Global Issues for Financial Professionals: Risks and Regulations

VerifiedAdded on 2023/06/04

|20

|5418

|168

Report

AI Summary

This report provides a comprehensive analysis of global issues, risks, and challenges faced by financial institutions and banks. It begins with an introduction to the global banking and financial system, highlighting the roles of key regulatory bodies like the World Bank and central banks. The report then delves into a critical review of global issues, including macroeconomic factors, political and legal instability, increasing competition, technological advancements, and socio-cultural changes, using PESTLE analysis to assess their impact. It examines specific risks such as capital adequacy, misconduct of operations, anti-money laundering, and non-performing loans. The report also discusses the current regulatory systems, emphasizing the roles of central banks, the European Central Bank, and the European Banking Authority. Finally, it proposes improvements to the regulatory environment to better organize, manage, and control banking and financial operations, offering insights for financial professionals navigating the complex global landscape.

Global Issues 1

Global Issues for the Financial Professional

Global Issues for the Financial Professional

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Global Issues 2

Contents

Introduction.................................................................................................................................................3

Critical Review of the global issues and Risks for the Financial Institutions or Banks...............................4

Current Regulatory System.........................................................................................................................9

Improvements to the Current Regulation System of the Banking and Finance..........................................14

Conclusion.................................................................................................................................................16

References.................................................................................................................................................18

Contents

Introduction.................................................................................................................................................3

Critical Review of the global issues and Risks for the Financial Institutions or Banks...............................4

Current Regulatory System.........................................................................................................................9

Improvements to the Current Regulation System of the Banking and Finance..........................................14

Conclusion.................................................................................................................................................16

References.................................................................................................................................................18

Global Issues 3

Introduction

The purpose of the report is to analyze the risks and challenges in the global scenario for the

banks and FIs from the global issues and the ways for the improvement in the legislative system

and regulations of the globalbanking system and financial operations.

The Global banking and financial system isthe large and wide framework of the legal agreements

between the global financial institutions or banks in order to facilitate the international financial

capital flows (both inflows and outflows) for the purpose of the trade financing or global

investment. It is headed by the banking and financial regulators, supervisors, and institutions

(like The World Bank, International Monetary Fund, the Central European Bank, and others) for

regulating and controlling the international banks, financial institutions, and insurance companies

at the superannuation level in the global industry.At the global level, it has been observed that

Central Bank is majorly responsible (in Europe, the UK, the USA, the UAE, except in the case of

Commonwealth Bank in Australia and Reserve Bank in India) for the legislative structures, legal

policies, and jurisdictions for the financial institutions (FIs) and banks in the most of the

countries. The banks in the global context involve the categories including the Central banks,

Merchant or Investment banks, Commercial banks, Retail banks, Cooperative banks, Public

banks, Industrial banks, and Development Banks(Reuvid, 2014).

This assignment looks at the major global issues, challenges, and risks for the banks and

financial institutions facing while operating in the regulatory and competitive environment at the

international level. The report also describes the legislation system, regulation policies, and

procedures for supervising and monitoring the banking and financial operations and the impact

of the regulatory changes on the operations in the global setting. Finally, the suggestions are

Introduction

The purpose of the report is to analyze the risks and challenges in the global scenario for the

banks and FIs from the global issues and the ways for the improvement in the legislative system

and regulations of the globalbanking system and financial operations.

The Global banking and financial system isthe large and wide framework of the legal agreements

between the global financial institutions or banks in order to facilitate the international financial

capital flows (both inflows and outflows) for the purpose of the trade financing or global

investment. It is headed by the banking and financial regulators, supervisors, and institutions

(like The World Bank, International Monetary Fund, the Central European Bank, and others) for

regulating and controlling the international banks, financial institutions, and insurance companies

at the superannuation level in the global industry.At the global level, it has been observed that

Central Bank is majorly responsible (in Europe, the UK, the USA, the UAE, except in the case of

Commonwealth Bank in Australia and Reserve Bank in India) for the legislative structures, legal

policies, and jurisdictions for the financial institutions (FIs) and banks in the most of the

countries. The banks in the global context involve the categories including the Central banks,

Merchant or Investment banks, Commercial banks, Retail banks, Cooperative banks, Public

banks, Industrial banks, and Development Banks(Reuvid, 2014).

This assignment looks at the major global issues, challenges, and risks for the banks and

financial institutions facing while operating in the regulatory and competitive environment at the

international level. The report also describes the legislation system, regulation policies, and

procedures for supervising and monitoring the banking and financial operations and the impact

of the regulatory changes on the operations in the global setting. Finally, the suggestions are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Global Issues 4

proposed for improving the regulatory environment in the global banking and financial scenario

for well organizing, managing, and controlling the banking and financial operations (Rael, 2017).

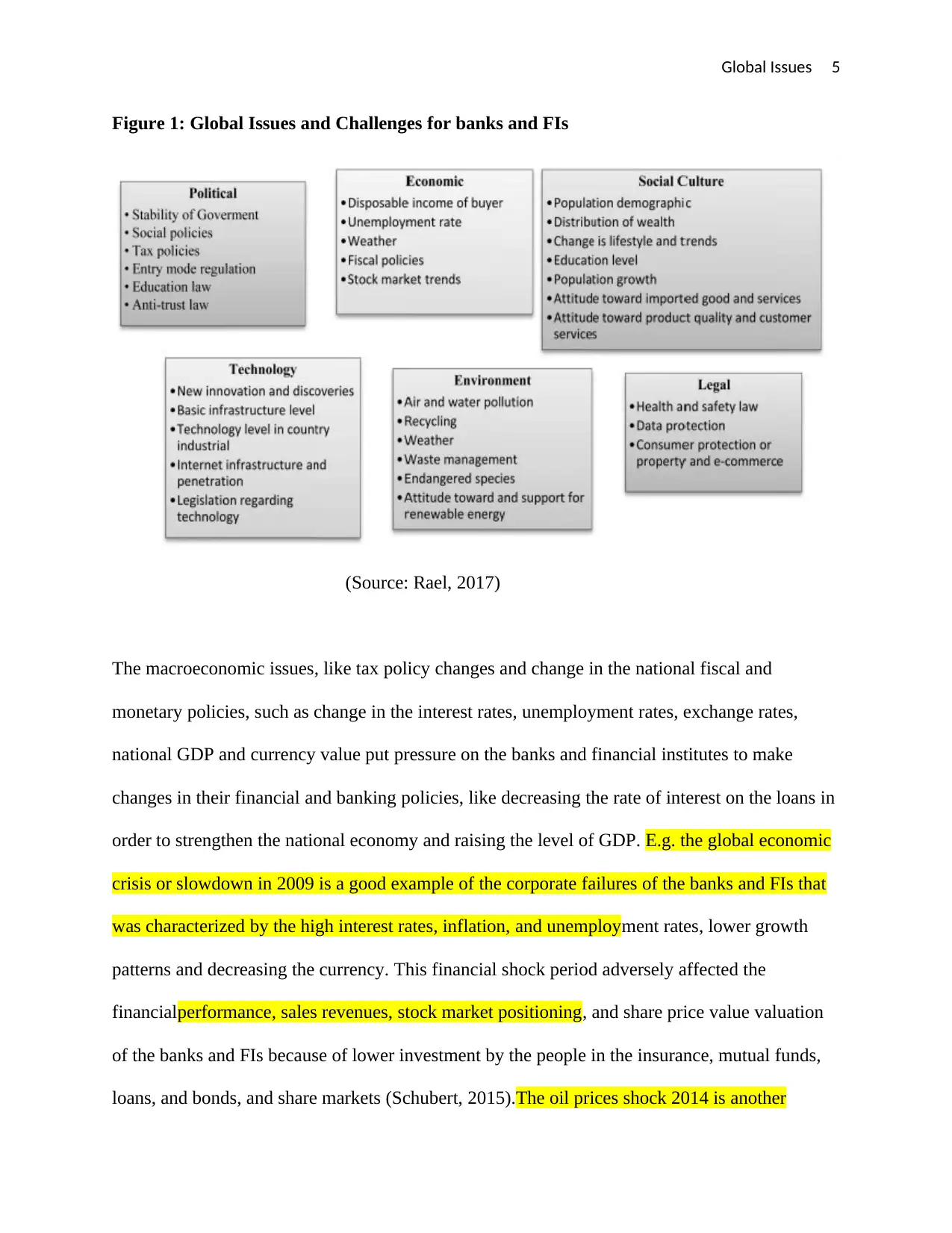

Critical Review of the global issues and Risks for the Financial Institutions or Banks

In the modern business environment of the International level, most of the banks or financial

institutions (FIs) face the complex global issue and challenges. PESTLE analysis is used to

analyze the impact of the external environmental changes or global issues, like the political

interferences, changing economic conditions, global financial crisis, changing customers’ needs

and preferences, technological risks, legal issues (taxation, laws and regulations), and

environmental factors on the banking operations, investments, financial policies, and insurance

operations of the banks, FIs, or insurance companies. For example, the increasing terror attacks

macroeconomic issues, rapid technology changes and increasing cyber-attacks, regulatory

changes, tax reforms, socio-cultural changes, and environmental pressures are such external

issues that may affect the financial policies, product planning and investment policies, financial

policies, and share market positioning, and foreign exchange policies of the banks and FIs while

operating at the international regulatory and competitive environment.Along with this, the banks

and FIS face issues, like the capital availability or finance sufficiency, quality of risk

management, increasing competition level from entry of new banks and FIs, stock market

changing trends, fiscal and monetary policy changes, and changing labor market conditions (like

the shortage of skilled labors) that can significantly influence their banking and financial

operations in the global setting (Stoner, 2012).The misconduct of the operations, Anti-money

Laundering, and IFRS 9 and IFRS 16, and non-performing loans are some growing challenges

for thebanks and FIs at the global scales.

proposed for improving the regulatory environment in the global banking and financial scenario

for well organizing, managing, and controlling the banking and financial operations (Rael, 2017).

Critical Review of the global issues and Risks for the Financial Institutions or Banks

In the modern business environment of the International level, most of the banks or financial

institutions (FIs) face the complex global issue and challenges. PESTLE analysis is used to

analyze the impact of the external environmental changes or global issues, like the political

interferences, changing economic conditions, global financial crisis, changing customers’ needs

and preferences, technological risks, legal issues (taxation, laws and regulations), and

environmental factors on the banking operations, investments, financial policies, and insurance

operations of the banks, FIs, or insurance companies. For example, the increasing terror attacks

macroeconomic issues, rapid technology changes and increasing cyber-attacks, regulatory

changes, tax reforms, socio-cultural changes, and environmental pressures are such external

issues that may affect the financial policies, product planning and investment policies, financial

policies, and share market positioning, and foreign exchange policies of the banks and FIs while

operating at the international regulatory and competitive environment.Along with this, the banks

and FIS face issues, like the capital availability or finance sufficiency, quality of risk

management, increasing competition level from entry of new banks and FIs, stock market

changing trends, fiscal and monetary policy changes, and changing labor market conditions (like

the shortage of skilled labors) that can significantly influence their banking and financial

operations in the global setting (Stoner, 2012).The misconduct of the operations, Anti-money

Laundering, and IFRS 9 and IFRS 16, and non-performing loans are some growing challenges

for thebanks and FIs at the global scales.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Global Issues 5

Figure 1: Global Issues and Challenges for banks and FIs

(Source: Rael, 2017)

The macroeconomic issues, like tax policy changes and change in the national fiscal and

monetary policies, such as change in the interest rates, unemployment rates, exchange rates,

national GDP and currency value put pressure on the banks and financial institutes to make

changes in their financial and banking policies, like decreasing the rate of interest on the loans in

order to strengthen the national economy and raising the level of GDP. E.g. the global economic

crisis or slowdown in 2009 is a good example of the corporate failures of the banks and FIs that

was characterized by the high interest rates, inflation, and unemployment rates, lower growth

patterns and decreasing the currency. This financial shock period adversely affected the

financialperformance, sales revenues, stock market positioning, and share price value valuation

of the banks and FIs because of lower investment by the people in the insurance, mutual funds,

loans, and bonds, and share markets (Schubert, 2015).The oil prices shock 2014 is another

Figure 1: Global Issues and Challenges for banks and FIs

(Source: Rael, 2017)

The macroeconomic issues, like tax policy changes and change in the national fiscal and

monetary policies, such as change in the interest rates, unemployment rates, exchange rates,

national GDP and currency value put pressure on the banks and financial institutes to make

changes in their financial and banking policies, like decreasing the rate of interest on the loans in

order to strengthen the national economy and raising the level of GDP. E.g. the global economic

crisis or slowdown in 2009 is a good example of the corporate failures of the banks and FIs that

was characterized by the high interest rates, inflation, and unemployment rates, lower growth

patterns and decreasing the currency. This financial shock period adversely affected the

financialperformance, sales revenues, stock market positioning, and share price value valuation

of the banks and FIs because of lower investment by the people in the insurance, mutual funds,

loans, and bonds, and share markets (Schubert, 2015).The oil prices shock 2014 is another

Global Issues 6

example of the global economic crisis that is a major issue for poor financial performance of the

FIs and banks; the increasing oil prices slow down the businesses of the oil companies that affect

the national economic growth, restructuring of the businesses, and decrease in the government

projects that in turn affect the asset value and quality, customers’ investments, profitability, and

liquidity of the FIs and banks.

The global political and legal issues, like political instability, government intervention, financial

policies and regulatory compliance by the finance minister, and tax rates also affect the banking

and financial operations. The global issues, like the terrorism risk exposure, geopolitical risks,

instability of the political system, changing regulatory environment, and changing the

international banking standards and regulations are such factors that enforce for the change in the

financial, investment, and operational policies and strategies of the banks and FIs. For example,

the banks and FIs can face the legal risks because of changing regulatory environment at the

international level with the updates of new laws and regulations, like Data protection laws,

Consumer protection laws, and Anti-Trust legislationthat can enforce the banks and FIs in the

term ofsecurity from the credit losses, privacy of file and documents, data security, and good

customer trust(RSM, 2017).

The increasinglycompetitive environment in the global context creates stiff competition for the

foreign banks from the local banks operating their banking operations in a number of nations

from many years. The local banks are creating the cost competitiveness, like pricing war with the

foreign banks.For example, two Western banks in the UAE have stopped their onshore banking

operations and two other foreign banks curtailed their SME operations and retail banking

ventures because of facing the high level or tougher competition level from the local European

banks, money laundering system and difficult working environment for the foreign banks.

example of the global economic crisis that is a major issue for poor financial performance of the

FIs and banks; the increasing oil prices slow down the businesses of the oil companies that affect

the national economic growth, restructuring of the businesses, and decrease in the government

projects that in turn affect the asset value and quality, customers’ investments, profitability, and

liquidity of the FIs and banks.

The global political and legal issues, like political instability, government intervention, financial

policies and regulatory compliance by the finance minister, and tax rates also affect the banking

and financial operations. The global issues, like the terrorism risk exposure, geopolitical risks,

instability of the political system, changing regulatory environment, and changing the

international banking standards and regulations are such factors that enforce for the change in the

financial, investment, and operational policies and strategies of the banks and FIs. For example,

the banks and FIs can face the legal risks because of changing regulatory environment at the

international level with the updates of new laws and regulations, like Data protection laws,

Consumer protection laws, and Anti-Trust legislationthat can enforce the banks and FIs in the

term ofsecurity from the credit losses, privacy of file and documents, data security, and good

customer trust(RSM, 2017).

The increasinglycompetitive environment in the global context creates stiff competition for the

foreign banks from the local banks operating their banking operations in a number of nations

from many years. The local banks are creating the cost competitiveness, like pricing war with the

foreign banks.For example, two Western banks in the UAE have stopped their onshore banking

operations and two other foreign banks curtailed their SME operations and retail banking

ventures because of facing the high level or tougher competition level from the local European

banks, money laundering system and difficult working environment for the foreign banks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Global Issues 7

These banks also facefinancial security issues, like terrorism financial risk exposure due to the

increasing terrorist activities at the international level (Stoner, 2012). Along with this, the banks

are facing a high level of competition from the financial technological firms

(FinTechcompanies)that provide the financial services based on the digital software. For

example, the digital payment app, like Google Wallet, PayPal, Skrill, Amazon App, and digital

wallets that are based on the application software for payment or customer service transactions

and create a stiff competition to the banks and FIs.

The banks and FIs also facing the global issue, like business risks arise when the banks and FIs

fail to implement the long-term plan and strategies to adapt to the external changes, market

conditions, customers’ demands, and shareholders’ expectations as well as inability to overcome

the business risks. The financial firms, banks, and insurance companies also face the operational

and systematic risks due to the human errors, server errors, the failure of IT systems, data loss or

increasing insecurity risk, and customer frauds with the purpose of the fraudulent practices or

deception to bankers or FIs, that may affect the banking business and financial management

operations of the banks and FIs.

The regulation compliance is the biggest issue for the banks and FIs as the banks are feeling

pressures from the systematic risk or errors, like the operational burden, increased sanction, and

due diligence (Haine, 2018). For example, the bankingsystem faces issues from the entrepreneurs

or SMEs who face the bank account-related problems because of the complex procedures of

account opening and documentation as well the complex verification process, insufficient

transparencies, and not enough guidelines from the bankers. More than 60% of the SMEs state

that they struggled to meet the debts because of the payment delays as well as failed in securing

new credit lines because of reducing exposure of the banks toward the SMEs. The SMEs are not

These banks also facefinancial security issues, like terrorism financial risk exposure due to the

increasing terrorist activities at the international level (Stoner, 2012). Along with this, the banks

are facing a high level of competition from the financial technological firms

(FinTechcompanies)that provide the financial services based on the digital software. For

example, the digital payment app, like Google Wallet, PayPal, Skrill, Amazon App, and digital

wallets that are based on the application software for payment or customer service transactions

and create a stiff competition to the banks and FIs.

The banks and FIs also facing the global issue, like business risks arise when the banks and FIs

fail to implement the long-term plan and strategies to adapt to the external changes, market

conditions, customers’ demands, and shareholders’ expectations as well as inability to overcome

the business risks. The financial firms, banks, and insurance companies also face the operational

and systematic risks due to the human errors, server errors, the failure of IT systems, data loss or

increasing insecurity risk, and customer frauds with the purpose of the fraudulent practices or

deception to bankers or FIs, that may affect the banking business and financial management

operations of the banks and FIs.

The regulation compliance is the biggest issue for the banks and FIs as the banks are feeling

pressures from the systematic risk or errors, like the operational burden, increased sanction, and

due diligence (Haine, 2018). For example, the bankingsystem faces issues from the entrepreneurs

or SMEs who face the bank account-related problems because of the complex procedures of

account opening and documentation as well the complex verification process, insufficient

transparencies, and not enough guidelines from the bankers. More than 60% of the SMEs state

that they struggled to meet the debts because of the payment delays as well as failed in securing

new credit lines because of reducing exposure of the banks toward the SMEs. The SMEs are not

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Global Issues 8

the most attractive customer segments for the banks in spite of the SMEs contribute to more than

60% of the global economy (Gangreddiwar, 2015).

The socio-cultural issues are faced by the banks and FIs due to the not predetermined customer

buying behaviors, changing preferences and expectations, and distinct investment patterns that

greatly affect the financial operations and banking businesses of the FIs and banks. For example,

the banks are feeling pressure for not delivering the quality services that are demanding from the

customers’ expectations (Burk, 2018). Along with this, the banks in many countries are not able

to satisfy the shareholders to some extent because of not delivering the enough on their

investments or significant returns on the equity.

The global issue, like reputational risk is subjected to the loss of the reputation of the FIs and

banks at the international level that may be caused due to the ineffective customer service and

poor customers’ feedbacks or negative reviews, rigid banking system, ineffective business

decisions, and data manipulations that may cause for the decreasing market positioning and the

loss of the customer share.Thetechnology issues or risks are caused by the failure of the IT

systems, increasing IT frauds and risks, and ineffective security system that have influenced the

financial operations of the FIs and banking operations (Spedding and Rose, 2008). e.g. the data

security risks is a big concern for the FIs and banks because of the system security problems,

increasing IT frauds by the hackers or cybercriminals, identity theft problems, and others that

maythreaten the privacy of files, documents and customer transaction information, the loss of

important data, credit losses and insecurity issues by other FIs, banks, and hackers.

The banks, financiers, and insurance companies face the global issue, like the liquidation risks

due tothe capital inadequacy, the lack of marketability of the investments, lending issues in the

daily customer operations, shares or insurance products not sold or bought quickly that can cause

the most attractive customer segments for the banks in spite of the SMEs contribute to more than

60% of the global economy (Gangreddiwar, 2015).

The socio-cultural issues are faced by the banks and FIs due to the not predetermined customer

buying behaviors, changing preferences and expectations, and distinct investment patterns that

greatly affect the financial operations and banking businesses of the FIs and banks. For example,

the banks are feeling pressure for not delivering the quality services that are demanding from the

customers’ expectations (Burk, 2018). Along with this, the banks in many countries are not able

to satisfy the shareholders to some extent because of not delivering the enough on their

investments or significant returns on the equity.

The global issue, like reputational risk is subjected to the loss of the reputation of the FIs and

banks at the international level that may be caused due to the ineffective customer service and

poor customers’ feedbacks or negative reviews, rigid banking system, ineffective business

decisions, and data manipulations that may cause for the decreasing market positioning and the

loss of the customer share.Thetechnology issues or risks are caused by the failure of the IT

systems, increasing IT frauds and risks, and ineffective security system that have influenced the

financial operations of the FIs and banking operations (Spedding and Rose, 2008). e.g. the data

security risks is a big concern for the FIs and banks because of the system security problems,

increasing IT frauds by the hackers or cybercriminals, identity theft problems, and others that

maythreaten the privacy of files, documents and customer transaction information, the loss of

important data, credit losses and insecurity issues by other FIs, banks, and hackers.

The banks, financiers, and insurance companies face the global issue, like the liquidation risks

due tothe capital inadequacy, the lack of marketability of the investments, lending issues in the

daily customer operations, shares or insurance products not sold or bought quickly that can cause

Global Issues 9

for the inability of the bankers and FIs to repay the investors. The credit risks are caused due to

the high credit exposures or inability/failure of the banks and FIs to meet the financial

obligations because of the financial failures in the bank loans, equities, bonds, swaps, bonds,

foreign commercial exchanges or interbank transactions(Richardson, Steffen, and Liverman,

2011).

Current Regulatory System

The World Bank acts as the main regulatory body to govern, supervise, and control over the

banking operations of the local banks and the foreign banks in each country. The World Bank

maintains the national government’s reserve of the gold, financial policies, banking regulations,

and the foreign currencies. There are different regulation mechanisms, legislation systems, and

structures for the banking and financial regulation and the conducts of the insurance operations.

The national governments in different countries employ the respective finance ministers,

regulatory agencies, and treasuries for influencing the internal controls, tax impositions, tariffs,

capital market control and the regulatory intervention through the banking regulators (like

Central Bank in most countries). The Central Banks (like in the UK, the USA, the UAE and most

of the European countries) provide the onshore banking regulations for directing the banking,

monetary, and credit policy and supervises in accordance of the State’s general policy in the

manner that it supports the national economy and currency stability(The World Bank Group,

2018).

In Europe, the European Central Bank (ECB) and European Banking Authority (EBA) are

responsible for supervising, controlling, and regulating the banking operations. The EBA

controls on the system risks, operational issues, or institutional weaknesses for the European

for the inability of the bankers and FIs to repay the investors. The credit risks are caused due to

the high credit exposures or inability/failure of the banks and FIs to meet the financial

obligations because of the financial failures in the bank loans, equities, bonds, swaps, bonds,

foreign commercial exchanges or interbank transactions(Richardson, Steffen, and Liverman,

2011).

Current Regulatory System

The World Bank acts as the main regulatory body to govern, supervise, and control over the

banking operations of the local banks and the foreign banks in each country. The World Bank

maintains the national government’s reserve of the gold, financial policies, banking regulations,

and the foreign currencies. There are different regulation mechanisms, legislation systems, and

structures for the banking and financial regulation and the conducts of the insurance operations.

The national governments in different countries employ the respective finance ministers,

regulatory agencies, and treasuries for influencing the internal controls, tax impositions, tariffs,

capital market control and the regulatory intervention through the banking regulators (like

Central Bank in most countries). The Central Banks (like in the UK, the USA, the UAE and most

of the European countries) provide the onshore banking regulations for directing the banking,

monetary, and credit policy and supervises in accordance of the State’s general policy in the

manner that it supports the national economy and currency stability(The World Bank Group,

2018).

In Europe, the European Central Bank (ECB) and European Banking Authority (EBA) are

responsible for supervising, controlling, and regulating the banking operations. The EBA

controls on the system risks, operational issues, or institutional weaknesses for the European

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Global Issues 10

banks. The European Securities and Marketing Authority (ESMA) controls on the capital

markets through the regulation mechanism and control on the financial operations, shares, and

stock exchanges. But, In Australia, the Commonwealth Bank is the main regulator for the

banking and financial operations. Along with this, the Australian Securities and Investment

Commission (ASIC) and the Australian Prudential Regulation Authority (APRA) are responsible

for supervising the banks, FIs, and insurers. In India, the Reserve Bank of India is the main

governmental body for supervising the banking operations, and the Securities and Exchange

Board of India for the capital markets, and IRDA (Insurance Regulatory Development Authority

for the insurance companies. So, there are different regulators in different countries for banking

regulation, financial regulation, and controlling the insurance operations(Khushurshahi, 2017).

The banks and FIs are needed to operate the global financial operations or investment ventures

under the regulatory mechanism of the global regulators (like the World Bank Group) or the

multinational organization, like International Monetary Fund, and the International Settlement of

Banks (like Basel Committee) that provide the regulatory guidelines for the banking supervision

and global financial system.In the sequence, other multinational organizations include

International Organization of Security Commission (coordinates for the financial security

regulations), International Association of Insurance Supervisors (IAIS) (supervision for the

insurance industry), International Accounting Standard Board (provides accounting and auditing

standards), Financial Stability Board (coordinate information and other activities among the

countries), and Financial Action Task Force on Money Laundering (collaboration on the money

laundering conflicts and terrorism finance battling).

The Banking Law in a number of countries establishes the legal provisions for the banking

regulations including the issuance of the currency, supervising, regulating, organizing, and

banks. The European Securities and Marketing Authority (ESMA) controls on the capital

markets through the regulation mechanism and control on the financial operations, shares, and

stock exchanges. But, In Australia, the Commonwealth Bank is the main regulator for the

banking and financial operations. Along with this, the Australian Securities and Investment

Commission (ASIC) and the Australian Prudential Regulation Authority (APRA) are responsible

for supervising the banks, FIs, and insurers. In India, the Reserve Bank of India is the main

governmental body for supervising the banking operations, and the Securities and Exchange

Board of India for the capital markets, and IRDA (Insurance Regulatory Development Authority

for the insurance companies. So, there are different regulators in different countries for banking

regulation, financial regulation, and controlling the insurance operations(Khushurshahi, 2017).

The banks and FIs are needed to operate the global financial operations or investment ventures

under the regulatory mechanism of the global regulators (like the World Bank Group) or the

multinational organization, like International Monetary Fund, and the International Settlement of

Banks (like Basel Committee) that provide the regulatory guidelines for the banking supervision

and global financial system.In the sequence, other multinational organizations include

International Organization of Security Commission (coordinates for the financial security

regulations), International Association of Insurance Supervisors (IAIS) (supervision for the

insurance industry), International Accounting Standard Board (provides accounting and auditing

standards), Financial Stability Board (coordinate information and other activities among the

countries), and Financial Action Task Force on Money Laundering (collaboration on the money

laundering conflicts and terrorism finance battling).

The Banking Law in a number of countries establishes the legal provisions for the banking

regulations including the issuance of the currency, supervising, regulating, organizing, and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Global Issues 11

supporting the banking systems and credit policy, advising the governments on the financial

matters and the monetary issues, and acting as a government’s bank for other banks. It acts as a

state’s financial agent at the global financial institutions. The Banking Law is related to

providing the regulatory provisions for the licensing, registrations, and operational controls of

the commercial banks, financial institutions, investment banks, representative banking or

financial service offices, and monetary and financial intermediaries in the countries (Export.gov,

2018).

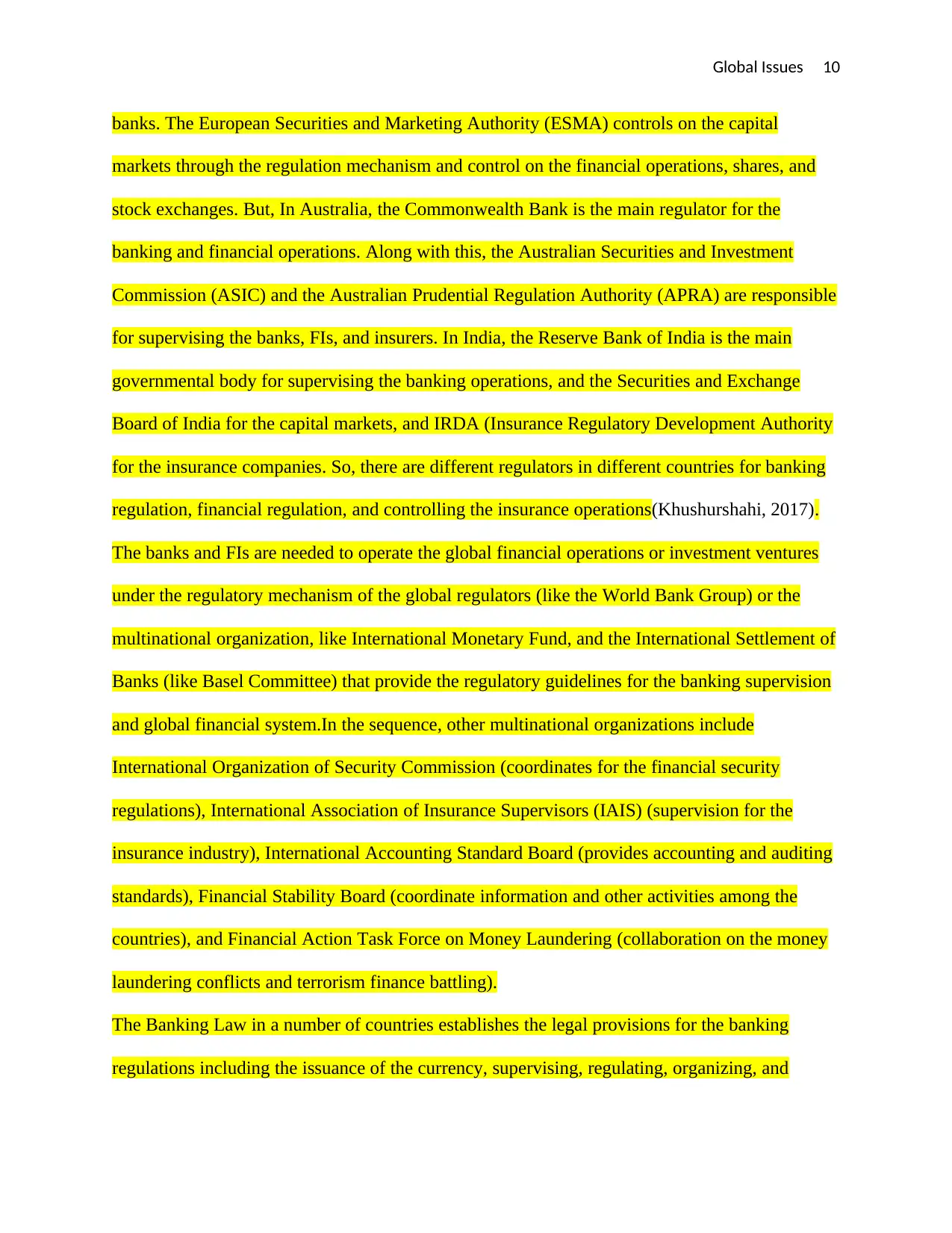

Figure 2: Global Banking Regulation System

(Source: EY.Com Publications, 2018)

The Banking Law is not applicable to governmental developmental funds, pension funds, private

savings, insurance companies and agencies, public credit institutions, and governmental

investment agencies and institutions. The commercial code set-out by the international Banking

Law contains the details provisions for governing the bank accounts and deposits, loans,

cheques, the bill of exchange, promissory note, and documentary credits and guarantees. Under

supporting the banking systems and credit policy, advising the governments on the financial

matters and the monetary issues, and acting as a government’s bank for other banks. It acts as a

state’s financial agent at the global financial institutions. The Banking Law is related to

providing the regulatory provisions for the licensing, registrations, and operational controls of

the commercial banks, financial institutions, investment banks, representative banking or

financial service offices, and monetary and financial intermediaries in the countries (Export.gov,

2018).

Figure 2: Global Banking Regulation System

(Source: EY.Com Publications, 2018)

The Banking Law is not applicable to governmental developmental funds, pension funds, private

savings, insurance companies and agencies, public credit institutions, and governmental

investment agencies and institutions. The commercial code set-out by the international Banking

Law contains the details provisions for governing the bank accounts and deposits, loans,

cheques, the bill of exchange, promissory note, and documentary credits and guarantees. Under

Global Issues 12

the Business Laws, the private or commercial banks in each country receive the funds from the

public in the market in the form of time deposits, demand, under notice, or replacement of

deposit certificates or debt instruments. The Banking Law also provides the regulation or legal

procedures related to issuance and collection of cheques, trading in foreign exchange of money

and precious metals (like gold), and placing of the private or public bonds(EY.Com Publications,

2018).

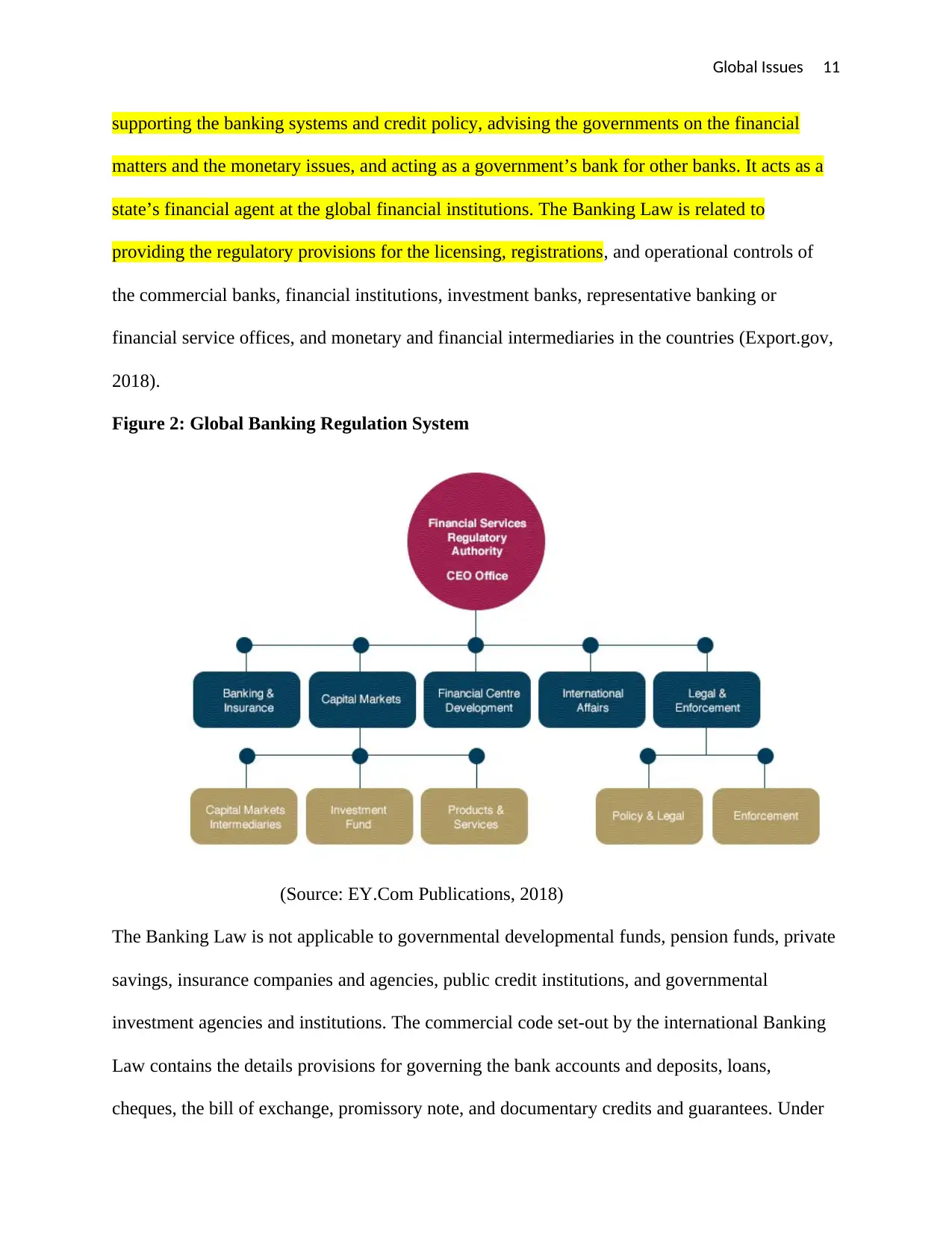

Figure 3: Global Forum for Banking and Financial Operations

The Central Bank in most of the countries is the primary national regulatory body that is

primarily responsible for overseeing, supervising, and monitoring the banking operations

(Anderson and Associates, 2018). For example, the current regulatory system in the European

the Business Laws, the private or commercial banks in each country receive the funds from the

public in the market in the form of time deposits, demand, under notice, or replacement of

deposit certificates or debt instruments. The Banking Law also provides the regulation or legal

procedures related to issuance and collection of cheques, trading in foreign exchange of money

and precious metals (like gold), and placing of the private or public bonds(EY.Com Publications,

2018).

Figure 3: Global Forum for Banking and Financial Operations

The Central Bank in most of the countries is the primary national regulatory body that is

primarily responsible for overseeing, supervising, and monitoring the banking operations

(Anderson and Associates, 2018). For example, the current regulatory system in the European

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.