Strategic Management: Financial Ratio Analysis of Car Companies

VerifiedAdded on 2022/12/05

|11

|1582

|232

Report

AI Summary

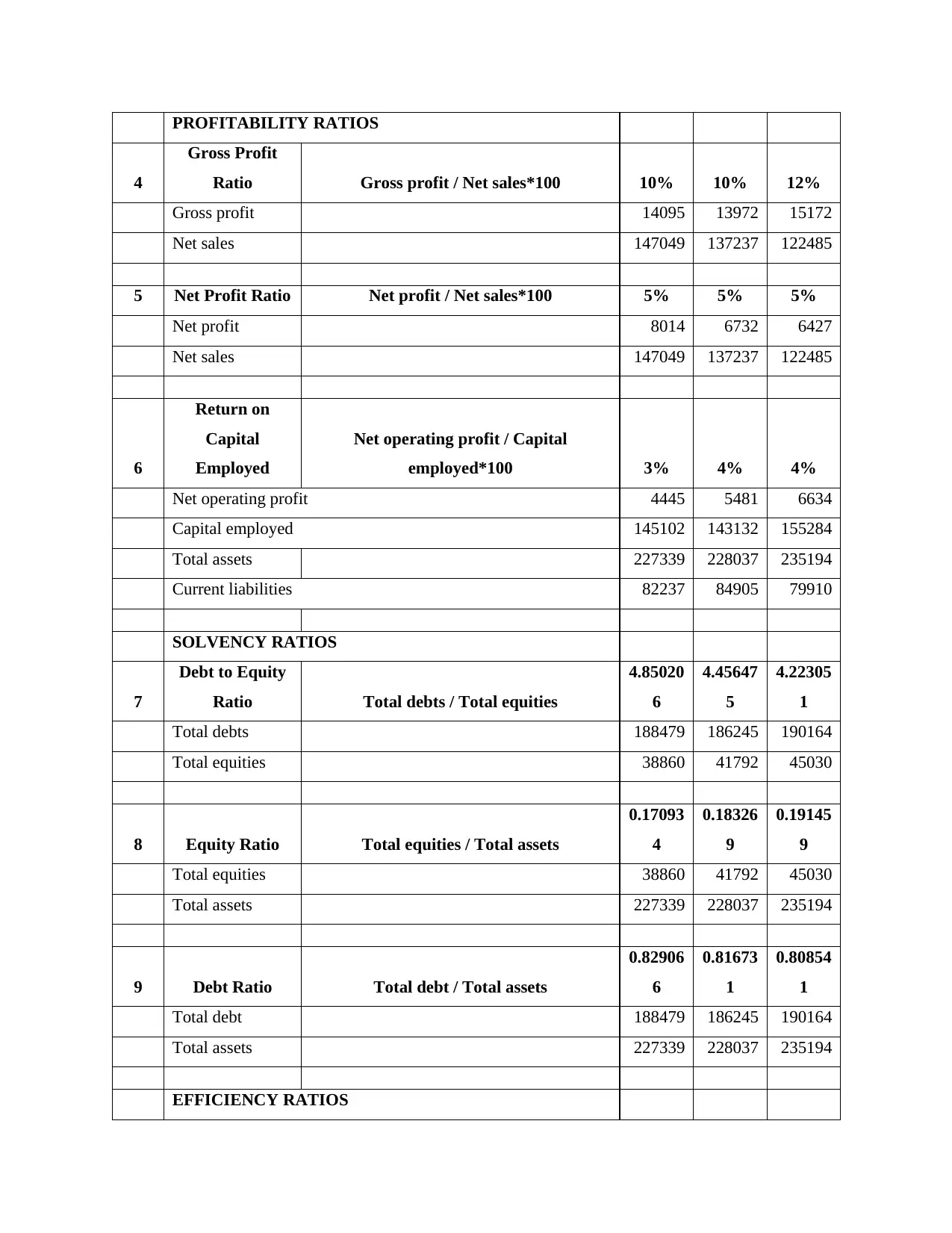

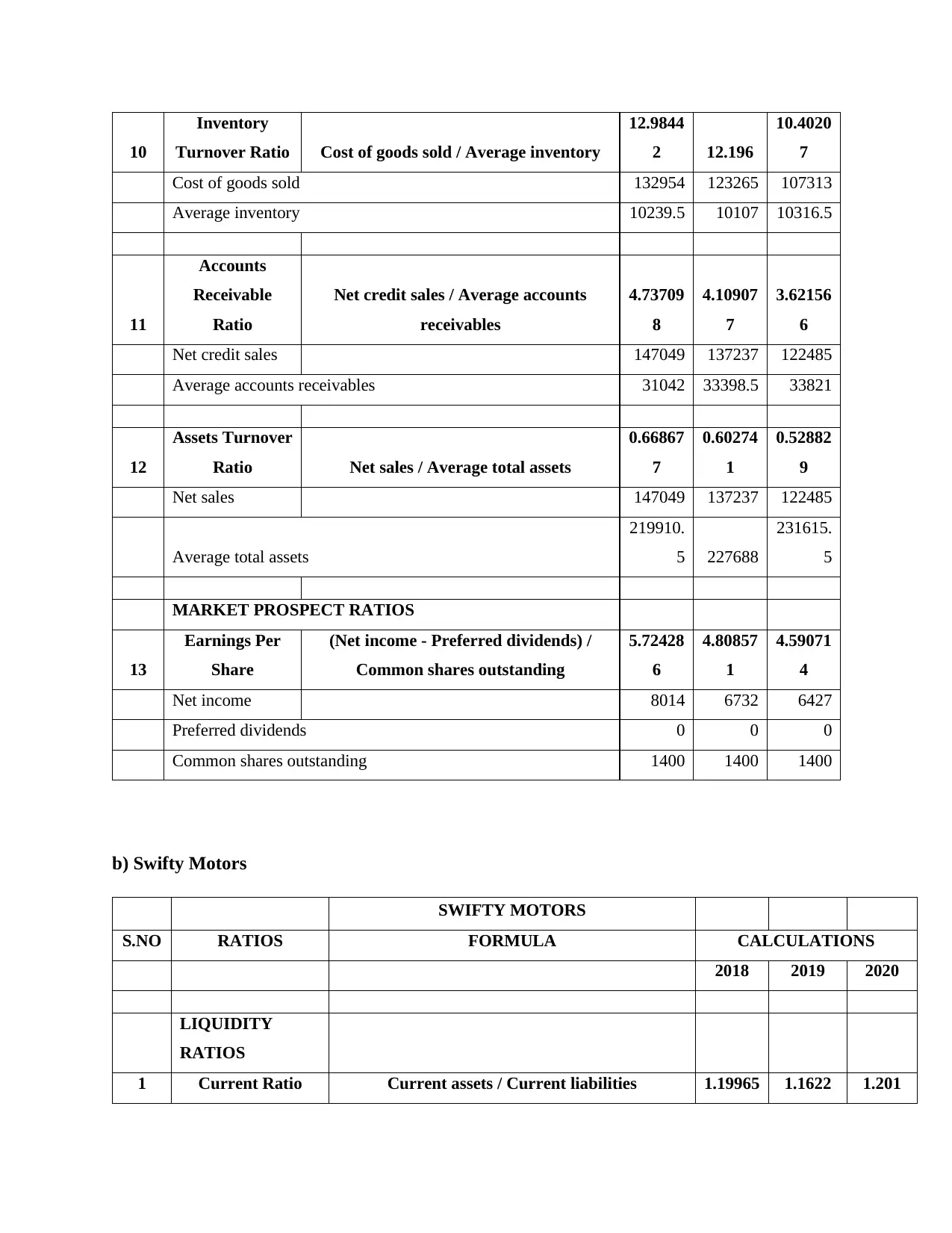

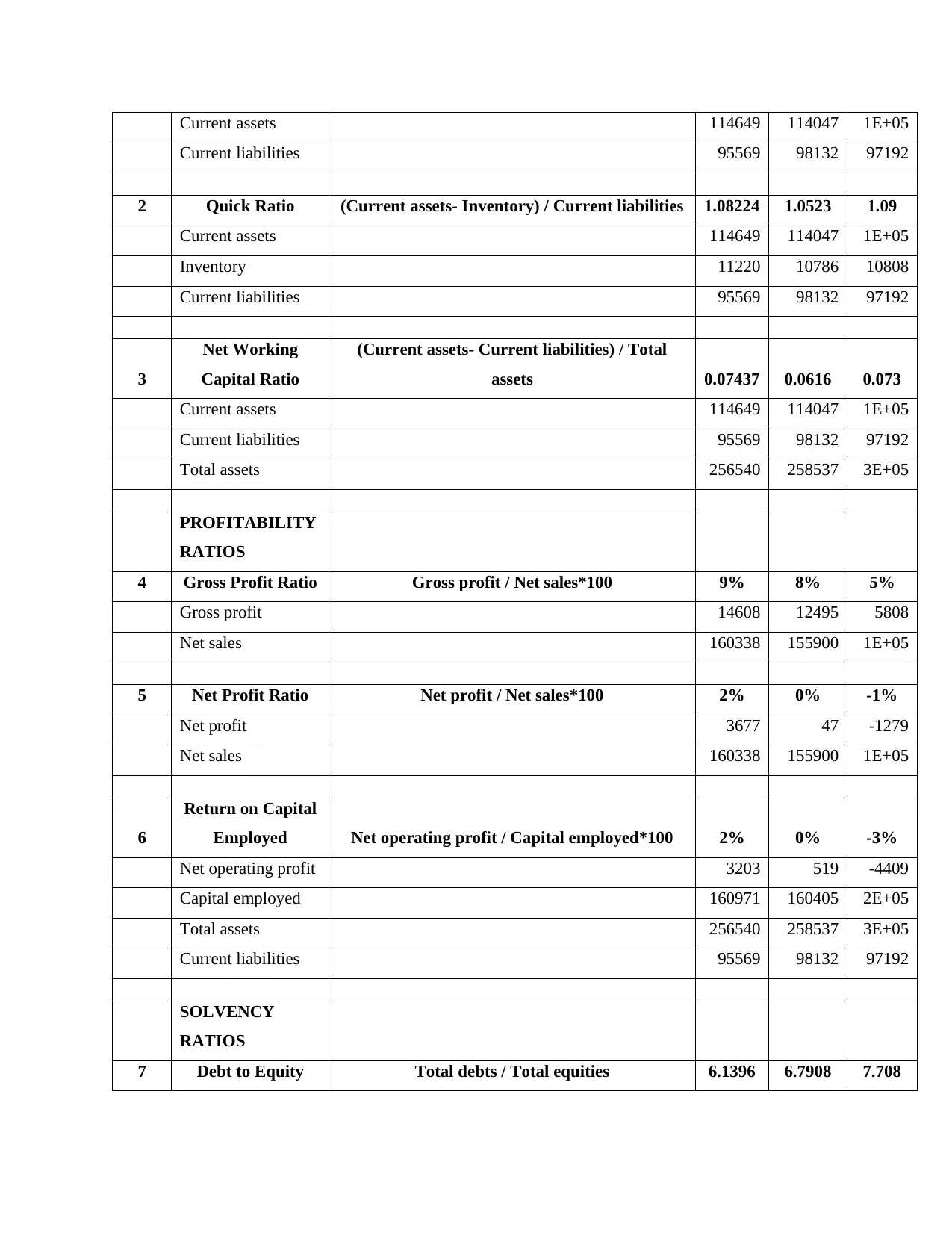

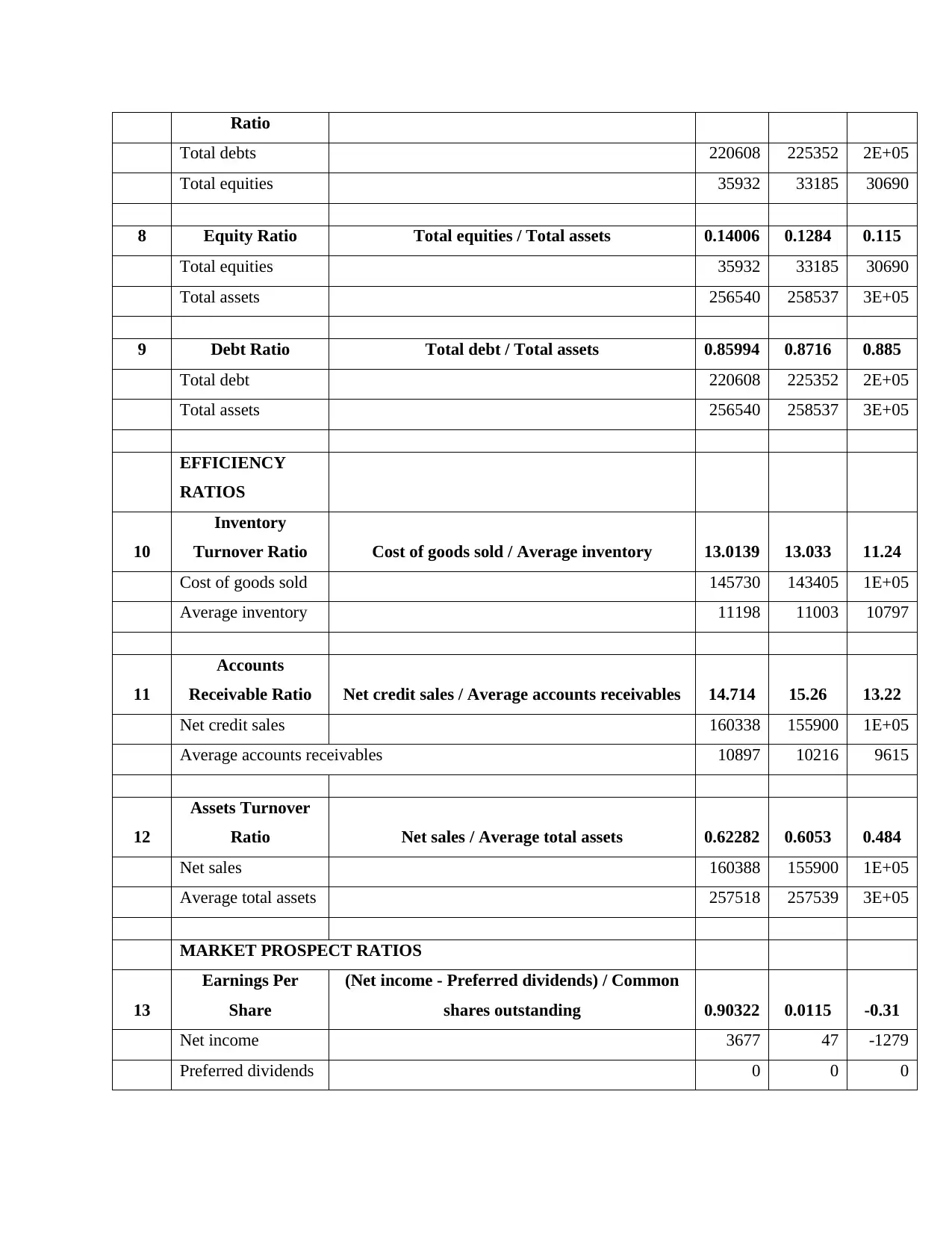

This report presents a comprehensive financial analysis comparing Gogo Motors and Swifty Motors, two fictional car companies. It begins with an introduction to ratio analysis and its importance in evaluating a company's financial health, covering liquidity, profitability, solvency, efficiency, and market prospect ratios. The main body of the report includes detailed calculations for each ratio, using financial data from 2018 to 2020. It offers interpretations of the results, highlighting the strengths and weaknesses of each company. Gogo Motors demonstrates stronger profitability, while Swifty Motors shows better efficiency in certain areas. The analysis concludes with investment suggestions, recommending Gogo Motors as a more profitable venture for potential investors due to its higher earnings per share. The report emphasizes the significance of ratio analysis in facilitating informed investment decisions and comparing business performance. The report utilizes the provided financial data to demonstrate quantitative numeracy skills, as required by the assignment brief.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.