. The main reason for such downfall is that firm entered into mortgage

backed securities and collateral debt obligation along with some financial players. They acquired

five corporations engaged in mortgage lending such as Aurora loan services, BNC mortgage etc.

which specialises in subprime mortgage lending which is riskier. Further they provide security

against such loan without proper documentation and borrowers of such subprime mortgages

becomes defaulters at the time of repayment of loan. This leads to a sharp downfall in

profitability of the firm in quarter end results and they continued till company filed their petition

to court for insolvency (Yildiran, 2021).

Similarities and differences with other events that fall under the same category are as under:

The great depression of late 1920s and last until 1930s was the most longest and severe

downfall in the modern history as it lasts almost for 10 years. This depression leads a sharp

decline in industrial production, creates mass unemployment and increases poverty ratio. In the

united states, effect of such depression was worst as compare to other countries as there is a

decline in industrial production nearly by 47%. Their GDP declines by 30% and unemployment

crossed the mark of 20% of total population (Demirgüç-Kunt, Peria and Tressel, 2020).

The differences between financial crises 2008 and great depression 1930s are as under:

The unemployment rate in great depression is more than 20% whereas in the financial

crisis such rate is 8.5%.

9000 plus bank fails during great depression which represent 50% (Approx) of the banks

nationwide whereas in financial crises 57 banks of the US gets affected representing 26%

(Approx.) of total financial institution of US.

Similarities in both crises can be viewed as leads to bigger change in the federal structure,

amendment in various policies and rules made by government. Further strong laws have been

incorporated by government to control the industries, financial institutions, and other class of

businesses in order to restrict all those unlawful activities that are against the public interest in

general (Diniz-Maganini, Rasheed and Sheng, 2021).

an important role in such crises. They become bankrupt in 2008 after filling petition for

bankruptcy to court. The main reason for such downfall is that firm entered into mortgage

backed securities and collateral debt obligation along with some financial players. They acquired

five corporations engaged in mortgage lending such as Aurora loan services, BNC mortgage etc.

which specialises in subprime mortgage lending which is riskier. Further they provide security

against such loan without proper documentation and borrowers of such subprime mortgages

becomes defaulters at the time of repayment of loan. This leads to a sharp downfall in

profitability of the firm in quarter end results and they continued till company filed their petition

to court for insolvency (Yildiran, 2021).

Similarities and differences with other events that fall under the same category are as under:

The great depression of late 1920s and last until 1930s was the most longest and severe

downfall in the modern history as it lasts almost for 10 years. This depression leads a sharp

decline in industrial production, creates mass unemployment and increases poverty ratio. In the

united states, effect of such depression was worst as compare to other countries as there is a

decline in industrial production nearly by 47%. Their GDP declines by 30% and unemployment

crossed the mark of 20% of total population (Demirgüç-Kunt, Peria and Tressel, 2020).

The differences between financial crises 2008 and great depression 1930s are as under:

The unemployment rate in great depression is more than 20% whereas in the financial

crisis such rate is 8.5%.

9000 plus bank fails during great depression which represent 50% (Approx) of the banks

nationwide whereas in financial crises 57 banks of the US gets affected representing 26%

(Approx.) of total financial institution of US.

Similarities in both crises can be viewed as leads to bigger change in the federal structure,

amendment in various policies and rules made by government. Further strong laws have been

incorporated by government to control the industries, financial institutions, and other class of

businesses in order to restrict all those unlawful activities that are against the public interest in

general (Diniz-Maganini, Rasheed and Sheng, 2021).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct and indirect implication of the above events:

The great depression 1930:

Direct Implication could be as under: -

50% economy of U.S shattered completely as bank system fails, GDP of U.S fall below

the bottom line, industrial production restricted to 50% of its normal capacity.

It affected the politics as people move their confidence against capitalism structure.

Banking system completely fails and depositors lost confidence in them and they rushed

to withdraw their money from banks and other financial institutions (Singh, 2018).

Deflation in prices of products and services as price falls by 30%. Therefore, helps

consumers as price is falling but on other hand it affects the farmers, businesses and

home owners.

Similarly, indirect implication could be:

1. Unemployment rate is below 4.2% till 1928 but it increases to 23% by the end of 1935.

2.There is a regular drop in personal income tax paid by individuals and other assesses so it

affects tax revenue of government.

3.International trade between U.S and other countries also affected by more than 50%. This leads

to decrease in tax collection in the form of export and import duty.

Financial crises 2008:

Direct Implication could be:

The great depression 1930:

Direct Implication could be as under: -

50% economy of U.S shattered completely as bank system fails, GDP of U.S fall below

the bottom line, industrial production restricted to 50% of its normal capacity.

It affected the politics as people move their confidence against capitalism structure.

Banking system completely fails and depositors lost confidence in them and they rushed

to withdraw their money from banks and other financial institutions (Singh, 2018).

Deflation in prices of products and services as price falls by 30%. Therefore, helps

consumers as price is falling but on other hand it affects the farmers, businesses and

home owners.

Similarly, indirect implication could be:

1. Unemployment rate is below 4.2% till 1928 but it increases to 23% by the end of 1935.

2.There is a regular drop in personal income tax paid by individuals and other assesses so it

affects tax revenue of government.

3.International trade between U.S and other countries also affected by more than 50%. This leads

to decrease in tax collection in the form of export and import duty.

Financial crises 2008:

Direct Implication could be:

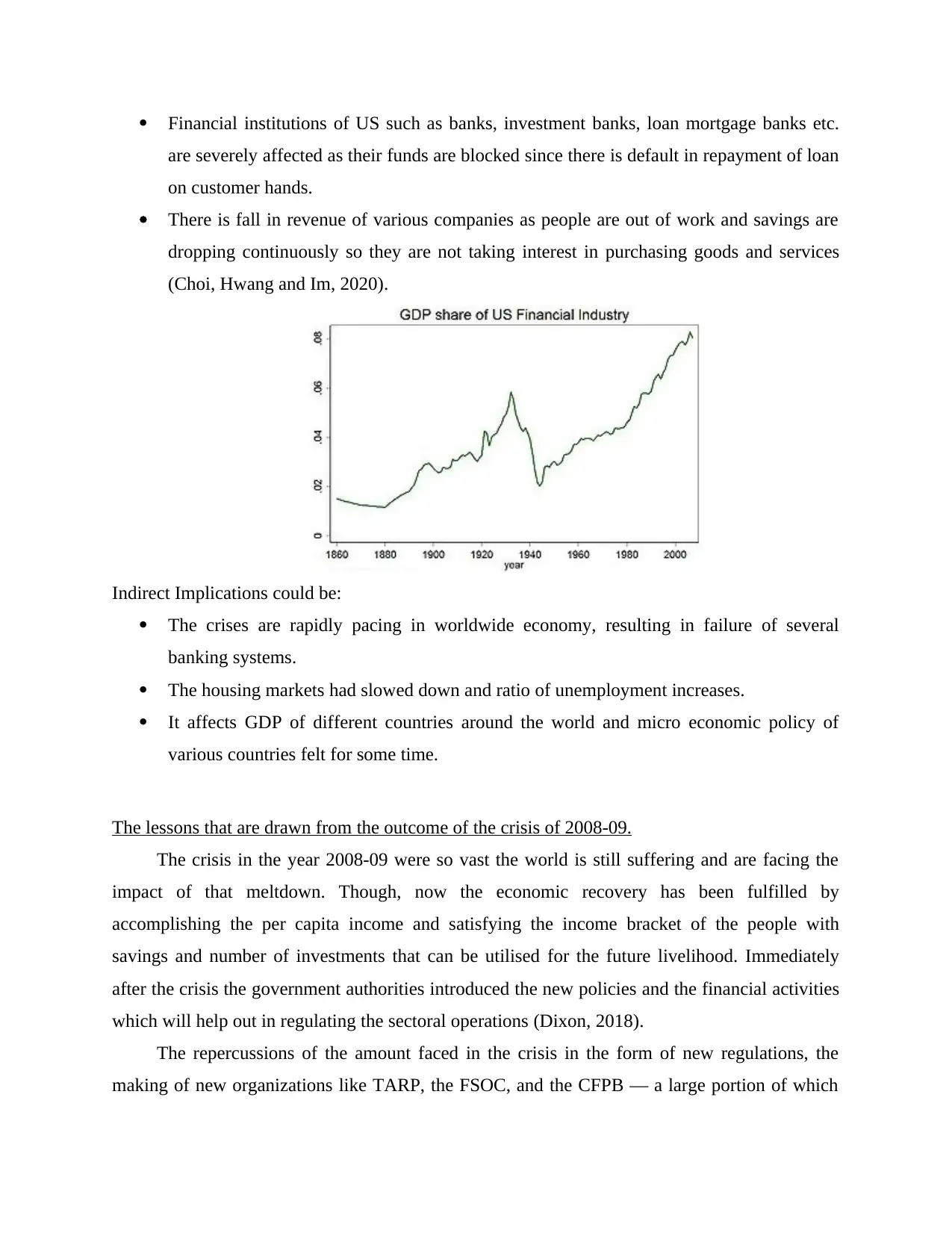

Financial institutions of US such as banks, investment banks, loan mortgage banks etc.

are severely affected as their funds are blocked since there is default in repayment of loan

on customer hands.

There is fall in revenue of various companies as people are out of work and savings are

dropping continuously so they are not taking interest in purchasing goods and services

(Choi, Hwang and Im, 2020).

Indirect Implications could be:

The crises are rapidly pacing in worldwide economy, resulting in failure of several

banking systems.

The housing markets had slowed down and ratio of unemployment increases.

It affects GDP of different countries around the world and micro economic policy of

various countries felt for some time.

The lessons that are drawn from the outcome of the crisis of 2008-09.

The crisis in the year 2008-09 were so vast the world is still suffering and are facing the

impact of that meltdown. Though, now the economic recovery has been fulfilled by

accomplishing the per capita income and satisfying the income bracket of the people with

savings and number of investments that can be utilised for the future livelihood. Immediately

after the crisis the government authorities introduced the new policies and the financial activities

which will help out in regulating the sectoral operations (Dixon, 2018).

The repercussions of the amount faced in the crisis in the form of new regulations, the

making of new organizations like TARP, the FSOC, and the CFPB — a large portion of which

are severely affected as their funds are blocked since there is default in repayment of loan

on customer hands.

There is fall in revenue of various companies as people are out of work and savings are

dropping continuously so they are not taking interest in purchasing goods and services

(Choi, Hwang and Im, 2020).

Indirect Implications could be:

The crises are rapidly pacing in worldwide economy, resulting in failure of several

banking systems.

The housing markets had slowed down and ratio of unemployment increases.

It affects GDP of different countries around the world and micro economic policy of

various countries felt for some time.

The lessons that are drawn from the outcome of the crisis of 2008-09.

The crisis in the year 2008-09 were so vast the world is still suffering and are facing the

impact of that meltdown. Though, now the economic recovery has been fulfilled by

accomplishing the per capita income and satisfying the income bracket of the people with

savings and number of investments that can be utilised for the future livelihood. Immediately

after the crisis the government authorities introduced the new policies and the financial activities

which will help out in regulating the sectoral operations (Dixon, 2018).

The repercussions of the amount faced in the crisis in the form of new regulations, the

making of new organizations like TARP, the FSOC, and the CFPB — a large portion of which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

scarcely exist today — new panels and sub-advisory groups, and stages for government officials,

informants and chiefs to fabricate their vocations on top of, and enough books to fill a divider at

a book shop, a significant number of which actually exist.

The bank of all types were prevented from the use of the unnecessary paperwork which

walk with difficulty to serve the consumers. This has made the system efficient and has become

healthy and more resistant compared from the 2008. The leverage ratios have also grown and

the economy manage a certain level of liquidity position in the financial market to cover the risk

in the global monetary system (Nolan, P., 2020).

The capital requirement of the customers is being fulfilled by reducing the leverage ratios

which are responsible for the prime mortgages that the country incurs.

A few enormous monetary firms experienced monetary trouble, and numerous monetary

business sectors experienced critical disturbance. Accordingly, the Federal Reserve gave

liquidity and backing through a scope of projects persuaded by a craving to work on the working

of monetary business sectors and establishments, and along these lines limit the damage to the

US economy.

The Federal Reserve has given phenomenal financial convenience because of the

seriousness of the withdrawal and the slow speed of the following recuperation. Moreover, the

monetary emergency prompted a scope of significant changes in banking and monetary

guideline, legislative regulation that altogether impacted the Federal Reserve.

After home costs crested in the start of 2007, as per the Federal Housing Finance Agency

House Price Index, the degree to which costs may ultimately fall turned into a critical inquiry for

the evaluating of home loan related protections since enormous decreases in home costs were

considered to probably prompt an increment in contract defaults and higher misfortunes to

holders of such protections. Enormous, cross country decreases in home costs had been

somewhat uncommon in the US authentic information, however the run-up in home costs

additionally had been phenomenal in its scale and degree. At last, home costs fell by over a fifth

on normal the country over from the main quarter of 2007 to the second quarter of 2011. This

decrease in home costs assisted with starting the monetary emergency of 2007-08, as monetary

market members confronted extensive vulnerability about the frequency of misfortunes on

contract related resources.

informants and chiefs to fabricate their vocations on top of, and enough books to fill a divider at

a book shop, a significant number of which actually exist.

The bank of all types were prevented from the use of the unnecessary paperwork which

walk with difficulty to serve the consumers. This has made the system efficient and has become

healthy and more resistant compared from the 2008. The leverage ratios have also grown and

the economy manage a certain level of liquidity position in the financial market to cover the risk

in the global monetary system (Nolan, P., 2020).

The capital requirement of the customers is being fulfilled by reducing the leverage ratios

which are responsible for the prime mortgages that the country incurs.

A few enormous monetary firms experienced monetary trouble, and numerous monetary

business sectors experienced critical disturbance. Accordingly, the Federal Reserve gave

liquidity and backing through a scope of projects persuaded by a craving to work on the working

of monetary business sectors and establishments, and along these lines limit the damage to the

US economy.

The Federal Reserve has given phenomenal financial convenience because of the

seriousness of the withdrawal and the slow speed of the following recuperation. Moreover, the

monetary emergency prompted a scope of significant changes in banking and monetary

guideline, legislative regulation that altogether impacted the Federal Reserve.

After home costs crested in the start of 2007, as per the Federal Housing Finance Agency

House Price Index, the degree to which costs may ultimately fall turned into a critical inquiry for

the evaluating of home loan related protections since enormous decreases in home costs were

considered to probably prompt an increment in contract defaults and higher misfortunes to

holders of such protections. Enormous, cross country decreases in home costs had been

somewhat uncommon in the US authentic information, however the run-up in home costs

additionally had been phenomenal in its scale and degree. At last, home costs fell by over a fifth

on normal the country over from the main quarter of 2007 to the second quarter of 2011. This

decrease in home costs assisted with starting the monetary emergency of 2007-08, as monetary

market members confronted extensive vulnerability about the frequency of misfortunes on

contract related resources.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Responses that came from the public and the criticism faced.

The monetary disaster has incited a quick reaction by government to keep away from a

breakdown of the monetary and banking frameworks and cut-off the financial impacts of the

credit crunch. Such approaches target balancing out the economy and starting a fast recuperation.

However, strategies likewise need to guarantee that the recuperation is tough, for example in

light of manageable development. The emergency ought not harm the drivers of long – term

development, yet ought to rather be utilized as a foundation to speed up underlying movements

towards a more grounded, more pleasant and cleaner monetary future. Neglecting to do as such

may lead just to an impermanent recuperation as the large scale financial and underlying

foundations of the current slump would stay immaculate.

The results that were faced by the public was not good because of the non - controllable

system of the bank. The banks were providing the loans at a cheaper rate that it could be with the

appropriate paperwork (de Carvalho, F.C and et.al., 2019).

The issues were resolved the imposing the restrictions on the dividend by giving them the

capital support from the government which could dilute the shareholder’s position in the market.

The consequences which were enforces by the bank were managed by bringing out the new

policies and maintain a controllable environment in the banks specially while granting the loans.

Some of the key players that were affecting during the crisis:

1. Treasury Secretary Henry Paulson- One of his popular choices as secretary was to allow

Lehman Brothers to come up short, encouraging a financial exchange drop of almost five

percent. In his energy not to rehash that misstep, he helped push the bank bailout through

Congress.

2. Federal Reserve Chair Ben Bernanke- In charge of the nation's driving money related

arrangement making body during the monetary emergency, Bernanke was the substance

of quantitative facilitating. This strategy included lessening loan fees and infusing more

cash into the economy to urge banks to loan and customers to spend. While numerous

legislators and business analysts were stressed quantitative facilitating would spike

expansion and new resource bubbles, some, including Nobel Prize-winning financial

expert Paul Krugman commend Bernanke's endeavors, and even demand that he helped

get control over the emergency, forestalling a much greater monetary calamity.

The monetary disaster has incited a quick reaction by government to keep away from a

breakdown of the monetary and banking frameworks and cut-off the financial impacts of the

credit crunch. Such approaches target balancing out the economy and starting a fast recuperation.

However, strategies likewise need to guarantee that the recuperation is tough, for example in

light of manageable development. The emergency ought not harm the drivers of long – term

development, yet ought to rather be utilized as a foundation to speed up underlying movements

towards a more grounded, more pleasant and cleaner monetary future. Neglecting to do as such

may lead just to an impermanent recuperation as the large scale financial and underlying

foundations of the current slump would stay immaculate.

The results that were faced by the public was not good because of the non - controllable

system of the bank. The banks were providing the loans at a cheaper rate that it could be with the

appropriate paperwork (de Carvalho, F.C and et.al., 2019).

The issues were resolved the imposing the restrictions on the dividend by giving them the

capital support from the government which could dilute the shareholder’s position in the market.

The consequences which were enforces by the bank were managed by bringing out the new

policies and maintain a controllable environment in the banks specially while granting the loans.

Some of the key players that were affecting during the crisis:

1. Treasury Secretary Henry Paulson- One of his popular choices as secretary was to allow

Lehman Brothers to come up short, encouraging a financial exchange drop of almost five

percent. In his energy not to rehash that misstep, he helped push the bank bailout through

Congress.

2. Federal Reserve Chair Ben Bernanke- In charge of the nation's driving money related

arrangement making body during the monetary emergency, Bernanke was the substance

of quantitative facilitating. This strategy included lessening loan fees and infusing more

cash into the economy to urge banks to loan and customers to spend. While numerous

legislators and business analysts were stressed quantitative facilitating would spike

expansion and new resource bubbles, some, including Nobel Prize-winning financial

expert Paul Krugman commend Bernanke's endeavors, and even demand that he helped

get control over the emergency, forestalling a much greater monetary calamity.

3. N.Y. Fed Chair Timothy Geithner- At the point when Lehman imploded, Geithner was

responsible for the most remarkable part of the Federal Reserve. A couple of months after

the fact, he became Treasury Secretary under President Barack Obama. On one hand,

Wall Street criticized him as somebody who over-controlled, while then again, moderate

activists saw him as a device of the banks. During his time at Treasury, Geithner was

additionally entangled in a discussion over his inability to completely report and pay

personal assessment from 2001 to 2004. Geithner apologized for the slip-up and paid the

IRS his exceptional obligation.

Suggestions that can be needed regarding the change in policy.

This suggests incorporating long term uncertainties in the momentary strategy bundles

presently gathered by states and executing categorical approaches pointed toward fortifying the

inventory side of the economy. While the effect of a portion of the last option activities might

arise in the medium – to long term, they warrant thought now in light of the fact that:

They add validity to government's acquiring requests that are forcing long term

obligation, consequently making a commitment to monetary manageability.

They exploit primary changes forced by the emergency to speed up a redeployment of

assets from weak exercises to those that offer the biggest longer term monetary also

friendly advantages.

CONCLUSION

From the above report it can be concluded that the economic crisis that were faced by the

whole world could be controlled then. In the report, the crunch faced by the Lehman Brothers is

discussed and the cause that were handled and confronted globally which led down the condition

to change the polices. The another crisis taken in the report is of the great depression which

happened in the 1930s and let to a great downfall of the economy. The standard of living was

deeply impacted by the crisis. Further the implications that were incurred due to the above events

are elaborated. Also the after impact of the crisis on the world and the lesson which was learned

from the endangerment is discussed. Moreover, the responses of the government in relation to

the calamity can the criticism by the public for the crisis is explained. The suggestion and the

responsible for the most remarkable part of the Federal Reserve. A couple of months after

the fact, he became Treasury Secretary under President Barack Obama. On one hand,

Wall Street criticized him as somebody who over-controlled, while then again, moderate

activists saw him as a device of the banks. During his time at Treasury, Geithner was

additionally entangled in a discussion over his inability to completely report and pay

personal assessment from 2001 to 2004. Geithner apologized for the slip-up and paid the

IRS his exceptional obligation.

Suggestions that can be needed regarding the change in policy.

This suggests incorporating long term uncertainties in the momentary strategy bundles

presently gathered by states and executing categorical approaches pointed toward fortifying the

inventory side of the economy. While the effect of a portion of the last option activities might

arise in the medium – to long term, they warrant thought now in light of the fact that:

They add validity to government's acquiring requests that are forcing long term

obligation, consequently making a commitment to monetary manageability.

They exploit primary changes forced by the emergency to speed up a redeployment of

assets from weak exercises to those that offer the biggest longer term monetary also

friendly advantages.

CONCLUSION

From the above report it can be concluded that the economic crisis that were faced by the

whole world could be controlled then. In the report, the crunch faced by the Lehman Brothers is

discussed and the cause that were handled and confronted globally which led down the condition

to change the polices. The another crisis taken in the report is of the great depression which

happened in the 1930s and let to a great downfall of the economy. The standard of living was

deeply impacted by the crisis. Further the implications that were incurred due to the above events

are elaborated. Also the after impact of the crisis on the world and the lesson which was learned

from the endangerment is discussed. Moreover, the responses of the government in relation to

the calamity can the criticism by the public for the crisis is explained. The suggestion and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

solution that were taken for the improvement of the situation from the crisis and also needed in

today’s times is discussed at the end of the report.

today’s times is discussed at the end of the report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Antoniades, A. and Antonarakis, A.S., 2022. Financial Crises, Environment and Transition.

In Financial Crises, Poverty and Environmental Sustainability: Challenges in the

Context of the SDGs and Covid-19 Recovery. (pp. 25-43). Springer, Cham.

Choi, M.J., Hwang, S. and Im, H., 2020. Cross-border Trade Credit and Trade Flows During the

Global Financial Crisis. Bank of Korea WP. 14.

de Carvalho, F.C and et.al., 2019. Development finance: theory and practice. In The Palgrave

Handbook of Development Economics (pp. 471-505). Palgrave Macmillan, Cham.

Demirgüç-Kunt, A., Peria, M.S.M. and Tressel, T., 2020. The global financial crisis and the

capital structure of firms: Was the impact more severe among SMEs and non-listed

firms?. Journal of Corporate Finance. 60. p.101514.

Diniz-Maganini, N., Rasheed, A.A. and Sheng, H.H., 2021. Exchange rate regimes and price

efficiency: Empirical examination of the impact of financial crisis. Journal of

International Financial Markets, Institutions and Money. 73. p.101361.

Diniz-Maganini, N., Rasheed, A.A. and Sheng, H.H., 2021. Exchange rate regimes and price

efficiency: Empirical examination of the impact of financial crisis. Journal of

International Financial Markets, Institutions and Money. 73. p.101361.

Dixon, A.D., 2018. Reflections on the power in and the power of financial markets.

In Handbook on the Geographies of Power. Edward Elgar Publishing.

Nolan, P., 2020. Finance and the Real Economy: China and the West Since the Asian Financial

Crisis. Routledge.

Singh, A., 2018. Global Financial Crisis and Price Risk Management in Gold Futures Market at

MCX, India. Romanian Economic Journal. 20(68).

Yildiran, M., 2021. EFFECTS OF FINANCE AND ACCOUNTING IN 2008 GLOBAL

FINANCIAL CRISIS 2008 KÜRESEL FİNANS KRİZİNDE FİNANS VE

MUHASEBE YAKLAŞIMLARININ ETKİSİ ISAF 2012 Gaziantep Bildiri Kitabı. (93-

102). Available at SSRN 3954095.

Books and Journals

Antoniades, A. and Antonarakis, A.S., 2022. Financial Crises, Environment and Transition.

In Financial Crises, Poverty and Environmental Sustainability: Challenges in the

Context of the SDGs and Covid-19 Recovery. (pp. 25-43). Springer, Cham.

Choi, M.J., Hwang, S. and Im, H., 2020. Cross-border Trade Credit and Trade Flows During the

Global Financial Crisis. Bank of Korea WP. 14.

de Carvalho, F.C and et.al., 2019. Development finance: theory and practice. In The Palgrave

Handbook of Development Economics (pp. 471-505). Palgrave Macmillan, Cham.

Demirgüç-Kunt, A., Peria, M.S.M. and Tressel, T., 2020. The global financial crisis and the

capital structure of firms: Was the impact more severe among SMEs and non-listed

firms?. Journal of Corporate Finance. 60. p.101514.

Diniz-Maganini, N., Rasheed, A.A. and Sheng, H.H., 2021. Exchange rate regimes and price

efficiency: Empirical examination of the impact of financial crisis. Journal of

International Financial Markets, Institutions and Money. 73. p.101361.

Diniz-Maganini, N., Rasheed, A.A. and Sheng, H.H., 2021. Exchange rate regimes and price

efficiency: Empirical examination of the impact of financial crisis. Journal of

International Financial Markets, Institutions and Money. 73. p.101361.

Dixon, A.D., 2018. Reflections on the power in and the power of financial markets.

In Handbook on the Geographies of Power. Edward Elgar Publishing.

Nolan, P., 2020. Finance and the Real Economy: China and the West Since the Asian Financial

Crisis. Routledge.

Singh, A., 2018. Global Financial Crisis and Price Risk Management in Gold Futures Market at

MCX, India. Romanian Economic Journal. 20(68).

Yildiran, M., 2021. EFFECTS OF FINANCE AND ACCOUNTING IN 2008 GLOBAL

FINANCIAL CRISIS 2008 KÜRESEL FİNANS KRİZİNDE FİNANS VE

MUHASEBE YAKLAŞIMLARININ ETKİSİ ISAF 2012 Gaziantep Bildiri Kitabı. (93-

102). Available at SSRN 3954095.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.