GMAS Accounting Information System: Process Analysis & IT Use

VerifiedAdded on 2023/06/13

|10

|1608

|353

Report

AI Summary

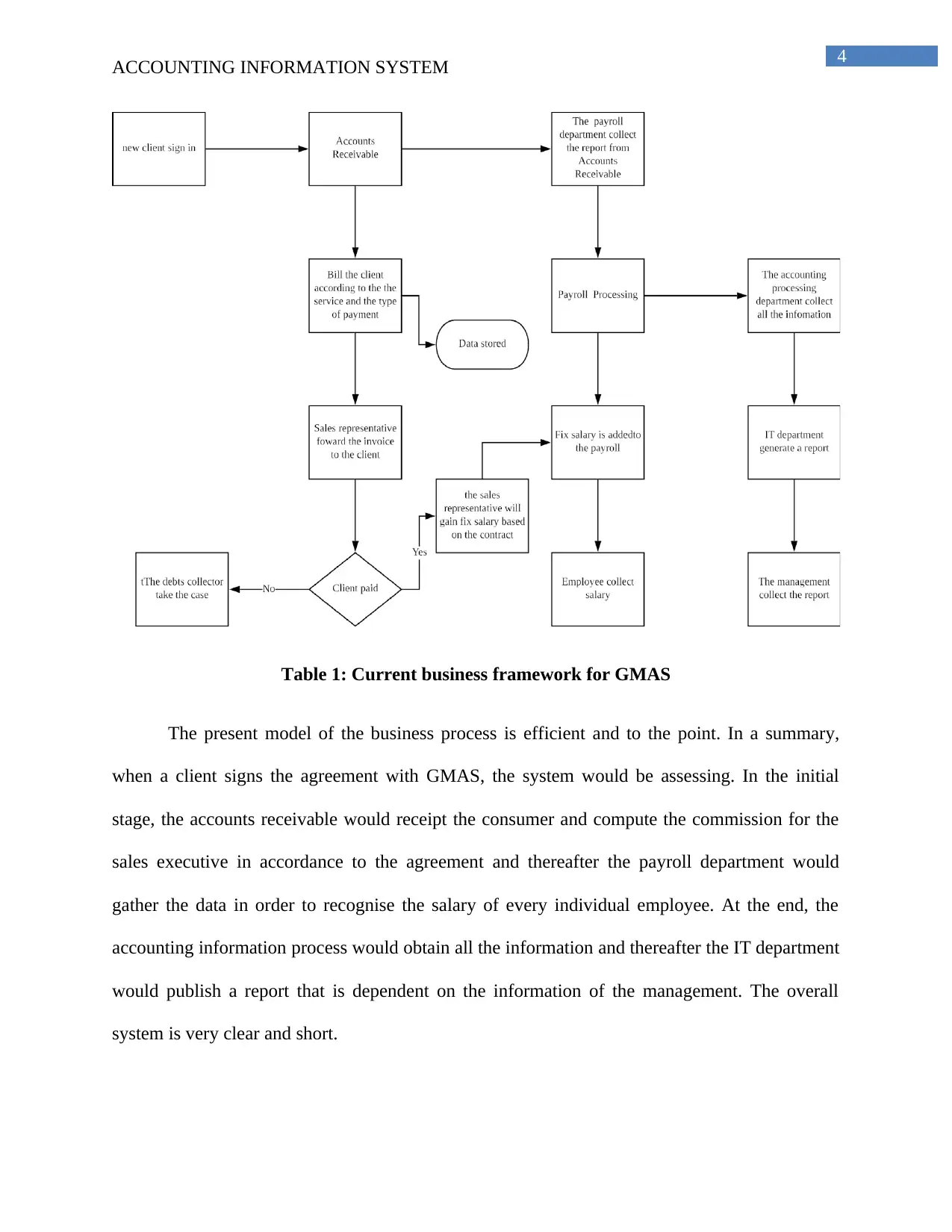

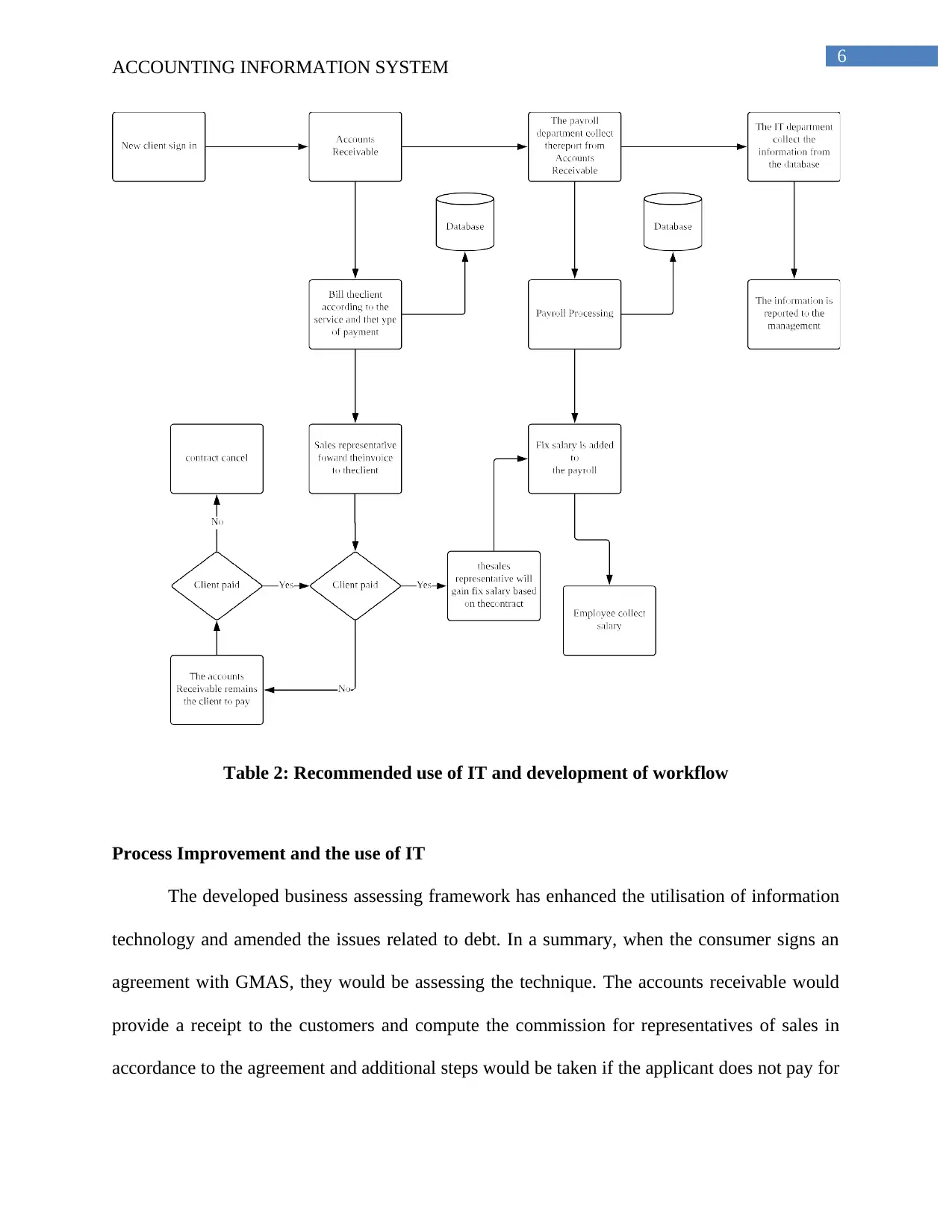

This report provides an analysis of an accounting information system within the context of GMAS, a company offering outsourced management accounting services. It begins by outlining the current business process framework, identifying key participants, inputs, and outputs. The report then delves into a problem analysis, highlighting inefficiencies related to third-party debt collection and the frequency of management reporting. To address these issues, the report proposes an improved business assessment framework that leverages information technology and streamlines the debt collection process. The recommended changes emphasize the use of a database to facilitate real-time information gathering and enhance the overall efficiency of the accounting system. The report concludes by referencing academic literature to support the analysis and proposed improvements.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.