Analyzing the Global Financial Crisis of 2007: An Economics Study

VerifiedAdded on 2022/10/19

|11

|2681

|417

Essay

AI Summary

This economics assignment delves into the causes of the 2007 global financial crisis, exploring the debate between financial innovations creating safe debt and the collapse of the housing bubble. The paper addresses the economic downturn by answering specific questions related to debt contracts, shared responsibility mortgages, securitization, and government interventions. It examines the views of economists like Amir Sufi, Atif Mian, Hammad Siddiqi, and Ricardo Caballero, assessing the impact of debt, money supply, and imbalances in the economy. The analysis covers the role of the housing bubble, safe debt creation, and the government's response, concluding that financial innovations, coupled with the housing bubble, were the primary drivers of the crisis, and recommends increased monitoring of the financial market to prevent future occurrences.

1

ECONOMICS ASSIGNMENT

ECONOMICS FOR MANAGERS

ECONOMICS ASSIGNMENT

ECONOMICS FOR MANAGERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive summary

The recession of 2007 was one of the biggest economic shocks in the world after the great

depression of 1929. The effects of recession spread across the US border to hit different

countries of the world. Some of the countries have not been able to bounce back from the

shock it had experienced. This paper discusses the main reason underneath the global

financial crisis of 2007. The study answers some of the questions and through that, it

discusses the reason for the global crisis.

Executive summary

The recession of 2007 was one of the biggest economic shocks in the world after the great

depression of 1929. The effects of recession spread across the US border to hit different

countries of the world. Some of the countries have not been able to bounce back from the

shock it had experienced. This paper discusses the main reason underneath the global

financial crisis of 2007. The study answers some of the questions and through that, it

discusses the reason for the global crisis.

3

Contents

Introduction................................................................................................................................3

Question 1..................................................................................................................................3

Question 2..................................................................................................................................4

Question 3..................................................................................................................................5

Question 4..................................................................................................................................5

Question 5..................................................................................................................................6

Question 6..................................................................................................................................7

Question 7..................................................................................................................................7

Conclusion and recommendations.............................................................................................8

Reference....................................................................................................................................9

Contents

Introduction................................................................................................................................3

Question 1..................................................................................................................................3

Question 2..................................................................................................................................4

Question 3..................................................................................................................................5

Question 4..................................................................................................................................5

Question 5..................................................................................................................................6

Question 6..................................................................................................................................7

Question 7..................................................................................................................................7

Conclusion and recommendations.............................................................................................8

Reference....................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

Economic depression is known as the phase when the global or national production of the

economy is low owing to the low aggregate demand for goods and services in the market. In

this phase, the unemployment reduces along with production that is not desirable for

economic growth and development. One such economic downturn of this century was the

global financial crisis of the year 2007. The objective of the paper is to discuss the reasons

underneath the global recession that contracted global production in all parts of the world.

The paper will approach the study question by answering a few questions that will lead to the

debate regarding the cause of the global financial crisis of 2007.

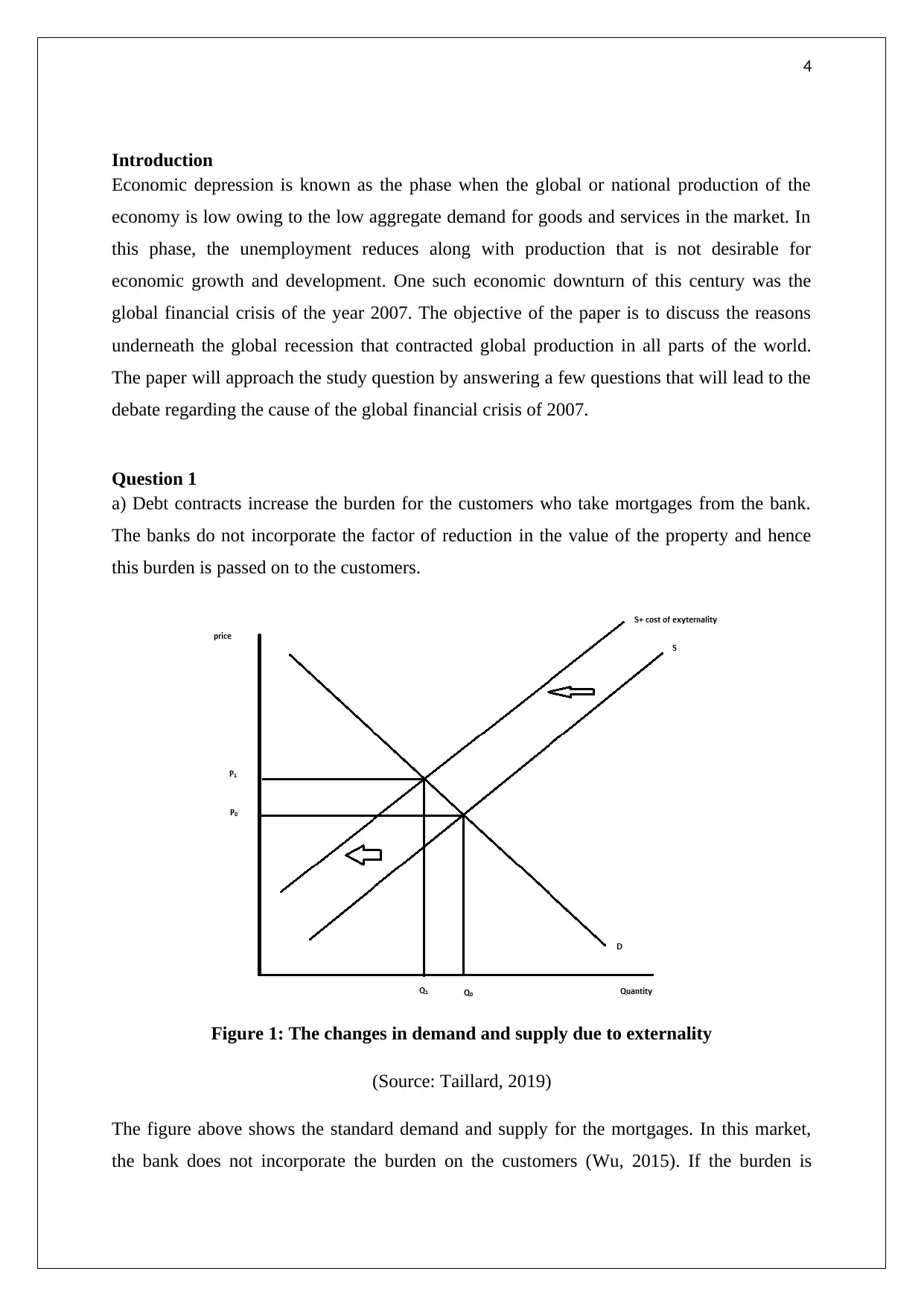

Question 1

a) Debt contracts increase the burden for the customers who take mortgages from the bank.

The banks do not incorporate the factor of reduction in the value of the property and hence

this burden is passed on to the customers.

Figure 1: The changes in demand and supply due to externality

(Source: Taillard, 2019)

The figure above shows the standard demand and supply for the mortgages. In this market,

the bank does not incorporate the burden on the customers (Wu, 2015). If the burden is

Introduction

Economic depression is known as the phase when the global or national production of the

economy is low owing to the low aggregate demand for goods and services in the market. In

this phase, the unemployment reduces along with production that is not desirable for

economic growth and development. One such economic downturn of this century was the

global financial crisis of the year 2007. The objective of the paper is to discuss the reasons

underneath the global recession that contracted global production in all parts of the world.

The paper will approach the study question by answering a few questions that will lead to the

debate regarding the cause of the global financial crisis of 2007.

Question 1

a) Debt contracts increase the burden for the customers who take mortgages from the bank.

The banks do not incorporate the factor of reduction in the value of the property and hence

this burden is passed on to the customers.

Figure 1: The changes in demand and supply due to externality

(Source: Taillard, 2019)

The figure above shows the standard demand and supply for the mortgages. In this market,

the bank does not incorporate the burden on the customers (Wu, 2015). If the burden is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

incorporated the cost of production will increase and the supply curve shifts upward leading

to a higher price and lower quantity of the mortgage.

b)

In mitigating the problem the coarse theorem can be applied where the banks would pay the

customers for the loss in value of the property proportional to the stake of the banks in the

property (Gorton, 2017). In that way, the banks would incorporate the social cost into the

standard mortgage supply and hence socially efficient outcome would be provided by the

market.

Question 2

Shared responsibility mortgages will have its interest payments and mortgage balance linked

to the house price index in the local market depending on the area zip code. As a result, when

the price of the property will reduce the interest payment and the mortgage balance would

also reduce at the same rate as the reduction the price. Therefore, the burden from the

customer will be shared between the lenders and the borrowers leading to a decline in

negative externality (He et al. 2016). Under this shared responsibly mortgages, the borrower

will also have pay price if the property is sold at a higher value than it was bought so that the

capital gain is divided between the customer and the bank.

incorporated the cost of production will increase and the supply curve shifts upward leading

to a higher price and lower quantity of the mortgage.

b)

In mitigating the problem the coarse theorem can be applied where the banks would pay the

customers for the loss in value of the property proportional to the stake of the banks in the

property (Gorton, 2017). In that way, the banks would incorporate the social cost into the

standard mortgage supply and hence socially efficient outcome would be provided by the

market.

Question 2

Shared responsibility mortgages will have its interest payments and mortgage balance linked

to the house price index in the local market depending on the area zip code. As a result, when

the price of the property will reduce the interest payment and the mortgage balance would

also reduce at the same rate as the reduction the price. Therefore, the burden from the

customer will be shared between the lenders and the borrowers leading to a decline in

negative externality (He et al. 2016). Under this shared responsibly mortgages, the borrower

will also have pay price if the property is sold at a higher value than it was bought so that the

capital gain is divided between the customer and the bank.

6

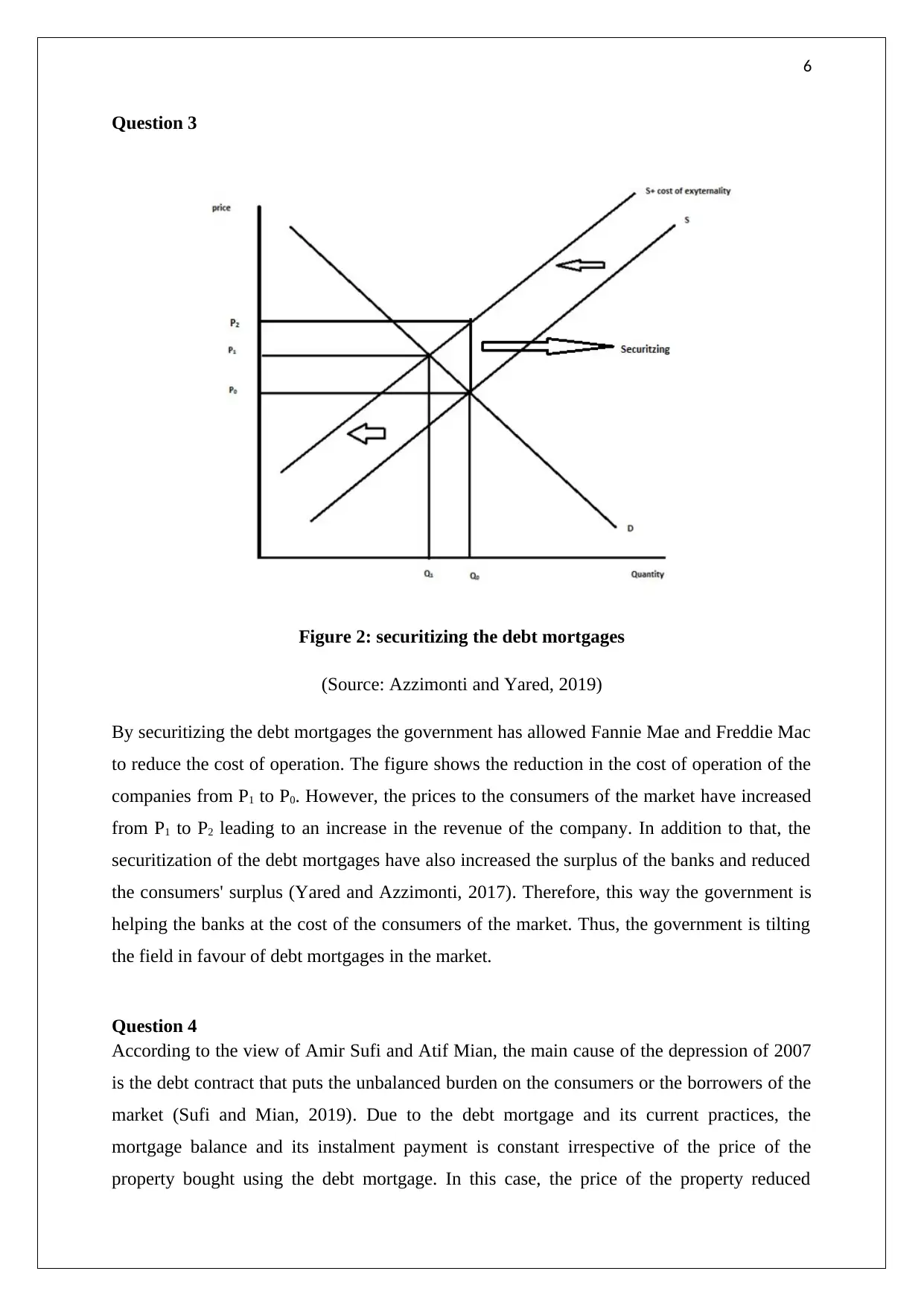

Question 3

Figure 2: securitizing the debt mortgages

(Source: Azzimonti and Yared, 2019)

By securitizing the debt mortgages the government has allowed Fannie Mae and Freddie Mac

to reduce the cost of operation. The figure shows the reduction in the cost of operation of the

companies from P1 to P0. However, the prices to the consumers of the market have increased

from P1 to P2 leading to an increase in the revenue of the company. In addition to that, the

securitization of the debt mortgages have also increased the surplus of the banks and reduced

the consumers' surplus (Yared and Azzimonti, 2017). Therefore, this way the government is

helping the banks at the cost of the consumers of the market. Thus, the government is tilting

the field in favour of debt mortgages in the market.

Question 4

According to the view of Amir Sufi and Atif Mian, the main cause of the depression of 2007

is the debt contract that puts the unbalanced burden on the consumers or the borrowers of the

market (Sufi and Mian, 2019). Due to the debt mortgage and its current practices, the

mortgage balance and its instalment payment is constant irrespective of the price of the

property bought using the debt mortgage. In this case, the price of the property reduced

Question 3

Figure 2: securitizing the debt mortgages

(Source: Azzimonti and Yared, 2019)

By securitizing the debt mortgages the government has allowed Fannie Mae and Freddie Mac

to reduce the cost of operation. The figure shows the reduction in the cost of operation of the

companies from P1 to P0. However, the prices to the consumers of the market have increased

from P1 to P2 leading to an increase in the revenue of the company. In addition to that, the

securitization of the debt mortgages have also increased the surplus of the banks and reduced

the consumers' surplus (Yared and Azzimonti, 2017). Therefore, this way the government is

helping the banks at the cost of the consumers of the market. Thus, the government is tilting

the field in favour of debt mortgages in the market.

Question 4

According to the view of Amir Sufi and Atif Mian, the main cause of the depression of 2007

is the debt contract that puts the unbalanced burden on the consumers or the borrowers of the

market (Sufi and Mian, 2019). Due to the debt mortgage and its current practices, the

mortgage balance and its instalment payment is constant irrespective of the price of the

property bought using the debt mortgage. In this case, the price of the property reduced

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

keeping the balance and instalment same. As a result, the wealth of the consumers reduced

which reflected in the aggregate demand for goods and services in the market. With the

decline in the value of the property, the purchasing power of the consumers also decline and

consumers started demanding less of goods and services from the market (Yared and

Azzimonti, 2017). That means the aggregate demand curve shifted to the left side with

unchanged aggregate supply and hence the output of the economy reduced. Therefore,

according to, Amir Sufi and Atif Mian, the main reason for the economic downturn is the

reduction in the aggregate demand stemmed from the debt mortgages and its features.

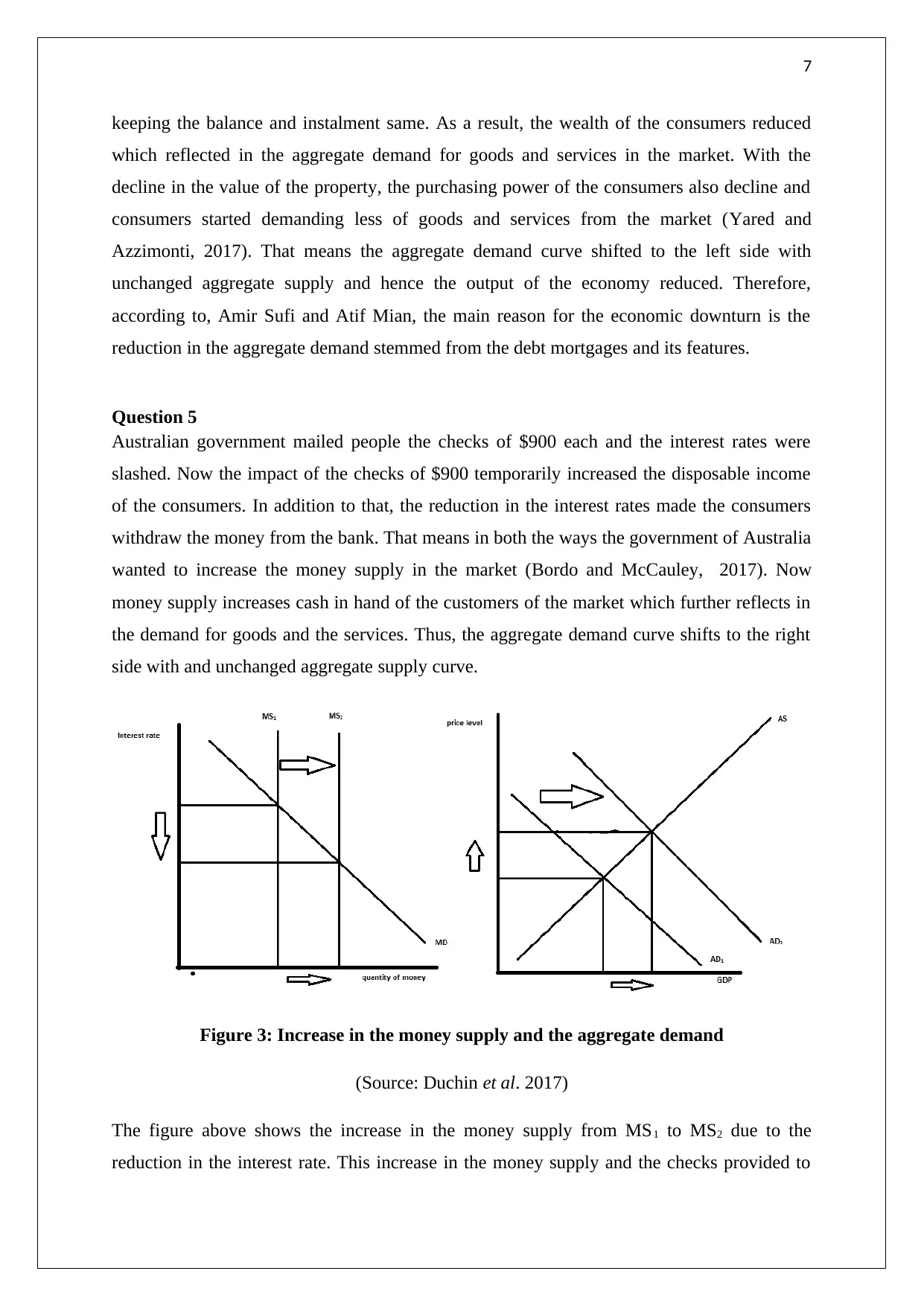

Question 5

Australian government mailed people the checks of $900 each and the interest rates were

slashed. Now the impact of the checks of $900 temporarily increased the disposable income

of the consumers. In addition to that, the reduction in the interest rates made the consumers

withdraw the money from the bank. That means in both the ways the government of Australia

wanted to increase the money supply in the market (Bordo and McCauley, 2017). Now

money supply increases cash in hand of the customers of the market which further reflects in

the demand for goods and the services. Thus, the aggregate demand curve shifts to the right

side with and unchanged aggregate supply curve.

Figure 3: Increase in the money supply and the aggregate demand

(Source: Duchin et al. 2017)

The figure above shows the increase in the money supply from MS1 to MS2 due to the

reduction in the interest rate. This increase in the money supply and the checks provided to

keeping the balance and instalment same. As a result, the wealth of the consumers reduced

which reflected in the aggregate demand for goods and services in the market. With the

decline in the value of the property, the purchasing power of the consumers also decline and

consumers started demanding less of goods and services from the market (Yared and

Azzimonti, 2017). That means the aggregate demand curve shifted to the left side with

unchanged aggregate supply and hence the output of the economy reduced. Therefore,

according to, Amir Sufi and Atif Mian, the main reason for the economic downturn is the

reduction in the aggregate demand stemmed from the debt mortgages and its features.

Question 5

Australian government mailed people the checks of $900 each and the interest rates were

slashed. Now the impact of the checks of $900 temporarily increased the disposable income

of the consumers. In addition to that, the reduction in the interest rates made the consumers

withdraw the money from the bank. That means in both the ways the government of Australia

wanted to increase the money supply in the market (Bordo and McCauley, 2017). Now

money supply increases cash in hand of the customers of the market which further reflects in

the demand for goods and the services. Thus, the aggregate demand curve shifts to the right

side with and unchanged aggregate supply curve.

Figure 3: Increase in the money supply and the aggregate demand

(Source: Duchin et al. 2017)

The figure above shows the increase in the money supply from MS1 to MS2 due to the

reduction in the interest rate. This increase in the money supply and the checks provided to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

the families would shift the aggregate demand curve to the right leading to an increased price

level and GDP.

Question 6

According to the articles of Hammad Siddiqi and Ricardo Caballero, the creation of the safe

debt will not prevent any upcoming economic downturn. The reason behind this is that safe

debt creations are not safe for the economy (Gourinchas and Rey, 2016). In the real world

when the banks sell risky loans to the financial companies, only a part of the so-called safe

debt is recovered. The articles also state that demand for safe debt or securitization is

increasing due to the innate nature of the human. However, this approach of the safe debt

creation converting the risky debts as safe debts was linked to the global financial crisis of

2007. He et al. (2019) stated that the safe debt creation or the securitization works as an

incentive to the customers of the market resulting in the creation of huge risky debt.

Therefore, the securitization of the shared responsibility mortgages is still vulnerable and can

give rise to an economic downturn as per the two articles.

Question 7

Caballero et al. (2016) stated that one of the main villains of the economic crisis of 2007 is

the imbalances in the economy. The demand for safe debt exposed the economy of the USA

and its national debt policies. Due to the securitization of the debt mortgages, the companies

were making a profit as shown in the above discussions. As a result, more and more

companies came to the market to meet the demand for securitized debt mortgages. To meet

the gap between the demands for safe debt the banks violated the regulations of debt creation

as well. At the same time, the government of the USA was also pursuing a policy that

ensured home for every citizen of the country. However, Nguyen and Liu (2017) stated that

more than the housing market it is the creation of the debt or the conversion of the risky debt

to "Safe" debt caused the imbalances in the economy.

Siddiqi (2019) stated that the companies sought to profit from the gaps of the market that

eventually pressurised the financial markets of the USA. The safe asset shortages provided

incentives to the sellers of the market to increase the supply. Therefore, forced creation of

risky debt and converting them to safe debts for the private benefits of the companies created

a panic situation in the financial market (Charles et al. 2016). To add to these imbalances in

demand and the supply and the urge for the private firm to capture the existing surplus from

the families would shift the aggregate demand curve to the right leading to an increased price

level and GDP.

Question 6

According to the articles of Hammad Siddiqi and Ricardo Caballero, the creation of the safe

debt will not prevent any upcoming economic downturn. The reason behind this is that safe

debt creations are not safe for the economy (Gourinchas and Rey, 2016). In the real world

when the banks sell risky loans to the financial companies, only a part of the so-called safe

debt is recovered. The articles also state that demand for safe debt or securitization is

increasing due to the innate nature of the human. However, this approach of the safe debt

creation converting the risky debts as safe debts was linked to the global financial crisis of

2007. He et al. (2019) stated that the safe debt creation or the securitization works as an

incentive to the customers of the market resulting in the creation of huge risky debt.

Therefore, the securitization of the shared responsibility mortgages is still vulnerable and can

give rise to an economic downturn as per the two articles.

Question 7

Caballero et al. (2016) stated that one of the main villains of the economic crisis of 2007 is

the imbalances in the economy. The demand for safe debt exposed the economy of the USA

and its national debt policies. Due to the securitization of the debt mortgages, the companies

were making a profit as shown in the above discussions. As a result, more and more

companies came to the market to meet the demand for securitized debt mortgages. To meet

the gap between the demands for safe debt the banks violated the regulations of debt creation

as well. At the same time, the government of the USA was also pursuing a policy that

ensured home for every citizen of the country. However, Nguyen and Liu (2017) stated that

more than the housing market it is the creation of the debt or the conversion of the risky debt

to "Safe" debt caused the imbalances in the economy.

Siddiqi (2019) stated that the companies sought to profit from the gaps of the market that

eventually pressurised the financial markets of the USA. The safe asset shortages provided

incentives to the sellers of the market to increase the supply. Therefore, forced creation of

risky debt and converting them to safe debts for the private benefits of the companies created

a panic situation in the financial market (Charles et al. 2016). To add to these imbalances in

demand and the supply and the urge for the private firm to capture the existing surplus from

9

the market, the inadequacy from the governing bodies and the authorities further made the

situations complex. According to Caballero (2018), the government bodies were the only

hope and option that could have absorbed the pressure stimulated from the excess demand for

safe assets. Nevertheless, the inactivity of the government and the false assumption of

complementing the government policies went in favour of private financial companies. It also

needs to be noted that the imbalances of the global market also plays a crucial role in the

creation of the securitized assets in the economy (Chen and Fik, 2017). The main reason for

the unexpected increase in demand for the safe asset is not only the higher demand for

housing in the US but also the expansion of the middle-class populations in the emerging

economies as well.

Adding to this complexion and irregularities in the financial market of the USA, the housing

bubble further worsened the situation that led to the financial crisis of 2007. The housing

bubble burst in the year 2007 leading to a devaluation of the properties that were bought from

the debt mortgages. As a result, not only the banks and the financial institutions faced severe

cash crunch the demand for other goods and services also plummeted. Feng and Wu (2015)

stated that the burden of mortgages increased after the housing bubble burst and hence

customers of the markets were left with a low level of disposable income. This low level of

disposable income further reduced the demand for the goods and the services in the market

leading to a leftward shift in the aggregate demand. This caused the low output level in the

economy and higher price level.

Conclusion and recommendations

Therefore, to sum up, it is the financial innovations at creating safe debt are the sole reason

for the economic downturn in the year 2007. This imbalances coupled with the housing

bubble is the main cause of the depression. The creation of the securitized debt mortgage led

to the creation of risky debt in the economy which manifested into a failure of the market

after the reduction in the price of properties in the early half of 2007. Therefore, the main

underlying reason for the economic crisis is the financial innovation and housing bubble burst

led to the amplification of the problem. Therefore, based on the finding of the paper it is

recommended to the government and authorities to increase monitoring in the financial

market so that private companies cannot capitalise on the market gap.

the market, the inadequacy from the governing bodies and the authorities further made the

situations complex. According to Caballero (2018), the government bodies were the only

hope and option that could have absorbed the pressure stimulated from the excess demand for

safe assets. Nevertheless, the inactivity of the government and the false assumption of

complementing the government policies went in favour of private financial companies. It also

needs to be noted that the imbalances of the global market also plays a crucial role in the

creation of the securitized assets in the economy (Chen and Fik, 2017). The main reason for

the unexpected increase in demand for the safe asset is not only the higher demand for

housing in the US but also the expansion of the middle-class populations in the emerging

economies as well.

Adding to this complexion and irregularities in the financial market of the USA, the housing

bubble further worsened the situation that led to the financial crisis of 2007. The housing

bubble burst in the year 2007 leading to a devaluation of the properties that were bought from

the debt mortgages. As a result, not only the banks and the financial institutions faced severe

cash crunch the demand for other goods and services also plummeted. Feng and Wu (2015)

stated that the burden of mortgages increased after the housing bubble burst and hence

customers of the markets were left with a low level of disposable income. This low level of

disposable income further reduced the demand for the goods and the services in the market

leading to a leftward shift in the aggregate demand. This caused the low output level in the

economy and higher price level.

Conclusion and recommendations

Therefore, to sum up, it is the financial innovations at creating safe debt are the sole reason

for the economic downturn in the year 2007. This imbalances coupled with the housing

bubble is the main cause of the depression. The creation of the securitized debt mortgage led

to the creation of risky debt in the economy which manifested into a failure of the market

after the reduction in the price of properties in the early half of 2007. Therefore, the main

underlying reason for the economic crisis is the financial innovation and housing bubble burst

led to the amplification of the problem. Therefore, based on the finding of the paper it is

recommended to the government and authorities to increase monitoring in the financial

market so that private companies cannot capitalise on the market gap.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Reference

Azzimonti, M. and Yared, P., 2019. The optimal public and private provision of safe

assets. Journal of Monetary Economics, 102, pp.126-144.

Bordo, M. and McCauley, R.N., 2017. A global shortage of safe assets: a new Triffin

dilemma?. Atlantic Economic Journal, 45(4), pp.443-451.

Caballero, R.J., 2018. Risk-centric macroeconomics and safe asset shortages in the global

economy: an illustration of mechanisms and policies. Available at SSRN 3253064.

Caballero, R.J., Farhi, E. and Gourinchas, P.O., 2016. Safe asset scarcity and aggregate

demand. American Economic Review, 106(5), pp.513-18.

Charles, K.K., Hurst, E. and Notowidigdo, M.J., 2016. The masking of the decline in

manufacturing employment by the housing bubble. Journal of Economic Perspectives, 30(2),

pp.179-200.

Chen, Y.H. and Fik, T., 2017. Housing-market bubble adjustment in coastal communities-A

spatial and temporal analysis of housing prices in Midwest Pinellas County, Florida. Applied

Geography, 80, pp.48-63.

Duchin, R., Gilbert, T., Harford, J. and Hrdlicka, C., 2017. Precautionary savings with risky

assets: When cash is not cash. The Journal of Finance, 72(2), pp.793-852.

Feng, Q. and Wu, G.L., 2015. Bubble or riddle? An asset-pricing approach evaluation on

China's housing market. Economic Modelling, 46, pp.376-383.

Gorton, G., 2017. The history and economics of safe assets. Annual Review of Economics, 9,

pp.547-586.

Gourinchas, P.O. and Rey, H., 2016. Real interest rates, imbalances and the curse of regional

safe asset providers at the zero lower bound (No. w22618). National Bureau of Economic

Research.

He, Z., Krishnamurthy, A. and Milbradt, K., 2016. What makes US government bonds safe

assets?. American Economic Review, 106(5), pp.519-23.

He, Z., Krishnamurthy, A. and Milbradt, K., 2019. A model of safe asset

determination. American Economic Review, 109(4), pp.1230-62.

Reference

Azzimonti, M. and Yared, P., 2019. The optimal public and private provision of safe

assets. Journal of Monetary Economics, 102, pp.126-144.

Bordo, M. and McCauley, R.N., 2017. A global shortage of safe assets: a new Triffin

dilemma?. Atlantic Economic Journal, 45(4), pp.443-451.

Caballero, R.J., 2018. Risk-centric macroeconomics and safe asset shortages in the global

economy: an illustration of mechanisms and policies. Available at SSRN 3253064.

Caballero, R.J., Farhi, E. and Gourinchas, P.O., 2016. Safe asset scarcity and aggregate

demand. American Economic Review, 106(5), pp.513-18.

Charles, K.K., Hurst, E. and Notowidigdo, M.J., 2016. The masking of the decline in

manufacturing employment by the housing bubble. Journal of Economic Perspectives, 30(2),

pp.179-200.

Chen, Y.H. and Fik, T., 2017. Housing-market bubble adjustment in coastal communities-A

spatial and temporal analysis of housing prices in Midwest Pinellas County, Florida. Applied

Geography, 80, pp.48-63.

Duchin, R., Gilbert, T., Harford, J. and Hrdlicka, C., 2017. Precautionary savings with risky

assets: When cash is not cash. The Journal of Finance, 72(2), pp.793-852.

Feng, Q. and Wu, G.L., 2015. Bubble or riddle? An asset-pricing approach evaluation on

China's housing market. Economic Modelling, 46, pp.376-383.

Gorton, G., 2017. The history and economics of safe assets. Annual Review of Economics, 9,

pp.547-586.

Gourinchas, P.O. and Rey, H., 2016. Real interest rates, imbalances and the curse of regional

safe asset providers at the zero lower bound (No. w22618). National Bureau of Economic

Research.

He, Z., Krishnamurthy, A. and Milbradt, K., 2016. What makes US government bonds safe

assets?. American Economic Review, 106(5), pp.519-23.

He, Z., Krishnamurthy, A. and Milbradt, K., 2019. A model of safe asset

determination. American Economic Review, 109(4), pp.1230-62.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Nguyen, P. and Liu, W.H., 2017. Time‐Varying Linkage of Possible Safe Haven Assets: A

Cross‐Market and Cross‐asset Analysis. International Review of Finance, 17(1), pp.43-76.

Siddiqi, H., (2019). How our addiction to safety could lead to another financial crisis.

[online] Available at: https://theconversation.com/how-our-addiction-to-safety-could-lead-to-

another-financial-crisis-71484 [Accessed 22 Sep. 2019].

Sufi, A and Mian A,. (2019). Shared responsibility mortgages - Equitable Growth. [online]

Available at: https://equitablegrowth.org/shared-responsibility-mortgages/ [Accessed 22 Sep.

2019].

Taillard, M., (2019). How to Make Securities Out of Just about Anything - dummies. [online]

Available at: https://www.dummies.com/business/accounting/auditing/how-to-make-

securities-out-of-just-about-anything/ [Accessed 22 Sep. 2019].

Wu, F., 2015. Commodification and housing market cycles in Chinese cities. International

Journal of Housing Policy, 15(1), pp.6-26.

Yared, P. and Azzimonti, M., 2017. The Public and Private Provision of Safe Assets. In 2017

Meeting Papers (No. 755). Society for Economic Dynamics.

Nguyen, P. and Liu, W.H., 2017. Time‐Varying Linkage of Possible Safe Haven Assets: A

Cross‐Market and Cross‐asset Analysis. International Review of Finance, 17(1), pp.43-76.

Siddiqi, H., (2019). How our addiction to safety could lead to another financial crisis.

[online] Available at: https://theconversation.com/how-our-addiction-to-safety-could-lead-to-

another-financial-crisis-71484 [Accessed 22 Sep. 2019].

Sufi, A and Mian A,. (2019). Shared responsibility mortgages - Equitable Growth. [online]

Available at: https://equitablegrowth.org/shared-responsibility-mortgages/ [Accessed 22 Sep.

2019].

Taillard, M., (2019). How to Make Securities Out of Just about Anything - dummies. [online]

Available at: https://www.dummies.com/business/accounting/auditing/how-to-make-

securities-out-of-just-about-anything/ [Accessed 22 Sep. 2019].

Wu, F., 2015. Commodification and housing market cycles in Chinese cities. International

Journal of Housing Policy, 15(1), pp.6-26.

Yared, P. and Azzimonti, M., 2017. The Public and Private Provision of Safe Assets. In 2017

Meeting Papers (No. 755). Society for Economic Dynamics.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.